Automated Assembly Market

Automated Assembly Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705502 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

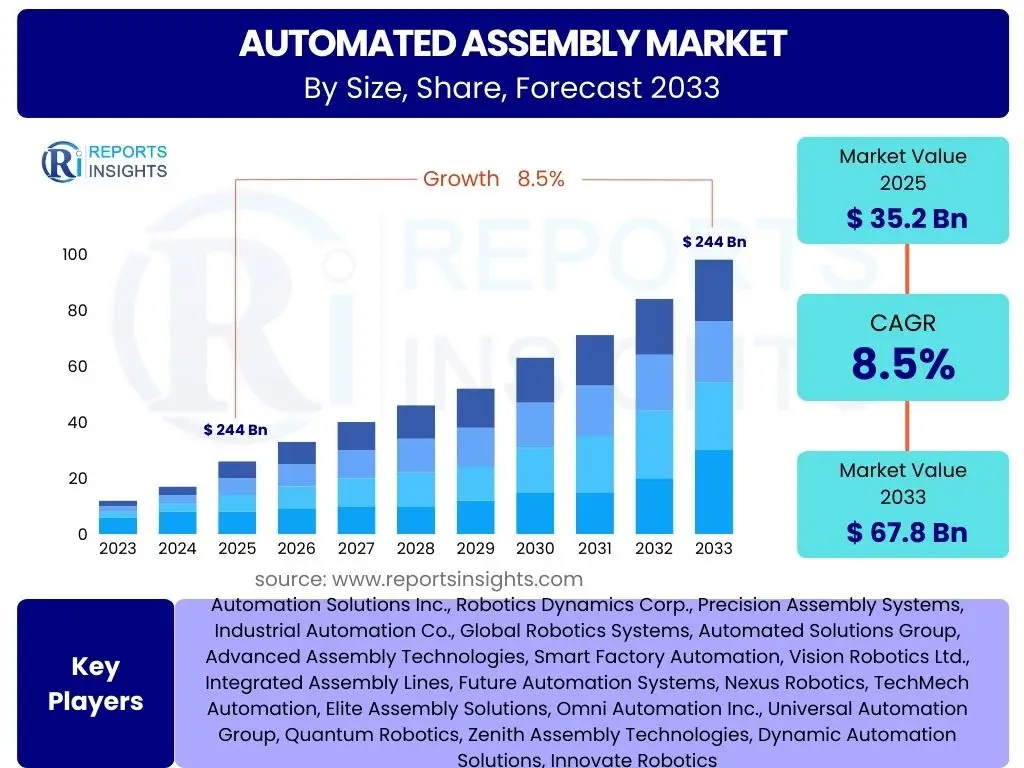

Automated Assembly Market Size

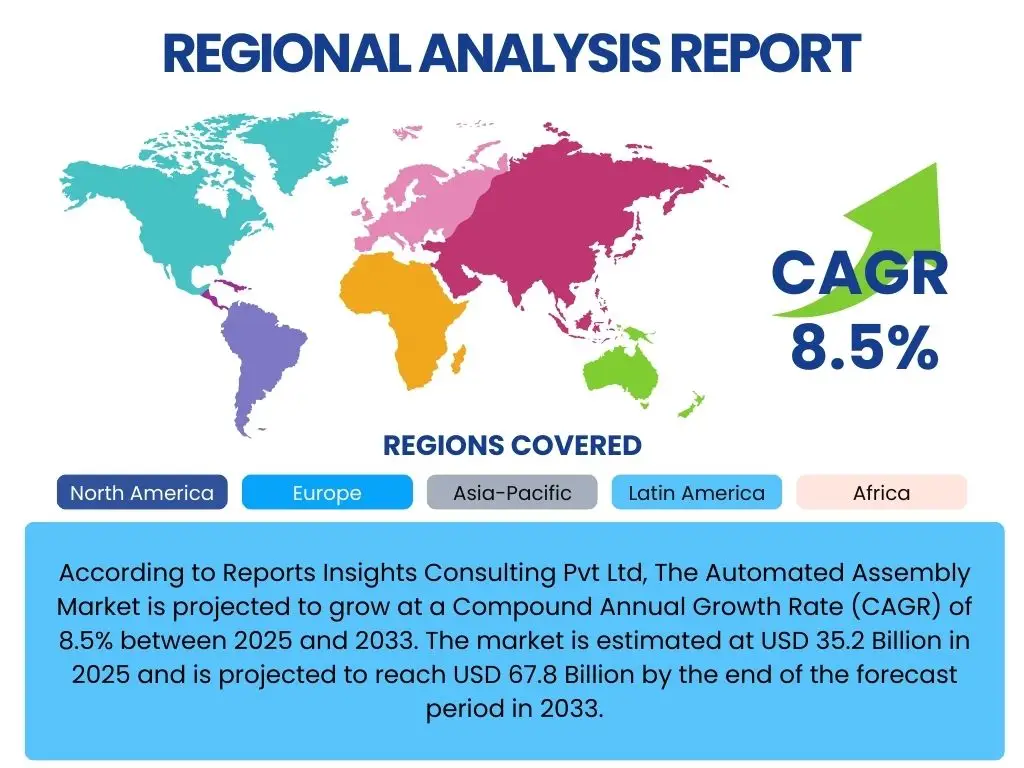

According to Reports Insights Consulting Pvt Ltd, The Automated Assembly Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 35.2 Billion in 2025 and is projected to reach USD 67.8 Billion by the end of the forecast period in 2033.

Key Automated Assembly Market Trends & Insights

Users frequently inquire about the evolving landscape of automated assembly, particularly concerning the integration of advanced technologies and shifts in manufacturing paradigms. A key theme revolves around the increasing adoption of Industry 4.0 principles, driving demand for more connected, intelligent, and flexible assembly lines. This includes the proliferation of collaborative robots (cobots), which work alongside human operators, and the integration of sophisticated vision systems for enhanced quality control and precision. The market is also witnessing a trend towards modular and reconfigurable assembly systems, allowing manufacturers greater agility to adapt to changing product designs and production volumes.

Another significant insight points to the growing emphasis on data-driven decision-making within automated assembly operations. Manufacturers are leveraging sensor data, machine learning algorithms, and real-time analytics to optimize processes, predict maintenance needs, and improve overall equipment effectiveness (OEE). This focus on digitalization extends to the development of digital twins for assembly lines, enabling virtual commissioning, simulation, and continuous improvement without disrupting physical operations. Furthermore, the push for sustainable manufacturing practices is influencing design choices in automated assembly, with a focus on energy efficiency and reduced material waste.

- Increased adoption of collaborative robots (cobots) for human-robot interaction.

- Prevalence of Industry 4.0 and Smart Factory initiatives.

- Expansion of advanced vision systems for enhanced quality and precision.

- Shift towards modular and reconfigurable assembly solutions.

- Integration of real-time data analytics and machine learning for process optimization.

- Development and utilization of digital twin technology for simulation and planning.

- Growing demand for flexible manufacturing systems to support mass customization.

- Emphasis on energy efficiency and sustainable practices in automated assembly.

AI Impact Analysis on Automated Assembly

Users commonly seek to understand how artificial intelligence (AI) is transforming automated assembly operations, particularly regarding efficiency, adaptability, and fault detection. AI is profoundly impacting this sector by enabling machines to learn from data, make intelligent decisions, and perform tasks with greater autonomy and precision. This includes AI-powered vision systems that can identify complex defects or variances with higher accuracy than traditional systems, leading to superior quality control. Furthermore, machine learning algorithms are being applied to optimize robot paths, improve pick-and-place accuracy, and reduce cycle times, thereby boosting overall throughput.

The influence of AI extends to predictive maintenance and anomaly detection, allowing manufacturers to anticipate equipment failures before they occur, minimizing downtime and optimizing maintenance schedules. AI also facilitates adaptive manufacturing, where assembly lines can automatically adjust to variations in product specifications or material properties, enhancing flexibility and reducing the need for manual reprogramming. The integration of AI with advanced robotics is fostering more intelligent and autonomous assembly cells capable of handling diverse tasks and complex product variants, ushering in an era of highly agile and self-optimizing production environments.

- AI-driven vision systems for advanced defect detection and quality assurance.

- Machine learning algorithms optimizing robot motion, path planning, and task execution.

- Predictive maintenance enabled by AI for reduced downtime and increased equipment lifespan.

- Adaptive manufacturing processes driven by AI for real-time adjustments to production.

- Enhanced human-robot collaboration through AI-powered contextual awareness.

- AI supporting autonomous decision-making in complex assembly sequences.

- Data analytics and AI for comprehensive process optimization and efficiency gains.

Key Takeaways Automated Assembly Market Size & Forecast

Common user inquiries about the Automated Assembly market's future center on its growth trajectory, the underlying drivers, and its implications for manufacturing productivity and competitiveness. A primary takeaway is the significant and sustained growth projected for the market, driven by a global push towards industrial automation, optimization of manufacturing processes, and the imperative to reduce operational costs. This growth is underpinned by advancements in robotics, AI, and connectivity, making automated assembly increasingly accessible and beneficial across a wider range of industries. The market is transitioning from traditional fixed automation to more flexible, intelligent, and collaborative systems.

Another key insight is the increasing integration of automated assembly solutions across diverse industrial applications, moving beyond traditional automotive and electronics sectors into medical devices, consumer goods, and aerospace. This diversification highlights the versatility and adaptability of modern assembly technologies. Furthermore, the market's expansion is closely linked to the global labor shortage crisis, prompting companies to invest in automation to maintain production levels and ensure quality. The forecast indicates that investments in automated assembly will be a critical strategy for manufacturers seeking to enhance efficiency, achieve higher precision, and foster innovation in product development over the coming decade.

- Significant and consistent market growth driven by global automation trends.

- Increased adoption across a broad spectrum of industries beyond traditional manufacturing.

- Technological advancements in robotics, AI, and vision systems are key growth enablers.

- Strategic investment in automation to address labor shortages and enhance productivity.

- Shift towards flexible, intelligent, and collaborative automated assembly solutions.

- Emphasis on precision manufacturing and improved quality control via automation.

- Critical role of automated assembly in achieving competitive advantage and fostering innovation.

Automated Assembly Market Drivers Analysis

The Automated Assembly Market is significantly driven by several macroeconomic and technological factors that compel industries to adopt advanced manufacturing solutions. A primary driver is the rising labor costs across various industrialized nations and the increasing scarcity of skilled labor, which forces manufacturers to seek automated alternatives to maintain production capacity and efficiency. Automation provides a viable solution by reducing reliance on manual labor, improving consistency, and enhancing the overall speed of assembly processes.

Furthermore, the growing demand for high-quality, high-precision products across sectors such as electronics, medical devices, and automotive necessitates the implementation of automated assembly systems. These systems are capable of achieving tolerances and repeatability that are difficult to consistently replicate manually. The push towards Industry 4.0 and smart manufacturing initiatives also serves as a strong catalyst, encouraging investments in interconnected and intelligent assembly lines that offer real-time data analysis, predictive maintenance, and optimized workflows. Additionally, increasing global competition is compelling manufacturers to enhance productivity and reduce time-to-market, which automated assembly effectively facilitates.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Labor Costs & Shortages | +1.2% | North America, Europe, East Asia | Short to Mid-term (2025-2030) |

| Increasing Demand for High-Precision Products | +0.9% | Global, particularly APAC, Europe | Mid to Long-term (2025-2033) |

| Industry 4.0 & Smart Manufacturing Adoption | +1.1% | Global, especially Developed Economies | Short to Mid-term (2025-2030) |

| Enhanced Production Efficiency & Cost Reduction | +0.8% | Global | Short to Long-term (2025-2033) |

| Government Initiatives & Support for Automation | +0.7% | China, Germany, Japan, USA | Mid-term (2025-2030) |

Automated Assembly Market Restraints Analysis

Despite the significant growth potential, the Automated Assembly Market faces several inherent restraints that could impede its widespread adoption. The substantial initial capital investment required for implementing sophisticated automated assembly systems is a primary barrier, particularly for small and medium-sized enterprises (SMEs). This high upfront cost includes not only the machinery itself but also the necessary software, integration services, and infrastructure upgrades, making it a significant financial commitment that many businesses might find prohibitive.

Another crucial restraint is the technical complexity associated with integrating, programming, and maintaining advanced automation systems. A lack of specialized skills within the existing workforce to operate and troubleshoot these complex systems can lead to operational bottlenecks and increased training costs. Furthermore, the rapid pace of technological advancements, while a driver, also poses a restraint as existing systems can become obsolete relatively quickly, necessitating frequent upgrades or replacements, which adds to the long-term cost burden. Cybersecurity concerns related to interconnected manufacturing systems and potential data breaches also present a significant challenge, requiring robust security measures that can add to implementation complexities and costs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment & Setup Costs | -1.0% | Global, particularly SMEs | Short to Mid-term (2025-2030) |

| Technical Complexity & Integration Challenges | -0.8% | Global | Short to Mid-term (2025-2030) |

| Lack of Skilled Workforce for Maintenance & Operation | -0.7% | Global | Short to Mid-term (2025-2030) |

| Rapid Technological Obsolescence | -0.6% | Global | Mid to Long-term (2025-2033) |

| Cybersecurity Risks & Data Privacy Concerns | -0.5% | Global | Mid to Long-term (2025-2033) |

Automated Assembly Market Opportunities Analysis

The Automated Assembly Market is ripe with numerous opportunities for expansion and innovation, driven by evolving industrial needs and technological breakthroughs. A significant opportunity lies in the burgeoning adoption of automated solutions by Small and Medium-sized Enterprises (SMEs). Historically, automation was largely confined to large corporations due to high costs, but the advent of more affordable, flexible, and easy-to-deploy robotic systems, including collaborative robots (cobots), is making automation accessible to a broader range of businesses. This untapped market segment offers substantial growth potential as SMEs seek to enhance their competitiveness and productivity.

Another key opportunity emerges from the increasing demand for customized and personalized products, which necessitates highly flexible and reconfigurable assembly lines. Automated systems, particularly those integrated with AI and advanced vision, are uniquely positioned to handle mass customization efficiently without significant retooling. Furthermore, the expansion into new application areas beyond traditional manufacturing, such as specialized medical device assembly, food and beverage processing, and logistics automation, presents significant avenues for market growth. The ongoing development of digital twin technology and simulation tools also creates opportunities for manufacturers to optimize assembly processes virtually before physical implementation, leading to faster deployment and reduced risk.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption by SMEs | +1.3% | Global, particularly Emerging Markets | Mid to Long-term (2025-2033) |

| Growth in New Application Areas | +1.0% | Global, diverse industries | Mid to Long-term (2025-2033) |

| Rise of Flexible & Reconfigurable Systems | +0.9% | Global | Short to Mid-term (2025-2030) |

| Advancements in AI & Machine Learning for Optimization | +0.8% | Global | Short to Long-term (2025-2033) |

| Development of Digital Twin & Simulation Technologies | +0.7% | Global | Mid-term (2025-2030) |

Automated Assembly Market Challenges Impact Analysis

The Automated Assembly Market, while promising, is not without its significant challenges that could affect the pace of its adoption and technological evolution. One major challenge is the inherent complexity of integrating diverse components and software systems from multiple vendors into a cohesive, functional automated assembly line. Achieving seamless communication and interoperability between robots, vision systems, conveyors, and various control software often requires extensive customization and expertise, which can lead to extended deployment times and higher costs.

Another critical challenge lies in managing the rapid pace of technological change and ensuring that automated systems remain relevant and efficient in the long term. As new generations of robots, sensors, and AI algorithms emerge, manufacturers face the dilemma of investing in cutting-edge technology versus leveraging existing infrastructure, leading to potential upgrade cycles and compatibility issues. Furthermore, ensuring the safety of human workers in environments where collaborative robots operate alongside them presents complex safety protocol and certification challenges. The scarcity of highly specialized talent capable of designing, implementing, and maintaining these advanced systems also poses a substantial hurdle, limiting the rate at which industries can fully embrace automation.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex System Integration & Interoperability | -0.9% | Global | Short to Mid-term (2025-2030) |

| Managing Rapid Technological Obsolescence | -0.7% | Global | Mid to Long-term (2025-2033) |

| Ensuring Workplace Safety with Collaborative Robots | -0.6% | Global, highly regulated regions | Short to Mid-term (2025-2030) |

| Talent Shortage in Automation Expertise | -0.8% | Global | Short to Mid-term (2025-2030) |

| High Energy Consumption & Sustainability Concerns | -0.5% | Global, particularly Europe | Mid to Long-term (2025-2033) |

Automated Assembly Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Automated Assembly Market, covering historical data, current market trends, and future growth projections. It meticulously examines the market drivers, restraints, opportunities, and challenges influencing the industry's trajectory. The scope includes detailed segmentation analysis by various factors, regional insights, and profiles of key industry players, offering a holistic view for strategic decision-making and competitive intelligence.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 35.2 Billion |

| Market Forecast in 2033 | USD 67.8 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Automation Solutions Inc., Robotics Dynamics Corp., Precision Assembly Systems, Industrial Automation Co., Global Robotics Systems, Automated Solutions Group, Advanced Assembly Technologies, Smart Factory Automation, Vision Robotics Ltd., Integrated Assembly Lines, Future Automation Systems, Nexus Robotics, TechMech Automation, Elite Assembly Solutions, Omni Automation Inc., Universal Automation Group, Quantum Robotics, Zenith Assembly Technologies, Dynamic Automation Solutions, Innovate Robotics |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automated Assembly Market is comprehensively segmented to provide a detailed understanding of its diverse components and application areas. This segmentation allows for precise market analysis, identifying key growth areas, and understanding industry-specific nuances. The market is primarily segmented by type of system, including robotic assembly, automated inspection, and material handling, reflecting the various operational capabilities offered by automation. Each type addresses specific manufacturing needs, from high-speed production to intricate quality verification.

Further segmentation by component provides insight into the technological building blocks of these systems, such as industrial robots, vision systems, control software, and end-effectors, highlighting the supply chain and technological dependencies. Segmentation by end-user industry, including automotive, electronics, medical devices, and food & beverages, illustrates the widespread adoption and customization of automated solutions across different manufacturing verticals, each with unique requirements and standards. Finally, the market is also broken down by specific operations performed, such as pick & place, joining, or testing, and by automation level (semi-automated vs. fully automated), offering a granular view of the market's structure and potential for growth in specific niches.

- By Type: Robotic Assembly Systems, Automated Inspection Systems, Automated Material Handling Systems, Automated Feeding & Dispensing Systems.

- By Component: Robots (Articulated, SCARA, Delta, Collaborative, Cartesian), Vision Systems (Cameras, Lighting, Software), Control Systems (PLCs, HMIs, Industrial PCs), Conveyors & Material Transport, End-Effectors (Grippers, Tools), Sensors & Actuators, Software (PLC Programming, Robotic Simulation, MES, SCADA).

- By End-User Industry: Automotive, Electronics & Electrical, Medical Devices & Pharmaceuticals, Food & Beverages, Aerospace & Defense, Consumer Goods, Heavy Machinery & Industrial Equipment, Logistics & Packaging.

- By Operation: Pick & Place, Joining (Welding, Fastening, Gluing), Dispensing & Coating, Testing & Inspection, Packaging & Palletizing, Material Removal.

- By Automation Level: Semi-Automated, Fully Automated.

Regional Highlights

- North America: This region is characterized by early adoption of advanced manufacturing technologies, strong emphasis on smart factories, and significant investment in automation due to rising labor costs. The United States and Canada are leading the market, driven by robust automotive, aerospace, and electronics industries. There is a growing trend towards reshoring manufacturing, further boosting automation demand.

- Europe: A mature market for automated assembly, with Germany being a key innovator and adopter, particularly in the automotive and industrial machinery sectors. The region benefits from strong government support for Industry 4.0 initiatives and a focus on high-precision manufacturing. Scandinavian countries and France are also showing increasing adoption rates, propelled by sustainability goals and efficiency drives.

- Asia Pacific (APAC): Expected to be the fastest-growing market, primarily due to rapid industrialization, increasing manufacturing output, and significant investments in automation by countries like China, Japan, South Korea, and India. China leads in volume and scale of adoption, while Japan excels in robotics technology. The region's large manufacturing base across electronics, automotive, and consumer goods fuels substantial demand for automated assembly solutions.

- Latin America: An emerging market with growing potential, particularly in countries like Mexico and Brazil. The region's proximity to North American markets and increasing foreign investments in manufacturing contribute to the adoption of automated assembly, especially within the automotive and consumer goods sectors.

- Middle East & Africa (MEA): This region is witnessing gradual adoption of automated assembly solutions, driven by diversification efforts from oil-dependent economies towards industrialization and smart city initiatives. Countries like UAE and Saudi Arabia are investing in advanced manufacturing to build sustainable economic futures, creating niche opportunities for automation.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automated Assembly Market.- ABB Ltd.

- FANUC Corporation

- Kuka AG (Midea Group)

- Yaskawa Electric Corporation

- Universal Robots A/S (Teradyne Inc.)

- Omron Corporation

- Festo AG & Co. KG

- Bosch Rexroth AG

- SMC Corporation

- Kawasaki Heavy Industries, Ltd.

- Comau S.p.A. (Stellantis)

- Mecademic Inc.

- Epson Robots (Seiko Epson Corporation)

- Denso Wave Inc.

- Staubli International AG

- Robotiq Inc.

- Adept Technology (Omron Corporation)

- Nidec Corporation

- SCHUNK GmbH & Co. KG

- SoftBank Robotics Group Corp.

Frequently Asked Questions

What is automated assembly?

Automated assembly refers to the use of machines, robots, and computer-controlled systems to perform tasks involved in assembling products, replacing or augmenting manual labor. It encompasses processes like part feeding, precise placement, joining, fastening, and quality inspection, often integrated into a continuous production line.

What are the primary benefits of implementing automated assembly systems?

The primary benefits include significant improvements in production efficiency, enhanced product quality and consistency, reduced labor costs, increased safety for workers, and greater throughput. Automated systems minimize human error, operate continuously, and can handle repetitive or hazardous tasks with precision.

Which industries are the largest adopters of automated assembly?

The automotive, electronics and electrical, medical devices, and consumer goods industries are historically the largest adopters of automated assembly. These sectors benefit immensely from the high precision, speed, and consistency that automation provides for complex product manufacturing.

How does AI impact the future of automated assembly?

AI is transforming automated assembly by enabling smarter decision-making, predictive maintenance, adaptive manufacturing, and enhanced quality control through advanced vision systems. It allows assembly lines to be more flexible, efficient, and capable of handling greater product variation without extensive reprogramming.

What are the main challenges in adopting automated assembly solutions?

Key challenges include high initial investment costs, the technical complexity of system integration, the need for a skilled workforce to operate and maintain the systems, and concerns regarding rapid technological obsolescence and cybersecurity risks. These factors require careful planning and strategic investment.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted