Automatic Call Distribution Software Market

Automatic Call Distribution Software Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708151 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

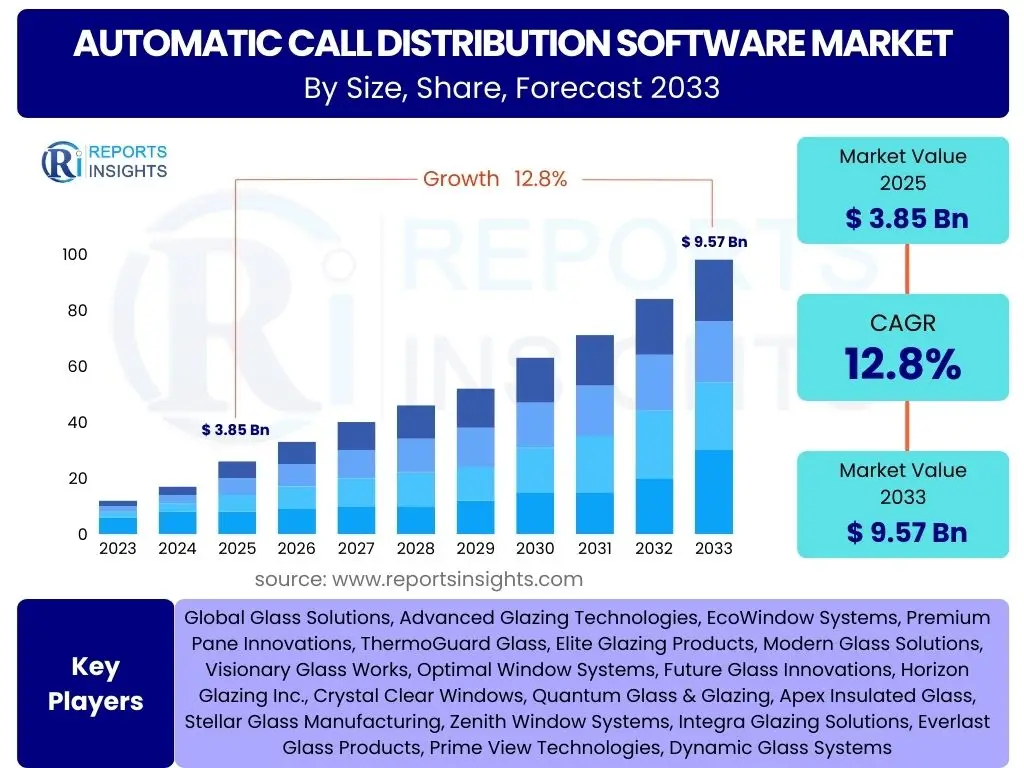

Automatic Call Distribution Software Market Size

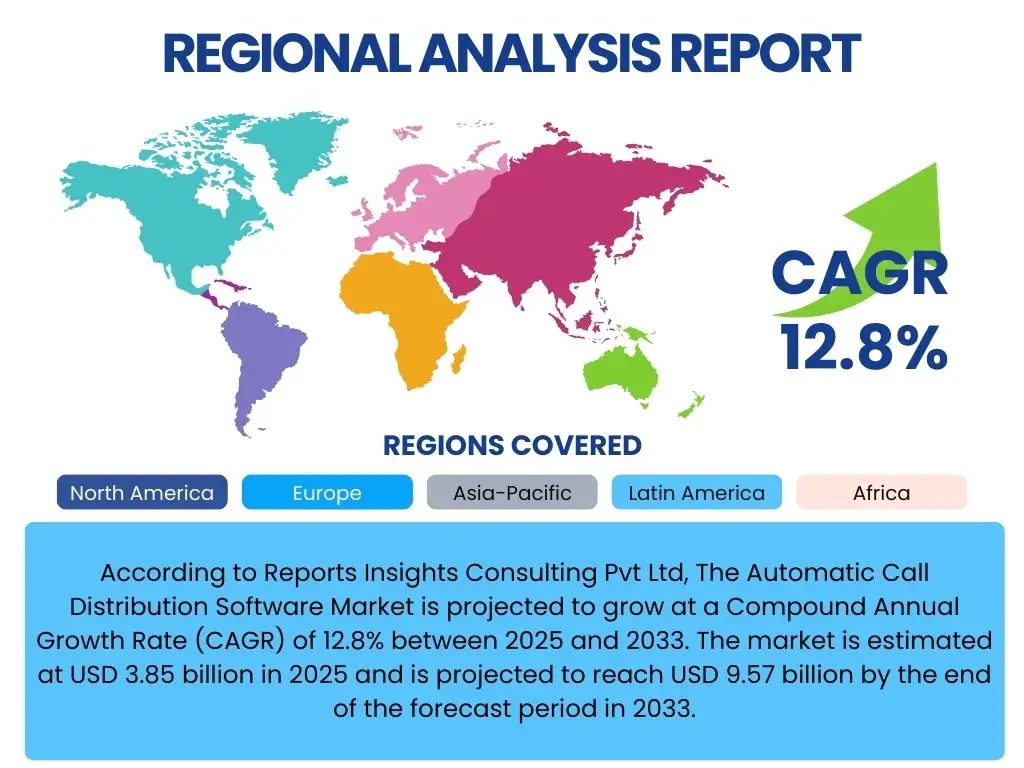

According to Reports Insights Consulting Pvt Ltd, The Automatic Call Distribution Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2033. The market is estimated at USD 3.85 billion in 2025 and is projected to reach USD 9.57 billion by the end of the forecast period in 2033.

Key Automatic Call Distribution Software Market Trends & Insights

The Automatic Call Distribution (ACD) software market is experiencing significant evolution, driven by the increasing demand for efficient and personalized customer service. Stakeholders frequently inquire about the emerging technologies and operational shifts shaping the future of call centers. Key questions revolve around the integration of advanced analytics, the move towards cloud-native solutions, and the importance of seamless omnichannel experiences, all of which are critical for enhancing agent productivity and customer satisfaction.

Furthermore, businesses are keenly observing trends related to remote work capabilities and the necessity for scalable, flexible communication platforms. The desire for real-time data insights to optimize routing strategies and improve first-contact resolution is also a prominent area of interest. These developments collectively point to a market prioritizing intelligent, data-driven, and adaptable ACD solutions.

- Shift towards cloud-based ACD solutions for scalability and flexibility.

- Integration of omnichannel routing for consistent customer experience across touchpoints.

- Emphasis on advanced analytics and reporting for performance optimization.

- Growing adoption of remote agent support features and virtual contact centers.

- Increased focus on personalized routing based on customer history and intent.

AI Impact Analysis on Automatic Call Distribution Software

The integration of Artificial Intelligence (AI) is profoundly transforming Automatic Call Distribution software, addressing common user questions about efficiency, automation, and intelligent routing. Users are particularly interested in how AI can streamline call center operations, reduce agent workload, and provide more personalized customer interactions. AI-driven capabilities such as intelligent routing based on sentiment analysis, predictive analytics for call volumes, and automated self-service options are becoming central to modern ACD systems, moving beyond traditional rule-based distribution.

Concerns often arise regarding the balance between automation and human interaction, as well as the data privacy implications of advanced AI. However, the overarching expectation is that AI will augment, rather than replace, human agents, empowering them with better tools and insights to handle complex queries. AI is anticipated to significantly enhance decision-making in routing, improve customer satisfaction by connecting customers to the most appropriate agent faster, and reduce operational costs through greater efficiency and automation of repetitive tasks.

- Enhanced intelligent routing: AI analyzes customer intent, sentiment, and historical data to route calls to the best-suited agent or department, significantly improving first-contact resolution rates.

- Predictive analytics: AI algorithms forecast call volumes and agent availability, allowing for proactive staffing adjustments and minimizing customer wait times.

- Automated self-service: AI-powered chatbots and virtual assistants handle routine queries, deflecting calls from live agents and providing instant support 24/7.

- Agent assistance: AI provides real-time recommendations, scripts, and information to agents during calls, enhancing their ability to resolve issues efficiently.

- Post-call analysis: AI analyzes call transcripts and recordings to identify trends, agent performance, and customer satisfaction levels, providing valuable insights for training and process improvement.

Key Takeaways Automatic Call Distribution Software Market Size & Forecast

The Automatic Call Distribution (ACD) software market is poised for robust expansion, driven by the imperative for enhanced customer experience and operational efficiency within contact centers globally. Key inquiries from businesses often center on the strategic implications of this growth, including how to leverage advanced ACD functionalities to gain a competitive edge and optimize resource allocation. The forecast indicates sustained investment in solutions that offer greater automation, intelligence, and integration capabilities to meet evolving customer demands.

A crucial insight is the increasing differentiation of ACD solutions through AI and cloud technologies, moving beyond basic call routing to sophisticated, data-driven customer interaction management. Companies are recognizing that modern ACD is not just about distributing calls, but about orchestrating entire customer journeys. This necessitates an understanding of how market growth translates into opportunities for adopting agile, scalable, and highly personalized customer service platforms to stay ahead in a competitive landscape.

- Significant market growth: The ACD software market is projected for substantial expansion, reaching nearly USD 9.6 billion by 2033, indicating strong demand for advanced call routing solutions.

- Cloud-first strategy: Cloud-based ACD solutions will dominate, offering unparalleled scalability, flexibility, and cost-efficiency for contact centers of all sizes.

- AI as a core differentiator: AI integration will be critical for competitive advantage, enabling intelligent routing, predictive analytics, and superior customer engagement.

- Enhanced customer experience: The market will prioritize solutions that deliver seamless omnichannel interactions and highly personalized customer journeys.

- Operational efficiency focus: Businesses will increasingly adopt ACD to optimize agent productivity, reduce operational costs, and improve first-contact resolution rates.

Automatic Call Distribution Software Market Drivers Analysis

The expansion of the Automatic Call Distribution (ACD) software market is predominantly fueled by the global emphasis on elevating customer experience and operational efficiency in contact centers. Businesses across various sectors are recognizing the critical role of streamlined customer interactions in brand loyalty and revenue growth. This drives the demand for sophisticated ACD systems that can intelligently manage call volumes, reduce wait times, and connect customers with the most appropriate resources swiftly.

Furthermore, the rapid digital transformation across industries and the proliferation of omnichannel communication channels necessitate advanced routing capabilities. As customers engage through voice, chat, email, and social media, enterprises require ACD solutions that can integrate these diverse touchpoints into a unified customer journey. This ensures consistency and efficiency, promoting the adoption of modern ACD platforms over traditional, siloed systems.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing demand for enhanced customer experience | +2.5% | Global, particularly North America & Europe | Short to Medium Term (2025-2029) |

| Growing adoption of cloud-based contact center solutions | +2.0% | North America, Europe, Asia Pacific | Medium to Long Term (2026-2033) |

| Rising need for operational efficiency and cost reduction in call centers | +1.8% | Global | Short to Medium Term (2025-2030) |

| Proliferation of omnichannel communication strategies | +1.5% | North America, Europe, Asia Pacific | Medium Term (2027-2032) |

| Integration of Artificial Intelligence and Machine Learning for intelligent routing | +1.7% | Global | Medium to Long Term (2028-2033) |

Automatic Call Distribution Software Market Restraints Analysis

Despite significant growth drivers, the Automatic Call Distribution (ACD) software market faces several restraints that could temper its expansion. A primary concern for many organizations is the substantial initial investment required for implementing advanced ACD systems, particularly for on-premise solutions or comprehensive cloud migrations. This capital outlay can be a significant barrier for small and medium-sized enterprises (SMEs) or companies with limited IT budgets, slowing their adoption of cutting-edge technologies.

Another critical restraint is the complexity associated with integrating new ACD software with existing legacy systems, such as CRM, ERP, and other communication platforms. Seamless interoperability is essential for maximizing the benefits of an ACD system, but achieving this can involve extensive customization, development costs, and potential data migration challenges. Concerns over data security and privacy, especially with cloud-based solutions handling sensitive customer information, also present a notable impediment, requiring robust compliance measures and fostering hesitation among risk-averse organizations.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial implementation costs for advanced systems | -1.2% | Global, particularly developing regions | Short to Medium Term (2025-2029) |

| Integration complexities with existing legacy systems | -1.0% | Global | Medium Term (2026-2031) |

| Data security and privacy concerns, especially for cloud deployments | -0.8% | Europe (GDPR), North America, Asia Pacific | Ongoing (2025-2033) |

| Lack of skilled personnel for managing and optimizing advanced ACD features | -0.7% | Global | Medium to Long Term (2027-2033) |

| Resistance to change within organizations to adopt new technologies | -0.5% | Global | Short to Medium Term (2025-2030) |

Automatic Call Distribution Software Market Opportunities Analysis

The Automatic Call Distribution (ACD) software market presents significant opportunities for growth, primarily driven by the continuous evolution of customer service paradigms and technological advancements. One major area of opportunity lies in the burgeoning adoption of cloud-native ACD solutions by small and medium-sized enterprises (SMEs) and large enterprises alike. The scalability, flexibility, and reduced infrastructure costs associated with cloud platforms enable businesses to implement sophisticated ACD capabilities without extensive capital expenditure, democratizing access to advanced contact center technologies.

Furthermore, the increasing demand for personalized customer engagement and proactive support creates avenues for innovation in ACD. Solutions that leverage AI and machine learning for predictive routing, sentiment analysis, and context-aware interactions can offer a distinct competitive advantage. Opportunities also exist in vertical-specific ACD solutions tailored for industries like healthcare, finance, and retail, addressing unique compliance requirements and operational workflows. The expansion into emerging markets, where contact center infrastructure is still developing, also represents a substantial growth frontier.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into emerging markets with growing contact center demand | +1.8% | Asia Pacific, Latin America, MEA | Medium to Long Term (2027-2033) |

| Development of niche or vertical-specific ACD solutions (e.g., healthcare, finance) | +1.5% | Global | Medium Term (2026-2031) |

| Increased adoption of AI and ML for hyper-personalization and proactive support | +2.2% | North America, Europe, Asia Pacific | Short to Medium Term (2025-2030) |

| Growing demand for integrating ACD with CRM and other business intelligence tools | +1.7% | Global | Medium Term (2026-2032) |

| Shift towards "work-from-anywhere" models driving demand for remote-friendly ACD | +1.6% | North America, Europe | Short to Medium Term (2025-2029) |

Automatic Call Distribution Software Market Challenges Impact Analysis

The Automatic Call Distribution (ACD) software market, while expanding, confronts several inherent challenges that can impact its growth trajectory and adoption rates. One significant challenge is the difficulty in effectively integrating sophisticated ACD systems with the diverse and often fragmented existing IT infrastructure of enterprises. Achieving seamless interoperability with legacy CRM systems, diverse communication channels, and other business applications can be technically complex, resource-intensive, and prone to compatibility issues, delaying deployment and hindering full functionality.

Moreover, the rapid pace of technological innovation, particularly in AI and machine learning, presents a challenge for both vendors and users. Vendors must continually invest in research and development to keep their offerings competitive, while users face the daunting task of understanding, implementing, and optimizing these complex technologies. Cybersecurity threats and ensuring data compliance, especially with the sensitive nature of customer interactions, also pose a continuous and evolving challenge, requiring robust security protocols and adherence to global regulations like GDPR and CCPA, which can increase the total cost of ownership and create adoption hurdles.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with disparate legacy systems and diverse communication channels | -1.1% | Global | Ongoing (2025-2033) |

| Managing data security, privacy, and regulatory compliance (e.g., GDPR, HIPAA) | -0.9% | Europe, North America | Ongoing (2025-2033) |

| Scarcity of skilled professionals to deploy, manage, and optimize advanced ACD solutions | -0.7% | Global | Medium to Long Term (2027-2033) |

| Cost and complexity of continuous updates and technology advancements | -0.6% | Global | Short to Medium Term (2025-2030) |

| Ensuring business continuity and system reliability during implementation and upgrades | -0.5% | Global | Short Term (2025-2028) |

Automatic Call Distribution Software Market - Updated Report Scope

This comprehensive market report provides a detailed analysis of the Automatic Call Distribution (ACD) Software market, encompassing historical data, current trends, and future projections. It delivers an in-depth understanding of market dynamics, segmentation, regional insights, competitive landscape, and the profound impact of emerging technologies like Artificial Intelligence. The report aims to equip stakeholders with actionable insights to navigate market complexities, identify growth opportunities, and formulate informed strategic decisions for the forecast period.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.85 billion |

| Market Forecast in 2033 | USD 9.57 billion |

| Growth Rate | 12.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Cisco Systems, Inc., Genesys, NICE Ltd., Five9, Inc., 8x8, Inc., Avaya Inc., Aspect Software, Inc. (Engage with Aspect), Talkdesk, Inc., LiveVox, Inc., RingCentral, Inc., Vonage, Twilio Inc., 3CX, ShoreTel, Inc. (Mitel), Connect First (acquired by InContact), Serenova (acquired by Lifesize), Bright Pattern, Inc., Evolve IP, Inc., CallTower, Inc., VCC Live |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automatic Call Distribution (ACD) software market is meticulously segmented to provide a granular view of its diverse components and application areas. This segmentation helps in understanding the specific drivers and adoption patterns across different deployment models, enterprise sizes, and industry verticals. By breaking down the market, stakeholders can identify precise opportunities and tailor strategies to address the unique needs of various customer groups, optimizing resource allocation and solution development.

- By Component: Solutions, Services

- By Deployment Model: On-Premise, Cloud-Based

- By Enterprise Size: Large Enterprises, Small & Medium Enterprises (SMEs)

- By Application: Customer Service, Telemarketing, Technical Support, Help Desk, Others

- By Industry Vertical: BFSI, IT & Telecommunications, Retail & E-commerce, Healthcare & Life Sciences, Government & Public Sector, Travel & Hospitality, Manufacturing, Others

Regional Highlights

- North America: Dominates the market due to early adoption of advanced contact center technologies, high concentration of large enterprises, and significant investments in cloud and AI-driven solutions. The presence of key market players also contributes to its leadership.

- Europe: Exhibits robust growth driven by increasing demand for enhanced customer experience, stringent regulatory compliance (e.g., GDPR) necessitating advanced data handling, and widespread adoption of cloud-based services across diverse industries.

- Asia Pacific (APAC): Expected to be the fastest-growing region, propelled by rapid digital transformation, burgeoning e-commerce sectors, expanding BPO activities, and growing awareness among SMEs regarding the benefits of automated customer service. Key countries include China, India, and Japan.

- Latin America: Shows steady growth with increasing investments in IT infrastructure and the adoption of modern contact center solutions, particularly in countries like Brazil and Mexico, focusing on cost-effective cloud solutions.

- Middle East and Africa (MEA): Emerging as a promising market due to government initiatives for digitalization, diversification of economies, and rising customer service demands in sectors like banking and telecommunications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automatic Call Distribution Software Market.- Cisco Systems, Inc.

- Genesys

- NICE Ltd.

- Five9, Inc.

- 8x8, Inc.

- Avaya Inc.

- Aspect Software, Inc. (Engage with Aspect)

- Talkdesk, Inc.

- LiveVox, Inc.

- RingCentral, Inc.

- Vonage

- Twilio Inc.

- 3CX

- ShoreTel, Inc. (Mitel)

- Connect First (acquired by InContact)

- Serenova (acquired by Lifesize)

- Bright Pattern, Inc.

- Evolve IP, Inc.

- CallTower, Inc.

- VCC Live

Frequently Asked Questions

What is Automatic Call Distribution (ACD) software?

Automatic Call Distribution (ACD) software is a system used in call centers to route incoming calls to the most appropriate agent or department based on predefined rules, customer data, and agent availability. Its primary goal is to improve efficiency, reduce wait times, and enhance customer satisfaction by ensuring callers connect with the best-suited resource quickly.

How does AI impact ACD software functionality?

AI significantly enhances ACD software by enabling intelligent routing based on customer intent and sentiment, predicting call volumes, empowering chatbots for self-service, providing real-time agent assistance, and analyzing post-call data for continuous improvement. This leads to more personalized and efficient customer interactions.

What are the main benefits of adopting cloud-based ACD solutions?

Cloud-based ACD solutions offer unparalleled scalability, allowing businesses to easily adjust capacity based on demand. They provide greater flexibility for remote workforces, reduce infrastructure costs, simplify maintenance and updates, and often integrate more seamlessly with other cloud-native business applications, enhancing overall operational agility.

Which industries are the primary adopters of ACD software?

ACD software is widely adopted across various industries, including Banking, Financial Services, and Insurance (BFSI), IT & Telecommunications, Retail & E-commerce, Healthcare & Life Sciences, and Government & Public Sector. Any sector with high volumes of customer interaction benefits significantly from intelligent call routing and management.

What are the key challenges in implementing new ACD software?

Key challenges in implementing new ACD software include integrating with existing legacy systems, managing data security and privacy compliance, the high initial cost of advanced systems, and the need for skilled personnel to configure and optimize complex features. Ensuring seamless transition and maintaining business continuity during deployment are also critical considerations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted