Automotive Engine Cylinder Block Market

Automotive Engine Cylinder Block Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709811 | Last Updated : December 17, 2025 |

Format : ![]()

![]()

![]()

![]()

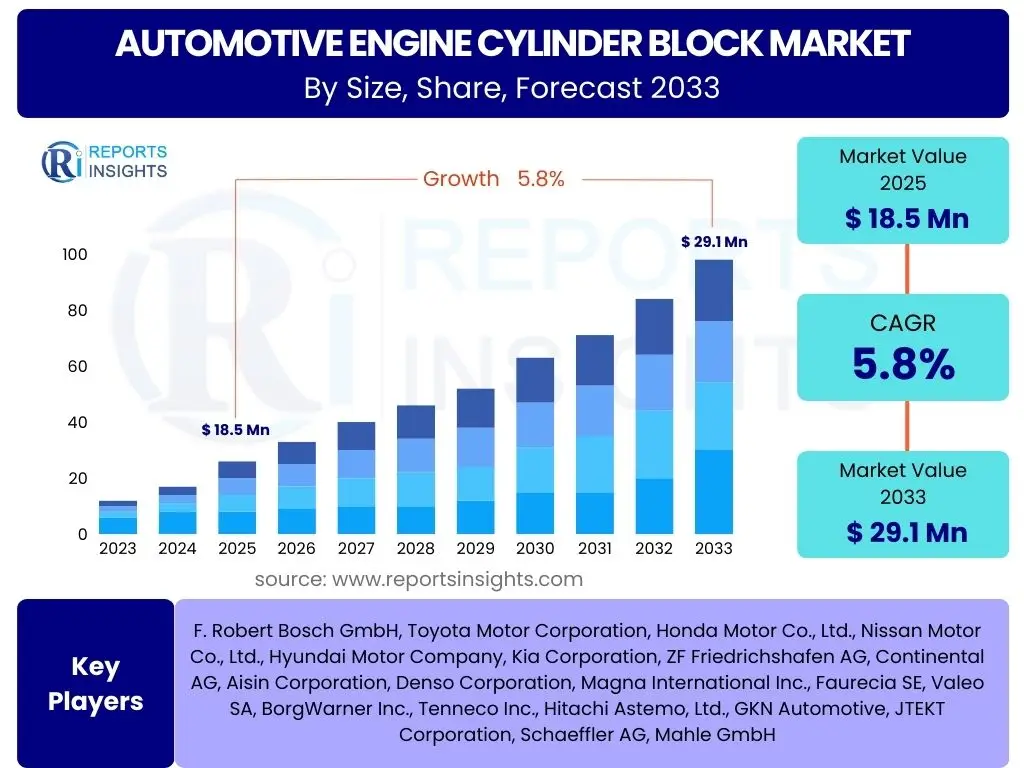

Automotive Engine Cylinder Block Market Size

According to Reports Insights Consulting Pvt Ltd, The Automotive Engine Cylinder Block Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 29.1 Billion by the end of the forecast period in 2033. This growth is driven by a confluence of factors including increasing global vehicle production, advancements in engine technologies, and a sustained demand for internal combustion engine (ICE) vehicles, particularly in emerging economies. Despite the rising adoption of electric vehicles, the aftermarket for engine components and the ongoing production of new ICE vehicles continue to fuel the cylinder block market's expansion.

The market's valuation reflects its critical role in the automotive industry, serving as the foundational component for all internal combustion engines. Demand is primarily influenced by both original equipment manufacturers (OEMs) and the aftermarket segment. Technological innovations in material science and manufacturing processes are enabling the production of lighter, more durable, and fuel-efficient cylinder blocks, which are essential for meeting stringent emission standards and consumer expectations for performance and economy. The long lifespan of vehicles and the necessity for replacement parts further bolster the market's stability and consistent growth trajectory over the forecast period.

Key Automotive Engine Cylinder Block Market Trends & Insights

Common user inquiries regarding the Automotive Engine Cylinder Block market trends often center on material innovations, lightweighting strategies, manufacturing advancements, and the impact of evolving powertrain technologies. Users frequently ask about the shift from traditional cast iron to aluminum alloys, the emergence of advanced casting techniques, and how global emission regulations are shaping design and production. There is also significant interest in the role of hybridization and the continued relevance of internal combustion engines, especially in commercial vehicles and certain passenger car segments, amidst the electrification push. These questions highlight a market grappling with legacy technology evolution and future sustainability demands.

Another prevalent area of interest involves the integration of digitalization in cylinder block manufacturing, including advanced simulation and rapid prototyping. Stakeholders are keen to understand how these technologies contribute to shorter development cycles, improved product quality, and cost efficiency. The longevity and repairability of cylinder blocks also feature prominently, with users exploring advancements in repair techniques and the availability of robust aftermarket solutions. These insights reveal a market that is mature yet dynamic, constantly adapting to technological shifts, regulatory pressures, and environmental considerations while striving for optimal performance and efficiency.

- Lightweighting through Advanced Materials: Increasing adoption of aluminum alloys (e.g., Al-Si alloys) and other composite materials over traditional cast iron to reduce vehicle weight, improve fuel efficiency, and lower emissions, driven by stringent environmental regulations.

- Enhanced Manufacturing Processes: Development and implementation of advanced casting techniques such as high-pressure die casting, squeeze casting, and lost-foam casting, alongside additive manufacturing for prototypes, leading to greater precision, structural integrity, and reduced waste.

- Modular Engine Architectures: Trend towards modular engine designs that allow for greater flexibility in production and customization, enabling manufacturers to efficiently produce different engine variants from a common cylinder block platform, thereby optimizing costs and scalability.

- Thermal Management Optimizations: Focus on integrating sophisticated cooling channels and innovative surface treatments within cylinder blocks to enhance thermal management, leading to improved engine performance, durability, and fuel economy.

- Electrification and Hybridization Impact: While full electrification gains momentum, the continued development of highly efficient internal combustion engines for hybrid vehicles and segments where battery electric vehicles are not yet fully viable sustains demand for advanced cylinder block designs.

- Digitalization in Design and Simulation: Increased use of CAE (Computer-Aided Engineering) tools, CFD (Computational Fluid Dynamics), and finite element analysis (FEA) for virtual prototyping, performance prediction, and structural optimization of cylinder blocks, reducing development time and costs.

AI Impact Analysis on Automotive Engine Cylinder Block

User queries regarding the impact of AI on the Automotive Engine Cylinder Block market frequently revolve around its application in design optimization, predictive maintenance, and advanced manufacturing processes. Users are keen to understand how AI can enhance the structural integrity and thermal efficiency of cylinder blocks, reduce material waste, and streamline production. Questions often explore AI's potential in simulating complex engine conditions, identifying design flaws early, and improving the overall longevity and performance of internal combustion engines. This highlights a strong interest in AI's capability to drive efficiency and innovation in a traditionally hardware-centric domain.

Furthermore, concerns and expectations surface about AI's role in quality control, anomaly detection during manufacturing, and supply chain optimization for cylinder block components. Stakeholders inquire about the feasibility of AI-powered systems to monitor production lines, predict equipment failures, and ensure consistent product quality, which are critical for high-volume automotive manufacturing. The discussion often extends to how AI might influence material selection, cost reduction, and the acceleration of R&D cycles for next-generation cylinder block designs, positioning AI as a transformative force capable of addressing both current manufacturing challenges and future performance demands.

- Design Optimization and Generative Design: AI algorithms can rapidly iterate through thousands of design variations for cylinder blocks, optimizing for factors like weight, strength, thermal efficiency, and manufacturability, far beyond human capabilities. This leads to lighter, more durable, and efficient designs.

- Predictive Maintenance for Manufacturing Equipment: AI-powered sensors and analytics can monitor the health of casting machines, CNC tools, and other manufacturing equipment used in cylinder block production. This enables predictive maintenance, reducing unplanned downtime, improving operational efficiency, and extending machine lifespans.

- Enhanced Quality Control and Anomaly Detection: AI-driven vision systems and sensors can inspect cylinder blocks during various stages of manufacturing, identifying microscopic defects, surface imperfections, or material inconsistencies with greater accuracy and speed than human inspectors.

- Material Science and Alloy Development: AI can accelerate the discovery and optimization of new materials and alloys for cylinder blocks, predicting their properties and performance under specific conditions, leading to novel lightweight and high-strength compositions.

- Supply Chain Optimization: AI can analyze complex supply chain data to optimize inventory levels, forecast demand for raw materials and finished cylinder blocks, and mitigate risks, leading to more resilient and cost-effective production.

- Process Optimization in Casting and Machining: Machine learning models can fine-tune parameters in casting and machining processes to reduce defects, improve surface finish, and minimize material waste, thereby increasing yield and efficiency.

- Simulation and Virtual Prototyping: AI enhances advanced simulation tools by making them more accurate and efficient, allowing engineers to virtually test cylinder block performance under extreme conditions, reducing the need for costly physical prototypes.

Key Takeaways Automotive Engine Cylinder Block Market Size & Forecast

User inquiries about the key takeaways from the Automotive Engine Cylinder Block market size and forecast frequently highlight a desire to understand the fundamental drivers of growth, the resilience of the market in the face of EV adoption, and the primary factors influencing its trajectory. There is a strong interest in discerning how material innovations, manufacturing efficiencies, and global economic shifts contribute to the market's overall health. Users typically seek clear, actionable insights into where growth opportunities lie and what challenges might impede market expansion over the forecast period, often contrasting traditional market influences with emerging technological and environmental pressures.

Another common theme in user questions concerns the interplay between OEM demand and the aftermarket segment, and their respective contributions to the market's projected value. Stakeholders often want to know which regions are poised for significant growth and why, as well as the types of cylinder blocks (e.g., aluminum vs. cast iron) that are expected to dominate. These inquiries underscore the need for a holistic view of the market, combining quantitative projections with qualitative analysis of underlying dynamics to provide a comprehensive understanding of its future landscape.

- Steady Growth Despite Electrification: The Automotive Engine Cylinder Block market is projected for consistent growth with a 5.8% CAGR, reaching USD 29.1 Billion by 2033, demonstrating resilience driven by robust ICE vehicle production in emerging markets and a strong aftermarket.

- Material Innovation as a Growth Catalyst: The shift towards lightweight materials like aluminum alloys is a primary driver, enhancing fuel efficiency and reducing emissions, crucial for meeting global regulatory standards and consumer demand for performance.

- Advanced Manufacturing Essential for Competitiveness: Adoption of advanced casting and machining techniques, along with digitalization, is critical for achieving precision, reducing costs, and improving product quality, underpinning market competitiveness.

- Emerging Economies as Key Growth Hubs: Asia Pacific, particularly China and India, will remain pivotal for market expansion due to increasing vehicle production and rising disposable incomes fueling demand for internal combustion engine vehicles.

- Aftermarket Sustains Demand: A significant portion of market revenue will continue to be generated from the aftermarket segment, driven by the vast installed base of ICE vehicles globally requiring maintenance and replacement parts.

- Regulatory Landscape Shapes Design: Stricter global emission norms (e.g., Euro 7, CAFE standards) compel continuous innovation in cylinder block design and manufacturing to achieve higher engine efficiency and lower pollutant output.

- AI and Digitalization for Future Efficiency: The integration of Artificial Intelligence in design, simulation, and manufacturing processes will be crucial for optimizing cylinder block performance, accelerating R&D, and enhancing production efficiency.

Automotive Engine Cylinder Block Market Drivers Analysis

The Automotive Engine Cylinder Block market is significantly propelled by the sustained demand for internal combustion engine (ICE) vehicles, particularly in developing economies where vehicle ownership is rapidly expanding. While electric vehicles gain traction in developed regions, the global fleet of ICE vehicles continues to grow, driven by affordability, existing infrastructure, and consumer preferences. This enduring demand necessitates a steady supply of cylinder blocks for new vehicle production and, crucially, for the extensive aftermarket for maintenance and repairs over the long lifespan of these vehicles.

Furthermore, stringent global emission regulations and the continuous push for improved fuel efficiency act as powerful drivers for innovation within the cylinder block market. Manufacturers are compelled to invest in research and development to produce lighter, more durable, and thermally efficient cylinder blocks that can support advanced engine technologies. This involves adopting new materials, such as aluminum alloys and composites, and employing sophisticated manufacturing processes that result in precision-engineered components capable of meeting stringent performance and environmental standards. The pursuit of enhanced engine performance and reduced environmental impact directly stimulates advancements in cylinder block technology.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increased Global Vehicle Production (ICE) | +1.5% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

| Stringent Emission Regulations | +1.2% | Europe, North America, Asia Pacific (China, India) | Medium to Long-term (2025-2033) |

| Demand for Lightweight Vehicles | +1.0% | Global | Long-term (2025-2033) |

| Technological Advancements in Materials & Manufacturing | +0.8% | Global | Long-term (2025-2033) |

| Growing Automotive Aftermarket | +0.7% | Global | Long-term (2025-2033) |

Automotive Engine Cylinder Block Market Restraints Analysis

A primary restraint on the Automotive Engine Cylinder Block market is the accelerating global shift towards electric vehicles (EVs). Governments worldwide are implementing policies and incentives to promote EV adoption, leading to significant investments in EV infrastructure and manufacturing. As EV production scales up and battery technology improves, the demand for internal combustion engines, and consequently their core components like cylinder blocks, is expected to gradually decline in certain key markets over the long term. This transition poses a significant challenge for manufacturers heavily invested in ICE component production, necessitating strategic diversification and adaptation.

Moreover, the high capital investment required for establishing and upgrading manufacturing facilities for cylinder blocks, especially for advanced materials and sophisticated casting techniques, acts as another restraint. The automotive industry operates on tight margins and demanding quality standards, making it challenging for new entrants or smaller players to compete without substantial financial backing. Additionally, volatility in raw material prices, particularly for metals like aluminum and iron, can impact production costs and profit margins, creating financial pressure on manufacturers and potentially dampening market growth. These factors contribute to a cautious investment environment and may slow innovation in some segments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Growth of Electric Vehicles (EVs) | -1.8% | North America, Europe, China | Medium to Long-term (2025-2033) |

| High Manufacturing Costs and Capital Investment | -0.9% | Global | Long-term (2025-2033) |

| Volatility in Raw Material Prices | -0.7% | Global | Short to Medium-term (2025-2029) |

| Supply Chain Disruptions | -0.5% | Global | Short-term (2025-2027) |

Automotive Engine Cylinder Block Market Opportunities Analysis

Significant opportunities exist in the continued innovation of material science for cylinder blocks, particularly in developing lightweight and high-strength alloys. The relentless demand for improved fuel efficiency and reduced emissions creates a strong impetus for manufacturers to explore novel aluminum, magnesium, and even composite materials that can offer superior performance characteristics while lowering overall engine weight. Companies that invest in advanced metallurgy and material engineering can gain a substantial competitive edge by meeting the evolving needs of engine designers and vehicle manufacturers, contributing to more sustainable and efficient automotive solutions.

Furthermore, the expanding aftermarket segment, especially in regions with a large and aging fleet of ICE vehicles, presents a robust growth opportunity. As vehicles remain on the road for longer periods, the demand for replacement cylinder blocks and components for repairs and refurbishment will continue to grow. Manufacturers can capitalize on this by strengthening their aftermarket distribution networks, offering high-quality replacement parts, and potentially exploring remanufacturing initiatives. This ensures a steady revenue stream independent of new vehicle sales trends, providing market stability and extending the product lifecycle beyond initial OEM installations.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Lightweight Materials | +1.3% | Global | Long-term (2025-2033) |

| Growth in Aftermarket Demand for Replacement Parts | +1.0% | Asia Pacific, North America, Europe | Long-term (2025-2033) |

| Technological Integration (AI, IoT, Digital Twins) in Manufacturing | +0.8% | Global | Medium to Long-term (2025-2033) |

| Expansion in Hybrid Vehicle Production | +0.6% | Europe, North America, Asia Pacific | Medium-term (2025-2030) |

| Localized Production in Emerging Markets | +0.5% | Asia Pacific, Latin America | Long-term (2025-2033) |

Automotive Engine Cylinder Block Market Challenges Impact Analysis

A significant challenge confronting the Automotive Engine Cylinder Block market is the ongoing pressure from rapidly evolving emission regulations globally. Governments are continuously tightening standards for particulate matter, NOx, and CO2 emissions, which necessitates profound and costly redesigns of internal combustion engines and their components. Cylinder block manufacturers must innovate to support engines that burn fuel more cleanly and efficiently, often requiring complex integration of advanced cooling systems, sophisticated geometries, and specialized surface treatments. Meeting these ever-increasing regulatory hurdles demands substantial R&D investment and can slow down market introduction of new engine designs.

Another prominent challenge is the increasing complexity of engine designs, driven by the demand for higher power density, improved fuel economy, and lower emissions. Modern cylinder blocks are no longer simple castings but intricate components integrating multiple functions and requiring extremely high precision in manufacturing. This complexity extends to thermal management, friction reduction, and noise, vibration, and harshness (NVH) mitigation, all of which impact cylinder block design. The intricate balance of these factors requires advanced engineering capabilities and stringent quality control, adding to manufacturing costs and potentially increasing development cycles for new products.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Emission Regulations and Compliance Costs | -1.3% | Global | Long-term (2025-2033) |

| Increasing Complexity of Engine Designs | -1.0% | Global | Medium to Long-term (2025-2033) |

| Competition from Alternative Powertrains | -0.8% | Developed Markets (Europe, North America) | Long-term (2025-2033) |

| Skilled Labor Shortage in Advanced Manufacturing | -0.6% | North America, Europe, parts of Asia Pacific | Medium to Long-term (2025-2033) |

Automotive Engine Cylinder Block Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Automotive Engine Cylinder Block market, covering historical data from 2019 to 2023 and offering detailed forecasts up to 2033. It meticulously examines market dynamics, including key growth drivers, significant restraints, emerging opportunities, and critical challenges impacting the industry landscape. The report provides a granular segmentation analysis based on material type, engine type, vehicle type, and manufacturing process, offering stakeholders a clear understanding of market evolution across various dimensions. Furthermore, it includes a thorough regional analysis to highlight geographical trends and competitive landscapes, along with profiles of leading market participants to provide insights into their strategies and market positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 29.1 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | F. Robert Bosch GmbH, Toyota Motor Corporation, Honda Motor Co., Ltd., Nissan Motor Co., Ltd., Hyundai Motor Company, Kia Corporation, ZF Friedrichshafen AG, Continental AG, Aisin Corporation, Denso Corporation, Magna International Inc., Faurecia SE, Valeo SA, BorgWarner Inc., Tenneco Inc., Hitachi Astemo, Ltd., GKN Automotive, JTEKT Corporation, Schaeffler AG, Mahle GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Engine Cylinder Block market is extensively segmented to provide a detailed understanding of its diverse landscape. Key segmentation categories include material type, engine type, vehicle type, and manufacturing process. Each segment reflects unique demand patterns, technological preferences, and growth trajectories. For instance, the material segment differentiates between traditional cast iron and advanced aluminum alloys, highlighting the industry's shift towards lighter and more efficient components. Understanding these segments is crucial for stakeholders to identify specific growth areas and tailor their product development and market strategies effectively.

Further granularity is achieved by segmenting based on engine configurations like inline and V-engines, which have distinct design requirements and market prevalence. The vehicle type segment, encompassing passenger cars and commercial vehicles, reflects varying demands in terms of durability, power, and cost efficiency. Lastly, the manufacturing process segment provides insights into the adoption of advanced casting and machining technologies, which are pivotal for achieving precision and mass production efficiency. This multi-dimensional segmentation allows for a comprehensive assessment of the market's current state and future potential, enabling targeted investment and innovation.

- By Material:

- Aluminum Alloy: Dominating new vehicle production due to lightweighting and superior thermal conductivity for enhanced fuel efficiency and emissions reduction.

- Cast Iron: Retains significant share, particularly in heavy-duty commercial vehicles and some passenger cars, favored for its durability, cost-effectiveness, and NVH characteristics.

- Others (e.g., Composites): Emerging materials with niche applications, offering potential for further weight reduction and performance improvements, though adoption is limited by cost and manufacturing complexity.

- By Engine Type:

- Inline Engines: Most common configuration, especially for 3 and 4-cylinder passenger cars and light commercial vehicles, known for simplicity and compact design.

- V-Engines: Used in higher-performance passenger cars and heavy commercial vehicles, offering better balance and higher power output in a compact length.

- Flat Engines: Niche application in sports cars and some utility vehicles, characterized by low center of gravity.

- Rotary Engines: Very limited production, noted for their compact size and unique power delivery characteristics.

- By Vehicle Type:

- Passenger Cars: Largest segment, driven by global sales volumes and the continuous demand for fuel-efficient and performance-oriented engines.

- Commercial Vehicles (Light): Includes vans and light trucks, where durability and efficiency are key, often utilizing robust inline engines.

- Commercial Vehicles (Heavy): Encompasses heavy trucks and buses, demanding exceptionally durable and high-output cylinder blocks, predominantly cast iron or specialized aluminum.

- By Manufacturing Process:

- Casting: Primary method, subdivided into Sand Casting (versatile for complex shapes, lower volume), Die Casting (high volume, high precision for aluminum), Lost-Foam Casting (complex geometries, good surface finish), and Squeeze Casting (improved mechanical properties).

- Machining: Essential post-casting process for achieving precise dimensions, surface finish, and functional features of the cylinder block.

- Others (e.g., Forging): Niche applications for specific engine components or high-stress areas.

- By Sales Channel:

- OEM (Original Equipment Manufacturer): Sales to vehicle manufacturers for new vehicle assembly, representing the largest share of the market.

- Aftermarket: Sales of replacement cylinder blocks and components for maintenance, repair, and refurbishment of existing vehicles, a steady and growing segment.

Regional Highlights

- North America: This region exhibits a mature automotive market with a strong emphasis on reducing emissions and increasing fuel efficiency. The demand for lightweight aluminum cylinder blocks is high, driven by stringent CAFE standards and consumer preference for powerful yet efficient engines, particularly in SUVs and light trucks. The aftermarket segment also remains robust due to a large installed base of vehicles and a culture of vehicle maintenance.

- Europe: Europe is at the forefront of emission regulation with initiatives like Euro 7, compelling automakers to integrate highly advanced engine technologies. This translates into a strong demand for innovative cylinder block designs, often employing sophisticated thermal management and lighter materials. While the shift to electric vehicles is rapid, the market for efficient ICE and hybrid engine components, including cylinder blocks, continues to evolve technologically.

- Asia Pacific (APAC): APAC represents the largest and fastest-growing market for automotive engine cylinder blocks, primarily fueled by the substantial vehicle production in China, India, Japan, and South Korea. Rising disposable incomes, increasing urbanization, and expanding middle-class populations in these countries are driving robust demand for both passenger and commercial vehicles. This region is also a major hub for manufacturing, with significant investments in both traditional and advanced production technologies for cylinder blocks.

- Latin America: The market in Latin America is characterized by steady growth in vehicle production, with a focus on affordable and durable vehicles. While material innovation is present, cost-effectiveness often drives decisions. Brazil and Mexico are key markets, with a growing demand for both new vehicles and a significant aftermarket for maintenance and repair parts. Economic stability and industrial growth are critical factors influencing market expansion.

- Middle East and Africa (MEA): This region shows a nascent but growing automotive industry, with demand influenced by infrastructure development and increasing vehicle ownership. The market for cylinder blocks is largely driven by imports and local assembly operations, with a strong aftermarket presence due to the prevalence of older vehicles. Investments in manufacturing capabilities are gradually increasing, offering future growth potential.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Engine Cylinder Block Market.- F. Robert Bosch GmbH

- Toyota Motor Corporation

- Honda Motor Co., Ltd.

- Nissan Motor Co., Ltd.

- Hyundai Motor Company

- Kia Corporation

- ZF Friedrichshafen AG

- Continental AG

- Aisin Corporation

- Denso Corporation

- Magna International Inc.

- Faurecia SE

- Valeo SA

- BorgWarner Inc.

- Tenneco Inc.

- Hitachi Astemo, Ltd.

- GKN Automotive

- JTEKT Corporation

- Schaeffler AG

- Mahle GmbH

Frequently Asked Questions

Analyze common user questions about the Automotive Engine Cylinder Block market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Automotive Engine Cylinder Block Market?

The Automotive Engine Cylinder Block Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, reaching an estimated USD 29.1 Billion by 2033.

How do emission regulations influence the cylinder block market?

Stringent emission regulations drive innovation towards lightweight materials like aluminum alloys and advanced designs, ensuring cylinder blocks support more fuel-efficient and lower-emission internal combustion engines.

What role do advanced materials play in the market?

Advanced materials, particularly aluminum alloys, are crucial for lightweighting vehicles, which improves fuel efficiency and reduces CO2 emissions, making them a primary driver for new cylinder block designs.

How does the rise of electric vehicles impact this market?

The rapid growth of electric vehicles poses a significant long-term restraint on the demand for internal combustion engine components, including cylinder blocks, particularly in developed automotive markets.

Which region is expected to lead market growth?

The Asia Pacific region, especially countries like China and India, is anticipated to lead market growth due to increasing vehicle production, rising disposable incomes, and expanding automotive industries.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted