Automotive LED Headlight Market

Automotive LED Headlight Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705052 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

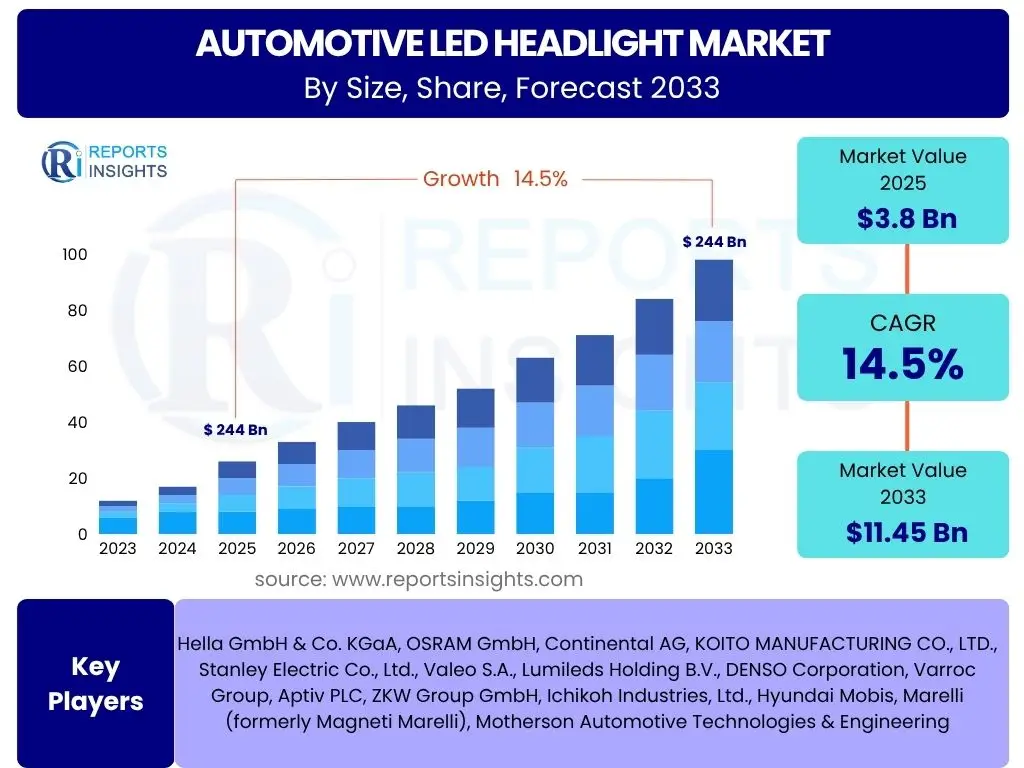

Automotive LED Headlight Market Size

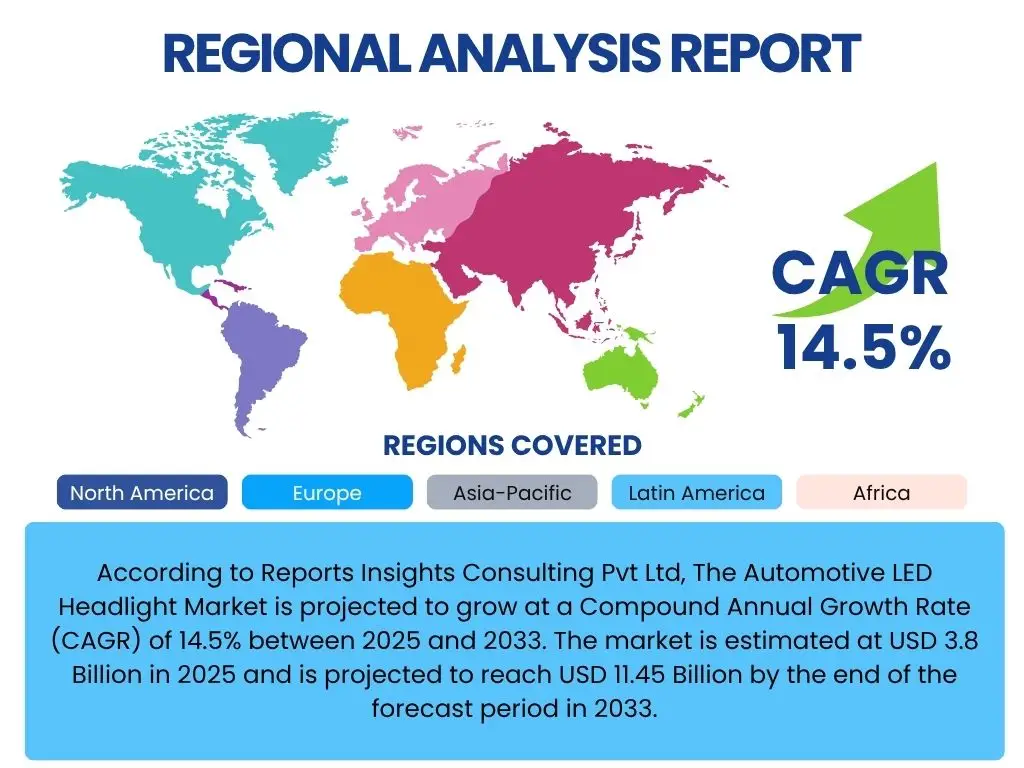

According to Reports Insights Consulting Pvt Ltd, The Automotive LED Headlight Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 14.5% between 2025 and 2033. The market is estimated at USD 3.8 Billion in 2025 and is projected to reach USD 11.45 Billion by the end of the forecast period in 2033.

Key Automotive LED Headlight Market Trends & Insights

The Automotive LED Headlight market is undergoing significant transformation, driven by advancements in lighting technology, evolving consumer preferences, and stringent regulatory frameworks. Users are increasingly seeking information on how these innovations contribute to enhanced vehicle safety, aesthetics, and energy efficiency. Key trends indicate a shift towards more sophisticated lighting systems that offer superior illumination and adaptive functionalities, improving nighttime visibility and reducing glare for oncoming drivers. Furthermore, the integration of LED technology into vehicle design is becoming a critical differentiator for automotive manufacturers, influencing both performance and brand appeal. The ongoing development of compact and powerful LED solutions is expanding their application across various vehicle segments.

There is a strong focus on the miniaturization of LED components, enabling more flexible and innovative headlight designs that contribute to the overall aesthetic appeal of modern vehicles. The adoption of adaptive driving beam (ADB) technology, which automatically adjusts light distribution to prevent dazzling other road users while maximizing illumination, is gaining traction. This trend is closely linked to advancements in sensor technology and intelligent control systems within vehicles. Additionally, the increasing demand for energy-efficient components in the context of electric vehicle proliferation is further accelerating the transition from traditional halogen and Xenon High-Intensity Discharge (HID) lamps to LEDs, which consume significantly less power and offer a longer lifespan. The market is also seeing a rise in decorative and customizable lighting features, allowing for personalization and brand identity expression, reflecting a blend of functionality and style.

- Growing adoption of Adaptive Driving Beam (ADB) technology for enhanced safety.

- Miniaturization of LED components enabling sleek and innovative headlight designs.

- Increasing integration of LED lighting in premium and luxury vehicle segments.

- Rise in demand for energy-efficient lighting solutions, especially in electric vehicles (EVs).

- Development of customizable and intelligent lighting systems for aesthetic and functional benefits.

- Emphasis on improved light output and beam control for superior nighttime visibility.

AI Impact Analysis on Automotive LED Headlight

The integration of Artificial Intelligence (AI) is set to revolutionize automotive LED headlight systems by enhancing their adaptive capabilities, predictive functions, and overall intelligence. Users are keenly interested in understanding how AI can make headlights smarter, safer, and more responsive to real-time driving conditions. Common questions revolve around AI's role in optimizing light distribution, recognizing road obstacles, and seamlessly interacting with advanced driver-assistance systems (ADAS). The primary expectation is that AI will move headlights beyond mere illumination, transforming them into proactive safety features that anticipate needs rather than just react to them. This involves complex algorithms processing sensor data to adjust beam patterns and intensity dynamically, providing an unprecedented level of control and precision.

AI's influence extends to enabling predictive lighting, where algorithms analyze navigation data, weather forecasts, and traffic conditions to pre-emptively adjust headlight settings before the driver encounters specific scenarios. For instance, AI can anticipate sharp turns or upcoming heavy rain and modify the beam pattern accordingly. Moreover, AI facilitates advanced object detection and recognition when integrated with vehicle cameras and sensors, allowing headlights to highlight pedestrians, cyclists, or wildlife more effectively, significantly boosting nighttime safety. This level of intelligent control also reduces driver fatigue by providing optimal visibility without manual adjustments. The continuous learning capabilities of AI systems could also lead to personalized lighting profiles based on driver habits and preferences, further enhancing the driving experience. Such advancements elevate headlights from simple components to crucial intelligent safety systems within the vehicle.

- AI enables predictive lighting, adjusting beams based on navigation, weather, and traffic data.

- Integration with ADAS for enhanced object detection and dynamic highlighting of road hazards.

- Optimized adaptive beam control for real-time adjustment of light patterns to avoid glare and maximize visibility.

- Potential for personalized lighting profiles based on driver behavior and environmental conditions.

- Facilitates advanced communication between headlights and other vehicle systems for holistic safety.

Key Takeaways Automotive LED Headlight Market Size & Forecast

The Automotive LED Headlight market is poised for robust expansion, driven by a confluence of technological advancements, increasing consumer awareness regarding safety, and stringent regulatory pressures mandating advanced lighting solutions. Users frequently inquire about the underlying factors contributing to this significant growth trajectory and what the future holds for this segment. The market's substantial projected CAGR underscores a strong shift from conventional lighting technologies to energy-efficient and highly functional LED systems across all vehicle categories. This growth is not merely volumetric but also indicative of an evolving landscape where innovation in lighting is a key competitive advantage for automotive manufacturers.

A primary takeaway is the accelerating adoption of LED headlights as standard equipment in new vehicle models, moving beyond their traditional presence only in luxury segments. This widespread integration is a testament to the cost-effectiveness and performance benefits of LEDs, which have become more accessible through manufacturing efficiencies and scale. The market forecast indicates sustained demand fueled by both OEM installations and a growing aftermarket for upgrades, particularly as older vehicle fleets seek to modernize their lighting systems. Furthermore, the report highlights that the emphasis on smart lighting, adaptive capabilities, and integration with autonomous driving technologies will be critical determinants of market growth, positioning LED headlights as integral components of future mobility solutions rather than mere accessories. The overall outlook is optimistic, reflecting a market that is mature enough to deliver reliable products yet dynamic enough for continuous innovation.

- Significant market growth projected, indicating strong industry confidence in LED technology.

- Shift towards LED headlights as standard equipment in a wider range of vehicle segments.

- Increasing consumer and regulatory demand for enhanced safety and energy efficiency.

- Technological advancements in adaptive and intelligent lighting systems are key growth drivers.

- OEM installations and aftermarket upgrades both contribute significantly to market expansion.

Automotive LED Headlight Market Drivers Analysis

The growth of the Automotive LED Headlight Market is primarily propelled by several key factors that converge to create a robust demand environment. One significant driver is the increasing emphasis on vehicle safety, where LED headlights offer superior illumination, clarity, and adaptive capabilities that significantly enhance visibility for drivers and reduce accident risks, particularly during nighttime or adverse weather conditions. Regulatory bodies worldwide are also playing a crucial role by introducing stricter lighting standards and promoting advanced lighting technologies, thereby compelling automotive manufacturers to integrate more sophisticated LED systems into their vehicles. This push for improved safety and compliance with evolving regulations ensures a foundational demand for LED headlights.

Furthermore, the aesthetic appeal and design flexibility offered by LED technology are becoming increasingly important for vehicle differentiation. LEDs allow for more compact and intricate headlight designs, contributing to the sleek and modern appearance of contemporary vehicles, which resonates strongly with consumer preferences. The rising trend of vehicle electrification also acts as a powerful driver; electric vehicles (EVs) benefit immensely from the high energy efficiency and lower power consumption of LEDs, which helps extend battery range. As the global automotive industry continues its pivot towards sustainable mobility, the inherent advantages of LED lighting in terms of energy efficiency and longevity make them an indispensable component for both traditional and electric vehicle platforms.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Advanced Safety Features | +3.5% | North America, Europe, Asia Pacific | 2025-2033 |

| Growing Automotive Production & Sales | +2.8% | Asia Pacific (China, India), Europe | 2025-2033 |

| Enhanced Energy Efficiency & Longevity of LEDs | +2.2% | Global, particularly EV markets | 2025-2033 |

| Technological Advancements in Adaptive Lighting | +2.0% | Europe, North America, Japan | 2025-2033 |

| Stringent Automotive Lighting Regulations | +1.5% | Europe, North America, China | 2025-2033 |

Automotive LED Headlight Market Restraints Analysis

Despite the robust growth trajectory, the Automotive LED Headlight market faces several notable restraints that could temper its expansion. One of the primary concerns is the relatively high manufacturing cost associated with LED headlight systems compared to conventional halogen or even Xenon HID lamps. The complexity of LED modules, which include multiple diodes, sophisticated control units, and advanced thermal management solutions, contributes significantly to their overall production expense. This higher cost can act as a barrier to adoption, particularly in budget-conscious vehicle segments or in developing markets where affordability is a crucial factor for consumers. While costs are declining with economies of scale, they still represent a hurdle for widespread penetration across all vehicle tiers.

Another significant restraint is the inherent complexity of thermal management for high-power LED arrays. LEDs generate heat, and effectively dissipating this heat is critical to maintaining their performance, longevity, and light output. Inadequate thermal management can lead to reduced efficiency, color shift, and premature failure of the LED components, posing a design challenge for manufacturers. Furthermore, the intricate nature of adaptive and matrix LED systems, which require precise calibration and integration with other vehicle sensors and software, adds to the complexity of development and production. Regulatory inconsistencies across different regions regarding the standards for adaptive lighting features can also complicate global market penetration, necessitating varied product designs or certifications, thereby increasing development costs and time-to-market. These factors collectively present challenges that stakeholders must address to ensure sustained market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Manufacturing Cost of LED Systems | -2.0% | Developing Economies, Budget Segments | 2025-2030 |

| Complex Thermal Management Requirements | -1.5% | Global | 2025-2033 |

| Design & Integration Complexity of Adaptive Systems | -1.0% | Global | 2025-2033 |

| Regulatory Hurdles & Standardization Issues | -0.8% | Specific Regions (e.g., North America vs. Europe) | 2025-2030 |

Automotive LED Headlight Market Opportunities Analysis

The Automotive LED Headlight market is rich with opportunities that can significantly accelerate its growth trajectory. One prominent avenue for expansion lies in the burgeoning electric vehicle (EV) segment. As EV production scales globally, the demand for highly efficient components that minimize power consumption and extend battery range will naturally favor LED lighting. LEDs, with their superior energy efficiency compared to traditional lighting, are becoming a standard choice for EV manufacturers, presenting a substantial growth opportunity as the automotive industry transitions to electrification. This trend is not limited to passenger EVs but also extends to commercial electric vehicles, further broadening the market scope.

Another significant opportunity resides in the aftermarket segment. As LED technology matures and its benefits become more widely recognized, vehicle owners are increasingly looking to upgrade their older vehicles with LED headlights to improve safety, aesthetics, and energy efficiency. The aftermarket offers a vast installed base of vehicles that can be retrofitted, presenting a substantial revenue stream for manufacturers and distributors of LED lighting solutions. Furthermore, the continuous innovation in smart lighting technologies, such as advanced adaptive driving beam (ADB) systems, projection capabilities, and integration with vehicle-to-everything (V2X) communication, opens up new functional possibilities and premium offerings. These advanced features can command higher price points and cater to the growing consumer demand for technologically sophisticated and intelligent vehicle components, thereby creating new market niches and enhancing profitability within the automotive lighting sector.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Penetration in Electric Vehicles (EVs) | +3.0% | Global (China, Europe, North America) | 2025-2033 |

| Growing Aftermarket Demand for LED Upgrades | +2.5% | North America, Europe, Asia Pacific | 2025-2033 |

| Development of Advanced & Smart Lighting Features | +2.0% | Global, particularly developed markets | 2025-2033 |

| Expansion into Emerging Markets & Mid-range Segments | +1.5% | Asia Pacific, Latin America, MEA | 2028-2033 |

Automotive LED Headlight Market Challenges Impact Analysis

The Automotive LED Headlight market, while promising, contends with several notable challenges that require strategic navigation by industry participants. One significant challenge is the intense competition among manufacturers, which often leads to price pressures and compressed profit margins. As LED technology becomes more commoditized and a greater number of players enter the market, differentiation becomes increasingly difficult, pushing companies to innovate rapidly while simultaneously managing costs. This competitive landscape demands continuous investment in research and development to stay ahead, which can be particularly challenging for smaller players with limited R&D budgets. The global supply chain also presents challenges, with potential disruptions impacting the availability and cost of critical components like semiconductor chips and specialized materials, which are essential for LED module production.

Another key challenge involves the rapid pace of technological evolution within the lighting sector. While innovation drives market growth, it also introduces the risk of rapid obsolescence for existing technologies and significant investment requirements for adopting new ones. Manufacturers must balance the need to innovate with the practicalities of mass production and market readiness. Furthermore, intellectual property (IP) disputes and patent infringements are becoming more prevalent given the complex technologies involved in advanced LED systems, potentially leading to costly legal battles and hindering market entry for new innovators. Ensuring global standardization for advanced features, such as adaptive driving beams, also remains a hurdle, as varying regional regulations can complicate product development and market expansion for multinational players. Addressing these multifaceted challenges is crucial for sustainable growth and long-term success in the dynamic automotive LED headlight market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition & Price Pressure | -1.8% | Global | 2025-2033 |

| Rapid Technological Obsolescence | -1.2% | Global | 2025-2033 |

| Supply Chain Vulnerabilities & Component Shortages | -1.0% | Global | 2025-2028 |

| Intellectual Property & Patent Disputes | -0.7% | Global | 2025-2033 |

Automotive LED Headlight Market - Updated Report Scope

This market research report provides a comprehensive analysis of the Automotive LED Headlight market, offering in-depth insights into its size, growth trends, segmentation, and competitive landscape. The scope encompasses detailed projections from 2025 to 2033, building upon historical data to provide a robust forecast. It meticulously examines the key drivers, restraints, opportunities, and challenges that shape the market, alongside an assessment of the impact of emerging technologies like Artificial Intelligence. The report aims to furnish stakeholders with actionable intelligence for strategic decision-making and investment planning within the dynamic automotive lighting industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.8 Billion |

| Market Forecast in 2033 | USD 11.45 Billion |

| Growth Rate | 14.5% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Hella GmbH & Co. KGaA, OSRAM GmbH, Continental AG, KOITO MANUFACTURING CO., LTD., Stanley Electric Co., Ltd., Valeo S.A., Lumileds Holding B.V., DENSO Corporation, Varroc Group, Aptiv PLC, ZKW Group GmbH, Ichikoh Industries, Ltd., Hyundai Mobis, Marelli (formerly Magneti Marelli), Motherson Automotive Technologies & Engineering |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive LED Headlight market is comprehensively segmented to provide a granular understanding of its diverse components and application areas. This segmentation helps in identifying specific growth pockets, understanding demand patterns across various vehicle types and technologies, and analyzing market dynamics at a detailed level. The primary segments include vehicle type, beam type, specific components comprising the LED headlight system, and the sales channel through which these products reach the end-users. Each segment reflects unique market characteristics, growth drivers, and competitive landscapes, contributing to the overall market complexity and opportunities.

The segmentation by vehicle type distinguishes between passenger cars and commercial vehicles, recognizing their distinct requirements and adoption rates for advanced lighting. Beam type segmentation highlights the evolution from standard low and high beams to more sophisticated Adaptive Driving Beam (ADB) systems, which represent the technological frontier. Furthermore, breaking down the market by component offers insights into the supply chain, from the fundamental LED chips and diodes to complex control units and thermal management solutions. Finally, the sales channel bifurcation into Original Equipment Manufacturer (OEM) and Aftermarket sales helps in assessing the primary installation market versus the replacement and upgrade market, providing a holistic view of the automotive LED headlight ecosystem and its multifaceted revenue streams.

- By Vehicle Type:

- Passenger Cars

- Commercial Vehicles

- By Beam Type:

- Low Beam

- High Beam

- Adaptive Driving Beam (ADB)

- By Component:

- LED Modules

- LED Chips/Diodes

- Heat Sinks

- Lenses

- Control Units

- By Sales Channel:

- Original Equipment Manufacturer (OEM)

- Aftermarket

Regional Highlights

- Asia Pacific (APAC): Expected to hold the largest market share due to high vehicle production volumes, rapid adoption of advanced technologies, and increasing disposable incomes in countries like China, India, Japan, and South Korea. Government initiatives promoting road safety and energy efficiency also contribute significantly to market growth in this region.

- Europe: A pioneer in automotive lighting technology and regulations, Europe is a key market for advanced LED headlights, particularly Adaptive Driving Beam (ADB) systems. Strict safety standards and a strong presence of premium automotive brands drive innovation and adoption of high-performance LED solutions.

- North America: Demonstrating robust growth, driven by consumer demand for advanced safety features, luxury vehicle sales, and the growing electric vehicle market. Regulatory harmonization with global standards, particularly for adaptive lighting, is expected to further accelerate market expansion.

- Latin America: An emerging market with increasing automotive production and a growing middle class, leading to rising demand for modern vehicle features, including LED headlights. Cost-effectiveness and government support for vehicle upgrades will be crucial for growth.

- Middle East and Africa (MEA): Projected to witness steady growth, fueled by increasing vehicle parc, infrastructure development, and growing consumer preference for feature-rich vehicles. Investments in automotive manufacturing and rising awareness of vehicle safety will contribute to market expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive LED Headlight Market.- Hella GmbH & Co. KGaA

- OSRAM GmbH

- Continental AG

- KOITO MANUFACTURING CO., LTD.

- Stanley Electric Co., Ltd.

- Valeo S.A.

- Lumileds Holding B.V.

- DENSO Corporation

- Varroc Group

- Aptiv PLC

- ZKW Group GmbH

- Ichikoh Industries, Ltd.

- Hyundai Mobis

- Marelli (formerly Magneti Marelli)

- Motherson Automotive Technologies & Engineering

Frequently Asked Questions

What is the projected growth rate of the Automotive LED Headlight Market?

The Automotive LED Headlight Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 14.5% between 2025 and 2033, demonstrating robust expansion.

What are the primary drivers for the Automotive LED Headlight Market?

Key drivers include increasing demand for enhanced vehicle safety, growing automotive production, improved energy efficiency and longevity of LEDs, technological advancements in adaptive lighting, and stringent automotive lighting regulations.

How does AI impact Automotive LED Headlight systems?

AI enhances headlights by enabling predictive lighting, optimizing adaptive beam control based on real-time conditions, and integrating with ADAS for advanced object detection, making systems smarter and more responsive.

Which regions are expected to dominate the Automotive LED Headlight Market?

Asia Pacific is expected to hold the largest market share due to high vehicle production and technology adoption, with Europe and North America also being significant markets driven by regulatory advancements and consumer demand for premium features.

What are the main challenges faced by the Automotive LED Headlight Market?

The primary challenges include high initial manufacturing costs, complex thermal management requirements, intense market competition, rapid technological obsolescence, and global supply chain vulnerabilities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted