Asbesto Cement Pipe Market

Asbesto Cement Pipe Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709882 | Last Updated : December 22, 2025 |

Format : ![]()

![]()

![]()

![]()

Asbesto Cement Pipe Market Size

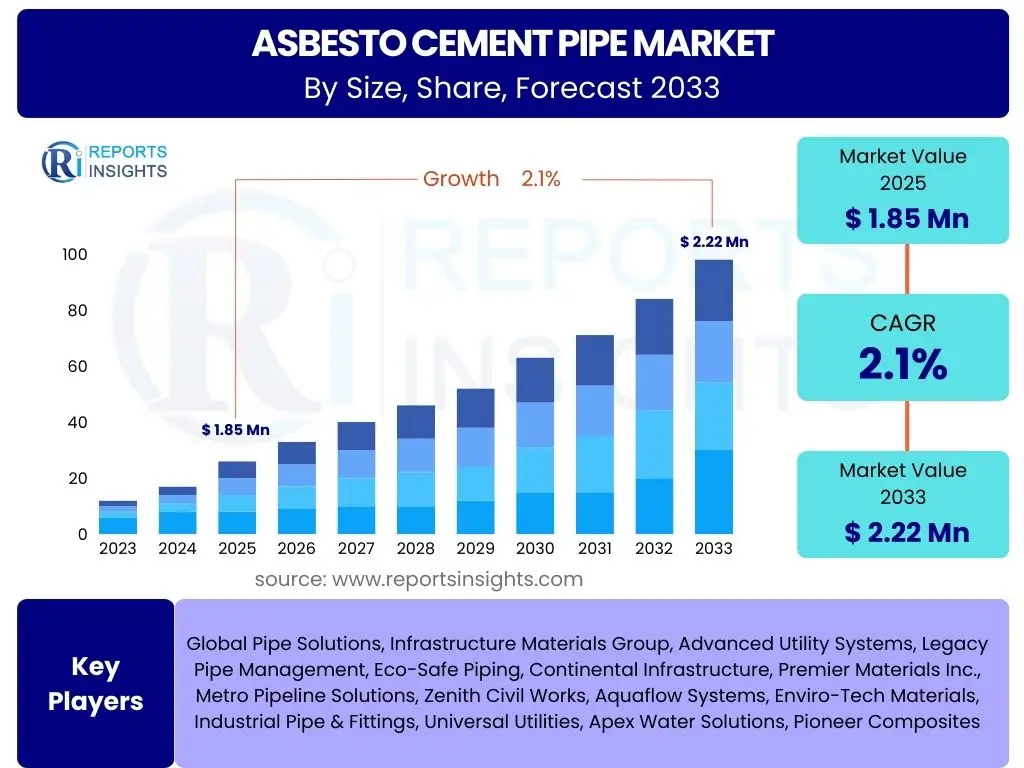

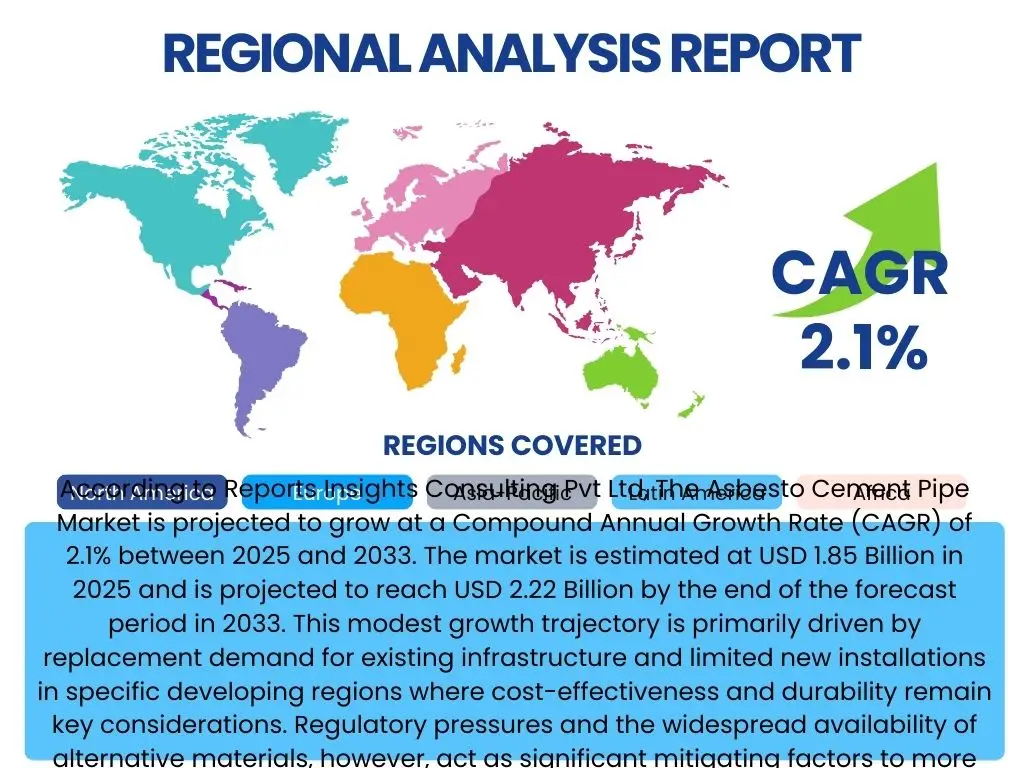

According to Reports Insights Consulting Pvt Ltd, The Asbesto Cement Pipe Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 2.1% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 2.22 Billion by the end of the forecast period in 2033. This modest growth trajectory is primarily driven by replacement demand for existing infrastructure and limited new installations in specific developing regions where cost-effectiveness and durability remain key considerations. Regulatory pressures and the widespread availability of alternative materials, however, act as significant mitigating factors to more substantial expansion.

Despite the prevailing negative perception and health concerns associated with asbestos, certain legacy applications and economic factors in particular geographies continue to sustain a niche market. Maintenance and repair of extensive pre-existing asbestos cement pipe networks, particularly in water and sewage systems, represent a substantial component of current market activity. The market's valuation reflects a balance between the phase-out efforts in developed nations and continued, albeit cautious, usage in areas prioritizing immediate infrastructure solutions.

Key Asbesto Cement Pipe Market Trends & Insights

Users frequently inquire about the enduring relevance of asbestos cement pipes, given the health risks and regulatory shifts. Key trends indicate a declining global market, heavily influenced by stringent health regulations and the transition to safer alternative materials. However, a significant trend involves the management and replacement of vast existing asbestos cement pipe infrastructure, particularly in water and wastewater networks, which contributes to ongoing demand for assessment, removal, and replacement services. Another emerging trend, though not directly in new pipe production, is the development of innovative, non-asbestos fiber cement materials that seek to replicate the desirable properties of traditional AC pipes without the associated health hazards, often leveraging sustainable or recycled components.

Furthermore, there is a trend towards specialized applications in regions where the material's durability and cost-efficiency are prioritized for specific industrial or non-potable water transport uses, especially in developing economies. Regulatory bodies are increasingly focusing on safe disposal methods and robust remediation protocols for existing installations, driving a segment focused on environmental compliance and public safety. Lastly, technological advancements in pipeline inspection and maintenance are aiding in the precise identification and prioritization of deteriorating asbestos cement pipes, allowing for more targeted and efficient replacement programs, thereby influencing market demand for related services.

- Global decline in new installations due to health concerns and regulations.

- Increasing focus on safe removal and replacement of existing legacy infrastructure.

- Rise in demand for non-asbestos fiber cement pipe alternatives.

- Cost-effectiveness and durability maintaining niche demand in developing regions.

- Technological advancements in inspection and maintenance of pipe networks.

AI Impact Analysis on Asbesto Cement Pipe

User questions regarding AI's impact on the asbestos cement pipe sector often center on how technology can mitigate risks, improve operational efficiency, or even identify new applications. While direct AI involvement in the manufacturing of new asbestos cement pipes is minimal due to the material's declining new production, AI significantly influences related aspects such as predictive maintenance, infrastructure management, and environmental monitoring. AI-powered analytics can process sensor data from aging pipe networks to predict failures, identify leakages, and prioritize sections for repair or replacement, thereby optimizing maintenance schedules and reducing operational costs for utilities managing these legacy systems. This predictive capability extends the useful life of existing infrastructure while informing strategic replacement decisions.

Moreover, AI and machine learning algorithms are increasingly being applied in material science research to develop advanced composite materials that offer superior properties without the use of asbestos, potentially creating a new generation of high-performance, safe piping solutions. AI can also assist in risk assessment and compliance monitoring by analyzing vast datasets related to environmental regulations, health impacts, and disposal protocols, ensuring safer handling and management of asbestos-containing materials during demolition or renovation projects. This shift from manufacturing to management and innovation of alternatives highlights AI's role in addressing the challenges posed by this legacy material.

- Predictive maintenance for existing asbestos cement pipe networks to extend lifespan and prevent failures.

- Optimized scheduling and resource allocation for safe removal and replacement projects using AI algorithms.

- AI-driven material science research for developing safe, high-performance fiber cement alternatives.

- Enhanced risk assessment and environmental compliance monitoring for asbestos-containing materials.

- Improved data analysis for infrastructure management and strategic planning in water utilities.

Key Takeaways Asbesto Cement Pipe Market Size & Forecast

Analysis of user questions regarding the market's trajectory consistently points to concerns about the balance between health risks, regulatory pressures, and the practicalities of managing vast existing infrastructure. The primary takeaway is that while new production of asbestos cement pipes is severely constrained globally, the market sustains itself through the extensive maintenance, repair, and eventual replacement of existing networks. This creates a specialized demand focused on asset management, safe handling, and the transition to alternative materials rather than traditional growth in manufacturing. The market's modest growth forecast reflects this dynamic, where the economic lifespan of installed pipes and the pace of their replacement largely dictate activity.

Another crucial insight is the significant regional disparity in market dynamics. Developed nations are primarily concerned with abatement and disposal, whereas some developing countries, driven by infrastructure needs and economic constraints, still consider asbestos cement pipes for specific applications, albeit with increasing awareness and regulatory scrutiny. The market is thus less about expansion and more about strategic management of a legacy material, with a growing emphasis on sustainability, worker safety, and environmental protection. Future innovation will primarily focus on non-asbestos alternatives and advanced asset management tools.

- Market growth driven by replacement and maintenance of existing infrastructure, not new installations.

- Stringent health regulations and environmental concerns are the primary market shapers.

- Significant regional variations in demand, with developing economies showing some sustained usage.

- Focus is shifting towards safe removal, disposal, and adoption of alternative piping materials.

- Market stability hinges on asset management strategies for legacy asbestos cement pipe networks.

Asbesto Cement Pipe Market Drivers Analysis

The asbestos cement pipe market, despite its well-documented challenges, continues to be influenced by several underlying drivers that sustain its presence in specific niches. A primary driver is the extensive existing infrastructure of asbestos cement pipes, particularly in water and sewage systems globally, installed decades ago due to their durability and cost-effectiveness at the time. The sheer volume of these installed pipes necessitates ongoing maintenance, repair, and eventual replacement, creating a persistent demand for services and, in some cases, specialized replacement materials. The economic lifespan of these pipes often extends beyond initial projections, prolonging the need for their management.

Furthermore, in certain developing economies, the initial low cost of installation and the inherent durability of asbestos cement pipes, combined with limited immediate access to more expensive modern alternatives, can still drive demand for specific non-potable water transport or drainage applications. This is often seen in regions where rapid infrastructure development is a priority and budget constraints are significant. While this driver is diminishing due to increased global awareness and regulatory pressures, it still plays a role in localized markets, particularly for non-pressure applications or in industrial settings where direct human contact is minimized and supervised.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Aging infrastructure and replacement demand | +1.5% | Global, particularly North America, Europe | Short to Mid-term (2025-2030) |

| Cost-effectiveness in developing economies | +0.8% | Parts of Asia Pacific, Latin America, Africa | Short-term (2025-2028) |

| Durability and resistance to corrosion | +0.5% | Niche industrial applications, specific regions | Short-term (2025-2027) |

| Specific non-potable water transport needs | +0.3% | Select emerging markets | Short-term (2025-2027) |

Asbesto Cement Pipe Market Restraints Analysis

The primary and most significant restraint on the asbestos cement pipe market is the overwhelming health and safety concerns associated with asbestos fibers. Inhalation of these fibers is linked to severe respiratory diseases, including asbestosis, lung cancer, and mesothelioma, leading to widespread bans and stringent regulations on the use, manufacturing, and even handling of asbestos-containing materials across most developed nations and increasingly in developing ones. This has drastically reduced new production and shifted focus towards remediation and alternative materials, severely limiting the market's growth potential. Public awareness and negative perception further compound these regulatory pressures, making new installations virtually impossible in many regions.

Another substantial restraint is the increasing availability and cost-competitiveness of alternative piping materials. Modern materials such as ductile iron, PVC, HDPE, fiberglass, and other fiber-reinforced composites offer comparable or superior performance characteristics in terms of strength, corrosion resistance, and durability, without the health risks. Continuous innovation in these alternative materials, coupled with economies of scale in their production, makes them a preferred choice for new infrastructure projects. Furthermore, the high costs associated with the safe removal, disposal, and remediation of existing asbestos cement pipes often outweigh any initial cost benefits, thereby acting as a disincentive for their continued use or replacement with similar materials.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Health risks and regulatory bans on asbestos | -3.0% | Global, particularly North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Availability of superior alternative materials | -1.8% | Global | Mid to Long-term (2025-2033) |

| High costs of safe disposal and remediation | -1.2% | Global | Mid to Long-term (2025-2033) |

| Negative public perception and liability concerns | -1.0% | Global | Long-term (2025-2033) |

Asbesto Cement Pipe Market Opportunities Analysis

Despite the prevailing negative sentiment, the asbestos cement pipe market does present certain opportunities, primarily in the domain of legacy infrastructure management. A significant opportunity lies in the specialized services for the inspection, assessment, and safe encapsulation or removal of existing asbestos cement pipelines. As these pipes age, municipalities and industrial entities require expert guidance and execution for their management, offering a niche for specialized engineering firms and contractors. This segment is driven by environmental regulations and public safety concerns, creating a sustained demand for professional services focused on responsible asset retirement and replacement planning.

Another area of opportunity exists in the development and adoption of non-asbestos fiber cement pipe technologies. Researchers and manufacturers are exploring new composite materials that replicate the strength, durability, and cost-effectiveness of traditional asbestos cement, but without hazardous components. Innovations utilizing basalt fibers, synthetic fibers, or cellulose fibers combined with cement offer a pathway to meet the demand for robust, affordable piping solutions in areas that historically relied on AC pipes. This presents a growth avenue for companies investing in research and development of these next-generation, environmentally sound alternatives, particularly for non-pressure and storm water applications in developing regions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Specialized services for existing AC pipe management (inspection, removal, disposal) | +1.0% | Global, especially North America, Europe | Mid to Long-term (2025-2033) |

| Development and adoption of non-asbestos fiber cement alternatives | +0.7% | Global, with emphasis on Asia Pacific, Latin America | Mid to Long-term (2025-2033) |

| Market for recycled materials from deconstructed AC pipes (post-treatment) | +0.4% | Europe, North America | Long-term (2028-2033) |

| Niche demand for robust, cost-effective piping in non-sensitive applications in emerging markets | +0.3% | Specific regions in Asia, Africa | Short to Mid-term (2025-2030) |

Asbesto Cement Pipe Market Challenges Impact Analysis

The asbestos cement pipe market faces severe challenges, primarily stemming from the pervasive health risks associated with asbestos exposure. The ongoing legal liabilities, strict regulatory frameworks, and public health concerns create a hostile environment for any new installations and drive the demand for costly and complex removal and disposal procedures. Companies involved in manufacturing or distribution, even of historical products, face significant reputational damage and legal scrutiny. This forces a rapid shift away from asbestos-containing materials towards safer alternatives, thereby constricting the market for traditional asbestos cement pipes to a near-zero growth rate in many regions.

Furthermore, the high capital expenditure required for establishing or maintaining safe manufacturing processes for asbestos-containing products, combined with the declining demand and increasing operational costs due to stringent health and safety protocols, makes continued production economically unviable for most manufacturers. The lack of investment in research and development for asbestos cement pipe enhancements, coupled with the robust innovation in alternative materials, further exacerbates the challenge. Managing the environmental impact of disposal and ensuring worker safety during handling and removal operations represent continuous and evolving challenges that impose significant financial and logistical burdens on market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent regulatory enforcement and legal liabilities | -2.5% | Global | Long-term (2025-2033) |

| High capital and operational costs for safe manufacturing/handling | -1.5% | Global | Mid to Long-term (2025-2033) |

| Lack of new market entrants and innovation for AC pipes | -1.0% | Global | Long-term (2025-2033) |

| Competition from advanced and safer alternative materials | -0.8% | Global | Mid to Long-term (2025-2033) |

Asbesto Cement Pipe Market - Updated Report Scope

This market insights report provides an in-depth analysis of the Asbesto Cement Pipe market, covering historical data, current market dynamics, and future projections. It examines key trends, drivers, restraints, opportunities, and challenges shaping the industry from 2019 to 2033. The scope encompasses market size estimations, growth rate forecasts, segmentation analysis by type, application, and end-use, alongside a comprehensive review of the competitive landscape and regional market performance. The report also integrates an impact assessment of AI technologies on sector operations and strategic decision-making, offering a holistic view for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 2.22 Billion |

| Growth Rate | 2.1% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Pipe Solutions, Infrastructure Materials Group, Advanced Utility Systems, Legacy Pipe Management, Eco-Safe Piping, Continental Infrastructure, Premier Materials Inc., Metro Pipeline Solutions, Zenith Civil Works, Aquaflow Systems, Enviro-Tech Materials, Industrial Pipe & Fittings, Universal Utilities, Apex Water Solutions, Pioneer Composites |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Asbesto Cement Pipe market is primarily segmented by pipe type, application, and end-use, reflecting the diverse, albeit niche, contexts in which these materials are still relevant. The type segmentation distinguishes between pressure pipes, typically used in water distribution, and non-pressure pipes, common for drainage and sewage. This distinction is crucial as pressure applications often demand higher material integrity and consistent performance. The application segmentation further refines this by categorizing usage across critical infrastructure sectors such as water supply, sewage, and drainage, as well as specific industrial and agricultural contexts where their unique properties might still be utilized. Each segment experiences different levels of demand and faces varying regulatory scrutiny.

The end-use segmentation provides insights into the primary consumers of asbestos cement pipes and related services. Municipal and public works sectors constitute a significant portion due to their responsibility for vast existing infrastructure networks. Industrial and agricultural sectors also contribute to demand for specialized applications, often driven by factors like chemical resistance or cost-efficiency in specific, controlled environments. Residential and commercial sectors typically have less direct involvement in new installations but are impacted by the need for safe removal and replacement of existing pipes within their properties or connecting infrastructure. Understanding these segmentations helps in pinpointing the remaining areas of market activity and the most prevalent types of engagement.

- By Type

- Pressure Pipes

- Non-Pressure Pipes

- By Application

- Water Supply Systems

- Sewage Systems

- Drainage Systems

- Industrial Applications

- Agricultural Irrigation

- By End-Use

- Municipal & Public Works

- Industrial Sector

- Residential Sector

- Commercial Sector

Regional Highlights

- North America: Characterized by significant efforts in asbestos abatement and replacement of aging water and wastewater infrastructure. The market here is predominantly driven by remediation services, with stringent regulations governing removal and disposal. Focus on safe alternatives and advanced pipe inspection technologies.

- Europe: Similar to North America, Europe shows strong regulatory control and a concerted push towards phasing out asbestos cement pipes. Key activities include systematic replacement programs, investment in non-asbestos alternatives, and extensive research into safe material management.

- Asia Pacific (APAC): Exhibits a mixed market dynamic. While developed economies within APAC are transitioning away from asbestos cement, certain developing nations still utilize them for non-potable water and drainage due to cost constraints and rapid infrastructure development needs. Growing awareness and regulation are slowly shifting this trend.

- Latin America: The region experiences ongoing demand for affordable infrastructure solutions, with asbestos cement pipes still in use for some non-pressure applications. However, increasing environmental and health awareness is gradually leading to a decline in new installations and a rise in replacement projects.

- Middle East and Africa (MEA): Represents a region with some sustained, albeit declining, usage of asbestos cement pipes, particularly in water and sewage infrastructure where cost-effectiveness and durability are critical. Regulatory landscapes vary significantly by country, influencing market dynamics.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Asbesto Cement Pipe Market.- Global Pipe Solutions

- Infrastructure Materials Group

- Advanced Utility Systems

- Legacy Pipe Management

- Eco-Safe Piping

- Continental Infrastructure

- Premier Materials Inc.

- Metro Pipeline Solutions

- Zenith Civil Works

- Aquaflow Systems

- Enviro-Tech Materials

- Industrial Pipe & Fittings

- Universal Utilities

- Apex Water Solutions

- Pioneer Composites

Frequently Asked Questions

Analyze common user questions about the Asbesto Cement Pipe market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current growth forecast for the Asbestos Cement Pipe market?

The Asbesto Cement Pipe market is projected for modest growth at a CAGR of 2.1% from 2025 to 2033, driven mainly by replacement demand for existing infrastructure and niche applications in developing regions.

What are the primary drivers influencing the Asbestos Cement Pipe market?

Key drivers include the extensive installed base of aging AC pipes requiring replacement or maintenance, and their historical cost-effectiveness and durability in specific, often non-potable, applications in some emerging economies.

What are the major restraints affecting the Asbestos Cement Pipe market?

Major restraints include severe health risks associated with asbestos, stringent global regulations and bans, the increasing availability of safer and competitive alternative piping materials, and high costs for safe disposal and remediation.

How is AI impacting the Asbestos Cement Pipe industry?

AI primarily impacts the industry through predictive maintenance for existing pipe networks, optimizing removal and replacement projects, and facilitating research into non-asbestos alternative materials, rather than new pipe manufacturing.

What opportunities exist within the Asbestos Cement Pipe market?

Opportunities are found in specialized services for the inspection, safe removal, and disposal of existing AC pipes, and in the research and development of non-asbestos fiber cement alternatives.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted