Automotive Diagnostic Scan Tool Market

Automotive Diagnostic Scan Tool Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704626 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

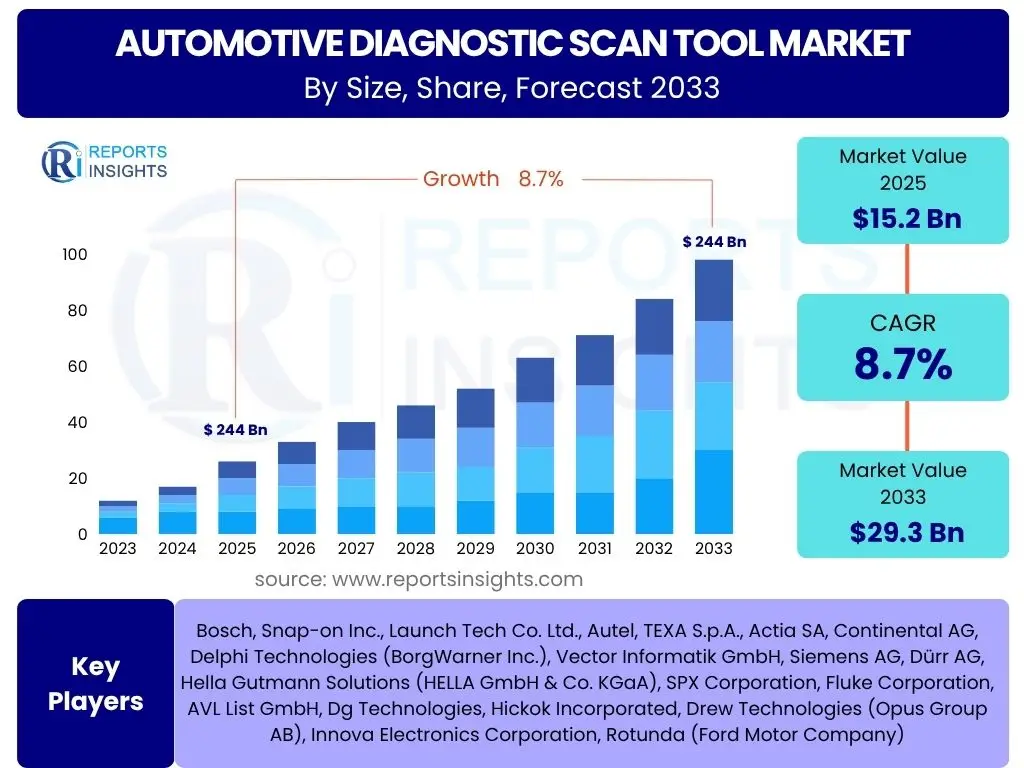

Automotive Diagnostic Scan Tool Market Size

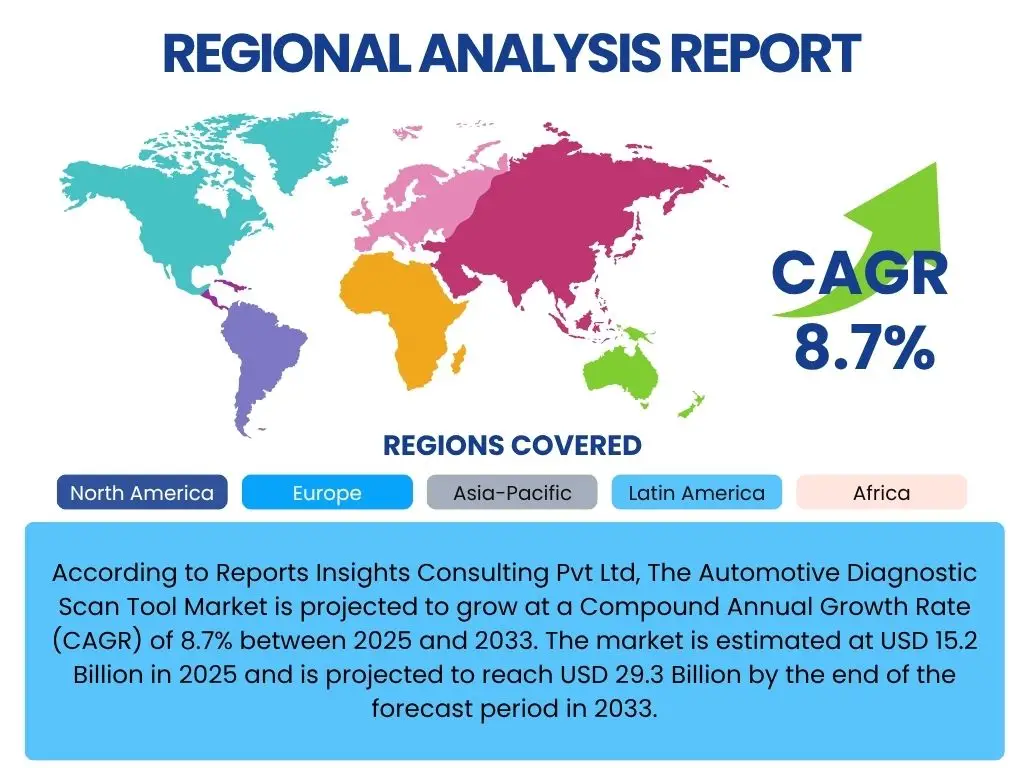

According to Reports Insights Consulting Pvt Ltd, The Automotive Diagnostic Scan Tool Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 29.3 Billion by the end of the forecast period in 2033.

Key Automotive Diagnostic Scan Tool Market Trends & Insights

The Automotive Diagnostic Scan Tool market is experiencing significant evolution driven by advancements in vehicle technology and the increasing complexity of automotive systems. Key user inquiries frequently revolve around the impact of vehicle electrification, the integration of advanced driver-assistance systems (ADAS), and the shift towards software-defined vehicles on diagnostic requirements. There is a strong interest in how diagnostic tools are adapting to these changes, particularly concerning their ability to perform remote diagnostics, over-the-air (OTA) updates, and handle cyber-physical security challenges.

Furthermore, the market is witnessing a trend towards more intuitive, user-friendly interfaces and enhanced connectivity features that allow for seamless data sharing and integration with workshop management systems. Users are also keen on understanding the role of artificial intelligence and machine learning in predictive maintenance and guided diagnostics. The increasing adoption of cloud-based solutions and subscription models for software updates and technical information is another area of significant curiosity, reflecting a move away from traditional one-time purchases towards ongoing service models.

- Increased integration with Advanced Driver-Assistance Systems (ADAS) for calibration and diagnostics.

- Rising demand for wireless and cloud-based diagnostic solutions.

- Growing adoption of Artificial Intelligence (AI) and Machine Learning (ML) for predictive maintenance and guided diagnostics.

- Emphasis on cybersecurity features in diagnostic tools due to connected vehicle risks.

- Development of specialized tools for Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs).

- Shift towards software-as-a-service (SaaS) and subscription-based models for software updates and technical data.

- Enhanced user interfaces (UI) and user experience (UX) for ease of use and efficiency.

AI Impact Analysis on Automotive Diagnostic Scan Tool

User queries regarding the impact of Artificial Intelligence (AI) on the Automotive Diagnostic Scan Tool market frequently explore how AI can enhance diagnostic accuracy, reduce repair times, and provide more proactive maintenance solutions. There is considerable interest in AI's capability to analyze vast amounts of vehicle data, identify subtle anomalies, and predict potential failures before they occur. Users are also curious about AI-powered guided diagnostics, where the system suggests troubleshooting steps, identifies probable causes based on symptom input, and even recommends specific repair procedures, thereby assisting technicians of varying skill levels.

AI's influence extends to enabling more sophisticated data analysis for fleet management, optimizing repair shop operations, and facilitating the development of self-diagnosing vehicles. Concerns often arise regarding data privacy and the ethical implications of AI's use in vehicle diagnostics, as well as the need for robust cybersecurity measures to protect sensitive vehicle data. Despite these considerations, the overarching expectation is that AI will revolutionize the diagnostic process, making it more efficient, precise, and less reliant on manual interpretation, ultimately leading to improved vehicle reliability and reduced operational costs.

- Enables predictive diagnostics by analyzing vehicle data patterns to anticipate failures.

- Powers guided troubleshooting, offering step-by-step repair recommendations.

- Facilitates advanced anomaly detection for intermittent or complex issues.

- Improves diagnostic accuracy by learning from a vast database of repair cases.

- Supports natural language processing for more intuitive human-tool interaction.

- Optimizes parts ordering and inventory management through predictive insights.

- Contributes to the development of autonomous vehicle diagnostic capabilities.

Key Takeaways Automotive Diagnostic Scan Tool Market Size & Forecast

The Automotive Diagnostic Scan Tool market is poised for robust expansion, reflecting the increasing technological sophistication of modern vehicles and the escalating demand for efficient and accurate diagnostic solutions. A primary takeaway is the consistent growth trajectory, driven by factors such as the proliferation of complex electronic systems, the ongoing integration of advanced driver-assistance systems (ADAS), and the global shift towards electric and hybrid vehicles, all of which necessitate specialized and frequently updated diagnostic capabilities. The forecast underscores a market that is not only expanding in volume but also evolving in terms of technological depth and breadth, moving towards more intelligent, connected, and integrated solutions.

Another crucial insight is the growing emphasis on software-driven diagnostics and the emergence of new business models, such as subscription services for diagnostic data and software updates. This shift highlights a move from traditional hardware-centric sales to a more service-oriented approach, ensuring tools remain current with rapidly changing vehicle technologies. Furthermore, the market's trajectory is heavily influenced by the imperative for cybersecurity in diagnostic processes, given the increasing connectivity of vehicles, and the continuous need for skilled technicians capable of operating these advanced tools, which presents both opportunities and challenges for industry stakeholders.

- Significant market growth anticipated, driven by vehicle technology evolution.

- Shift towards software-centric and connected diagnostic solutions.

- Increasing demand for specialized tools for electric and hybrid vehicles.

- Emergence of subscription models for diagnostic software and data.

- Cybersecurity and data integrity becoming critical considerations for tool development.

- Continuous need for technician training to keep pace with tool advancements.

- Market expansion influenced by both OEM and aftermarket segment demands.

Automotive Diagnostic Scan Tool Market Drivers Analysis

The Automotive Diagnostic Scan Tool market is propelled by several potent drivers, primarily the escalating complexity of modern vehicles. As vehicles integrate more electronic control units (ECUs), sensors, and advanced systems like ADAS, the need for sophisticated diagnostic tools to identify and resolve issues accurately becomes paramount. This complexity reduces the effectiveness of traditional manual troubleshooting and necessitates precise, digital diagnostic capabilities. Furthermore, the global growth in vehicle parc, particularly in developing economies, continuously expands the base of vehicles requiring routine maintenance and occasional repairs, thereby fueling the demand for diagnostic tools across both OEM and independent repair sectors.

Another significant driver is the stringent emission regulations being imposed worldwide. These regulations mandate regular vehicle inspections and maintenance to ensure compliance, which often relies on diagnostic tools to monitor engine performance, emission levels, and identify any faults. The proliferation of connected vehicles and the increasing interest in predictive maintenance also serve as strong catalysts. Connected vehicles generate vast amounts of data that, when analyzed by diagnostic tools, can enable proactive maintenance, reduce downtime, and improve overall vehicle efficiency, shifting the industry from reactive repairs to preventative service models.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Vehicle Complexity & Electronics | +2.1% | Global, particularly North America, Europe, Asia Pacific | 2025-2033 |

| Rising Vehicle Production & Sales | +1.8% | Asia Pacific (China, India), North America, Europe | 2025-2033 |

| Stringent Emission Regulations | +1.5% | Europe, North America, Asia Pacific (e.g., China, Japan) | 2025-2033 |

| Growth of Connected Car Technology | +1.3% | Global, high in developed markets | 2025-2033 |

| Demand for Predictive Maintenance | +1.0% | Global, particularly commercial fleets, high-end vehicles | 2026-2033 |

Automotive Diagnostic Scan Tool Market Restraints Analysis

Despite the positive growth trajectory, the Automotive Diagnostic Scan Tool market faces several significant restraints that could temper its expansion. One primary concern is the high initial cost associated with acquiring advanced diagnostic tools, especially those equipped with specialized software for electric vehicles (EVs) or complex ADAS systems. This upfront investment can be prohibitive for smaller independent repair shops or individual mechanics, limiting their ability to upgrade to the latest technology and potentially creating a disparity in service capabilities across the market. Furthermore, the ongoing costs of software licenses, subscriptions for technical data, and regular updates add to the operational expenditure, which can deter some users.

Another considerable restraint is the rapid obsolescence of diagnostic hardware and software due to the fast pace of technological innovation in the automotive industry. As new vehicle models are introduced with updated architectures and communication protocols, older diagnostic tools can quickly become incompatible or require costly upgrades, forcing users into a continuous investment cycle. Additionally, the lack of skilled technicians capable of effectively utilizing and interpreting the data from highly sophisticated diagnostic tools poses a significant challenge. This skills gap necessitates substantial training and re-training efforts, which can be time-consuming and expensive for workshops, potentially slowing down the adoption of advanced diagnostic solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment & Recurring Software Costs | -1.2% | Global, more pronounced in developing regions | 2025-2033 |

| Rapid Technological Obsolescence | -0.9% | Global, particularly markets with high tech adoption | 2025-2033 |

| Shortage of Skilled Technicians | -0.8% | Global, especially pronounced in emerging markets | 2025-2033 |

| Data Security and Privacy Concerns | -0.6% | Europe (GDPR), North America, Asia Pacific | 2025-2033 |

| Software Piracy & Counterfeit Tools | -0.5% | Emerging markets, global aftermarket | 2025-2033 |

Automotive Diagnostic Scan Tool Market Opportunities Analysis

The Automotive Diagnostic Scan Tool market is abundant with opportunities, largely stemming from the ongoing transformation of the automotive sector. The rapid global adoption of Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs) presents a significant growth avenue. These vehicles possess unique architectures, battery management systems, and high-voltage components that require specialized diagnostic tools, creating a new segment within the market. Manufacturers who innovate to meet these specific diagnostic needs stand to gain a competitive edge. Furthermore, the increasing integration of telematics and connected car technologies opens doors for remote diagnostics and over-the-air (OTA) updates, allowing issues to be addressed without a physical visit to a workshop, enhancing convenience and efficiency.

Emerging markets, particularly in Asia Pacific and Latin America, represent substantial untapped potential due to their expanding vehicle populations and developing automotive infrastructures. As disposable incomes rise and vehicle ownership increases in these regions, so too will the demand for efficient and accessible diagnostic services. Moreover, the growing interest in predictive maintenance, fueled by advancements in Artificial Intelligence (AI) and Machine Learning (ML), offers an opportunity for tool manufacturers to develop more intelligent, data-driven solutions that can anticipate failures, optimize service schedules, and reduce unexpected breakdowns. The shift towards subscription-based models for software and data access also creates recurring revenue streams and fosters long-term customer relationships, moving beyond one-time hardware sales.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in EV & HEV Market | +1.9% | Global, strong in Europe, China, North America | 2025-2033 |

| Expansion in Emerging Markets | +1.6% | Asia Pacific (India, Southeast Asia), Latin America, MEA | 2025-2033 |

| Advancements in AI & Predictive Diagnostics | +1.4% | Global, particularly developed markets | 2026-2033 |

| Remote Diagnostics & Telematics Integration | +1.2% | Global, for fleets and connected vehicles | 2025-2033 |

| Subscription & SaaS Business Models | +1.0% | Global, across all market segments | 2025-2033 |

Automotive Diagnostic Scan Tool Market Challenges Impact Analysis

The Automotive Diagnostic Scan Tool market confronts several challenges that necessitate strategic responses from industry players. A significant hurdle is the issue of interoperability, where diagnostic tools from one manufacturer may not seamlessly interact with vehicles or components from another, leading to fragmented solutions and inefficiencies for repair shops that service multiple brands. This challenge is exacerbated by the proprietary nature of some vehicle diagnostic protocols, which can restrict access for third-party tool providers. The need for continuous and costly software updates to keep pace with rapid advancements in vehicle technology and evolving diagnostic protocols also represents a substantial financial and operational challenge for tool users, particularly smaller independent garages.

Cybersecurity threats pose an increasingly critical challenge, as connected diagnostic tools can become potential entry points for malicious actors seeking to compromise vehicle systems or steal sensitive data. Ensuring the integrity and security of diagnostic communication pathways is paramount to maintaining trust and preventing vehicle vulnerabilities. Furthermore, the sheer complexity of modern automotive systems, including intricately networked ECUs and advanced software functions, demands highly sophisticated diagnostic capabilities that can be difficult and expensive to develop. This complexity also necessitates a continuous upskilling of technicians, as diagnostic errors can lead to costly misdiagnoses or even safety critical failures, thereby placing pressure on training and education within the automotive service industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Interoperability & Standardization Issues | -1.1% | Global, affects multi-brand workshops | 2025-2033 |

| Rapid Technological & Software Update Needs | -0.9% | Global, across all segments | 2025-2033 |

| Cybersecurity Risks & Data Breaches | -0.8% | Global, higher in connected vehicle ecosystems | 2025-2033 |

| High Development Costs for Advanced Tools | -0.7% | Global, impacts manufacturers and end-users | 2025-2033 |

| Training & Skill Development for Technicians | -0.6% | Global, especially in regions with emerging automotive sectors | 2025-2033 |

Automotive Diagnostic Scan Tool Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Automotive Diagnostic Scan Tool market, covering historical trends from 2019 to 2023 and offering a robust forecast spanning 2025 to 2033. The scope encompasses market sizing, growth rate projections, and detailed segmentation across various parameters, including tool type, connectivity, vehicle application, and end-use. It also highlights key market trends, drivers, restraints, opportunities, and challenges influencing market dynamics. Furthermore, the report features regional insights and profiles of prominent market players, offering a holistic view of the competitive landscape and strategic recommendations for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 29.3 Billion |

| Growth Rate | 8.7% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Bosch, Snap-on Inc., Launch Tech Co. Ltd., Autel, TEXA S.p.A., Actia SA, Continental AG, Delphi Technologies (BorgWarner Inc.), Vector Informatik GmbH, Siemens AG, Dürr AG, Hella Gutmann Solutions (HELLA GmbH & Co. KGaA), SPX Corporation, Fluke Corporation, AVL List GmbH, Dg Technologies, Hickok Incorporated, Drew Technologies (Opus Group AB), Innova Electronics Corporation, Rotunda (Ford Motor Company) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Diagnostic Scan Tool market is intricately segmented to provide a granular view of its diverse components and drivers. These segmentations allow for a comprehensive understanding of various product types, technological integrations, vehicle applications, and end-user demands, highlighting specific growth areas and market dynamics within each category. The breakdown by tool type, for instance, reflects the ongoing evolution from traditional handheld devices to advanced PC-based and mobile device-driven solutions, each catering to different user preferences and technical requirements. Connectivity options further delineate the market, showcasing the increasing preference for wireless solutions that offer greater flexibility and remote diagnostic capabilities.

Moreover, the market is segmented by vehicle type, differentiating between the diagnostic needs of passenger vehicles and various commercial vehicle categories, each with its unique complexity and regulatory compliance demands. The application segment identifies key end-users, from OEM and independent repair shops to DIY enthusiasts and large fleet management operations, underscoring the varied market penetration strategies employed by manufacturers. This multi-faceted segmentation provides a robust framework for stakeholders to identify niche opportunities, tailor product development, and refine marketing strategies to address the specific needs of different market segments effectively.

- By Tool Type: Handheld Diagnostic Tools, PC-based Diagnostic Tools, Mobile Device-based Diagnostic Tools

- By Connectivity: Wired Diagnostic Tools, Wireless Diagnostic Tools (Bluetooth, Wi-Fi, 5G)

- By Vehicle Type: Passenger Vehicles, Commercial Vehicles (Light Commercial Vehicles, Medium & Heavy Commercial Vehicles)

- By Application: OEM Repair Shops, Independent Repair Shops, DIY/Aftermarket, Fleet Management

- By Sales Channel: Online, Offline

Regional Highlights

- North America: This region represents a mature and technologically advanced market for automotive diagnostic scan tools. It is characterized by high adoption rates of cutting-edge diagnostic technologies, driven by a large vehicle parc, robust automotive aftermarket, and stringent emission regulations. The presence of major automotive OEMs and a strong emphasis on connected car technologies contribute significantly to market growth.

- Europe: Europe is a significant market, propelled by stringent vehicle safety and environmental regulations, pushing the demand for highly accurate and compliant diagnostic tools. The region also exhibits a strong preference for advanced, integrated diagnostic solutions, especially with the rapid adoption of electric vehicles and sophisticated ADAS features.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market due to increasing vehicle production, rising disposable incomes, and the expanding automotive aftermarket in countries like China, India, Japan, and South Korea. The rapid electrification of vehicles and the growing demand for efficient repair and maintenance services are key drivers.

- Latin America: This region is an emerging market for automotive diagnostic scan tools, characterized by a growing vehicle population and developing automotive infrastructure. The increasing demand for basic to mid-range diagnostic tools, coupled with the gradual adoption of more advanced technologies, marks its growth trajectory.

- Middle East and Africa (MEA): The MEA region is experiencing steady growth, primarily driven by increasing vehicle sales, infrastructure development, and a rising awareness among consumers and workshops about the benefits of modern diagnostic equipment. Investments in automotive service centers are also contributing to market expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Diagnostic Scan Tool Market.- Bosch

- Snap-on Inc.

- Launch Tech Co. Ltd.

- Autel

- TEXA S.p.A.

- Actia SA

- Continental AG

- Delphi Technologies (BorgWarner Inc.)

- Vector Informatik GmbH

- Siemens AG

- Dürr AG

- Hella Gutmann Solutions (HELLA GmbH & Co. KGaA)

- SPX Corporation

- Fluke Corporation

- AVL List GmbH

- Dg Technologies

- Hickok Incorporated

- Drew Technologies (Opus Group AB)

- Innova Electronics Corporation

- Rotunda (Ford Motor Company)

Frequently Asked Questions

Analyze common user questions about the Automotive Diagnostic Scan Tool market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is an Automotive Diagnostic Scan Tool?

An Automotive Diagnostic Scan Tool is an electronic device used to interface with a vehicle's onboard diagnostic (OBD) system. It reads diagnostic trouble codes (DTCs), monitors various sensors, and performs specific tests to identify and troubleshoot issues within a vehicle's electronic systems, engine, transmission, and other components.

Why is the Automotive Diagnostic Scan Tool market growing?

The market is growing primarily due to the increasing complexity of modern vehicles, the proliferation of electronic control units (ECUs), the rise of electric and hybrid vehicles requiring specialized diagnostics, and stringent emission regulations mandating precise vehicle monitoring and maintenance.

How does AI impact Automotive Diagnostic Scan Tools?

AI enhances diagnostic tools by enabling predictive maintenance, analyzing vast datasets for more accurate troubleshooting, providing guided repair steps, and optimizing workshop efficiency. It also supports advanced anomaly detection and contributes to the development of self-diagnosing vehicle systems.

What are the key trends shaping the Automotive Diagnostic Scan Tool market?

Key trends include the shift towards wireless and cloud-based diagnostics, increased integration with Advanced Driver-Assistance Systems (ADAS) calibration, the adoption of Artificial Intelligence (AI) for predictive maintenance, a focus on cybersecurity features, and the development of specialized tools for electric vehicles (EVs).

What challenges do manufacturers face in this market?

Manufacturers face challenges such as ensuring interoperability across diverse vehicle brands, keeping pace with rapid technological advancements requiring continuous software updates, addressing cybersecurity risks in connected diagnostic environments, and navigating the high development costs for sophisticated tools.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted