Automotive Cockpit Module Market

Automotive Cockpit Module Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704895 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

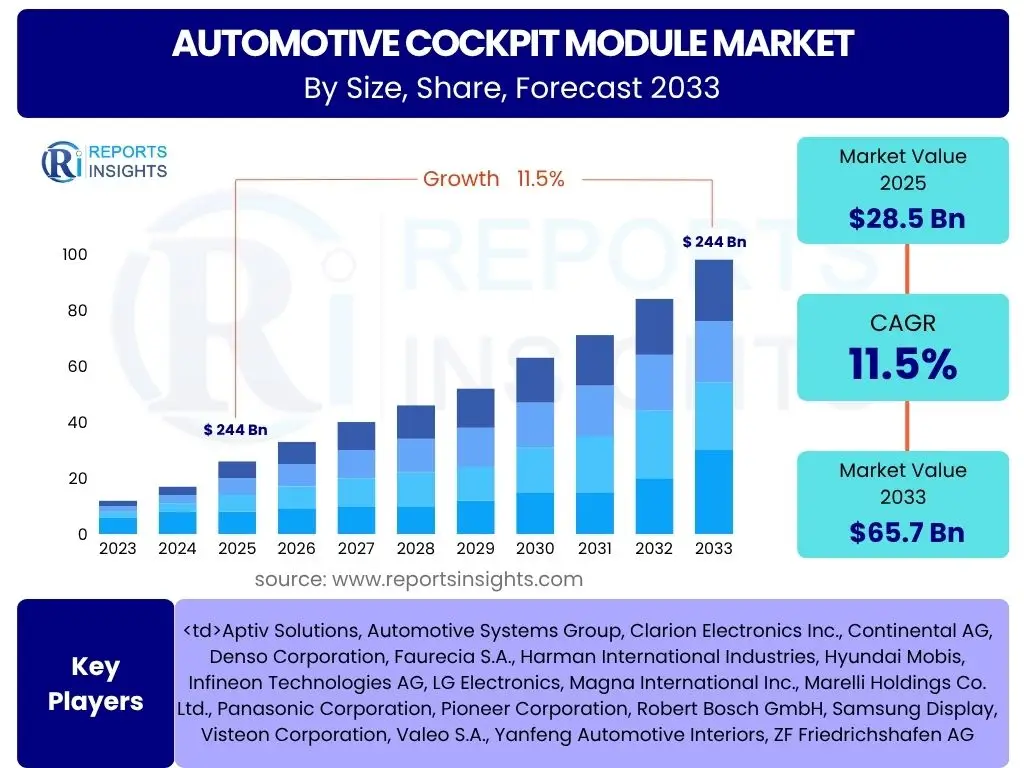

Automotive Cockpit Module Market Size

According to Reports Insights Consulting Pvt Ltd, The Automotive Cockpit Module Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2025 and 2033. The market is estimated at USD 28.5 Billion in 2025 and is projected to reach USD 65.7 Billion by the end of the forecast period in 2033.

Key Automotive Cockpit Module Market Trends & Insights

The automotive cockpit module market is undergoing a profound transformation, driven by advancements in digital technologies, connectivity, and artificial intelligence. User inquiries frequently highlight a shift towards more immersive, personalized, and intuitive in-car experiences. There is significant interest in how traditional physical controls are being replaced by sophisticated digital interfaces, integrating multiple functionalities into a seamless, cohesive unit. Furthermore, the convergence of infotainment, driver information, and safety systems within a unified cockpit architecture is a recurring theme, reflecting the industry's push towards enhanced user interaction and convenience.

Consumers and industry stakeholders are increasingly focused on the integration of advanced human-machine interfaces (HMI), the proliferation of high-resolution displays, and the capabilities enabled by software-defined vehicles. The quest for a truly connected and personalized cabin experience is reshaping design philosophies and technological investments. This paradigm shift emphasizes not just the display of information, but the intelligent processing and delivery of relevant data to drivers and passengers, alongside a growing demand for sustainable and modular cockpit solutions.

- Digital Cockpit Evolution: Shift from analog to fully digital and reconfigurable displays, integrating instrument clusters, infotainment, and climate control into a unified screen experience.

- Software-Defined Vehicle (SDV) Integration: Increasing reliance on software to define and update cockpit functionalities, enabling over-the-air (OTA) updates and personalized features post-purchase.

- Seamless Connectivity and 5G Adoption: Enhanced in-car connectivity for real-time data, navigation, entertainment, and vehicle-to-everything (V2X) communication, leveraging 5G networks.

- Advanced Human-Machine Interface (HMI) & User Experience (UX): Development of intuitive multi-modal HMI including voice control, gesture recognition, haptic feedback, and augmented reality (AR) displays for enhanced safety and comfort.

- Personalization and Customization: AI-driven systems that learn driver preferences for seat position, climate, media, and navigation, offering a tailored in-car environment.

- Sustainable Materials and Modular Design: Growing adoption of eco-friendly materials and modular cockpit architectures to facilitate easier upgrades, repair, and recycling, aligning with circular economy principles.

AI Impact Analysis on Automotive Cockpit Module

User questions regarding the impact of AI on automotive cockpit modules frequently revolve around how artificial intelligence enhances user interaction, safety, and personalization. There is a strong interest in AI's role in creating more intuitive and adaptive in-car environments, moving beyond simple voice commands to truly intelligent assistants that anticipate needs. Key concerns often include the capabilities of AI in processing complex data for predictive maintenance, optimizing driver alerts, and seamlessly integrating with advanced driver-assistance systems (ADAS) and autonomous driving functionalities.

The pervasive influence of AI is transforming the cockpit from a mere control center into an intelligent, responsive co-pilot. AI algorithms are crucial for processing vast amounts of sensory data, enabling features such as gaze tracking, emotion detection, and personalized climate control. Furthermore, users are curious about how AI contributes to cybersecurity within the cockpit, protecting sensitive data and ensuring system integrity in an increasingly connected vehicle. The integration of generative AI is also emerging as a topic, with potential applications in dynamic content generation and contextual assistance.

- Enhanced Voice AI and Natural Language Processing (NLP): AI-powered intelligent assistants offering more natural, conversational interactions for vehicle controls, navigation, and infotainment, reducing driver distraction.

- Personalized User Experience (UX): AI algorithms learn individual driver and passenger preferences (e.g., climate, music, seat position, lighting) to proactively adjust the cabin environment, enhancing comfort and satisfaction.

- Predictive Maintenance and Diagnostics: AI monitors vehicle systems and driver behavior to predict potential faults or maintenance needs, communicating alerts via the cockpit interface.

- Advanced Driver Monitoring Systems (DMS): AI-driven cameras and sensors detect driver drowsiness, distraction, and vital signs, providing real-time alerts and enhancing safety.

- ADAS & Autonomous Driving Integration: AI processes sensor data for ADAS features (e.g., adaptive cruise control, lane-keeping assist) and provides intuitive visualizations and alerts within the cockpit for autonomous driving modes.

- Cybersecurity Enhancements: AI-driven anomaly detection and threat identification systems embedded within cockpit modules to protect against cyberattacks and ensure data integrity.

Key Takeaways Automotive Cockpit Module Market Size & Forecast

User questions about the key takeaways from the Automotive Cockpit Module market size and forecast consistently point to the significant growth trajectory and the underlying technological shifts. Insights reveal a market poised for substantial expansion, driven by the escalating demand for connected, autonomous, shared, and electric (CASE) vehicles. The forecast emphasizes a clear industry pivot towards digital and software-centric cockpit architectures, moving away from traditional, hardware-defined systems. The primary focus for stakeholders lies in capitalizing on the opportunities presented by digitalization and the integration of advanced user experiences.

The market's robust Compound Annual Growth Rate (CAGR) underscores the rapid adoption of sophisticated in-car technologies. A key takeaway is the imperative for automotive manufacturers and Tier-1 suppliers to invest heavily in software development, AI integration, and cybersecurity measures to remain competitive. Furthermore, the increasing complexity of these modules necessitates strategic partnerships across the automotive, technology, and electronics sectors to deliver innovative and seamless solutions. The market is not just growing in volume but also in sophistication, with a strong emphasis on user-centric design and the ability to offer dynamic, updatable features.

- Significant Market Expansion: The market is projected for robust growth, nearly tripling in value from 2025 to 2033, driven by technological integration and consumer demand.

- Technology-Driven Evolution: Core growth is fueled by advancements in digital displays, AI, connectivity, and Human-Machine Interface (HMI) solutions, making cockpits more intelligent and interactive.

- Software-Centric Transformation: A fundamental shift towards software-defined cockpits is evident, enabling over-the-air (OTA) updates, personalization, and new revenue streams through subscription services.

- Enhanced User Experience Focus: The industry's priority is on delivering highly personalized, intuitive, and immersive in-cabin experiences that integrate entertainment, information, and safety seamlessly.

- Strategic Collaborations and Investments: Manufacturers are increasingly forming partnerships with technology companies and investing in R&D to develop advanced materials, integrated systems, and robust cybersecurity protocols.

Automotive Cockpit Module Market Drivers Analysis

The Automotive Cockpit Module Market is primarily propelled by the escalating demand for advanced in-car experiences and the rapid evolution of automotive technology. Consumers increasingly seek vehicles equipped with sophisticated infotainment systems, seamless connectivity, and intuitive user interfaces, transforming the cockpit from a utilitarian space into a personalized digital hub. This demand is further amplified by the global push towards electric vehicles (EVs) and autonomous driving, which necessitate more advanced and integrated cockpit architectures to manage complex data flows and enhance user interaction with new functionalities.

Moreover, the integration of advanced driver-assistance systems (ADAS) and the proliferation of high-resolution displays play a crucial role in driving market growth. OEMs are focusing on differentiating their vehicles through superior in-cabin technology and user experience, leading to greater investments in R&D for innovative cockpit solutions. The shift towards software-defined vehicles (SDVs) also empowers manufacturers to offer customizable and upgradable features, attracting tech-savvy consumers and creating new revenue streams, thus significantly contributing to market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Connected and Digital Cockpits | +1.8% | Global, particularly North America, Europe, APAC (China, South Korea) | Short to Mid-Term (2025-2029) |

| Growth in Premium and Luxury Vehicle Segments | +1.5% | Global, particularly Europe, North America, APAC (China) | Mid-Term (2027-2033) |

| Rising Adoption of Electric Vehicles (EVs) and Autonomous Features | +2.1% | Global, particularly Europe, North America, APAC (China, Japan) | Short to Long-Term (2025-2033) |

| Advancements in Human-Machine Interface (HMI) Technologies | +1.6% | Global | Short to Mid-Term (2025-2030) |

| Consumer Preference for Personalized In-Car Experiences | +1.4% | Global | Mid to Long-Term (2027-2033) |

| Emergence of Software-Defined Vehicles (SDVs) | +1.9% | Global, particularly North America, Europe | Mid to Long-Term (2028-2033) |

Automotive Cockpit Module Market Restraints Analysis

Despite the robust growth prospects, the Automotive Cockpit Module Market faces several significant restraints that could impede its full potential. A primary concern is the substantial research and development (R&D) costs associated with integrating complex digital systems, advanced displays, and artificial intelligence into the cockpit architecture. These high investment requirements can be a barrier for smaller players and place considerable financial strain on larger manufacturers, potentially slowing down innovation cycles or increasing end-product costs for consumers.

Furthermore, the market is highly susceptible to global supply chain disruptions, particularly concerning semiconductor components and specialized electronic parts. Geopolitical tensions, trade disputes, and unforeseen events such as pandemics can lead to component shortages, production delays, and increased material costs, directly impacting manufacturing output and market availability. Cybersecurity threats and data privacy concerns also represent a formidable restraint. As cockpits become increasingly connected and handle sensitive user data, ensuring robust security measures and compliance with stringent data protection regulations (e.g., GDPR) becomes a critical, complex, and costly challenge, which if not adequately addressed, can erode consumer trust and market adoption.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Research and Development (R&D) Costs | -0.7% | Global | Short to Mid-Term (2025-2030) |

| Supply Chain Vulnerabilities and Component Shortages | -1.2% | Global, particularly Asia Pacific (China, Taiwan) | Short to Mid-Term (2025-2028) |

| Cybersecurity Risks and Data Privacy Concerns | -0.9% | Global, particularly Europe, North America | Long-Term (2025-2033) |

| Regulatory Complexities and Standardization Challenges | -0.6% | Europe, North America, China | Mid-Term (2027-2032) |

| Rapid Technological Obsolescence and Upgrade Cycles | -0.5% | Global | Mid to Long-Term (2028-2033) |

| High Initial Investment for OEMs and Tier-1 Suppliers | -0.8% | Global | Short to Mid-Term (2025-2029) |

Automotive Cockpit Module Market Opportunities Analysis

The Automotive Cockpit Module Market is replete with opportunities for innovation and growth, driven by evolving consumer expectations and technological breakthroughs. One significant area lies in the ongoing development and integration of augmented reality (AR) and virtual reality (VR) technologies within the cockpit. These immersive experiences can transform navigation, infotainment, and driver assistance, offering new ways to display critical information and engage occupants, creating distinct competitive advantages for early adopters and innovators.

Furthermore, the expansion into emerging markets, particularly in Asia Pacific, Latin America, and Africa, presents substantial growth avenues. As these regions experience rising disposable incomes and increasing vehicle penetration, the demand for advanced, digitally enhanced cockpits is expected to surge. The trend towards vehicle subscription services and shared mobility also opens doors for new business models where cockpit personalization and adaptability become paramount, allowing for dynamic user profiles and tailored experiences regardless of vehicle ownership. Additionally, the continued advancement of biometric authentication and health monitoring systems integrated into the cockpit offers significant potential for enhancing both security and wellness within the vehicle cabin.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Augmented Reality (AR) and Virtual Reality (VR) Cockpits | +1.7% | Global, particularly North America, Europe, Japan | Mid to Long-Term (2028-2033) |

| Expansion into Emerging Markets | +1.3% | Asia Pacific (India, Southeast Asia), Latin America, Middle East & Africa | Short to Long-Term (2025-2033) |

| Growth of Vehicle Subscription and Shared Mobility Services | +1.0% | North America, Europe, China | Mid-Term (2027-2032) |

| Integration of Advanced Biometric and Health Monitoring Systems | +1.5% | Global | Mid to Long-Term (2028-2033) |

| Leveraging AI and Machine Learning for Hyper-Personalization | +1.6% | Global | Short to Long-Term (2025-2033) |

| Strategic Partnerships with Consumer Electronics and Tech Companies | +1.2% | Global | Short to Mid-Term (2025-2030) |

Automotive Cockpit Module Market Challenges Impact Analysis

The Automotive Cockpit Module Market faces several intricate challenges that demand sophisticated solutions from manufacturers and suppliers. One of the primary hurdles is ensuring seamless integration across diverse vehicle platforms and models, particularly as cockpits become more complex and software-defined. Achieving interoperability between hardware components from various suppliers and proprietary software systems is a significant technical challenge that can lead to increased development time and costs.

Moreover, managing the increasing software complexity and ensuring robust validation processes for millions of lines of code is a formidable task. This complexity not only raises the risk of software bugs and recalls but also necessitates a highly skilled workforce, contributing to talent shortages in specialized areas like embedded software development and AI engineering. Addressing cybersecurity threats remains a persistent challenge, as connected cockpits become attractive targets for malicious actors. Protecting sensitive user data and vehicle functionalities from sophisticated cyberattacks requires continuous investment in advanced security protocols and real-time threat detection, adding another layer of complexity and cost to module development and maintenance.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring Seamless Integration Across Diverse Vehicle Platforms | -0.8% | Global | Short to Mid-Term (2025-2030) |

| Managing Increasing Software Complexity and Validation | -1.0% | Global | Short to Long-Term (2025-2033) |

| Addressing Evolving Cybersecurity Threats and Vulnerabilities | -1.1% | Global | Long-Term (2025-2033) |

| Talent Shortage in Specialized Software and AI Fields | -0.7% | Global, particularly North America, Europe | Mid to Long-Term (2027-2033) |

| Achieving Cost-Effectiveness with Advanced Feature Integration | -0.9% | Global | Short to Mid-Term (2025-2029) |

| Maintaining Interoperability Between Different Systems and Vendors | -0.6% | Global | Short to Long-Term (2025-2033) |

Automotive Cockpit Module Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Automotive Cockpit Module Market, offering strategic insights into its current landscape, historical performance, and future growth trajectories. The scope encompasses detailed market sizing, segmentation analysis by various parameters, and regional breakdowns, ensuring a holistic understanding of market dynamics. It also highlights key trends, identifies significant drivers, restraints, opportunities, and challenges shaping the industry, alongside an assessment of the competitive landscape featuring leading market participants.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 28.5 Billion |

| Market Forecast in 2033 | USD 65.7 Billion |

| Growth Rate | 11.5% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Aptiv Solutions, Automotive Systems Group, Clarion Electronics Inc., Continental AG, Denso Corporation, Faurecia S.A., Harman International Industries, Hyundai Mobis, Infineon Technologies AG, LG Electronics, Magna International Inc., Marelli Holdings Co. Ltd., Panasonic Corporation, Pioneer Corporation, Robert Bosch GmbH, Samsung Display, Visteon Corporation, Valeo S.A., Yanfeng Automotive Interiors, ZF Friedrichshafen AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Cockpit Module Market is meticulously segmented to provide a granular understanding of its diverse facets and varying dynamics across different product types, technologies, vehicle categories, and end-user applications. This segmentation highlights the specific areas of growth and technological adoption within the broader market, enabling a targeted analysis of trends and opportunities. Analyzing these segments provides critical insights into consumer preferences, technological shifts, and the competitive landscape, facilitating strategic decision-making for market players.

The primary segmentation divides the market based on components, ranging from advanced display systems like LCD, OLED, and MicroLED, to increasingly sophisticated Head-Up Displays (HUDs), and fully digital instrument clusters. Further differentiation occurs by the type of vehicle (passenger cars versus commercial vehicles) and the underlying technology, distinguishing between digital, smart, and fully integrated cockpit solutions. The market is also segmented by end-use (OEM versus aftermarket) and sales channels, reflecting the complex value chain and distribution strategies within the automotive industry.

- By Component:

- Display Systems (LCD, OLED, MicroLED)

- Head-Up Displays (HUD)

- Instrument Clusters (Digital, Hybrid)

- Infotainment Systems

- HVAC Controls

- Others (Sensors, Cameras, Wiring, Control Units)

- By Vehicle Type:

- Passenger Cars (Sedans, SUVs, Hatchbacks, Luxury Vehicles)

- Commercial Vehicles (Light-Duty, Medium-Duty, Heavy-Duty)

- By Technology:

- Digital Cockpit

- Smart Cockpit

- Integrated Cockpit

- By End-Use:

- Original Equipment Manufacturer (OEM)

- Aftermarket

- By Sales Channel:

- Direct

- Indirect

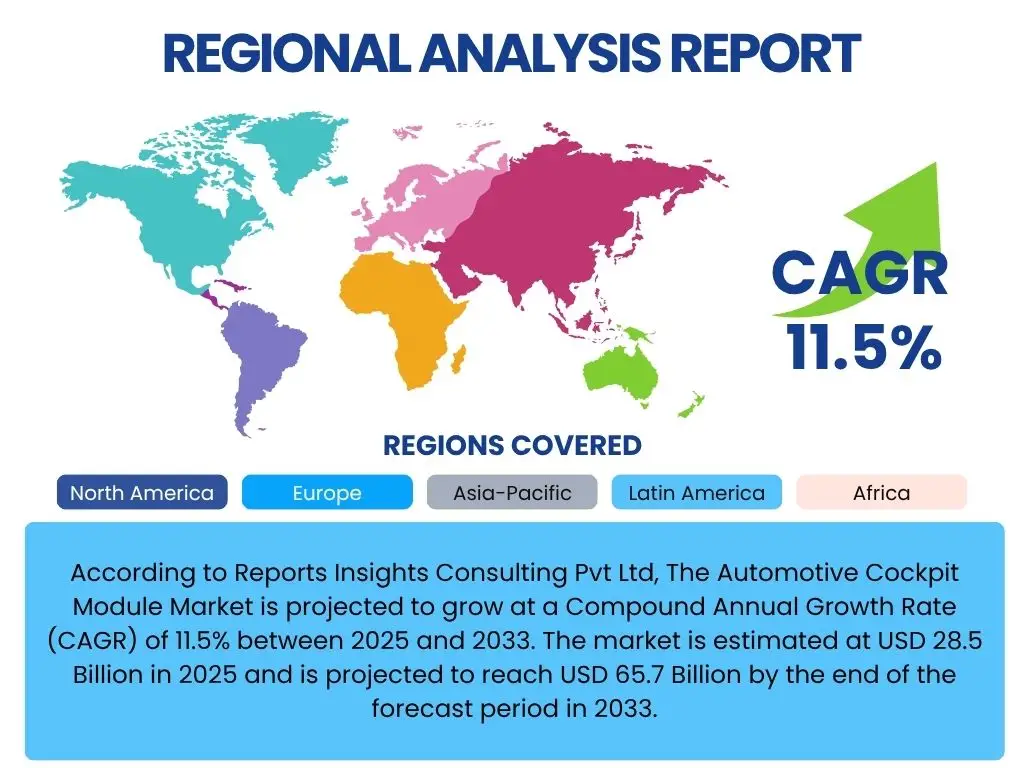

Regional Highlights

- North America: This region exhibits a strong demand for advanced infotainment and connectivity features, driven by tech-savvy consumers and the rapid adoption of electric and autonomous vehicles. The presence of major automotive manufacturers and significant investments in R&D contribute to its market leadership, particularly in premium and luxury segments. Regulatory frameworks pushing for enhanced vehicle safety also spur the integration of sophisticated cockpit modules.

- Europe: Europe is a key market propelled by stringent safety regulations, a strong emphasis on premium vehicle segments, and high consumer expectations for integrated digital experiences. Germany, France, and the UK are at the forefront of adopting advanced cockpit technologies, driven by innovation in design, HMI, and sustainable manufacturing practices. The shift towards electrification further accelerates the demand for new cockpit architectures.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, primarily due to the large automotive production bases in China, Japan, South Korea, and India. Rapid urbanization, increasing disposable incomes, and the burgeoning middle class are driving higher vehicle sales and a growing demand for feature-rich cars. China stands out with its aggressive adoption of EVs and smart vehicle technologies, making it a pivotal market for cockpit module innovation and deployment.

- Latin America: This region is experiencing steady growth, influenced by increasing automotive production and a rising consumer demand for connected and modern vehicle features. While still developing compared to other regions, there is a growing interest in digital cockpits, particularly in countries like Brazil and Mexico, as vehicle sales volumes increase and technology penetration expands.

- Middle East and Africa (MEA): The MEA region is characterized by a growing automotive market, especially in the GCC countries, driven by economic diversification and infrastructure development. The demand for luxury vehicles with advanced cockpit features is notable. While specific technology adoption rates vary, the overall market trajectory indicates a gradual but consistent increase in the demand for sophisticated in-car electronics.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Cockpit Module Market.- Aptiv Solutions

- Automotive Systems Group

- Clarion Electronics Inc.

- Continental AG

- Denso Corporation

- Faurecia S.A.

- Harman International Industries

- Hyundai Mobis

- Infineon Technologies AG

- LG Electronics

- Magna International Inc.

- Marelli Holdings Co. Ltd.

- Panasonic Corporation

- Pioneer Corporation

- Robert Bosch GmbH

- Samsung Display

- Visteon Corporation

- Valeo S.A.

- Yanfeng Automotive Interiors

- ZF Friedrichshafen AG

Frequently Asked Questions

Analyze common user questions about the Automotive Cockpit Module market and generate a concise list of summarized FAQs reflecting key topics and concerns.What defines an Automotive Cockpit Module?

An Automotive Cockpit Module is an integrated system comprising essential components such as display screens, instrument clusters, infotainment systems, climate controls, and various switches and sensors, designed to provide driver information, control functionalities, and entertainment within a vehicle's cabin. Modern modules are increasingly digital, software-driven, and designed for a seamless user experience.

How is the Automotive Cockpit Module Market expected to grow?

The Automotive Cockpit Module Market is projected for substantial growth, with a Compound Annual Growth Rate (CAGR) of 11.5% from 2025 to 2033. It is estimated at USD 28.5 Billion in 2025 and is forecast to reach USD 65.7 Billion by 2033, driven by the increasing demand for connected, autonomous, and electric vehicles.

What key technologies are driving innovation in cockpit modules?

Key technologies driving innovation include high-resolution digital displays (LCD, OLED, MicroLED), advanced Human-Machine Interfaces (HMI) with voice and gesture control, artificial intelligence (AI) for personalization and predictive functions, enhanced connectivity (5G, V2X), and software-defined architectures enabling over-the-air (OTA) updates and modularity.

What are the main challenges facing the Automotive Cockpit Module Market?

Primary challenges include high research and development costs, vulnerabilities in the global supply chain, increasing software complexity and validation requirements, persistent cybersecurity threats, and the ongoing talent shortage in specialized technology fields, all of which necessitate significant investment and strategic planning.

How does AI impact the user experience in modern cockpit modules?

AI significantly enhances user experience by enabling personalized settings (climate, media, seating), intelligent voice assistants for natural interaction, predictive maintenance alerts, and advanced driver monitoring systems (DMS) for safety. AI also plays a crucial role in seamlessly integrating ADAS and autonomous driving features into the cockpit interface.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted