Automotive Millimeter Wave Radar Market

Automotive Millimeter Wave Radar Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710218 | Last Updated : December 30, 2025 |

Format : ![]()

![]()

![]()

![]()

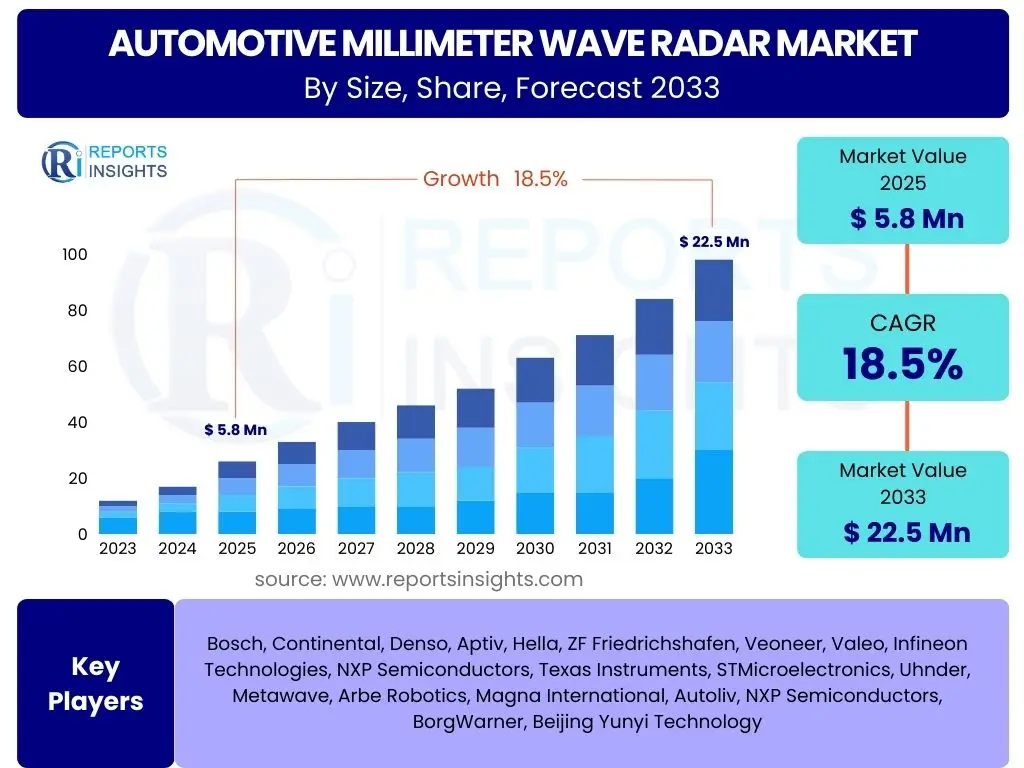

Automotive Millimeter Wave Radar Market Size

According to Reports Insights Consulting Pvt Ltd, The Automotive Millimeter Wave Radar Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 5.8 Billion in 2025 and is projected to reach USD 22.5 Billion by the end of the forecast period in 2033.

Key Automotive Millimeter Wave Radar Market Trends & Insights

Market analysis indicates a strong user interest in understanding the core technological advancements and application expansion driving the automotive millimeter wave radar sector. Common inquiries revolve around the shift towards higher frequency bands, the integration of radar with other ADAS sensors, and the evolving role of radar in achieving higher levels of autonomous driving. Users are also keen on how these trends are impacting vehicle safety and efficiency. The insights suggest a market characterized by continuous innovation aimed at improving detection capabilities, object classification, and environmental perception for advanced driver-assistance systems and fully autonomous vehicles.

The increasing demand for enhanced safety features and the rapid progress in autonomous driving technologies are undeniably shaping the market landscape. Miniaturization of radar units, combined with improved processing power, allows for more compact and versatile integration into vehicle designs. Furthermore, the development of 4D imaging radar is gaining traction, offering richer point cloud data that significantly improves environmental mapping and object differentiation, crucial for complex driving scenarios. These technological shifts are not merely incremental; they represent fundamental advancements that are redefining the capabilities and applications of automotive radar systems.

- Escalating adoption of 77 GHz and 79 GHz radar systems for superior resolution and range.

- Increasing integration of radar with cameras, LiDAR, and ultrasonic sensors for robust sensor fusion.

- Development and deployment of 4D imaging radar for enhanced environmental perception and object classification.

- Growing demand for advanced driver-assistance systems (ADAS) in entry-level and mid-range vehicle segments.

- Focus on software-defined radar and over-the-air (OTA) updates for continuous performance improvement.

- Expansion of radar applications beyond traditional front and rear sensing to include interior cabin monitoring and gesture recognition.

AI Impact Analysis on Automotive Millimeter Wave Radar

User queries regarding AI's influence on automotive millimeter wave radar frequently center on how artificial intelligence algorithms enhance raw radar data processing, improve object recognition and tracking, and enable more sophisticated decision-making in autonomous systems. There is significant interest in how AI can overcome traditional radar limitations, such as distinguishing between stationary and moving objects in complex scenarios or mitigating interference. Users anticipate that AI will be a pivotal force in pushing radar capabilities beyond simple distance and velocity measurements, transforming it into an intelligent perception system critical for advanced automation.

The application of AI in automotive radar extends across various aspects, from signal processing to predictive analytics. Machine learning models are being employed to filter noise, extract intricate features from radar returns, and classify objects with unprecedented accuracy, reducing false positives and improving overall system reliability. Furthermore, AI-driven sensor fusion algorithms enable radar data to be seamlessly combined with information from other sensors, creating a comprehensive and resilient perception model for the vehicle. This integration is vital for achieving Level 3 and higher autonomous driving, where robust environmental understanding is paramount for safe operation. AI is not just optimizing existing radar functions; it is enabling entirely new levels of performance and intelligence for automotive safety and autonomy.

- Enhanced object classification and differentiation through deep learning algorithms applied to radar data.

- Improved clutter rejection and noise reduction using AI-powered signal processing techniques.

- Advanced sensor fusion with cameras and LiDAR, leveraging AI to create a holistic and robust perception model.

- Predictive analytics and behavior forecasting for other road users, enabled by machine learning.

- Development of cognitive radar systems that adapt their transmission parameters based on environmental conditions.

- Enabling of real-time decision-making and path planning for autonomous vehicles through AI-driven insights from radar.

Key Takeaways Automotive Millimeter Wave Radar Market Size & Forecast

A central theme identified from user inquiries regarding the automotive millimeter wave radar market size and forecast is the expectation of sustained, robust growth driven by the inexorable push towards autonomous driving and enhanced vehicle safety. Users seek clarity on which segments, technologies, and regions are poised for the most significant expansion, as well as the underlying factors propelling this growth. The consensus among market stakeholders is that the increasing stringency of safety regulations, coupled with consumer demand for advanced features, will ensure a consistently upward trajectory for the market.

The market's expansion is not merely linear but characterized by significant innovation and diversification. While passenger vehicles currently dominate, the commercial vehicle segment, particularly in logistics and public transport, is anticipated to present considerable growth opportunities. The transition to higher frequency bands (77/79 GHz) is a critical technological shift enabling this growth, offering superior performance essential for higher levels of autonomy. Furthermore, emerging markets are expected to play an increasingly important role in market expansion as ADAS features become more standardized globally. These combined factors solidify the automotive millimeter wave radar market as a high-growth sector with long-term potential.

- The market is on a steep growth curve, projected to more than quadruple by 2033, driven by ADAS and autonomous vehicle adoption.

- 77 GHz and 79 GHz radar technologies are expected to be the primary growth engines due to their superior performance.

- Passenger vehicles will remain the largest application segment, but commercial vehicle applications are poised for rapid growth.

- Regulatory mandates for ADAS features, such as Automatic Emergency Braking (AEB) and Adaptive Cruise Control (ACC), are crucial market accelerators.

- Asia Pacific is anticipated to exhibit the highest growth rate, fueled by robust automotive production and technology adoption.

- Technological advancements in 4D imaging radar and AI-driven processing will unlock new applications and enhance system reliability.

Automotive Millimeter Wave Radar Market Drivers Analysis

The proliferation of Advanced Driver-Assistance Systems (ADAS) and the accelerating development of autonomous driving technologies are paramount drivers for the automotive millimeter wave radar market. As safety regulations become more stringent globally, the mandatory inclusion of features such as Automatic Emergency Braking (AEB), Adaptive Cruise Control (ACC), and Blind Spot Detection (BSD) in new vehicles directly fuels the demand for sophisticated radar sensors. These systems rely heavily on the precise distance and velocity measurements provided by millimeter wave radar, ensuring a high level of functional safety and operational performance.

Furthermore, the automotive industry's strategic shift towards higher levels of autonomous driving, from Level 2+ to Level 3 and beyond, necessitates a robust and redundant perception suite, with radar playing a crucial role alongside cameras and LiDAR. The inherent advantages of radar, such as its robust performance in adverse weather conditions (fog, rain, snow) and its ability to penetrate objects to some extent, make it indispensable for all-weather autonomous operation. The continuous research and development in electric and hybrid vehicles also indirectly supports radar market growth, as these vehicles often integrate advanced technologies from their inception to offer premium safety and convenience features, further cementing radar's position as a foundational sensing technology.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption of ADAS Features | +4.5% | Global, especially North America, Europe, China | Short to Mid-term (2025-2029) |

| Growing Demand for Autonomous Driving Technologies | +3.8% | Global, particularly US, Germany, Japan, China | Mid to Long-term (2027-2033) |

| Stringent Vehicle Safety Regulations and Mandates | +3.0% | Europe (Euro NCAP), North America (NHTSA), Japan, South Korea | Short to Mid-term (2025-2030) |

| Technological Advancements in Radar Systems (e.g., 4D Imaging) | +2.5% | Global, particularly R&D hubs in Germany, US, Japan | Mid to Long-term (2026-2033) |

| Expansion of Electric Vehicle (EV) and Hybrid Vehicle Market | +1.5% | China, Europe, North America | Short to Long-term (2025-2033) |

Automotive Millimeter Wave Radar Market Restraints Analysis

Despite the robust growth projections, the automotive millimeter wave radar market faces several notable restraints that could temper its expansion. One significant challenge is the relatively high cost associated with advanced radar systems, particularly those operating at higher frequencies (77/79 GHz) and offering 4D imaging capabilities. This cost factor can be a barrier to widespread adoption, especially in price-sensitive vehicle segments and emerging markets, limiting the penetration of these advanced safety features into lower-tier vehicles.

Another key restraint is the complexity involved in sensor fusion and data interpretation when integrating radar with other perception sensors like cameras and LiDAR. Achieving seamless, real-time data correlation and robust decision-making from diverse sensor inputs requires sophisticated algorithms and significant processing power, which can add to development costs and computational overhead. Furthermore, while radar is resilient to many weather conditions, its performance can still be affected by heavy rain, dense fog, or snow accumulation on the sensor's radome, potentially leading to reduced accuracy or temporary blind spots. Regulatory hurdles and standardization challenges across different regions also introduce complexities for manufacturers operating on a global scale, requiring adaptation to diverse technical requirements and certification processes.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Radar Systems | -2.0% | Global, particularly emerging markets | Short to Mid-term (2025-2030) |

| Complexity in Sensor Fusion and Data Interpretation | -1.5% | Global, especially for L3+ autonomous systems | Short to Mid-term (2025-2028) |

| Potential for Interference from Other Radar Systems | -1.0% | Dense urban areas, high ADAS penetration regions | Mid-term (2027-2032) |

| Limited Resolution Compared to LiDAR for Certain Applications | -0.8% | Global, particularly for high-definition mapping | Mid to Long-term (2028-2033) |

| Vulnerability to Radome Contamination (e.g., snow, mud) | -0.7% | Regions with severe weather conditions (e.g., Nordic countries, Canada) | Short to Long-term (2025-2033) |

Automotive Millimeter Wave Radar Market Opportunities Analysis

The automotive millimeter wave radar market is replete with significant opportunities stemming from ongoing technological innovation and expanding application areas. The development of next-generation 4D imaging radar presents a substantial opportunity, as it promises to deliver richer, higher-resolution point cloud data that rivals or even surpasses the capabilities of traditional LiDAR for certain tasks, particularly in adverse weather conditions. This advancement enhances object detection, classification, and free-space mapping, which are critical for enabling higher levels of autonomous driving (L3, L4, and L5) and can potentially reduce reliance on other, more expensive sensor modalities in some scenarios.

Furthermore, the emergence of Vehicle-to-Everything (V2X) communication technologies offers a compelling opportunity for radar. Integrating radar data with V2X information can provide an unprecedented level of situational awareness, allowing vehicles to perceive objects and hazards beyond their direct line of sight or around corners. This fusion of local sensor data with shared network information significantly enhances safety and efficiency. Beyond traditional ADAS and autonomous driving, new application domains, such as interior cabin monitoring (e.g., detecting forgotten children or pets, gesture control), parking assist systems, and even aftermarket radar solutions, are opening up. The continuous push for cost reduction through economies of scale and advanced manufacturing techniques also creates opportunities for broader market penetration across all vehicle segments, including commercial vehicles and specialty vehicles.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and Integration of 4D Imaging Radar | +3.2% | Global, particularly automotive innovation hubs | Mid to Long-term (2027-2033) |

| Expansion into Level 3, 4, and 5 Autonomous Driving Applications | +2.8% | US, Europe, China, Japan | Mid to Long-term (2028-2033) |

| Integration with Vehicle-to-Everything (V2X) Communication | +2.0% | Global, smart city initiatives | Mid-term (2027-2032) |

| New Applications such as Cabin Monitoring and Gesture Control | +1.5% | Europe, North America, Japan | Short to Mid-term (2025-2030) |

| Growth in Aftermarket and Commercial Vehicle Installations | +1.0% | Global, particularly fleet operators | Short to Long-term (2025-2033) |

Automotive Millimeter Wave Radar Market Challenges Impact Analysis

The automotive millimeter wave radar market faces several inherent challenges that demand innovative solutions from manufacturers and developers. One significant challenge is the potential for mutual interference between radar systems, especially as the number of radar-equipped vehicles on the road increases and multiple radar units are installed on a single vehicle. This interference can lead to reduced accuracy, false detections, or missed objects, compromising the reliability of ADAS and autonomous driving functions. Developing robust interference mitigation techniques, whether through advanced signal processing or frequency modulation, remains a key technical hurdle.

Another critical challenge involves the immense amount of data generated by high-resolution radar systems, particularly 4D imaging radar. Efficiently processing, storing, and transmitting this data in real-time, within the constraints of automotive electrical architectures, requires powerful onboard computing capabilities and optimized algorithms. The precise classification of objects in complex scenarios, such as distinguishing between pedestrians, cyclists, and inanimate objects in dense urban environments, also poses an ongoing challenge, as radar's raw data can be less intuitive than camera images. Additionally, achieving cost-effectiveness while maintaining high performance and reliability, especially for mass-market adoption, necessitates continuous innovation in manufacturing processes and material science. Addressing these challenges is paramount for the automotive millimeter wave radar market to fully realize its potential and ensure widespread, safe deployment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Mitigation of Radar Interference in Dense Environments | -1.8% | Global, especially urban areas | Short to Mid-term (2025-2030) |

| Processing and Interpreting High-Volume 4D Radar Data | -1.4% | Global, particularly for L3+ systems | Mid-term (2027-2032) |

| Accurate Object Classification in Complex Scenarios | -1.2% | Global, particularly urban and suburban environments | Short to Long-term (2025-2033) |

| Ensuring Cybersecurity for Connected Radar Systems | -1.0% | Global, critical for all connected vehicles | Short to Long-term (2025-2033) |

| Standardization and Regulatory Alignment Across Regions | -0.9% | Global, impacting market entry and deployment | Mid-term (2027-2032) |

Automotive Millimeter Wave Radar Market - Updated Report Scope

This comprehensive market insights report meticulously examines the automotive millimeter wave radar market, offering an in-depth analysis of its current landscape, growth trajectories, and future outlook. It provides a detailed segmentation across various parameters, including frequency band, application, vehicle type, range, and component, to offer a granular understanding of market dynamics. The report further investigates key drivers, restraints, opportunities, and challenges influencing market expansion, alongside a thorough regional analysis. A significant focus is placed on the impact of emerging technologies like AI and 4D imaging radar, presenting actionable insights for stakeholders. The objective is to equip businesses with strategic intelligence for informed decision-making in this evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.8 Billion |

| Market Forecast in 2033 | USD 22.5 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Bosch, Continental, Denso, Aptiv, Hella, ZF Friedrichshafen, Veoneer, Valeo, Infineon Technologies, NXP Semiconductors, Texas Instruments, STMicroelectronics, Uhnder, Metawave, Arbe Robotics, Magna International, Autoliv, NXP Semiconductors, BorgWarner, Beijing Yunyi Technology |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The automotive millimeter wave radar market is broadly segmented across several critical dimensions, providing a granular view of its structure and growth dynamics. These segmentations are crucial for understanding market nuances, identifying high-growth areas, and tailoring strategies for specific product offerings or application domains. The divisions primarily revolve around the technological specifications of the radar units, their intended uses within vehicles, and the types of vehicles they are integrated into, reflecting the diverse requirements of the automotive industry.

Further analysis into these segments reveals that the 77 GHz and 79 GHz frequency bands are rapidly gaining dominance due to their superior resolution and compact size, essential for advanced ADAS and autonomous driving. Within applications, ADAS features such as AEB and ACC continue to drive significant volumes, while the autonomous driving segment represents the highest growth potential as L3+ vehicles become more prevalent. Passenger vehicles, especially luxury and mid-range segments, remain the largest end-users, though commercial vehicles are also adopting radar for enhanced safety and operational efficiency. The component segmentation highlights the increasing complexity and technological sophistication required to deliver high-performance radar systems, underscoring the innovation in semiconductor and electronic control unit development.

- By Type: This segment differentiates radar systems based on their operating frequency, primarily categorizing them into 24 GHz, 77 GHz, and 79 GHz. The higher frequency bands (77/79 GHz) are increasingly favored for their higher resolution, precision, and smaller form factor, making them ideal for advanced applications.

- By Application: This segmentation covers the primary uses of automotive radar, broadly divided into Advanced Driver Assistance Systems (ADAS) and Autonomous Driving. ADAS applications include Adaptive Cruise Control (ACC), Automatic Emergency Braking (AEB), Blind Spot Detection (BSD), Forward Collision Warning (FCW), Lane Change Assist (LCA), Parking Assist, and Rear Cross Traffic Alert (RCTA). Autonomous Driving represents systems with Level 3 and higher automation.

- By Vehicle Type: This categorizes the market by the type of vehicle in which the radar systems are installed. It includes Passenger Vehicles, further sub-segmented into Entry-Level, Mid-Range, and Luxury cars, and Commercial Vehicles, which comprise Light Commercial Vehicles (LCV) and Heavy Commercial Vehicles (HCV).

- By Range: Radar systems are classified by their operational detection distance as Short-Range Radar (SRR), typically used for parking assist and blind spot detection; Medium-Range Radar (MRR), used for adaptive cruise control and lane change assist; and Long-Range Radar (LRR), primarily for forward collision warning and high-speed ACC.

- By Component: This segment breaks down the radar system into its core constituent parts, including the Transceiver Module, Antenna Module, Electronic Control Unit (ECU), Digital Signal Processor (DSP), Power Amplifier, and Microcontroller, highlighting the underlying technological infrastructure.

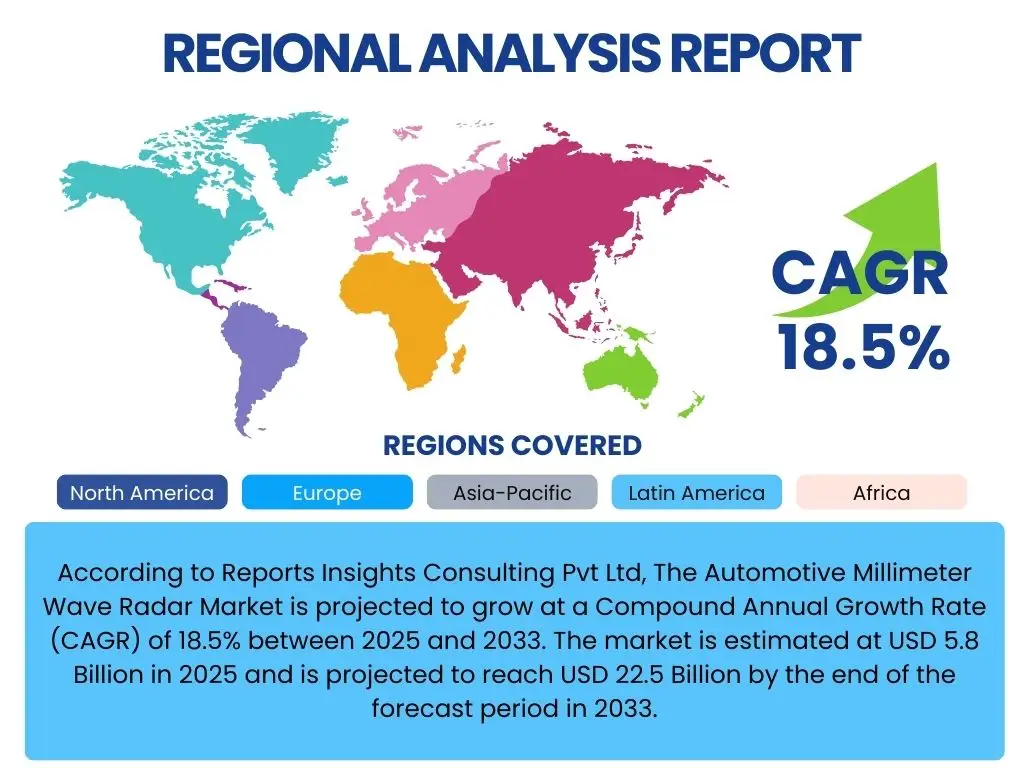

Regional Highlights

- North America: This region is a significant market, driven by stringent safety regulations, a high adoption rate of ADAS features, and substantial investment in autonomous vehicle research and development. The presence of major automotive OEMs and tech companies further fuels market growth.

- Europe: Europe stands out due to proactive regulatory mandates for ADAS features, such as Euro NCAP safety ratings, which encourage widespread adoption of radar-based systems. Germany, with its robust automotive industry, and countries focused on sustainable mobility are key contributors.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market, largely due to the high volume of automotive production in China, Japan, South Korea, and India. Rapid urbanization, increasing disposable incomes, and government initiatives promoting vehicle safety and smart transportation are key drivers.

- Latin America: While currently a smaller market, Latin America is expected to show steady growth as vehicle safety standards improve and consumer awareness of ADAS benefits increases, particularly in Brazil and Mexico.

- Middle East and Africa (MEA): This region is an emerging market, with growth driven by infrastructure development projects, increasing luxury vehicle sales, and governmental efforts to enhance road safety in countries like Saudi Arabia and the UAE.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Millimeter Wave Radar Market.- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Aptiv PLC

- Hella GmbH & Co. KGaA

- ZF Friedrichshafen AG

- Veoneer Inc.

- Valeo S.A.

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Texas Instruments Incorporated

- STMicroelectronics N.V.

- Uhnder, Inc.

- Metawave Corporation

- Arbe Robotics Ltd.

- Magna International Inc.

- Autoliv Inc.

- Panasonic Corporation

- BorgWarner Inc.

- Beijing Yunyi Technology Co., Ltd.

Frequently Asked Questions

Analyze common user questions about the Automotive Millimeter Wave Radar market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is automotive millimeter wave radar?

Automotive millimeter wave radar is a sensor technology that uses electromagnetic waves in the millimeter wave frequency band to detect objects, measure their distance, speed, and angle relative to the vehicle. It is crucial for Advanced Driver-Assistance Systems (ADAS) and autonomous driving due to its robust performance in various environmental conditions.

How does millimeter wave radar contribute to autonomous driving?

Millimeter wave radar provides essential perception data for autonomous vehicles by accurately detecting obstacles, vehicles, and pedestrians, and measuring their velocity in all weather conditions. It complements other sensors like cameras and LiDAR, contributing to a redundant and robust environmental perception system necessary for safe autonomous operation.

What are the key frequency bands used in automotive radar?

The primary frequency bands used in automotive radar are 24 GHz, 77 GHz, and 79 GHz. While 24 GHz is commonly used for short-range applications, 77 GHz and 79 GHz are increasingly adopted for their superior resolution, longer range, and smaller form factors, making them ideal for advanced ADAS and autonomous driving features.

What is 4D imaging radar and why is it important?

4D imaging radar is an advanced technology that provides not only range, velocity, and azimuth but also elevation information, effectively creating a 4D point cloud of the environment. This significantly improves object detection, classification, and free-space mapping, enhancing the vehicle's ability to perceive complex scenarios and enabling higher levels of autonomous driving.

What challenges does the automotive millimeter wave radar market face?

Key challenges include mitigating interference from other radar systems, efficiently processing the large volumes of data generated by high-resolution radar, accurately classifying objects in complex environments, and managing the cost of advanced systems. Cybersecurity for connected radar systems and global regulatory standardization are also ongoing concerns for the market.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted