Automotive Piston System Market

Automotive Piston System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709217 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

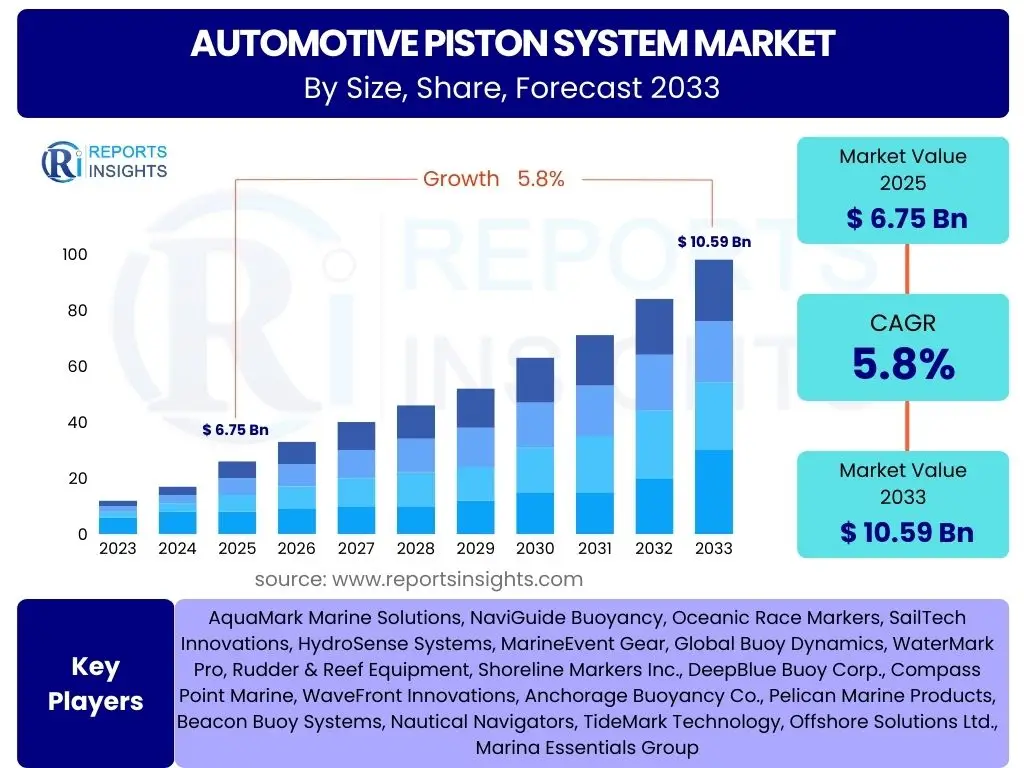

Automotive Piston System Market Size

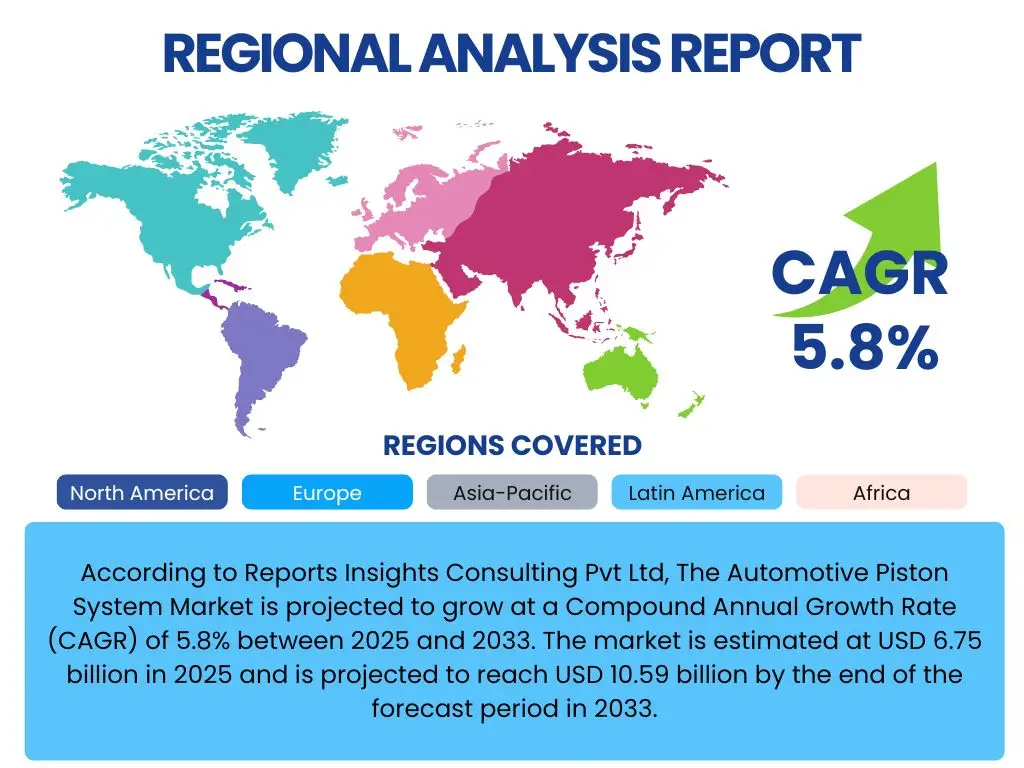

According to Reports Insights Consulting Pvt Ltd, The Automotive Piston System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 6.75 billion in 2025 and is projected to reach USD 10.59 billion by the end of the forecast period in 2033.

Key Automotive Piston System Market Trends & Insights

The Automotive Piston System market is currently undergoing significant transformation driven by evolving automotive industry standards and consumer demands. Common user inquiries often revolve around how advancements in engine technology, stringent environmental regulations, and the shift towards electric vehicles are influencing piston design, materials, and overall market dynamics. Users are keenly interested in understanding which technologies are gaining traction and how manufacturers are adapting to these changes to maintain performance while meeting new requirements. The market is witnessing a pronounced shift towards enhanced efficiency, durability, and reduced emissions, directly impacting the innovation trajectory for piston systems.

Furthermore, there is considerable interest in the global and regional disparities in market trends. Stakeholders frequently ask about the adoption rates of advanced piston technologies in different geographies, particularly focusing on emerging markets versus established automotive hubs. The influence of geopolitical factors, raw material costs, and supply chain resilience on market stability and growth is also a recurrent theme in user questions. The ongoing evolution of internal combustion engines (ICE) alongside the rise of hybrid electric vehicles (HEVs) ensures that piston systems remain a critical, albeit evolving, component within the automotive landscape.

- Engine Downsizing and Turbocharging: Trend towards smaller, more powerful engines requiring high-performance, durable pistons.

- Advanced Material Adoption: Increasing use of lightweight materials like aluminum alloys, steel, and composites for reduced weight and improved fuel efficiency.

- Enhanced Piston Ring Technologies: Development of low-friction, high-strength piston rings to minimize energy loss and emissions.

- Thermal Management Solutions: Integration of advanced cooling channels and coatings for improved heat dissipation and operational stability.

- Stricter Emission Regulations: Demand for piston systems that contribute to lower CO2 and NOx emissions.

- Hybrid Vehicle Integration: Design adaptations for piston systems in hybrid powertrains, optimizing for intermittent operation.

AI Impact Analysis on Automotive Piston System

User inquiries frequently explore the transformative potential of Artificial Intelligence (AI) across the automotive piston system lifecycle, from initial design to post-production performance monitoring. Common questions include how AI can accelerate material discovery for pistons, optimize manufacturing processes for greater precision and efficiency, and enable predictive maintenance strategies to extend engine life. Users are keenly interested in the practical applications of AI in simulating complex combustion dynamics, thereby enabling engineers to refine piston geometry and material composition for enhanced fuel efficiency and reduced emissions well before physical prototyping begins. The ability of AI to analyze vast datasets related to material properties, operational stresses, and failure modes is seen as a critical tool for driving innovation and problem-solving in this highly engineered component segment.

There is also considerable curiosity regarding AI's role in supply chain optimization and quality control for piston systems. Stakeholders often question how AI algorithms can predict demand fluctuations for specific piston types, manage inventory more effectively, and identify potential defects in manufacturing lines with greater accuracy than traditional methods. Furthermore, the long-term implications of AI on the skillset required within the piston manufacturing industry, including the potential for workforce reskilling and the emergence of new roles, are significant areas of user concern and expectation. The integration of AI is expected to lead to more robust, reliable, and environmentally friendly piston systems, aligning with the broader industry trend towards sustainable and intelligent manufacturing.

- Predictive Maintenance: AI algorithms analyze engine data to predict piston wear and potential failures, enabling proactive servicing.

- Generative Design and Optimization: AI aids in designing complex piston geometries for optimal performance, weight, and material usage.

- Manufacturing Process Optimization: AI-driven systems monitor and adjust production parameters for higher precision and reduced defects.

- Material Science Acceleration: AI expedites the discovery and development of novel lightweight and high-strength piston materials.

- Quality Control and Inspection: AI-powered vision systems enhance inspection accuracy, identifying microscopic flaws in pistons and rings.

- Supply Chain Efficiency: AI optimizes logistics and inventory management for piston component manufacturing and distribution.

Key Takeaways Automotive Piston System Market Size & Forecast

User queries regarding the Automotive Piston System market size and forecast consistently highlight a need for clarity on the primary growth drivers, the influence of evolving automotive technologies, and the impact of regional market dynamics. Stakeholders are particularly interested in understanding how the ongoing transition towards cleaner energy vehicles, including hybrid and electric models, will reshape the demand for conventional piston systems, even as internal combustion engines continue to dominate a significant portion of the global vehicle fleet for the foreseeable future. The continued focus on fuel efficiency and emission reduction remains a core determinant of market growth, driving innovation in piston material science and design.

A significant takeaway is that while the long-term outlook for purely internal combustion engine vehicles faces headwinds from electrification, the piston system market will demonstrate resilience through technological adaptation. This includes the development of highly optimized pistons for advanced gasoline direct injection (GDI) and diesel engines, as well as specialized designs for hybrid powertrains that face unique operational demands. Furthermore, the aftermarket segment is anticipated to play a crucial role, driven by the vast installed base of ICE vehicles globally, providing a stable revenue stream even as new vehicle production paradigms shift. Geographic expansion, particularly in emerging automotive markets, will also be a critical factor in achieving the projected growth figures, making regional analysis an indispensable component of market understanding.

- Steady Growth Trajectory: Despite electrification trends, the market projects consistent growth driven by advanced ICE and hybrid applications.

- Innovation-Driven Market: Continuous advancements in materials, coatings, and designs are crucial for meeting efficiency and emission standards.

- Hybrid Vehicle Influence: Piston systems are evolving to support the unique requirements of hybrid powertrains, ensuring continued relevance.

- Aftermarket Resilience: A substantial existing vehicle parc ensures sustained demand for replacement and upgrade piston systems.

- Regional Market Divergence: Growth rates and technology adoption vary significantly across North America, Europe, Asia Pacific, and other regions.

Automotive Piston System Market Drivers Analysis

The Automotive Piston System market is primarily driven by several critical factors centered around global environmental concerns, regulatory frameworks, and technological advancements within the automotive industry. A key driver is the increasing demand for fuel-efficient vehicles, which necessitates the development of lighter, more durable, and friction-optimized piston systems. Manufacturers are continually investing in research and development to create pistons that can withstand higher operating pressures and temperatures while contributing to lower overall vehicle weight, directly translating to improved fuel economy and reduced carbon emissions. This ongoing push for efficiency is a constant impetus for innovation across the piston system value chain.

Furthermore, the stringent emission regulations imposed by governments worldwide, such as Euro 6/7, CAFE standards, and China VI, are forcing automotive manufacturers to adopt advanced engine technologies that rely on highly optimized piston systems. These regulations mandate significant reductions in particulate matter and nitrogen oxides, compelling piston designers to innovate in areas such as combustion chamber geometry, piston ring design, and piston cooling mechanisms. The global increase in vehicle production, particularly in emerging economies, also acts as a foundational driver, expanding the overall market volume for both original equipment manufacturing (OEM) and aftermarket components. Lastly, the rise of hybrid electric vehicles (HEVs) presents a unique driver, requiring pistons optimized for stop-start operation and varying load conditions, ensuring their continued relevance in the evolving powertrain landscape.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stricter Emission Norms & Fuel Efficiency Standards | +1.5% | Global, especially EU, North America, APAC (China, India) | Short to Medium Term (2025-2029) |

| Increasing Global Vehicle Production & Sales | +1.2% | APAC, Latin America, Middle East & Africa | Medium to Long Term (2027-2033) |

| Advancements in Engine Technologies (e.g., Turbocharging, GDI) | +0.8% | Global | Short to Medium Term (2025-2030) |

| Growing Demand for Lightweight & High-Performance Pistons | +0.7% | North America, Europe, APAC | Medium Term (2026-2031) |

Automotive Piston System Market Restraints Analysis

While the Automotive Piston System market exhibits robust growth potential, several factors act as significant restraints, limiting its overall expansion. A primary concern is the accelerating global shift towards electric vehicles (EVs), which inherently do not require traditional piston systems. As governments and automotive manufacturers commit increasingly to electrification goals, the long-term demand for internal combustion engine (ICE) components, including pistons, is projected to decline. This paradigm shift poses a fundamental challenge to the market, forcing manufacturers to diversify or innovate into new areas. The pace of EV adoption, particularly in developed regions, will directly influence the severity of this restraint.

Another notable restraint involves the volatile costs of raw materials, such as aluminum, steel, and specialized alloys, which are crucial for piston manufacturing. Fluctuations in commodity prices, driven by global supply chain disruptions, geopolitical tensions, and trade policies, can significantly impact production costs and profit margins for piston system manufacturers. This unpredictability makes long-term planning and pricing strategies challenging, potentially leading to increased manufacturing costs that are difficult to pass on to consumers or OEMs. Furthermore, the high capital investment required for advanced manufacturing processes and research and development into new materials also presents a barrier, especially for smaller players in the market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Accelerated Adoption of Electric Vehicles (EVs) | -1.8% | Global, especially Europe, North America, China | Medium to Long Term (2028-2033) |

| Volatile Raw Material Prices (Aluminum, Steel Alloys) | -0.9% | Global | Short to Medium Term (2025-2029) |

| High Research & Development Costs for Advanced Piston Systems | -0.5% | Global | Short to Medium Term (2025-2030) |

Automotive Piston System Market Opportunities Analysis

Despite existing restraints, the Automotive Piston System market presents several compelling opportunities for growth and innovation. A significant opportunity lies in the continuous development and adoption of advanced piston materials and coating technologies. As engine performance demands increase and emission standards become more stringent, there is a growing need for pistons that can withstand extreme conditions, offer superior friction reduction, and are lighter in weight. This creates a fertile ground for materials science innovation, including composites, advanced aluminum alloys, and specialized surface treatments, enabling manufacturers to offer premium, high-performance solutions that command better margins and meet evolving OEM specifications. Investing in these areas can unlock new market segments and solidify competitive positions.

Another key opportunity is the expanding aftermarket for automotive components, particularly in regions with a large installed base of older internal combustion engine vehicles. As these vehicles age, there is a consistent demand for replacement pistons and related components for maintenance and repair. This aftermarket segment is less susceptible to the immediate impacts of electrification trends and offers stable, long-term revenue streams. Furthermore, the burgeoning market for hybrid electric vehicles (HEVs) and plug-in hybrid electric vehicles (PHEVs) also presents a unique opportunity. These vehicles still utilize ICEs, but often with specific operational requirements (e.g., frequent stop-start cycles), necessitating specially designed piston systems that are optimized for these intermittent operations, thereby creating a new niche for specialized piston product lines. Lastly, geographical expansion into rapidly industrializing economies, where vehicle ownership is on the rise, offers significant growth prospects.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Materials & Surface Coatings | +1.0% | Global, especially high-tech automotive hubs | Medium to Long Term (2027-2033) |

| Growth in the Automotive Aftermarket Segment | +0.9% | Global, particularly developing economies | Long Term (2029-2033) |

| Increasing Demand for Hybrid Electric Vehicle Piston Systems | +0.8% | Europe, North America, APAC (Japan, South Korea) | Medium Term (2026-2032) |

Automotive Piston System Market Challenges Impact Analysis

The Automotive Piston System market faces a range of significant challenges that could impede its growth and evolution. One of the primary challenges is the increasing complexity of engine designs, driven by the need to meet conflicting demands for higher performance, better fuel efficiency, and lower emissions. This requires piston systems to operate under increasingly extreme conditions – higher combustion pressures, elevated temperatures, and faster engine speeds – while maintaining durability and reliability. Designing and manufacturing pistons that can withstand these stresses, often within tighter packaging constraints, demands substantial engineering expertise and investment, leading to higher development costs and longer lead times for new product introduction.

Another critical challenge stems from the intense competitive landscape and the pressure on pricing. The automotive supply chain is highly competitive, with OEMs consistently seeking cost reductions from their suppliers. This puts immense pressure on piston system manufacturers to optimize their production processes, achieve economies of scale, and innovate efficiently to remain competitive without compromising on quality or performance. Furthermore, the rapid pace of technological change, including advancements in engine control units (ECUs) and alternative powertrain technologies, requires continuous adaptation and investment in new production capabilities, posing a financial burden and risk of technological obsolescence. Navigating these complexities while maintaining profitability represents a formidable hurdle for market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technological Complexity & High R&D Investment | -0.7% | Global | Short to Medium Term (2025-2030) |

| Intense Price Competition & Cost Pressure from OEMs | -0.6% | Global | Short Term (2025-2028) |

| Managing Supply Chain Disruptions & Material Sourcing | -0.4% | Global | Short to Medium Term (2025-2029) |

Automotive Piston System Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Automotive Piston System market, covering key market dynamics, technological advancements, competitive landscape, and future growth prospects. It segments the market by various criteria, offering granular insights into demand and supply trends across different regions and product types. The report aims to equip stakeholders with actionable intelligence to make informed strategic decisions in this evolving automotive component sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.75 Billion |

| Market Forecast in 2033 | USD 10.59 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Mahle GmbH, Federal-Mogul LLC (Tenneco), Rheinmetall Automotive AG (Kolbenschmidt Pierburg), Aisin Corporation, Art Metal Mfg. Co. Ltd., Kubota Corporation, Shriram Pistons & Rings Ltd., TP Manufacturing Co. Ltd., Capricorn Automotive GmbH, Ross Racing Pistons, JE Pistons, Wiseco Piston Inc., CP-Carrillo, Arias Pistons, Wossner Piston Inc., PowerMax Piston Rings, Nippon Piston Ring Co. Ltd., Riken Corporation, Honda Foundry Co. Ltd., Hitachi Astemo Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Piston System market is comprehensively segmented to provide a detailed understanding of its various facets, enabling stakeholders to identify key growth areas and niche opportunities. This segmentation considers different components of the piston system, the materials used in their construction, the engine types they serve, the vehicle types they are installed in, and the channels through which they are sold. Each segment provides unique insights into demand patterns, technological preferences, and market penetration, illustrating the diverse landscape of the industry.

- By Component

- Piston

- Piston Ring

- Piston Pin

- Cylinder Liner

- By Material

- Aluminum Alloy

- Steel

- Cast Iron

- Composites

- By Engine Type

- Gasoline Engine

- Diesel Engine

- Hybrid Engine

- By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- By Sales Channel

- Original Equipment Manufacturer (OEM)

- Aftermarket

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to high vehicle production volumes, rapid industrialization, increasing disposable income, and the presence of major automotive manufacturing hubs, particularly in China, India, Japan, and South Korea. This region is a hotbed for both OEM supply and a burgeoning aftermarket.

- Europe: A significant market driven by stringent emission regulations and a strong emphasis on fuel efficiency, fostering innovation in advanced piston materials and designs. Countries like Germany, France, and the UK are leading in the development and adoption of high-performance piston systems for both conventional and hybrid powertrains.

- North America: Characterized by a robust automotive industry with a focus on larger engine capacities and increasing demand for pickup trucks and SUVs. The region also exhibits a strong aftermarket segment and is actively adopting advanced engine technologies to meet evolving fuel economy standards.

- Latin America: An emerging market experiencing consistent growth in vehicle production and sales, particularly in Brazil and Mexico. This region presents opportunities for both OEM and aftermarket suppliers, though economic volatility can influence market stability.

- Middle East and Africa (MEA): Shows steady growth driven by expanding vehicle fleets, urbanization, and investments in infrastructure. The region relies heavily on vehicle imports and also possesses a growing aftermarket segment for automotive components.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Piston System Market.- Mahle GmbH

- Federal-Mogul LLC (Tenneco)

- Rheinmetall Automotive AG (Kolbenschmidt Pierburg)

- Aisin Corporation

- Art Metal Mfg. Co. Ltd.

- Kubota Corporation

- Shriram Pistons & Rings Ltd.

- TP Manufacturing Co. Ltd.

- Capricorn Automotive GmbH

- Ross Racing Pistons

- JE Pistons

- Wiseco Piston Inc.

- CP-Carrillo

- Arias Pistons

- Wossner Piston Inc.

- PowerMax Piston Rings

- Nippon Piston Ring Co. Ltd.

- Riken Corporation

- Honda Foundry Co. Ltd.

- Hitachi Astemo Ltd.

Frequently Asked Questions

What is the projected growth rate for the Automotive Piston System Market?

The Automotive Piston System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, reaching an estimated USD 10.59 billion by 2033 from USD 6.75 billion in 2025.

How do emission regulations impact the Automotive Piston System Market?

Stringent global emission regulations drive demand for advanced piston systems that reduce CO2 and NOx emissions, leading to innovations in lightweight materials, low-friction designs, and optimized combustion chamber geometries for improved fuel efficiency and environmental compliance.

What role does Artificial Intelligence (AI) play in the Automotive Piston System industry?

AI is increasingly utilized for generative design and optimization of piston geometries, accelerating material discovery, enhancing manufacturing precision and quality control, and enabling predictive maintenance strategies to extend the lifespan of piston systems.

Which regions are key contributors to the Automotive Piston System Market's growth?

Asia Pacific is the leading region due to high vehicle production and industrialization, followed by Europe and North America, driven by technological innovation and the demand for advanced, fuel-efficient piston systems.

How does the rise of Electric Vehicles (EVs) affect the Automotive Piston System Market?

While the long-term adoption of EVs poses a restraint on the conventional piston market, the market adapts by focusing on highly optimized pistons for advanced gasoline, diesel, and hybrid powertrains, ensuring continued relevance in the evolving automotive landscape.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted