Automated Teller Machine Market

Automated Teller Machine Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706535 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

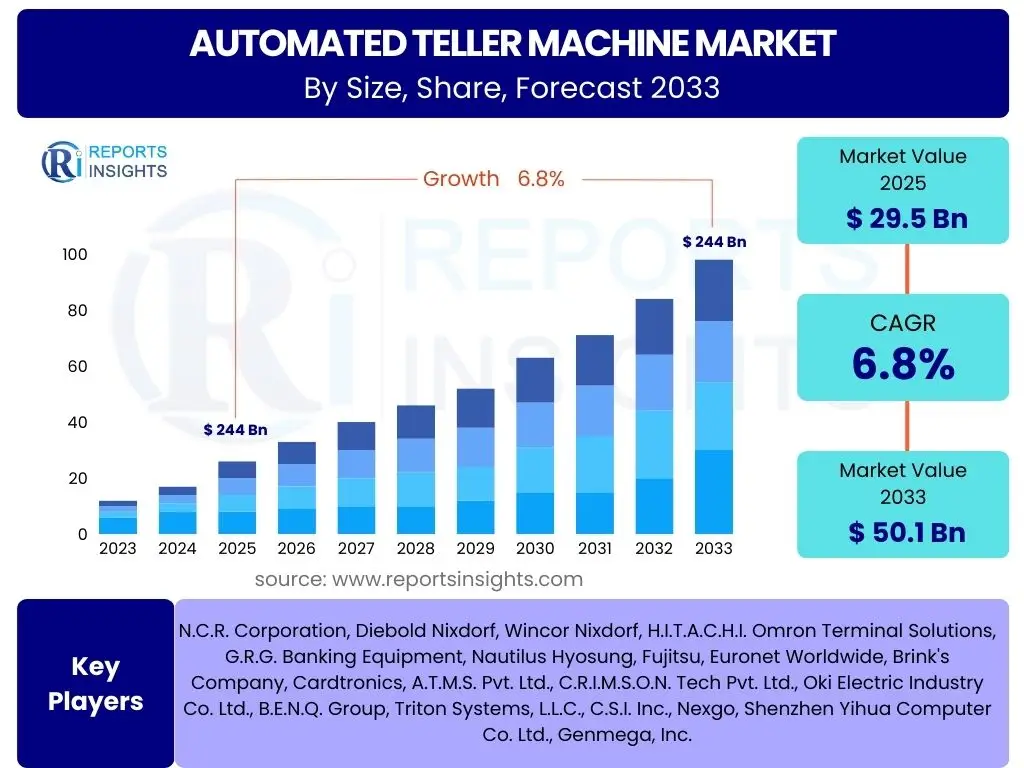

Automated Teller Machine Market Size

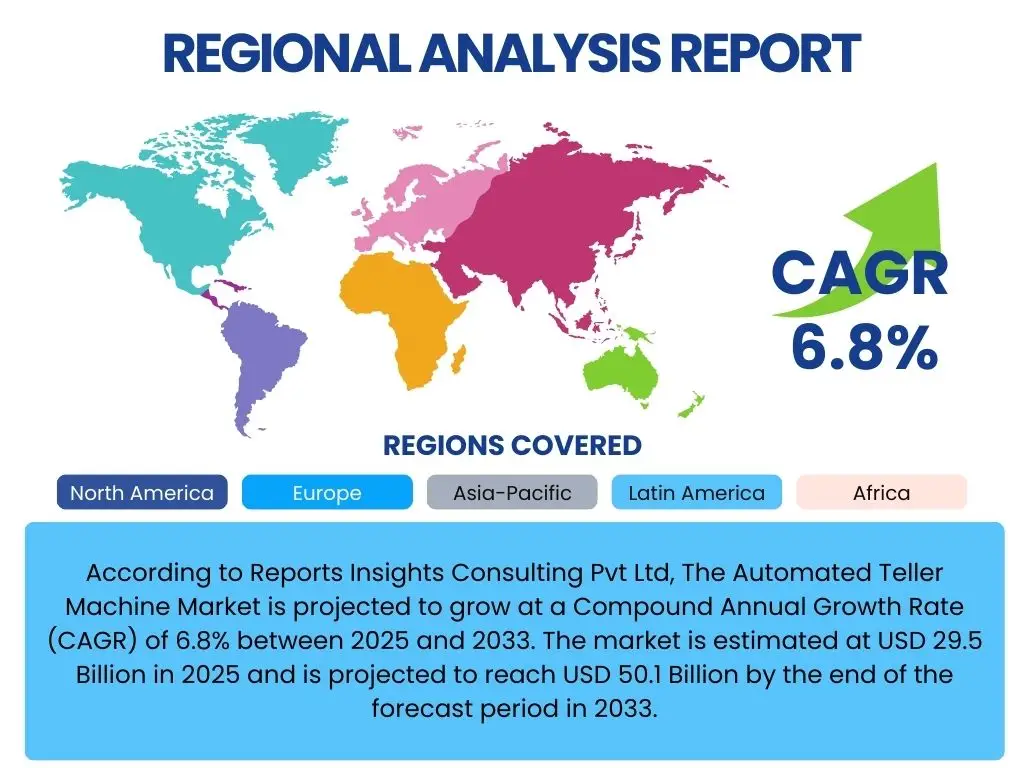

According to Reports Insights Consulting Pvt Ltd, The Automated Teller Machine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 29.5 Billion in 2025 and is projected to reach USD 50.1 Billion by the end of the forecast period in 2033.

Key Automated Teller Machine Market Trends & Insights

The Automated Teller Machine (ATM) market is undergoing significant transformation, driven by a confluence of technological advancements, evolving consumer behaviors, and strategic adaptations by financial institutions. Users frequently inquire about the enduring relevance of ATMs in an increasingly digital world, the types of new services ATMs are offering, and how security concerns are being addressed. This analysis reveals a market that is not shrinking but rather repositioning itself, moving beyond basic cash transactions to become multi-functional service hubs that complement digital banking channels.

A prominent trend is the shift from purely cash-dispensing machines to advanced, full-service terminals capable of a wider array of transactions, including bill payments, cardless withdrawals, account opening, and even biometric authentication. Financial institutions are investing in smart ATMs that provide an elevated customer experience, mimicking some of the services traditionally offered by bank tellers. This evolution is crucial for maintaining customer engagement and providing accessibility for those who still prefer or require physical banking interactions, especially in regions with varying levels of digital adoption.

Furthermore, there is a growing emphasis on enhancing the security features of ATMs and improving their operational efficiency through predictive maintenance and remote monitoring. As digital fraud becomes more sophisticated, so too do the countermeasures integrated into ATM systems, including advanced surveillance, anti-skimming technologies, and robust encryption protocols. The market is also seeing a rise in white-label and brown-label ATMs, particularly in emerging economies, expanding access to financial services in underserved areas and contributing to financial inclusion initiatives.

- Transition to multi-functional smart ATMs offering diverse services beyond cash.

- Integration of advanced security features like biometric authentication and anti-skimming.

- Increased adoption of cardless and QR code-based transaction capabilities.

- Expansion of white-label and brown-label ATMs in non-bank locations.

- Focus on predictive maintenance and remote management for operational efficiency.

- Development of ATMs as mini-branches to offer personalized customer interactions.

AI Impact Analysis on Automated Teller Machine

The integration of Artificial Intelligence (AI) is set to profoundly reshape the Automated Teller Machine (ATM) landscape, addressing common user questions about the future capabilities, security, and efficiency of these banking touchpoints. Users often wonder how AI can enhance the user experience, improve fraud detection, and streamline maintenance for ATMs. AI's analytical capabilities allow for a deeper understanding of customer behavior and transaction patterns, enabling ATMs to offer more personalized services and anticipate user needs, thereby transforming a transactional device into a more interactive and intelligent self-service portal.

In terms of security, AI is revolutionizing fraud detection and prevention at ATMs. Machine learning algorithms can analyze vast amounts of transaction data in real-time to identify anomalies and suspicious patterns that might indicate fraudulent activity, far surpassing traditional rule-based systems. This proactive approach helps mitigate risks such as card skimming, unauthorized withdrawals, and other forms of financial crime, thereby enhancing the overall security posture of ATM networks and increasing customer trust. Beyond security, AI also plays a crucial role in predictive maintenance, allowing service providers to anticipate hardware failures or cash replenishment needs before they become critical issues, minimizing downtime and improving operational efficiency.

Furthermore, AI-powered voice assistance and natural language processing are improving accessibility and user interaction for ATMs, making them more user-friendly for diverse populations, including those with disabilities. AI can also optimize cash management by predicting demand more accurately across different locations, reducing instances of ATMs running out of cash or holding excessive reserves. This comprehensive integration of AI transforms ATMs from static machines into dynamic, intelligent agents that contribute significantly to a seamless and secure banking ecosystem.

- Enhanced fraud detection through real-time anomaly analysis and behavioral biometrics.

- Predictive maintenance for reduced downtime and optimized cash management.

- Personalized customer experiences via AI-driven recommendations and user profiling.

- Improved accessibility and user interaction with AI-powered voice assistance and chatbots.

- Optimization of ATM network deployment based on AI-driven demand forecasting.

- Automated incident response and remote troubleshooting enabled by intelligent systems.

Key Takeaways Automated Teller Machine Market Size & Forecast

Key takeaways from the Automated Teller Machine market size and forecast reveal a dynamic sector undergoing strategic evolution rather than outright decline. Users frequently question the long-term viability of ATMs given the rise of digital payments and cashless economies. However, the market forecast indicates continued growth, albeit with a shifting focus. This growth is primarily fueled by the sustained demand for cash in many regions, the critical role of ATMs in financial inclusion, and their transformation into comprehensive service points that bridge the gap between digital and physical banking.

The market's resilience is largely attributed to the ongoing modernization of ATM infrastructure and the expansion of financial services in emerging economies. While mature markets may see consolidation and an emphasis on advanced functionality and enhanced security, developing regions are experiencing an increase in ATM deployment to cater to a burgeoning banked population and to facilitate easier access to financial transactions. The investment in smart ATMs, capable of diverse transactions, solidifies their position as essential components of the omnichannel banking strategy.

Overall, the Automated Teller Machine market is not merely surviving but adapting. Its future lies in becoming intelligent, secure, and versatile self-service banking terminals that support a hybrid banking model. The forecast growth underscores the continuous relevance of physical cash access and the convenience offered by strategically located ATMs, making them an indispensable part of the global financial infrastructure for the foreseeable future.

- The ATM market is experiencing steady growth, driven by modernization and expansion in emerging economies.

- ATMs are evolving into multi-functional service hubs, extending beyond simple cash transactions.

- Financial inclusion initiatives globally heavily rely on ATM networks, particularly in underserved areas.

- Technological advancements, including AI and biometrics, are key to enhancing security and user experience.

- Despite the rise of digital payments, cash remains a crucial medium in many parts of the world, sustaining ATM demand.

- The market's future is characterized by intelligent, secure, and integrated self-service banking solutions.

Automated Teller Machine Market Drivers Analysis

The Automated Teller Machine market is propelled by several robust drivers that underscore its continued relevance in the global financial ecosystem. A primary driver is the enduring demand for cash, particularly in regions where digital payment infrastructure is less developed or where a significant portion of transactions still occur in physical currency. Even in highly digitized economies, ATMs serve as a crucial touchpoint for cash access, emergency withdrawals, and specific transactions like remittances or certain bill payments, catering to diverse consumer preferences and needs. This persistent demand ensures a fundamental base for ATM services.

Another significant driver is the global push for financial inclusion. In many developing countries, ATMs are often the first and most accessible point of contact for individuals entering the formal banking system. They provide essential services like balance inquiries, withdrawals, and deposits in areas where bank branches may be scarce, thereby empowering unbanked and underbanked populations. Furthermore, the continuous innovation in ATM functionalities, such as cardless transactions, biometric authentication, and the ability to process a wider array of banking services, enhances convenience and attracts more users, acting as a strong growth catalyst for the market.

The strategic expansion by banks and independent ATM deployers (IADs) into new geographies and non-traditional locations also contributes substantially to market growth. As urban centers expand and rural areas gain access to banking, the deployment of ATMs ensures widespread availability of financial services. Additionally, the increasing need for efficiency in banking operations leads financial institutions to leverage ATMs for automated services, reducing the burden on human tellers and streamlining branch operations, which directly impacts the market positively.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Persistent Demand for Cash and Physical Transactions | +1.5% | Asia Pacific, Latin America, Middle East & Africa, Europe | Short to Mid-term (2025-2030) |

| Growing Financial Inclusion Initiatives | +1.2% | Asia Pacific (India, China), Latin America (Brazil, Mexico), MEA | Mid to Long-term (2025-2033) |

| Technological Advancements and Enhanced Functionalities | +1.0% | North America, Europe, Asia Pacific | Ongoing (2025-2033) |

| Expansion of ATM Networks into New Locations | +0.8% | Emerging Markets Globally | Mid-term (2025-2030) |

| Banks' Focus on Operational Efficiency and Cost Reduction | +0.7% | Global | Ongoing (2025-2033) |

Automated Teller Machine Market Restraints Analysis

Despite the positive growth drivers, the Automated Teller Machine market faces several significant restraints that could impede its expansion. A primary concern is the escalating adoption of digital payment methods, including mobile payments, online banking, and contactless cards. In many developed economies, there is a clear trend towards cashless transactions, reducing the reliance on physical currency and, consequently, the demand for ATM withdrawals. This shift in consumer preference directly impacts the frequency of ATM usage and the economic viability of maintaining extensive ATM networks for some financial institutions.

Another considerable restraint is the high operational and maintenance costs associated with ATMs. These costs include hardware procurement, software licensing, physical security measures, cash management (replenishment and collection), network connectivity, and regular servicing. For financial institutions, especially smaller banks and credit unions, the capital expenditure and ongoing operational expenses of ATMs can be substantial. This financial burden can lead to a consolidation or reduction in ATM fleet sizes, particularly in areas with lower transaction volumes or higher digital adoption rates, thereby limiting market growth.

Furthermore, security threats, such as card skimming, malware attacks, and physical tampering, pose a continuous challenge. The need for constant upgrades to security hardware and software, along with compliance with evolving regulatory standards like PCI DSS, adds to the complexity and cost of ATM operations. The inherent vulnerability of physical cash and the infrastructure required to secure it acts as a deterrent for both providers and users in certain contexts, pushing some consumers towards digital alternatives perceived as more secure or convenient. These multifaceted challenges necessitate ongoing innovation and strategic adaptation from market participants.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption of Digital Payments | -1.3% | North America, Europe, China | Ongoing (2025-2033) |

| High Operational and Maintenance Costs of ATMs | -1.0% | Global | Ongoing (2025-2033) |

| Growing Security Threats and Fraud Attempts | -0.8% | Global | Ongoing (2025-2033) |

| Stringent Regulatory Compliance Requirements | -0.6% | Europe, North America | Ongoing (2025-2033) |

| Declining Cash Usage in Developed Economies | -0.5% | Scandinavia, UK, Canada, Australia | Long-term (2028-2033) |

Automated Teller Machine Market Opportunities Analysis

Despite the challenges, the Automated Teller Machine market is ripe with opportunities that can drive substantial future growth. A significant opportunity lies in the integration of ATMs with digital banking platforms and fintech solutions. By allowing users to initiate transactions on their mobile devices and complete them at an ATM, or by offering services like cryptocurrency purchases and bill payments for a wider range of utilities, ATMs can become vital bridge points in an omnichannel banking strategy. This synergy enhances the overall customer experience and leverages the existing physical infrastructure for new digital-era services, making ATMs more versatile and attractive to a tech-savvy generation.

Emerging markets, particularly in Asia Pacific, Latin America, and Africa, present vast untapped potential for ATM deployment. These regions often have large unbanked populations and rapidly developing economies where access to traditional banking infrastructure is limited. ATMs can serve as cost-effective and efficient channels for financial inclusion, providing essential services to millions who are just entering the formal financial system. The demand for basic cash services, coupled with the increasing adoption of digital payment methods that still require cash-out points, creates a robust environment for ATM expansion in these areas.

Furthermore, the evolution of ATMs into advanced service terminals that offer services beyond cash transactions, such as opening accounts, applying for loans, and providing video conferencing with bank representatives, represents a significant growth avenue. These "smart ATMs" or "assisted self-service terminals" can reduce the need for physical branch visits, lower bank operational costs, and offer a premium, personalized experience. Investing in such high-value, feature-rich ATMs provides a competitive edge and secures the long-term relevance of the ATM in a transforming financial landscape, capitalizing on the convenience of 24/7 self-service and the efficiency of automation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Digital Banking and Fintech Solutions | +1.4% | Global | Ongoing (2025-2033) |

| Expansion in Emerging and Underserved Markets | +1.3% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-term (2025-2033) |

| Evolution into Advanced Self-Service Terminals | +1.1% | North America, Europe, Developed Asia Pacific | Ongoing (2025-2033) |

| Increased Demand for Cardless and Biometric Transactions | +0.9% | Global | Mid-term (2025-2030) |

| ATMs as Hubs for Non-Banking Services (e.g., Ticket Sales, Cryptocurrency) | +0.7% | Specific Niche Markets, Urban Centers | Long-term (2028-2033) |

Automated Teller Machine Market Challenges Impact Analysis

The Automated Teller Machine market faces several inherent challenges that demand strategic responses from industry players to sustain growth and relevance. One of the most pressing challenges is the escalating threat of cyberattacks and advanced fraud schemes. As ATMs become more integrated with digital networks and offer broader services, they become more attractive targets for sophisticated criminals employing malware, phishing, and physical tampering methods like sophisticated skimming devices. Protecting sensitive customer data and ensuring transaction integrity requires continuous investment in cutting-edge security technologies and regular software updates, which can be costly and complex for deployers.

Another significant challenge stems from the rapid pace of technological change and the potential for hardware obsolescence. ATMs are long-term capital investments, but the components and software within them can become outdated quickly, necessitating frequent upgrades or even complete replacement to maintain competitiveness and compliance. This continuous need for modernization places a considerable financial burden on financial institutions and independent deployers, especially in a market where transaction volumes might be declining in some segments due to digital migration. Balancing the cost of new technology with return on investment becomes a critical strategic decision.

Furthermore, the changing consumer behavior, driven by a preference for mobile and online banking, poses a fundamental challenge to the traditional role of ATMs. While ATMs are adapting to offer more diverse services, convincing consumers to utilize these physical channels when digital alternatives are often more convenient remains a hurdle. Regulatory complexities, including data privacy laws and financial compliance standards, also add layers of operational difficulty, requiring diligent adherence and regular audits. Addressing these multifaceted challenges effectively is crucial for the long-term viability and growth of the ATM market, pushing industry participants towards innovative and adaptive solutions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Cybersecurity Risks and Sophisticated Fraud | -1.1% | Global | Ongoing (2025-2033) |

| Rapid Technological Obsolescence and Upgrade Costs | -0.9% | Global | Ongoing (2025-2033) |

| Evolving Consumer Preference for Digital Channels | -0.7% | Developed Economies | Long-term (2028-2033) |

| Intense Competition from Alternative Payment Methods | -0.6% | Global | Ongoing (2025-2033) |

| Compliance with Complex and Changing Regulations | -0.4% | Europe, North America | Ongoing (2025-2033) |

Automated Teller Machine Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Automated Teller Machine (ATM) market, delivering a detailed understanding of its current landscape, historical performance, and future growth trajectories. It encompasses a thorough examination of market size, trends, drivers, restraints, opportunities, and challenges affecting the industry. The scope includes a detailed segmentation analysis, regional insights, and profiles of key market players, offering a holistic view of the market dynamics and strategic foresight for stakeholders seeking to navigate the evolving financial technology sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 29.5 Billion |

| Market Forecast in 2033 | USD 50.1 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | N.C.R. Corporation, Diebold Nixdorf, Wincor Nixdorf, H.I.T.A.C.H.I. Omron Terminal Solutions, G.R.G. Banking Equipment, Nautilus Hyosung, Fujitsu, Euronet Worldwide, Brink's Company, Cardtronics, A.T.M.S. Pvt. Ltd., C.R.I.M.S.O.N. Tech Pvt. Ltd., Oki Electric Industry Co. Ltd., B.E.N.Q. Group, Triton Systems, L.L.C., C.S.I. Inc., Nexgo, Shenzhen Yihua Computer Co. Ltd., Genmega, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automated Teller Machine market is intricately segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for a precise analysis of specific product types, deployment strategies, functional capabilities, and solution offerings, revealing tailored insights into consumer preferences and market opportunities across different verticals and geographies. Understanding these segments is crucial for stakeholders to develop targeted strategies and optimize resource allocation within the evolving ATM ecosystem.

- By Type: This segment distinguishes between Traditional ATMs, which primarily handle cash dispensing, and Smart ATMs, offering advanced functionalities like cheque deposits, bill payments, and cardless transactions. Also included are Brown Label ATMs (owned by a service provider but branded by a bank) and White Label ATMs (owned and operated by non-bank entities).

- By Location: Categorizes ATMs based on their physical placement, including On-premise (within bank branches), Off-premise (retail stores, shopping malls, airports), and Worksite (corporate campuses, factories).

- By Deployment: Differentiates between Indoor ATMs, typically found within enclosed spaces, and Outdoor ATMs, which are exposed to external environments and often require more robust design.

- By Function: This critical segment breaks down the market by the specific services an ATM provides, such as basic Cash Dispensing, Cash Deposit, advanced Card-less Transactions, Account Services (balance inquiry, mini-statements), Bill Payments, Statement Printing, and Check Cashing.

- By Solution: Divides the market into the core components that make up an ATM system. This includes Hardware (e.g., cash dispensers, deposit modules, card readers, printers, security systems), Software (e.g., transaction management, security software, monitoring software), and Services (e.g., managed services, installation and maintenance, consulting services).

Regional Highlights

- North America: This region represents a mature ATM market characterized by a focus on technological innovation and the modernization of existing infrastructure. While cash usage has seen some decline due to pervasive digital payment adoption, ATMs are transforming into sophisticated self-service terminals offering a wide range of services beyond cash, including interactive video teller capabilities and biometric authentication. The emphasis is on enhancing convenience, security, and integration with digital banking channels to provide a seamless omnichannel experience. Consolidation of ATM networks and strategic placement in high-traffic retail locations are key trends.

- Europe: Europe showcases a diverse ATM landscape. Western European countries are rapidly moving towards cashless societies, prompting banks to reduce their ATM footprints and invest in high-tech, multi-functional ATMs that streamline branch operations. Conversely, Eastern and Southern European nations still exhibit robust cash demand, driving steady deployment of traditional ATMs alongside smart ATMs for basic financial access. Stringent regulatory frameworks for security and data privacy significantly influence ATM development and deployment across the continent, fostering continuous innovation in compliance and fraud prevention technologies.

- Asia Pacific (APAC): APAC is the fastest-growing market for ATMs, driven by vast unbanked populations, increasing financial literacy, and rapid urbanization, particularly in emerging economies like India, China, and Southeast Asian countries. The region sees massive deployments of both traditional ATMs for basic financial inclusion and smart ATMs to cater to a burgeoning middle class. The rise of independent ATM deployers (IADs) and white-label ATMs is prominent, expanding access to financial services in rural and semi-urban areas. Mobile payment integration with ATMs for cash-in/cash-out services is also a significant trend.

- Latin America: This region is experiencing significant growth in the ATM market, fueled by ongoing efforts towards financial inclusion and the high prevalence of cash-based economies. Brazil, Mexico, and Argentina are key markets where ATMs play a vital role in providing banking services to a large segment of the population, especially in remote areas. There is a growing demand for advanced security features and multi-functional ATMs capable of handling bill payments and remittances. Economic volatility and varying regulatory environments across countries present unique challenges and opportunities for ATM deployers.

- Middle East and Africa (MEA): The MEA region presents substantial growth opportunities for the ATM market, driven by increasing urbanization, economic development, and initiatives to bring financial services to underserved populations. Countries in the GCC region (e.g., UAE, Saudi Arabia) are investing in advanced, high-tech ATMs with enhanced security and personalized services to cater to a digitally savvy population. In contrast, many African nations are seeing significant growth in basic ATM deployment to expand financial access, particularly through white-label and brown-label models, making ATMs crucial for bridging the financial gap.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automated Teller Machine Market.- N.C.R. Corporation

- Diebold Nixdorf

- Wincor Nixdorf

- H.I.T.A.C.H.I. Omron Terminal Solutions

- G.R.G. Banking Equipment

- Nautilus Hyosung

- Fujitsu

- Euronet Worldwide

- Brink's Company

- Cardtronics

- A.T.M.S. Pvt. Ltd.

- C.R.I.M.S.O.N. Tech Pvt. Ltd.

- Oki Electric Industry Co. Ltd.

- B.E.N.Q. Group

- Triton Systems, L.L.C.

- C.S.I. Inc.

- Nexgo

- Shenzhen Yihua Computer Co. Ltd.

- Genmega, Inc.

Frequently Asked Questions

Analyze common user questions about the Automated Teller Machine market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current growth trajectory of the Automated Teller Machine market?

The Automated Teller Machine (ATM) market is projected for steady growth, with a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. This growth is driven by modernization, expansion in emerging markets, and the evolution of ATMs into multi-functional self-service terminals, despite the rise of digital payments.

Are ATMs becoming obsolete with the rise of digital payments?

No, ATMs are not becoming obsolete but are instead evolving. While digital payments reduce some cash transactions, ATMs are adapting by offering a wider range of services, including cardless transactions, bill payments, and biometric authentication. They serve as essential physical touchpoints in an increasingly omnichannel banking environment, particularly for cash access and financial inclusion in many regions.

How is Artificial Intelligence (AI) impacting ATM operations?

AI is significantly impacting ATMs by enhancing fraud detection through real-time anomaly analysis, improving operational efficiency via predictive maintenance, and personalizing customer experiences. AI-powered voice assistance and optimized cash management also contribute to more secure, efficient, and user-friendly ATM services, transforming them into intelligent banking points.

What are the key drivers for the Automated Teller Machine market?

Key drivers include the persistent global demand for cash, especially in emerging economies, alongside initiatives promoting financial inclusion. Technological advancements that expand ATM functionalities beyond basic cash services, such as cardless transactions and biometric authentication, also play a crucial role, making ATMs more convenient and versatile.

What are the primary challenges facing the ATM market?

The main challenges for the ATM market involve increasing cybersecurity risks and sophisticated fraud attempts, requiring continuous investment in security. Additionally, the rapid pace of technological obsolescence and the associated upgrade costs, coupled with evolving consumer preferences towards digital banking channels, present significant hurdles for market players to overcome.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted