Automotive Lidar Sensor Market

Automotive Lidar Sensor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710403 | Last Updated : January 05, 2026 |

Format : ![]()

![]()

![]()

![]()

Automotive Lidar Sensor Market Size

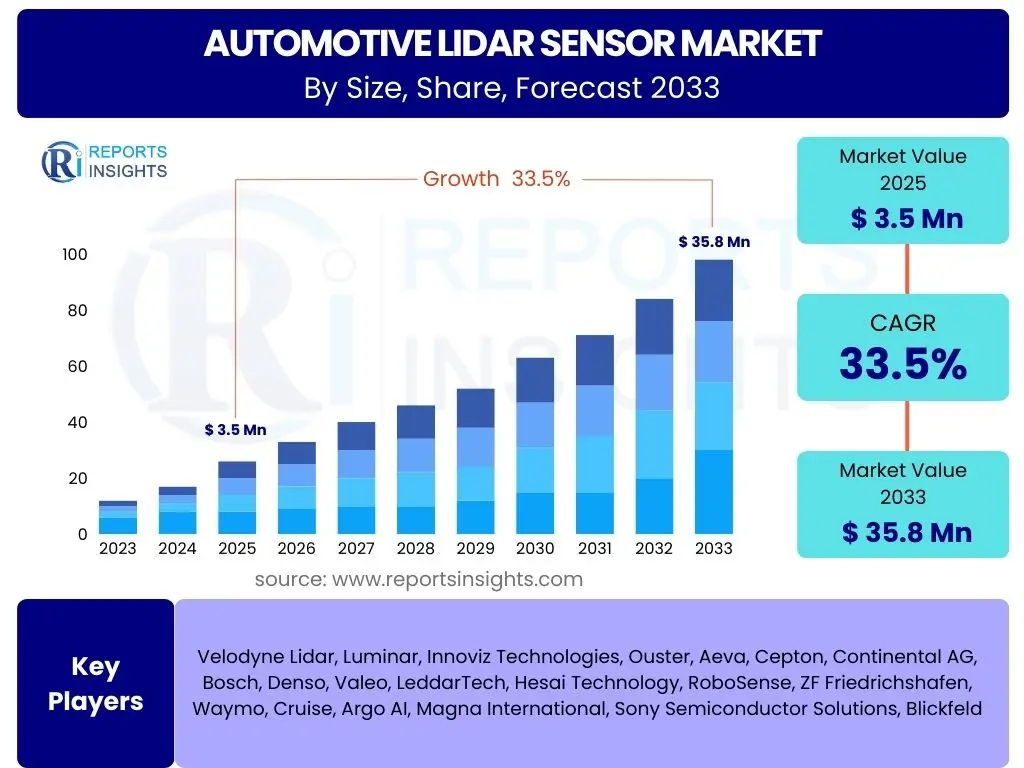

According to Reports Insights Consulting Pvt Ltd, The Automotive Lidar Sensor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 33.5% between 2025 and 2033. The market is estimated at USD 3.5 Billion in 2025 and is projected to reach USD 35.8 Billion by the end of the forecast period in 2033.

Key Automotive Lidar Sensor Market Trends & Insights

The automotive lidar sensor market is undergoing significant transformation driven by advancements in autonomous driving and advanced driver-assistance systems (ADAS). Key trends indicate a strong shift towards solid-state lidar technology, which offers advantages in terms of cost, size, and durability compared to traditional mechanical lidar systems. This technological evolution is crucial for widespread adoption across various vehicle segments, from passenger cars to commercial fleets. The integration of lidar with other sensor modalities, such as radar and cameras, is also a prominent trend, enabling more robust and redundant perception systems for enhanced safety and operational reliability in diverse environmental conditions.

Furthermore, the market is observing a growing emphasis on miniaturization and improved power efficiency of lidar units, making them easier to integrate into vehicle designs without compromising aesthetics or aerodynamic performance. The development of high-resolution, long-range lidar sensors capable of precise object detection and classification at various distances is another critical trend, directly addressing the stringent requirements of Level 3, 4, and 5 autonomous driving. This includes capabilities to operate effectively under challenging weather conditions, which has historically been a limitation for lidar systems. The continued investment in research and development by both established players and emerging startups is fueling rapid innovation in sensor performance and manufacturing scalability.

- Shift towards Solid-State Lidar Technology

- Enhanced Sensor Fusion with Cameras and Radar

- Miniaturization and Improved Power Efficiency

- Development of High-Resolution, Long-Range Lidar

- Increased Integration with ADAS and Autonomous Driving Platforms

- Focus on Cost Reduction for Mass Market Adoption

- Advancements in Lidar Performance in Adverse Weather Conditions

AI Impact Analysis on Automotive Lidar Sensor

Artificial intelligence profoundly influences the automotive lidar sensor market by transforming how lidar data is processed, interpreted, and utilized within a vehicle's perception stack. AI algorithms, particularly deep learning and machine learning, are essential for extracting meaningful insights from the dense point cloud data generated by lidar sensors. This includes precise object detection, classification (e.g., distinguishing pedestrians from cyclists or vehicles), and tracking of dynamic objects in real-time. The ability of AI to filter noise, fill in gaps from sparse data, and identify patterns contributes significantly to the robustness and reliability of autonomous driving systems, making lidar data more actionable and accurate.

Moreover, AI plays a crucial role in the sensor fusion process, where data from lidar, cameras, radar, and ultrasonic sensors are combined to create a comprehensive and redundant environmental model. AI-powered fusion algorithms can leverage the strengths of each sensor type while mitigating their individual limitations, leading to a more complete and accurate understanding of the vehicle's surroundings. This enhances the system's ability to navigate complex urban environments, predict the behavior of other road users, and make critical driving decisions. The ongoing development of sophisticated AI models is directly correlated with improvements in lidar performance and its effectiveness in achieving higher levels of autonomy, addressing key concerns about perception accuracy and safety.

- Advanced Point Cloud Processing and Interpretation

- Enhanced Object Detection, Classification, and Tracking

- Improved Sensor Fusion for Comprehensive Environmental Understanding

- Predictive Analytics for Path Planning and Decision Making

- Noise Reduction and Data Infilling in Lidar Point Clouds

- Real-time Scene Understanding and Semantic Segmentation

- Enabling Higher Levels of Autonomous Driving Functionality

Key Takeaways Automotive Lidar Sensor Market Size & Forecast

The Automotive Lidar Sensor Market is poised for substantial expansion over the forecast period, driven primarily by the escalating demand for advanced driver-assistance systems (ADAS) and the relentless pursuit of fully autonomous vehicles. The projected robust Compound Annual Growth Rate (CAGR) underscores the critical role lidar technology is expected to play in enhancing vehicle safety, situational awareness, and ultimately, the future of mobility. This growth is not merely volumetric but also indicative of the increasing integration of lidar across various vehicle types and price points, moving from niche luxury and research applications to mainstream automotive deployment. The market's significant valuation increase reflects the confidence in lidar's ability to address the complex perception challenges inherent in autonomous driving scenarios.

A significant takeaway is the ongoing technological maturation and cost optimization efforts within the lidar industry. As manufacturing processes become more efficient and solid-state designs gain prominence, the barriers to entry for vehicle manufacturers are steadily decreasing, fostering wider adoption. This trend, coupled with evolving regulatory frameworks that increasingly emphasize active safety features, will continue to accelerate market penetration. The forecasted market size by 2033 highlights a transformative period where lidar sensors transition from a nascent technology to a foundational component of modern vehicles, crucial for both safety enhancements and the realization of a truly autonomous future.

- Exponential Market Growth driven by ADAS and Autonomous Driving

- Lidar as a Foundational Sensor for Future Mobility

- Technological Advancements are Reducing Costs and Increasing Durability

- Increasing Integration Across Passenger and Commercial Vehicles

- Strong Investment and Innovation Fueling Market Expansion

- Critical for Enhanced Vehicle Safety and Redundant Perception Systems

- Shifting from Niche Applications to Mass Market Adoption

Automotive Lidar Sensor Market Drivers Analysis

The automotive lidar sensor market is fundamentally driven by the accelerating demand for Advanced Driver-Assistance Systems (ADAS) and the global push towards autonomous driving. These technologies heavily rely on precise and reliable environmental perception, which lidar sensors excel at providing through accurate 3D mapping and object detection. Furthermore, increasing regulatory mandates and consumer expectations for enhanced vehicle safety features are compelling automakers to integrate sophisticated sensor suites, with lidar emerging as a crucial component. The continuous innovation in lidar technology, leading to smaller, more robust, and more cost-effective solutions, also acts as a significant market driver, making it an increasingly viable option for mass production vehicles.

The expansion of electric vehicle (EV) production and the development of intelligent transportation infrastructure also contribute to market growth. EVs often serve as platforms for advanced technologies, including autonomous features, positioning them as early adopters of lidar. Additionally, the potential for lidar to enhance vehicle-to-everything (V2X) communication by providing detailed environmental data for smart city applications further broadens its appeal. As manufacturers scale production and achieve greater economies of scale, the unit cost of lidar sensors is expected to decrease, making them more accessible and fostering greater market penetration.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for ADAS & Autonomous Driving | +8.5% | Global, particularly North America, Europe, APAC | Short to Long Term |

| Stringent Vehicle Safety Regulations | +6.0% | Europe, North America, China | Medium to Long Term |

| Technological Advancements & Cost Reduction | +7.0% | Global | Short to Medium Term |

| Growth in Electric Vehicle Production | +5.5% | China, Europe, North America | Medium to Long Term |

| Investment in Robotaxis & Ride-Sharing Services | +3.5% | North America, China, Select European Cities | Medium Term |

Automotive Lidar Sensor Market Restraints Analysis

Despite the promising growth trajectory, the automotive lidar sensor market faces several significant restraints that could impede its full potential. A primary concern remains the relatively high cost of lidar sensors, especially for higher-performance units, which can significantly increase the overall price of a vehicle. While costs are declining, they still present a barrier to widespread adoption in entry-level and mid-range vehicle segments. This cost sensitivity requires a delicate balance between performance and affordability, often leading to compromises in sensor specifications for broader market integration. Another key restraint is the current performance limitations of lidar in adverse weather conditions, such as heavy rain, fog, or snow, where the laser beams can be scattered or absorbed, leading to reduced accuracy and range. This necessitates reliance on sensor fusion with radar and cameras to ensure robustness, adding complexity and cost.

Furthermore, the automotive industry's inherent resistance to rapid technological shifts and the long development cycles for new vehicle platforms pose a challenge. Integrating lidar into existing vehicle architectures requires significant engineering efforts, testing, and validation, which can be time-consuming and expensive. The competitive landscape, with alternative sensing technologies like high-resolution cameras and advanced radar systems continually improving, also acts as a restraint. While lidar offers unique advantages, the perception that other sensors might offer "good enough" performance for certain ADAS levels at a lower cost can slow down lidar adoption. The lack of universal standardization across lidar interfaces and data formats also adds complexity for automakers working with multiple suppliers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost of Lidar Systems | -4.0% | Global, particularly developing markets | Short to Medium Term |

| Performance Limitations in Adverse Weather Conditions | -3.0% | Regions with diverse weather (e.g., North America, Europe) | Short to Medium Term |

| Integration Complexity with Vehicle Architectures | -2.5% | Global | Short to Medium Term |

| Competition from Alternative Sensing Technologies (Radar, Camera) | -2.0% | Global | Short to Medium Term |

| Lack of Industry Standardization | -1.5% | Global | Medium Term |

Automotive Lidar Sensor Market Opportunities Analysis

The automotive lidar sensor market presents numerous lucrative opportunities driven by evolving technological landscapes and new application areas. The expansion of Level 3 and higher autonomous driving features in consumer vehicles represents a significant opportunity. As regulatory frameworks mature and public acceptance of self-driving technology grows, the demand for robust perception systems like lidar will increase substantially. Beyond traditional passenger cars, the commercial vehicle sector, including autonomous trucks, buses, and last-mile delivery vehicles, offers a vast untapped market where lidar can enhance operational efficiency and safety. These applications often require higher reliability and performance, aligning well with lidar's capabilities.

Another compelling opportunity lies in the development of specialized lidar solutions for smart city infrastructure and intelligent transportation systems (ITS). Lidar sensors can be deployed in traffic management, pedestrian detection, and smart intersection monitoring, providing real-time data for optimizing traffic flow and improving urban safety. Furthermore, the growth of the robotaxi and ride-sharing industry, which inherently relies on fully autonomous fleets, presents a significant and immediate market for high-performance lidar sensors. The ongoing innovation in solid-state lidar technology, particularly for chip-scale integration, promises further cost reductions and performance enhancements, opening doors for even broader adoption across diverse vehicle segments and potentially new mobility services. Emerging markets in Asia Pacific, particularly China, India, and South Korea, are rapidly investing in smart mobility solutions and electric vehicles, creating new avenues for market penetration.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of L3+ Autonomous Driving in Consumer Vehicles | +7.0% | Global, particularly North America, Europe, China | Medium to Long Term |

| Growth in Commercial Autonomous Vehicles (Trucks, Buses) | +6.5% | North America, Europe, China | Medium to Long Term |

| Emergence of Smart City Infrastructure and ITS | +4.0% | Global, especially China, EU, select US cities | Medium Term |

| Development of Cost-Effective, High-Performance Solid-State Lidar | +5.0% | Global | Short to Medium Term |

| New Mobility Services (Robotaxis, Automated Shuttles) | +3.5% | North America, China, Europe | Short to Medium Term |

Automotive Lidar Sensor Market Challenges Impact Analysis

The automotive lidar sensor market faces a distinct set of challenges that require innovative solutions and strategic approaches to overcome. One significant challenge is the inherent complexity of processing the massive amounts of data generated by lidar sensors in real-time. This requires powerful onboard computing capabilities and sophisticated algorithms, which can add to the system's cost, power consumption, and thermal management complexities. Ensuring the accuracy and reliability of lidar data across an extreme range of operating conditions, including varying temperatures, vibrations, and electromagnetic interference, is another critical technical hurdle. The environmental robustness of lidar units, particularly their ability to withstand harsh automotive conditions, remains a concern for widespread adoption.

Furthermore, achieving standardization for lidar sensor performance metrics, interfaces, and safety protocols across the industry is a considerable challenge. The lack of common standards can hinder interoperability, increase integration costs for automakers, and potentially slow down market growth due to fragmented development efforts. Supply chain complexities, including the availability of specialized components and manufacturing capabilities for high-volume production, also present a challenge. As the demand for lidar escalates, ensuring a robust and scalable supply chain capable of meeting automotive industry requirements for quality and reliability will be paramount. Finally, the ongoing legal and regulatory landscape surrounding autonomous driving and the use of lidar in different jurisdictions adds another layer of complexity, requiring continuous adaptation and compliance from manufacturers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Real-time Data Processing and Computational Requirements | -3.5% | Global | Short to Medium Term |

| Ensuring Environmental Robustness and Durability | -2.8% | Global | Short to Medium Term |

| Lack of Industry-Wide Standardization | -2.2% | Global | Medium Term |

| Supply Chain Scalability and Component Availability | -1.8% | Global | Short to Medium Term |

| Regulatory and Legal Uncertainties for Autonomous Driving | -1.5% | North America, Europe, China | Medium to Long Term |

Automotive Lidar Sensor Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Automotive Lidar Sensor Market, encompassing historical data, current market dynamics, and future growth projections. It aims to offer strategic insights into market size, segmentation, regional trends, key drivers, restraints, opportunities, and challenges influencing the industry. The report covers the period from 2019 to 2033, providing stakeholders with a detailed understanding of market evolution and forecasting future trajectories based on technological advancements, regulatory changes, and competitive landscapes. Special attention is given to the impact of artificial intelligence and emerging market trends, ensuring a holistic perspective for informed decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 35.8 Billion |

| Growth Rate | 33.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Velodyne Lidar, Luminar, Innoviz Technologies, Ouster, Aeva, Cepton, Continental AG, Bosch, Denso, Valeo, LeddarTech, Hesai Technology, RoboSense, ZF Friedrichshafen, Waymo, Cruise, Argo AI, Magna International, Sony Semiconductor Solutions, Blickfeld |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Lidar Sensor Market is comprehensively segmented across various dimensions to provide a granular understanding of its structure and dynamics. These segmentations are crucial for identifying specific market niches, understanding technological preferences, and analyzing adoption patterns across different vehicle types and applications. The segmentation by technology distinguishes between the traditional mechanical lidar, known for its 360-degree coverage, and the rapidly evolving solid-state lidar, which promises greater reliability, compactness, and cost-effectiveness through various sub-technologies like Flash, MEMS, and Optical Phased Array. This distinction highlights the industry's move towards more integrated and durable solutions suitable for mass production.

Further segmentation by application categorizes the market based on its use in Advanced Driver-Assistance Systems (ADAS), such as adaptive cruise control and automatic emergency braking, versus the more advanced requirements of fully autonomous driving at Level 3 and above. This helps in understanding the varying performance requirements and integration complexities. Vehicle type segmentation differentiates between passenger cars and commercial vehicles, recognizing their distinct design cycles, regulatory environments, and price sensitivities. Range-based segmentation assesses the market's needs for short, medium, and long-range detection, critical for different driving scenarios. Finally, component-level segmentation provides insights into the supply chain and technological contributions of various parts of a lidar system, from transceivers and receivers to processing units and optics.

- By Technology: Solid-State Lidar (Flash Lidar, MEMS Lidar, Optical Phased Array Lidar), Mechanical Lidar

- By Application: Advanced Driver-Assistance Systems (ADAS) (Adaptive Cruise Control, Lane Keeping Assist, Automatic Emergency Braking, Blind Spot Detection), Autonomous Driving (L3, L4, L5)

- By Vehicle Type: Passenger Vehicles (Sedans, SUVs, Hatchbacks), Commercial Vehicles (Trucks, Buses, Robotaxis, Delivery Vans)

- By Range: Short Range, Medium Range, Long Range

- By Component: Transceiver, Receiver, Processor, Optics, Other Components

Regional Highlights

- North America: A leader in autonomous vehicle research and development, with significant investment from tech companies and traditional automakers. Strong regulatory support for testing and deployment of autonomous vehicles, particularly in states like California and Arizona. High adoption rate of ADAS features in new vehicles.

- Europe: Driven by stringent safety regulations and a strong emphasis on reducing road fatalities. Major automotive manufacturers are actively integrating lidar into their next-generation vehicles. Growing market for premium and luxury cars featuring advanced ADAS.

- Asia Pacific (APAC): The fastest-growing region, primarily propelled by China's aggressive push into autonomous driving, electric vehicles, and smart city initiatives. Japan and South Korea are also significant players with robust automotive industries and technological innovation. India shows emerging potential with increasing infrastructure development and consumer awareness for vehicle safety.

- Latin America: Nascent but developing market with increasing demand for vehicle safety features and growing urbanization. Opportunities for entry-level ADAS and eventually autonomous solutions.

- Middle East and Africa (MEA): Emerging market with significant government investment in smart city projects and autonomous transportation in countries like UAE and Saudi Arabia. Potential for rapid adoption of cutting-edge automotive technologies.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Lidar Sensor Market.- Velodyne Lidar

- Luminar

- Innoviz Technologies

- Ouster

- Aeva

- Cepton

- Continental AG

- Robert Bosch GmbH

- Denso Corporation

- Valeo S.A.

- LeddarTech

- Hesai Technology

- RoboSense

- ZF Friedrichshafen AG

- Waymo LLC

- Cruise LLC

- Argo AI

- Magna International Inc.

- Sony Semiconductor Solutions Corporation

- Blickfeld GmbH

Frequently Asked Questions

Analyze common user questions about the Automotive Lidar Sensor market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is an automotive lidar sensor?

An automotive lidar sensor is a remote sensing technology that uses pulsed laser light to measure distances to objects and create detailed 3D maps of a vehicle's surroundings. It emits millions of laser pulses per second and calculates distances based on the time it takes for the light to reflect back, providing highly accurate and precise spatial data crucial for Advanced Driver-Assistance Systems (ADAS) and autonomous driving.

Why is lidar important for autonomous cars?

Lidar is critical for autonomous cars because it provides superior 3D depth perception and object detection capabilities compared to other sensors, particularly in measuring distance and velocity accurately. Its ability to generate dense point clouds offers a precise understanding of the environment, supplementing cameras and radar to ensure robust perception, redundancy, and safer navigation in complex driving scenarios.

What are the main types of automotive lidar sensors?

The main types of automotive lidar sensors are mechanical lidar and solid-state lidar. Mechanical lidar typically rotates to provide a 360-degree field of view, while solid-state lidar uses no moving parts, offering advantages in terms of durability, size, and cost. Solid-state lidar includes technologies like Flash Lidar, MEMS (Micro-Electro-Mechanical Systems) Lidar, and Optical Phased Array Lidar, each with distinct operational principles and benefits.

What are the key challenges facing the automotive lidar market?

Key challenges include the relatively high cost of lidar systems, which hinders mass market adoption, and limitations in performance during adverse weather conditions like heavy rain or fog. Other challenges involve the complexity of real-time data processing, the need for industry standardization, and seamless integration into existing vehicle architectures, as well as establishing a scalable and reliable supply chain.

What is the future outlook for the automotive lidar sensor market?

The future outlook for the automotive lidar sensor market is highly positive, projecting substantial growth driven by the continuous advancement of ADAS and autonomous driving technologies. As costs decline and performance improves, especially with the proliferation of solid-state solutions, lidar is expected to become a standard component in an increasing number of vehicles, playing a pivotal role in enhancing vehicle safety and enabling higher levels of autonomy.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted