Automotive AR and VR Market

Automotive AR and VR Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700650 | Last Updated : July 26, 2025 |

Format : ![]()

![]()

![]()

![]()

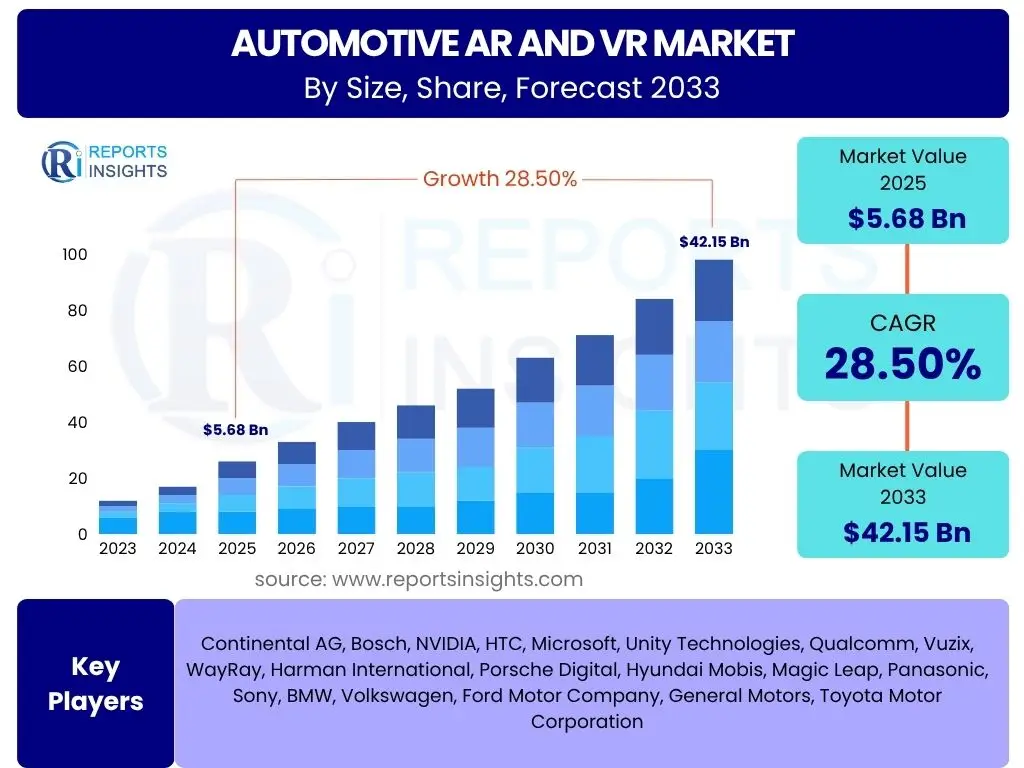

Automotive AR and VR Market Size

Automotive AR and VR Market is projected to grow at a Compound annual growth rate (CAGR) of 28.5% between 2025 and 2033, valued at USD 5.68 billion in 2025 and is projected to grow by USD 42.15 billion by 2033 the end of the forecast period.

Key Automotive AR and VR Market Trends & Insights

The Automotive AR and VR market is undergoing significant transformation, driven by technological advancements and evolving consumer expectations for in-vehicle experiences. Key trends indicate a shift towards deeper integration of immersive technologies across various automotive functionalities, from vehicle design and manufacturing to in-car entertainment and safety systems. These trends are shaping a future where digital and physical realities seamlessly merge within the automotive ecosystem, offering enhanced user interaction and operational efficiencies.

- Increased adoption of augmented reality for advanced driver-assistance systems (ADAS) and navigation.

- Growing integration of virtual reality in vehicle design, prototyping, and testing phases.

- Development of immersive in-car entertainment and infotainment systems leveraging AR/VR.

- Rise in demand for virtual showrooms and interactive sales tools using VR technology.

- Expansion of AR/VR applications in automotive manufacturing for training and maintenance.

AI Impact Analysis on Automotive AR and VR

Artificial intelligence is profoundly reshaping the landscape of automotive AR and VR, acting as a pivotal enabler for more intelligent, responsive, and personalized immersive experiences. AI algorithms enhance the capabilities of AR/VR systems by improving data processing, predictive analytics, and content generation, making these technologies more effective and efficient for automotive applications. The synergy between AI and AR/VR is leading to the creation of advanced solutions that are intuitive, context-aware, and highly impactful for both manufacturers and end-users.

- AI-powered object recognition and tracking for highly accurate AR overlays in navigation and ADAS.

- Personalized VR content delivery based on driver behavior and preferences through AI analytics.

- Predictive maintenance and diagnostics utilizing AI to interpret sensor data for AR-guided repairs.

- Optimization of AR/VR system performance, reducing latency and improving rendering through AI algorithms.

- AI-driven generation of realistic virtual environments for training simulations and vehicle prototyping.

Key Takeaways Automotive AR and VR Market Size & Forecast

- The market is poised for robust expansion, driven by continuous innovation in immersive technologies.

- Significant growth opportunities exist in integrating AR/VR across the entire automotive value chain.

- North America and Europe are currently leading in adoption due to advanced technological infrastructure and consumer demand.

- The convergence of Artificial Intelligence with AR/VR is a fundamental catalyst for market evolution.

- Emphasis on enhancing user experience, improving safety, and streamlining operational processes is central to market development.

- Increasing investment in research and development by automotive OEMs and technology providers is accelerating market maturity.

- The shift towards software-defined vehicles creates a fertile ground for deeper AR/VR integration.

- Customization and personalization of in-car digital experiences are becoming key competitive differentiators.

- Demand for efficient remote collaboration tools in design and manufacturing is boosting AR/VR adoption.

- The automotive AR and VR market is transitioning from niche applications to mainstream integration within vehicles.

Automotive AR and VR Market Drivers Analysis

The Automotive AR and VR market is propelled by a confluence of technological advancements, evolving consumer expectations, and the automotive industry's strategic imperative to innovate. These drivers collectively foster an environment conducive to the widespread adoption and integration of immersive technologies across the vehicle lifecycle. From enhancing in-car safety and entertainment to revolutionizing design and manufacturing processes, the push for digital transformation within the automotive sector is a primary force behind market expansion. The increasing sophistication of hardware and software, coupled with a growing recognition of the operational efficiencies and consumer engagement opportunities AR/VR offers, continues to accelerate market growth. This robust growth trajectory is further supported by the industry's commitment to creating smarter, safer, and more engaging driving and ownership experiences.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for enhanced in-car experience: Consumers increasingly seek advanced infotainment, personalized navigation, and immersive entertainment within vehicles, driving the integration of AR/VR solutions. | +6.0% | Global, particularly North America, Europe, Asia Pacific | Short to Medium Term (2025-2029) |

| Increased adoption of ADAS and autonomous vehicles: AR complements ADAS by providing intuitive visual overlays for safety warnings, navigation, and environmental awareness, while VR aids in autonomous vehicle training and simulation. | +5.5% | North America, Europe, China | Medium to Long Term (2027-2033) |

| Rise in virtual prototyping and design in automotive manufacturing: VR and AR significantly accelerate vehicle development cycles, reduce physical prototype costs, and enable global collaborative design, leading to faster innovation. | +5.0% | Europe, Japan, South Korea, Germany, USA | Short to Medium Term (2025-2030) |

| Advancements in AR/VR hardware and software technologies: Continuous improvements in display resolution, processing power, sensor accuracy, and software development kits make AR/VR solutions more accessible, powerful, and seamless for automotive integration. | +4.5% | Global, with innovation hubs in USA, China, South Korea, Japan | Ongoing throughout Forecast Period |

| Focus on driver safety and situational awareness: AR head-up displays (HUDs) provide critical information directly in the driver's line of sight, enhancing safety by minimizing distraction and improving reaction times to road conditions. | +4.0% | Europe, North America, Japan | Short to Medium Term (2025-2030) |

Automotive AR and VR Market Restraints Analysis

Despite the promising growth trajectory, the Automotive AR and VR market faces several significant restraints that could impede its full potential. These challenges range from the inherent technological limitations and high implementation costs to potential user discomfort and privacy concerns. Overcoming these hurdles requires substantial investment in research and development, standardization efforts, and a concerted focus on user-centric design. While the long-term outlook remains positive, addressing these restraints is crucial for ensuring widespread adoption and sustained market expansion. Manufacturers and developers must work collaboratively to mitigate these issues and build robust, user-friendly, and secure AR/VR solutions for the automotive sector.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High cost of AR/VR hardware and integration: The specialized hardware, sensors, and complex integration required for automotive-grade AR/VR systems increase the overall cost, making them less accessible for mass-market vehicles. | -3.5% | Global, especially emerging markets | Short to Medium Term (2025-2028) |

| Computational complexity and latency issues: Real-time rendering of high-fidelity AR/VR content in dynamic automotive environments demands immense processing power, leading to potential latency or system lag, which can impact user experience and safety. | -3.0% | Global | Short Term (2025-2027) |

| Potential for motion sickness (VR) and driver distraction (AR): Immersive VR experiences in moving vehicles can induce motion sickness for some users, while poorly designed AR interfaces might distract drivers, posing safety risks and hindering adoption. | -2.5% | Global | Medium Term (2026-2030) |

| Data privacy and cybersecurity concerns: AR/VR systems collect significant user data and vehicle environment information. Ensuring the security and privacy of this sensitive data is a critical challenge that requires robust solutions and compliance with regulations. | -2.0% | Europe (GDPR), North America, China | Ongoing throughout Forecast Period |

Automotive AR and VR Market Opportunities Analysis

The Automotive AR and VR market is ripe with substantial opportunities for growth and innovation, extending beyond traditional applications into new revenue streams and operational efficiencies. These opportunities are driven by the continuous evolution of digital technologies, a growing appetite for personalized and engaging user experiences, and the automotive industry's pursuit of smart manufacturing and connected vehicle ecosystems. Leveraging these opportunities requires strategic partnerships, agile development, and a keen understanding of emerging consumer and industrial needs. As the technology matures and becomes more accessible, the scope for application will expand significantly, unlocking new market segments and transformative use cases.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into commercial vehicle applications: AR/VR can significantly enhance training, maintenance, and logistics for commercial fleets, improving operational efficiency, safety, and reducing downtime. | +4.0% | North America, Europe, Asia Pacific | Medium to Long Term (2027-2033) |

| Development of personalized in-car entertainment and productivity: Tailored VR experiences for passengers and AR overlays for vehicle controls can transform commuting into a more engaging and productive time, attracting a broader consumer base. | +3.5% | Global, especially tech-savvy markets | Short to Medium Term (2025-2029) |

| Integration with metaverse and digital twins concepts: The automotive industry can leverage AR/VR to create comprehensive digital twins of vehicles and factories, enabling advanced simulations, remote diagnostics, and immersive virtual interactions within the metaverse. | +3.0% | Global, with early adopters in USA, Europe, Japan | Long Term (2028-2033) |

| Aftermarket upgrades and custom solutions: As technology matures, aftermarket AR/VR units and customizable software solutions can offer new revenue streams, allowing consumers to enhance older vehicles with modern immersive features. | +2.5% | Global, strong potential in developing markets | Medium to Long Term (2027-2033) |

Automotive AR and VR Market Challenges Impact Analysis

The Automotive AR and VR market, while promising, is not without its share of significant challenges that necessitate careful consideration and strategic planning. These challenges span regulatory complexities, issues of user acceptance, the rapid pace of technological obsolescence, and the inherent difficulties in integrating cutting-edge systems into existing vehicle architectures. Addressing these challenges is paramount for the sustainable growth and widespread adoption of AR/VR technologies within the automotive sector. Successfully navigating these hurdles will require collaborative efforts between technology providers, automotive OEMs, and regulatory bodies to ensure that immersive experiences are safe, secure, and seamlessly integrated into the driving environment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Regulatory hurdles for in-car AR/VR use: Safety regulations regarding driver distraction, augmented reality display standards, and data usage policies vary by region and are still evolving, posing significant challenges for global deployment and standardization. | -2.8% | Europe, North America, China | Ongoing throughout Forecast Period |

| User acceptance and comfort levels: Widespread adoption depends on overcoming potential issues like discomfort from prolonged use of headsets (VR), visual fatigue from AR overlays, and ensuring intuitive, non-distracting user interfaces for drivers. | -2.2% | Global | Medium Term (2026-2030) |

| Rapid technological obsolescence and integration complexity: The fast pace of AR/VR technological advancement means systems can quickly become outdated, creating challenges for automotive OEMs regarding upgrade cycles, cost-effectiveness, and seamless integration into long-lifecycle vehicle platforms. | -1.8% | Global | Ongoing throughout Forecast Period |

| Developing compelling, non-distracting AR content for drivers: Creating AR content that enhances situational awareness and provides useful information without overwhelming or diverting the driver's attention is a critical design and safety challenge. | -1.5% | Global | Short to Medium Term (2025-2029) |

Automotive AR and VR Market - Updated Report Scope

The updated scope of this comprehensive market research report provides an in-depth analysis of the Automotive AR and VR market, offering critical insights into its current state, historical performance, and future projections. It encompasses a detailed examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The report is meticulously curated to assist stakeholders in understanding the dynamic market landscape, identifying lucrative investment avenues, and formulating informed business strategies. It highlights the influence of emerging technologies like AI and offers a competitive analysis of leading market players, ensuring a holistic view of the market's potential and trajectory.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.68 Billion |

| Market Forecast in 2033 | USD 42.15 Billion |

| Growth Rate | 28.5% CAGR from 2025 to 2033 |

| Number of Pages | 258 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Continental AG, Bosch, NVIDIA, HTC, Microsoft, Unity Technologies, Qualcomm, Vuzix, WayRay, Harman International, Porsche Digital, Hyundai Mobis, Magic Leap, Panasonic, Sony, BMW, Volkswagen, Ford Motor Company, General Motors, Toyota Motor Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive AR and VR market is extensively segmented to provide a granular understanding of its diverse components and applications, enabling a comprehensive market analysis. Each segment represents a critical aspect of the market, reflecting different technological approaches, end-use cases, and vehicle types. This segmentation helps in identifying specific growth pockets, understanding market dynamics unique to each category, and formulating targeted strategies for various stakeholders. The detailed breakdown below captures the multi-faceted nature of this evolving market.- By Component: This segment differentiates between the physical and digital elements that constitute AR/VR systems in the automotive sector.

- Hardware: Encompasses the physical devices and components essential for AR and VR experiences.

- Head-mounted displays (HMDs): Devices worn on the head to provide immersive visual experiences for VR or augmented overlays for AR.

- Haptic devices: Technologies that provide tactile feedback, enhancing the sense of touch in virtual or augmented environments.

- Processors: High-performance computing units vital for rendering complex AR/VR graphics and running applications in real-time.

- Sensors: Devices such as cameras, accelerometers, gyroscopes, and depth sensors that capture environmental data and user movements for tracking and interaction within AR/VR.

- Software: Refers to the digital programs and platforms that power AR/VR applications.

- SDKs (Software Development Kits): Tools and libraries that enable developers to create AR/VR applications for specific platforms.

- Cloud platforms: Cloud-based services for processing, storing, and distributing AR/VR content and data, enabling scalability and remote access.

- Content creation tools: Software applications used to design, model, animate, and generate 3D assets and environments for AR/VR experiences.

- Hardware: Encompasses the physical devices and components essential for AR and VR experiences.

- By Technology: This fundamental segmentation distinguishes between the two primary forms of immersive technology.

- Augmented Reality (AR): Overlays digital information onto the real-world view, enhancing the user's perception of reality. In automotive, this is crucial for navigation, ADAS, and maintenance.

- Virtual Reality (VR): Creates a completely simulated environment that fully immerses the user, primarily used in automotive for design, training, and virtual showrooms.

- By Application: This segment categorizes the diverse uses of AR/VR within the automotive industry, highlighting their functional relevance.

- Infotainment: Integration of AR/VR for enhanced in-car entertainment, interactive displays, and multimedia experiences for passengers.

- Navigation: AR-powered navigation systems that overlay directions, points of interest, and traffic information directly onto the real-world view through the windshield or head-up displays.

- ADAS (Advanced Driver-Assistance Systems): AR applications that provide real-time warnings, object detection highlights, and contextual information to drivers, improving safety.

- Prototyping and Design: Use of VR for virtual vehicle walkthroughs, collaborative design reviews, and AR for overlaying digital design iterations onto physical models, streamlining the development process.

- Training: VR simulations for driver training, technician training for complex repairs, and sales personnel product knowledge training.

- Sales and Marketing: VR showrooms, interactive AR configurators, and virtual test drives used by dealerships and manufacturers to engage customers and showcase vehicles.

- Maintenance and Repair: AR-guided instructions for technicians, remote assistance for complex repairs, and virtual diagnostics, enhancing efficiency and accuracy in after-sales service.

- By Vehicle Type: This segmentation reflects the different market needs and integration complexities across various types of vehicles.

- Passenger Vehicles: Includes cars, SUVs, and other vehicles primarily used for personal transport, where AR/VR focuses on consumer experience, safety, and infotainment.

- Commercial Vehicles: Encompasses trucks, buses, and vans, where AR/VR applications are more geared towards operational efficiency, driver training, logistics management, and predictive maintenance.

- Light Commercial Vehicles: Smaller commercial vehicles used for deliveries and lighter-duty transport.

- Heavy Commercial Vehicles: Large trucks and buses used for heavy-duty transport and public transit.

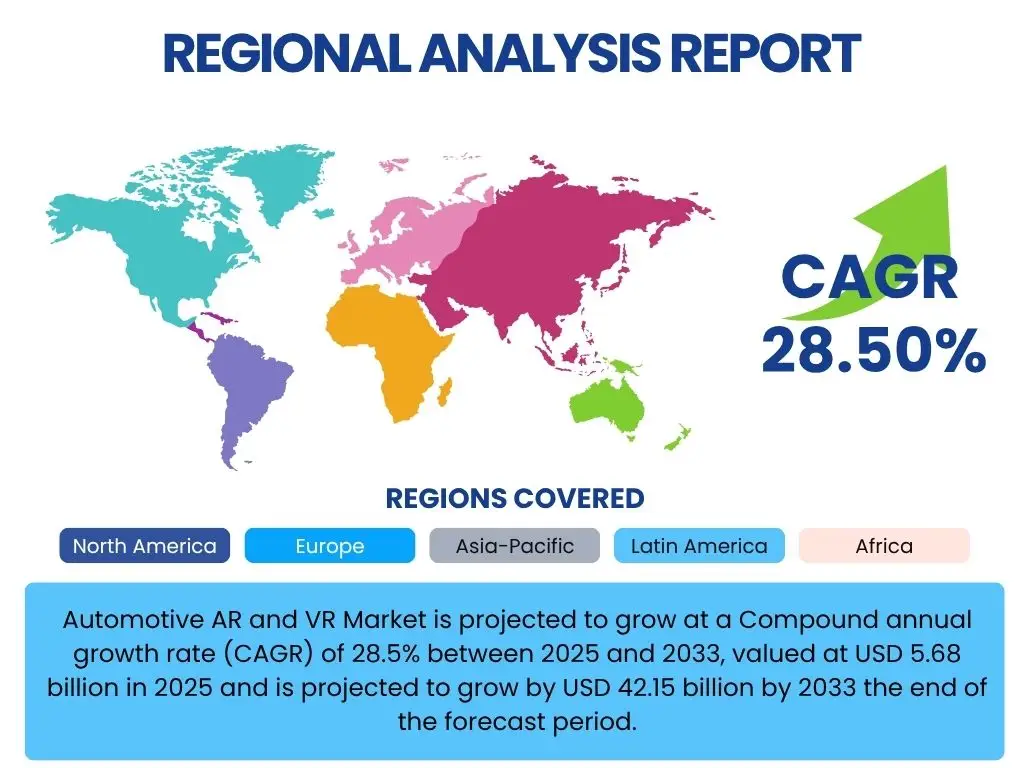

Regional Highlights

The global Automotive AR and VR market exhibits significant regional disparities in terms of adoption rates, technological development, and market maturity. Certain regions are leading the charge in integrating immersive technologies due to strong technological infrastructure, high consumer spending power, and proactive government initiatives supporting innovation in the automotive sector. Understanding these regional dynamics is crucial for market participants to tailor their strategies and investments effectively, leveraging regional strengths and addressing localized challenges. North America stands out as a dominant force in the Automotive AR and VR market, primarily due to the presence of key technology innovators, major automotive OEMs, and a high rate of early technology adoption among consumers. The region benefits from substantial investments in R&D, particularly in areas like autonomous vehicles and advanced driver-assistance systems, where AR applications are proving indispensable. Consumer demand for advanced in-car infotainment and safety features also drives significant market growth, particularly in the United States, fostering a competitive environment that encourages continuous innovation and product development. Europe demonstrates a strong inclination towards advanced manufacturing and luxury automotive segments, making it a significant market for AR/VR applications in vehicle design, virtual prototyping, and precision manufacturing. Countries like Germany, with its robust automotive engineering heritage, are at the forefront of integrating immersive technologies into their production lines and R&D centers. Stringent safety regulations and a focus on driver assistance further contribute to the adoption of AR-enabled solutions, ensuring a steady growth trajectory for the market across the European Union. Asia Pacific is emerging as a rapidly growing market, fueled by large-volume automotive production, increasing consumer disposable incomes, and government support for digital transformation. Countries such as China, Japan, and South Korea are key players, with China being a major manufacturing hub and an increasingly important consumer market for advanced vehicle technologies. Japan and South Korea, renowned for their technological prowess, are also actively developing and deploying cutting-edge AR/VR solutions, especially in the areas of smart cockpits, electric vehicle development, and virtual training for manufacturing efficiency. The region's vast population and burgeoning middle class represent a substantial opportunity for future market expansion. Latin America, the Middle East, and Africa (MEA) currently represent nascent markets for Automotive AR and VR, with adoption primarily concentrated in basic applications such as virtual showrooms for sales and marketing. However, these regions hold significant long-term potential as infrastructure develops, disposable incomes rise, and the automotive industry expands its footprint. Initial growth is expected to be driven by partnerships with international technology providers and increasing awareness of the benefits of AR/VR in enhancing the vehicle ownership experience and optimizing industrial processes.

Top Key Players:

The market research report covers the analysis of key stake holders of the Automotive AR and VR Market. Some of the leading players profiled in the report include -- Continental AG

- Bosch

- NVIDIA

- HTC

- Microsoft

- Unity Technologies

- Qualcomm

- Vuzix

- WayRay

- Harman International

- Porsche Digital

- Hyundai Mobis

- Magic Leap

- Panasonic

- Sony

- BMW

- Volkswagen

- Ford Motor Company

- General Motors

- Toyota Motor Corporation

Frequently Asked Questions:

What is the Automotive AR and VR Market size and its projected growth?

The Automotive AR and VR Market was valued at approximately USD 5.68 billion in 2025. It is projected to grow significantly at a Compound Annual Growth Rate (CAGR) of 28.5% between 2025 and 2033, reaching an estimated market size of USD 42.15 billion by the end of the forecast period. This robust growth is driven by increasing integration of immersive technologies across vehicle design, manufacturing, and in-car user experiences.What are the key applications of AR/VR in the automotive industry?

AR/VR technologies are applied across a wide range of functions within the automotive industry. Key applications include enhanced infotainment systems for passengers, augmented reality navigation and advanced driver-assistance systems (ADAS) for improved safety and awareness, and virtual reality for accelerating vehicle prototyping and design. Additionally, these technologies are crucial for efficient training programs, immersive sales and marketing experiences like virtual showrooms, and streamlined maintenance and repair operations.How is AI impacting the Automotive AR and VR Market?

Artificial Intelligence (AI) plays a transformative role in the Automotive AR and VR Market by enhancing the intelligence, personalization, and efficiency of immersive solutions. AI algorithms enable features such as precise object recognition for AR overlays, personalized VR content delivery based on user preferences, and predictive maintenance through AI-driven diagnostics in AR. Furthermore, AI optimizes system performance by reducing latency and improving rendering, and powers the generation of highly realistic virtual environments for simulations, making AR/VR systems more advanced and effective.Which regions are leading the adoption of Automotive AR and VR technologies?

North America and Europe are currently leading the adoption of Automotive AR and VR technologies. North America benefits from a strong presence of technology innovators and early technology adopters, along with significant R&D investments in autonomous driving and ADAS. Europe, particularly Germany, excels in integrating AR/VR into luxury automotive design, manufacturing, and safety systems. The Asia Pacific region, led by countries like China, Japan, and South Korea, is rapidly emerging as a significant market due to its large production volumes and increasing technological advancements.What are the main challenges hindering market growth?

The Automotive AR and VR Market faces several challenges that could impact its growth. These include the high cost associated with advanced AR/VR hardware and complex integration processes, which can limit mass-market adoption. Computational complexity and potential latency issues pose technical hurdles. Furthermore, concerns regarding motion sickness from VR experiences and the risk of driver distraction from poorly designed AR interfaces are significant user acceptance challenges. Data privacy and cybersecurity concerns also present ongoing regulatory and implementation challenges for comprehensive market expansion.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted