Automotive Pipe Market

Automotive Pipe Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703105 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

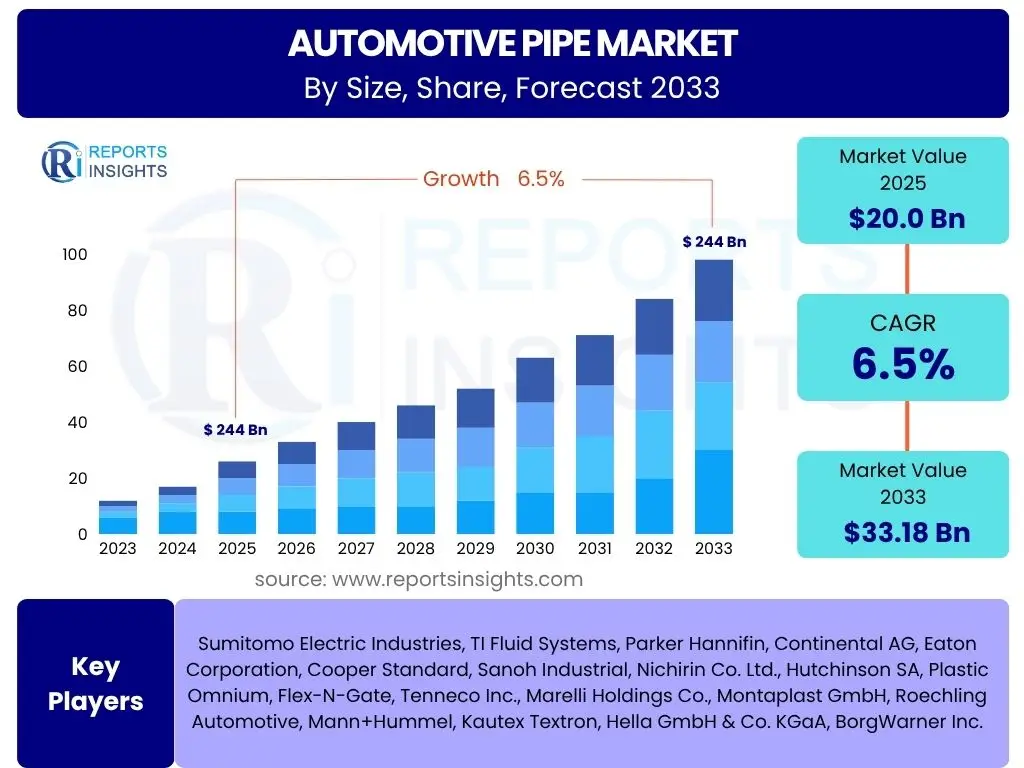

Automotive Pipe Market Size

According to Reports Insights Consulting Pvt Ltd, The Automotive Pipe Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 20.0 billion in 2025 and is projected to reach USD 33.18 billion by the end of the forecast period in 2033.

Key Automotive Pipe Market Trends & Insights

The automotive pipe market is currently undergoing significant transformations, driven by evolving vehicle technologies, stringent environmental regulations, and a heightened focus on vehicle performance and safety. Key trends indicate a decisive shift towards lighter materials, enabling fuel efficiency and reduced emissions, which are critical for meeting global environmental mandates. Furthermore, the burgeoning electric vehicle (EV) segment is creating new demands for specialized cooling and thermal management pipes, distinctly different from traditional internal combustion engine (ICE) vehicle requirements. This necessitates innovation in material science and manufacturing processes to accommodate unique thermal properties and pressure demands.

Another prominent trend is the integration of advanced manufacturing techniques, such as additive manufacturing (3D printing) for prototyping and specialized components, alongside increased automation and digitalization in production lines. This enhances precision, reduces waste, and accelerates product development cycles. The market also observes a growing emphasis on modular and standardized pipe assemblies to streamline vehicle assembly processes and reduce overall manufacturing complexity. This approach not only improves efficiency but also facilitates easier maintenance and replacement in the aftermarket, contributing to vehicle longevity and owner satisfaction.

Moreover, the focus on sustainable practices throughout the supply chain is gaining traction, with an increased preference for recyclable materials and energy-efficient production methods. This aligns with broader corporate sustainability goals and consumer demand for environmentally responsible products. The development of intelligent piping systems, equipped with sensors for real-time monitoring of fluid pressure, temperature, and flow, represents an emerging trend that will contribute to predictive maintenance and enhanced vehicle diagnostics, further elevating the functional sophistication of automotive pipes.

- Lightweighting initiatives through advanced materials like high-strength steel, aluminum, and composites.

- Increased demand for specialized thermal management pipes in Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs).

- Adoption of advanced manufacturing processes, including additive manufacturing and automation.

- Growing emphasis on modular designs and pre-assembled pipe modules for simplified integration.

- Development of smart piping systems with integrated sensors for real-time monitoring and diagnostics.

- Sustainability focus, promoting recyclable materials and eco-friendly production methods.

AI Impact Analysis on Automotive Pipe

Artificial Intelligence (AI) is set to significantly revolutionize various facets of the automotive pipe market, from design and manufacturing to quality control and supply chain management. Common user questions often revolve around how AI can enhance efficiency, reduce costs, and improve product reliability. In design, AI algorithms can optimize pipe geometries for better flow dynamics, thermal performance, and material usage, leading to more efficient and durable components. This includes predictive modeling for stress analysis and fatigue life, accelerating the research and development cycle by simulating diverse operating conditions without extensive physical prototyping.

In manufacturing, AI-driven solutions are being deployed for predictive maintenance of machinery, minimizing downtime and optimizing production schedules by forecasting equipment failures before they occur. AI-powered vision systems are enhancing quality control by performing rapid and precise inspections of welds, material defects, and dimensional accuracy, far surpassing human capabilities. Furthermore, AI contributes to optimizing manufacturing processes by analyzing vast datasets from production lines, identifying inefficiencies, and suggesting improvements in parameters such as temperature, pressure, and flow rates to achieve higher yields and consistent quality.

Supply chain optimization is another critical area where AI can deliver substantial impact. By analyzing historical data, market trends, and geopolitical factors, AI can provide accurate forecasts for raw material demand, optimize inventory levels, and identify potential disruptions, thus enhancing supply chain resilience and reducing lead times. The integration of AI in robotics for automated assembly and handling of pipes will also improve precision, speed, and safety on the factory floor, driving down labor costs and boosting overall operational efficiency within the automotive pipe manufacturing ecosystem.

- Optimized design and simulation for pipe geometry, material selection, and thermal performance.

- Predictive maintenance for manufacturing equipment, reducing downtime and operational costs.

- Enhanced quality control through AI-powered vision systems for defect detection.

- Process optimization in manufacturing to improve yield, consistency, and resource utilization.

- Intelligent supply chain management for demand forecasting, inventory optimization, and risk mitigation.

Key Takeaways Automotive Pipe Market Size & Forecast

The automotive pipe market is poised for robust growth, reflecting the dynamic shifts within the global automotive industry. A significant takeaway is the consistent demand driven by both the production of new vehicles, including a rapidly expanding electric vehicle segment, and the ongoing requirements of the aftermarket for repairs and replacements. The forecast highlights a substantial increase in market valuation, underscoring the indispensable role of various piping systems in modern vehicles, from essential fluid transfer to complex thermal management. This growth is underpinned by continuous innovation in material science and manufacturing processes, aimed at improving performance, durability, and compliance with increasingly stringent regulatory standards.

A crucial insight is the dual impact of evolving regulations and technological advancements. Stricter emission norms are compelling manufacturers to adopt lightweight and more efficient piping solutions for internal combustion engines, while the electrification trend is spurring demand for specialized, high-performance pipes for battery cooling, HVAC, and power electronics. This diversification in application is a key factor sustaining market expansion. Furthermore, the increasing complexity of vehicle architectures means that reliable and advanced piping systems are becoming even more critical for overall vehicle functionality, safety, and efficiency, cementing their position as foundational components.

The market's resilience is also attributed to geographical diversification, with emerging economies in Asia Pacific and Latin America offering significant growth opportunities due to rising vehicle production and increasing disposable incomes. Concurrently, established markets in North America and Europe continue to drive demand through technological upgrades, vehicle replacement cycles, and the rapid adoption of electric vehicles. This global outlook, coupled with persistent innovation in materials and manufacturing, ensures a positive trajectory for the automotive pipe market, making it a critical area for investment and technological development within the automotive supply chain.

- Projected robust growth trajectory driven by new vehicle production and aftermarket demand.

- Significant market value increase by 2033, emphasizing the essential nature of piping systems.

- Demand fueled by stringent emission regulations and the rapid transition to electric vehicles (EVs).

- Innovation in lightweight materials and advanced manufacturing critical for future growth.

- Strong growth opportunities in emerging markets alongside sustained demand in developed regions.

Automotive Pipe Market Drivers Analysis

The automotive pipe market is primarily driven by the escalating global vehicle production, encompassing traditional internal combustion engine vehicles, and, more significantly, the rapid expansion of the electric vehicle segment. As automotive manufacturers continue to innovate and expand their portfolios, the demand for high-performance and specialized piping systems across various applications—such as fuel lines, brake lines, air conditioning systems, and thermal management—naturally increases. This growth is further propelled by the continuous evolution of vehicle architectures, which integrate more complex fluid transfer systems and require durable, efficient, and lightweight pipe solutions.

Stringent emission regulations globally are a significant catalyst for market growth, pushing manufacturers to adopt advanced materials and designs that contribute to vehicle lightweighting and improved fuel efficiency. This includes the use of materials like high-strength steel, aluminum, and advanced plastics, which reduce overall vehicle weight and thereby lower emissions. Furthermore, the increasing adoption of electric and hybrid vehicles necessitates entirely new types of piping for battery thermal management, power electronics cooling, and cabin heating/cooling, creating novel demand streams that traditional vehicles did not require, thereby diversifying the market's growth avenues and fostering innovation in pipe technology.

Technological advancements in manufacturing processes, such as precision welding, hydroforming, and additive manufacturing, also act as key drivers. These innovations enable the production of more complex geometries, tighter tolerances, and improved structural integrity, enhancing the performance and reliability of automotive pipes. Moreover, the growing emphasis on vehicle safety and reliability compels automakers to use higher quality and more robust piping systems, which are essential for critical functions like braking and fuel delivery, further stimulating demand for premium and technologically advanced pipe solutions across all vehicle segments.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Vehicle Production | +1.8% | Global, particularly Asia Pacific (China, India) | 2025-2033 |

| Rising Demand for Electric Vehicles (EVs) | +1.5% | North America, Europe, Asia Pacific (China) | 2025-2033 |

| Stringent Emission and Fuel Economy Regulations | +1.2% | Europe, North America, Asia Pacific (Japan, South Korea) | 2025-2030 |

| Technological Advancements in Materials & Manufacturing | +1.0% | Global, especially developed markets | 2025-2033 |

| Growing Focus on Vehicle Safety and Performance | +0.8% | Global | 2025-2033 |

Automotive Pipe Market Restraints Analysis

Despite the positive growth trajectory, the automotive pipe market faces several significant restraints that could impede its expansion. One primary concern is the volatility in raw material prices, particularly for metals like steel, aluminum, and copper, as well as polymers and rubbers. Fluctuations in commodity markets, driven by geopolitical events, supply chain disruptions, or changes in mining and production capacities, directly impact the manufacturing costs of pipes. These unpredictable price movements can compress profit margins for pipe manufacturers and lead to higher end-product costs for automakers, potentially slowing down adoption of new technologies or shifting material preferences.

Another significant restraint is the increasing complexity of vehicle design and the integration of diverse technologies. As vehicles become more sophisticated with advanced driver-assistance systems (ADAS), infotainment, and complex thermal management for electric powertrains, the available space for traditional piping systems becomes constrained. This necessitates highly specialized, custom-designed pipes that are challenging and costly to produce, leading to longer development cycles and potentially higher unit costs. Furthermore, the integration of multiple systems within a limited space demands exceptional durability and reliability from pipes, increasing the risk of failure if design or manufacturing tolerances are not precisely met, which can incur significant warranty costs for manufacturers.

Moreover, intense competition within the automotive component manufacturing sector, coupled with pricing pressures from major OEMs, consistently challenges the profitability of pipe suppliers. OEMs often demand cost reductions year over year, forcing manufacturers to continuously optimize their production processes and material sourcing. This pressure can stifle investment in research and development for new pipe technologies, especially for smaller players. Additionally, the transition towards electric vehicles, while creating new opportunities, also poses a restraint for manufacturers heavily invested in legacy ICE-related piping, requiring substantial retooling and strategic shifts that entail significant capital expenditure and risk.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -1.0% | Global | 2025-2033 |

| Intense Market Competition & Pricing Pressure | -0.7% | Global | 2025-2033 |

| Complexity of Vehicle Integration and Miniaturization | -0.6% | Developed Markets | 2025-2030 |

| Supply Chain Disruptions & Geopolitical Instability | -0.5% | Global | Short to Medium Term (2025-2028) |

Automotive Pipe Market Opportunities Analysis

The burgeoning global shift towards electric vehicles (EVs) presents a transformative opportunity for the automotive pipe market. Unlike traditional internal combustion engines, EVs require sophisticated thermal management systems for batteries, power electronics, and electric motors to ensure optimal performance, longevity, and safety. This necessitates the development and production of entirely new types of pipes and hose assemblies designed to handle varying temperatures, pressures, and specific coolants, often demanding materials with enhanced thermal conductivity, chemical resistance, and lightweight properties. Manufacturers who can innovate and specialize in these unique EV piping solutions stand to gain a significant competitive advantage and capture a substantial share of this rapidly expanding segment.

Emerging markets, particularly in Asia Pacific, Latin America, and parts of Africa, offer substantial growth opportunities. These regions are experiencing rapid urbanization, increasing disposable incomes, and a corresponding surge in vehicle ownership and production. As these markets mature, there will be a sustained demand for both new vehicle pipes and aftermarket replacement parts. Investing in local manufacturing capabilities, developing cost-effective solutions tailored to regional needs, and establishing robust distribution networks in these areas can unlock significant market potential. This geographic diversification helps to mitigate risks associated with saturation or slower growth in traditional automotive markets.

Technological advancements, including additive manufacturing (3D printing) and the development of high-performance composite materials, represent further opportunities. Additive manufacturing enables rapid prototyping of complex pipe geometries and the production of customized, low-volume components with intricate internal structures that are difficult to achieve with conventional methods. This technology can reduce lead times and material waste. Similarly, the ongoing research and development into new composite materials, smart materials, and advanced coatings can lead to pipes with superior strength-to-weight ratios, enhanced corrosion resistance, and integrated sensing capabilities, opening doors for high-value applications and premium product offerings that command better margins and contribute to overall vehicle efficiency and intelligence.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Electric and Hybrid Vehicle Production | +2.0% | Global, particularly North America, Europe, Asia Pacific | 2025-2033 |

| Expansion in Emerging Automotive Markets | +1.5% | Asia Pacific (India, Southeast Asia), Latin America | 2025-2033 |

| Development of Advanced & Lightweight Materials | +1.0% | Global | 2025-2033 |

| Aftermarket Demand & Replacement Parts Market | +0.8% | Global | Ongoing |

Automotive Pipe Market Challenges Impact Analysis

The automotive pipe market faces significant challenges, notably the complexities associated with adhering to stringent global and regional regulatory standards, particularly concerning emissions and safety. Compliance with evolving environmental legislation, such as Euro 7 in Europe or upcoming CAFE standards in North America, requires continuous innovation in materials and manufacturing processes to ensure pipes contribute to lower vehicle emissions and improved fuel efficiency. Meeting these diverse and often conflicting regulations across different geographical markets adds considerable design, testing, and certification costs for manufacturers, potentially slowing down product development and market entry for new solutions.

Another prominent challenge is the increasing sophistication of vehicle systems, demanding pipes with higher performance capabilities and integration complexities. Modern vehicles feature compact engine compartments and complex routing requirements for various fluid lines (fuel, brake, coolant, HVAC, etc.), especially with the integration of hybrid and electric powertrains. This necessitates pipes with tight bend radii, specialized connectors, and exceptional resistance to extreme temperatures, pressures, and corrosive fluids. Manufacturing these highly customized and precision-engineered pipes requires advanced production technologies, significant capital investment, and a highly skilled workforce, posing barriers for smaller manufacturers and increasing the overall cost structure.

Furthermore, the automotive industry's inherent susceptibility to economic downturns and geopolitical instability poses a considerable challenge. Economic slowdowns can directly impact consumer purchasing power, leading to reduced new vehicle sales and subsequently lower demand for automotive pipes. Geopolitical tensions, trade disputes, and natural disasters can disrupt global supply chains, affecting the availability and cost of raw materials and components, leading to production delays and increased operational risks. Navasigating these external uncertainties while simultaneously investing in new technologies and capacities to meet future market demands is a critical balancing act for players in the automotive pipe market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Compliance with Evolving Environmental Regulations | -0.9% | Global | 2025-2033 |

| High Research & Development Costs for New Technologies | -0.7% | Global | 2025-2033 |

| Integration Complexities with Advanced Vehicle Systems | -0.6% | Developed Markets | 2025-2030 |

| Skilled Labor Shortage & Workforce Training | -0.4% | Global | 2025-2033 |

Automotive Pipe Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global Automotive Pipe Market, offering a detailed segmentation by material type, application, vehicle type, and sales channel, along with a thorough regional and country-level breakdown. It examines key market trends, drivers, restraints, opportunities, and challenges influencing market dynamics, offering strategic insights for stakeholders. The report also includes a competitive landscape analysis, profiling key market players and their strategies, to provide a holistic view of the industry's current state and future prospects, focusing on technological advancements and market shifts.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 20.0 billion |

| Market Forecast in 2033 | USD 33.18 billion |

| Growth Rate | 6.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Sumitomo Electric Industries, TI Fluid Systems, Parker Hannifin, Continental AG, Eaton Corporation, Cooper Standard, Sanoh Industrial, Nichirin Co. Ltd., Hutchinson SA, Plastic Omnium, Flex-N-Gate, Tenneco Inc., Marelli Holdings Co., Montaplast GmbH, Roechling Automotive, Mann+Hummel, Kautex Textron, Hella GmbH & Co. KGaA, BorgWarner Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Pipe Market is extensively segmented to provide a granular view of its diverse components and applications, enabling a deeper understanding of market dynamics and growth opportunities. This comprehensive segmentation reflects the complex requirements of modern vehicles and the varied materials and technologies employed in pipe manufacturing. Each segment contributes uniquely to the overall market landscape, driven by specific industry trends, technological advancements, and regulatory demands, allowing stakeholders to identify niche markets and tailor strategies effectively.

- By Material:

- Steel: Traditional and high-strength steel for robust applications like exhaust systems and brake lines.

- Aluminum: Lightweight alternative for applications requiring thermal conductivity and corrosion resistance.

- Copper: Utilized for its excellent thermal properties in certain cooling and HVAC systems.

- Plastic: Increasingly used for lightweighting in fuel lines, air intake, and fluid transfer systems.

- Rubber: Flexible hoses for coolant, oil, and brake fluid transfer, offering vibration absorption.

- Composites: Advanced materials for specialized applications requiring high strength-to-weight ratios.

- By Application:

- Fuel Lines: For gasoline, diesel, and alternative fuels.

- Brake Lines: Critical for hydraulic braking systems.

- AC Lines: For air conditioning and refrigerant transfer.

- Exhaust Pipes: For expelling engine exhaust gases.

- Coolant Hoses: For engine and battery thermal management.

- Turbocharger Hoses: For high-temperature and pressure air transfer.

- Air Induction Pipes: For directing air to the engine.

- Oil Lines: For engine oil and transmission fluid.

- Power Steering Hoses: For hydraulic power steering systems.

- EGR Pipes: For Exhaust Gas Recirculation systems.

- By Vehicle Type:

- Passenger Vehicles: Including sedans, SUVs, hatchbacks, and compact cars.

- Light Commercial Vehicles: Vans, pickups, and small trucks.

- Heavy Commercial Vehicles: Buses and large trucks.

- Electric Vehicles: Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), Fuel Cell Electric Vehicles (FCEVs).

- By Sales Channel:

- OEM (Original Equipment Manufacturer): Pipes supplied directly to vehicle manufacturers for new vehicle assembly.

- Aftermarket: Pipes sold for replacement and repair purposes post-vehicle sale.

- By End-Use:

- Engine: Components within the engine system.

- Chassis: Pipes integrated into the vehicle's frame and suspension.

- Body: Piping within the vehicle body structure.

- HVAC: Heating, Ventilation, and Air Conditioning systems.

- Braking System: Essential for vehicle safety and control.

- Fuel Delivery System: From fuel tank to engine.

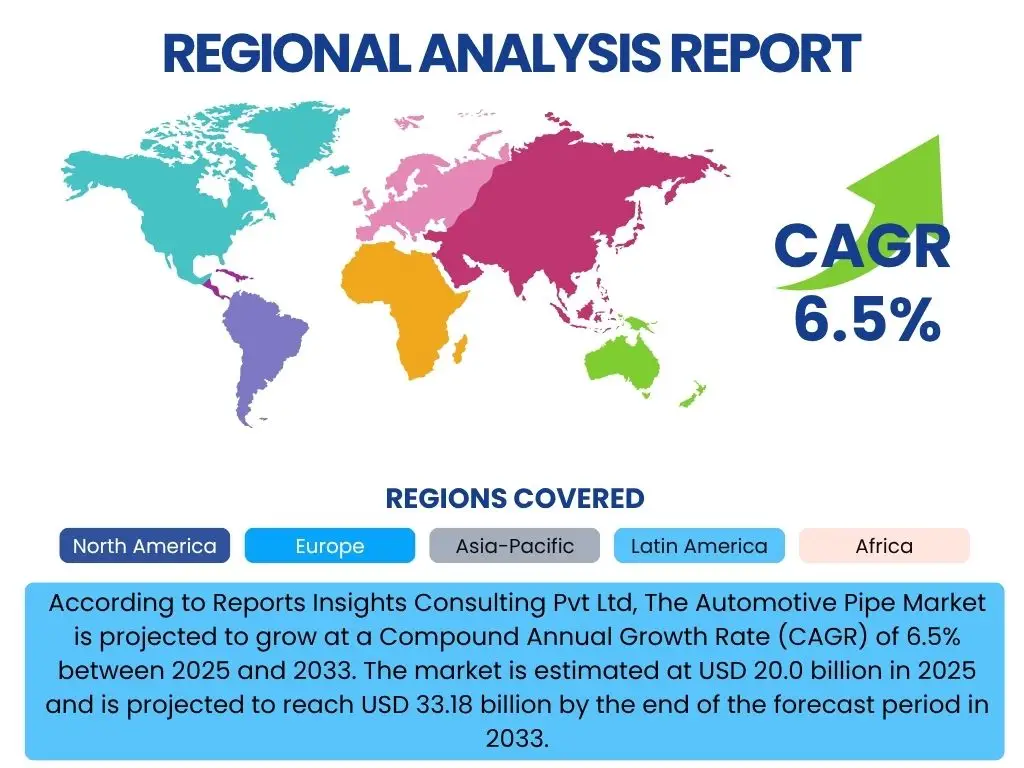

Regional Highlights

- North America: The North American automotive pipe market is characterized by robust demand driven by strong light vehicle sales, a growing aftermarket segment, and significant investments in electric vehicle (EV) production. The region's stringent emission regulations push for advanced lightweight and high-performance piping solutions. The presence of major automotive OEMs and a well-developed supply chain contribute to sustained demand. Innovations in manufacturing technology and material science are readily adopted here, particularly for improving fuel efficiency in traditional vehicles and optimizing thermal management in the rapidly expanding EV sector. The focus on vehicle safety and increasingly complex vehicle architectures also propels the demand for reliable and durable piping systems.

- Europe: Europe represents a mature yet highly innovative market for automotive pipes, largely influenced by the region's pioneering role in environmental regulations and the accelerating transition to electric mobility. European countries lead in the adoption of stringent emission standards, which necessitate continuous development of lightweight, durable, and highly efficient piping components to reduce CO2 emissions. The robust automotive manufacturing base, coupled with extensive research and development activities, fosters the introduction of advanced materials like composites and smart piping systems. The increasing sales of premium and luxury vehicles also contribute to the demand for high-quality and customized pipe solutions, reflecting a strong emphasis on performance and sophisticated engineering.

- Asia Pacific (APAC): The Asia Pacific region stands as the largest and fastest-growing market for automotive pipes, primarily fueled by massive vehicle production volumes in countries like China, India, Japan, and South Korea. Rapid industrialization, urbanization, and rising disposable incomes have led to a surge in vehicle ownership, both passenger and commercial. This region is also at the forefront of electric vehicle manufacturing, creating immense demand for specialized EV-related piping for battery cooling and thermal management. While cost-effectiveness remains a key factor, there is a growing emphasis on quality and technological advancement, particularly in markets like Japan and South Korea, driving the adoption of advanced pipe solutions and materials.

- Latin America: The Latin American automotive pipe market is characterized by steady growth, primarily driven by expanding vehicle production in countries such as Brazil and Mexico, which serve as major manufacturing hubs for both regional and export markets. Economic recovery and increasing consumer spending are contributing to rising vehicle sales. While often a price-sensitive market, there is a gradual shift towards adopting more advanced and efficient piping solutions, partly influenced by global automotive trends and increasing regulatory pressures for environmental performance. The aftermarket segment also plays a significant role in this region, driven by the need for maintenance and replacement parts for an aging vehicle fleet.

- Middle East and Africa (MEA): The MEA region presents emerging opportunities for the automotive pipe market, albeit with varying dynamics across sub-regions. Growth is influenced by rising vehicle sales in affluent Gulf Cooperation Council (GCC) countries and increasing automotive manufacturing activities, particularly in countries like South Africa and Morocco. Investments in infrastructure development and economic diversification initiatives are slowly expanding the automotive sector. Demand for pipes is driven by new vehicle imports and a growing localized production, along with a significant aftermarket due to the harsh operating conditions in some areas. The adoption of advanced piping technologies is often slower than in developed markets but is gradually increasing with foreign investments and technological transfers.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Pipe Market.- Sumitomo Electric Industries

- TI Fluid Systems

- Parker Hannifin

- Continental AG

- Eaton Corporation

- Cooper Standard

- Sanoh Industrial

- Nichirin Co. Ltd.

- Hutchinson SA

- Plastic Omnium

- Flex-N-Gate

- Tenneco Inc.

- Marelli Holdings Co.

- Montaplast GmbH

- Roechling Automotive

- Mann+Hummel

- Kautex Textron

- Hella GmbH & Co. KGaA

- BorgWarner Inc.

Frequently Asked Questions

What is the projected growth rate of the Automotive Pipe Market?

The Automotive Pipe Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033.

What are the primary drivers of growth in the Automotive Pipe Market?

Key drivers include increasing global vehicle production, the rapid expansion of electric vehicle (EV) manufacturing, stringent emission regulations, and continuous advancements in materials and manufacturing technologies for lightweight and high-performance pipes.

How is AI impacting the Automotive Pipe Market?

AI is influencing the market through optimized design and simulation, predictive maintenance in manufacturing, enhanced quality control via AI-powered vision systems, and intelligent supply chain management for improved efficiency and reduced costs.

Which regions are expected to show significant growth in the Automotive Pipe Market?

Asia Pacific is anticipated to be the largest and fastest-growing market due to high vehicle production volumes and EV adoption, while North America and Europe will continue to be strong markets driven by technological advancements and strict regulations.

What are the main types of materials used for automotive pipes?

Automotive pipes are primarily manufactured using materials such as steel, aluminum, copper, various plastics, rubber, and advanced composites, each selected based on specific application requirements like temperature resistance, pressure handling, and weight reduction.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted