Artificial Tendon and Ligament Market

Artificial Tendon and Ligament Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705975 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

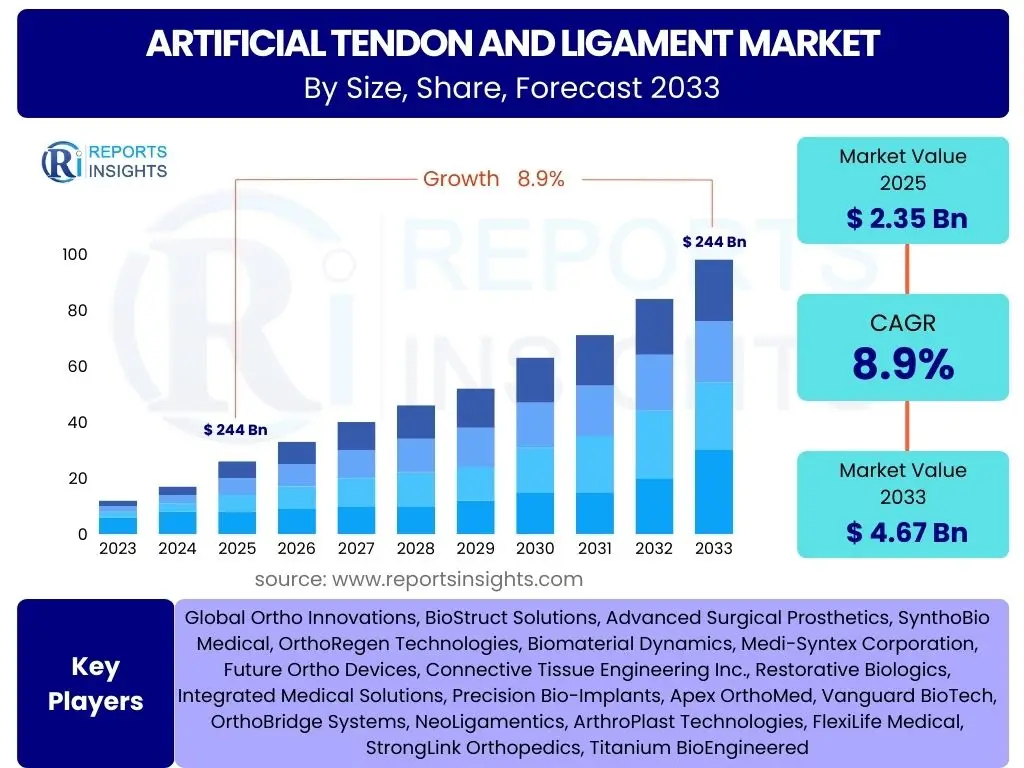

Artificial Tendon and Ligament Market Size

According to Reports Insights Consulting Pvt Ltd, The Artificial Tendon and Ligament Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 2.35 Billion in 2025 and is projected to reach USD 4.67 Billion by the end of the forecast period in 2033.

Key Artificial Tendon and Ligament Market Trends & Insights

The Artificial Tendon and Ligament market is experiencing dynamic shifts driven by advancements in biomaterials, surgical techniques, and a rising global incidence of musculoskeletal injuries. Key insights reveal a growing demand for durable, biocompatible, and functionally superior synthetic implants, often spurred by an aging population and increased participation in sports activities. There is a discernible trend towards minimally invasive surgical procedures that utilize these artificial solutions, aiming for reduced patient recovery times and improved post-operative outcomes. Furthermore, the convergence of material science with biological engineering is paving the way for next-generation products that offer enhanced integration with native tissues.

- Advancements in biomaterials, including novel polymers and composite structures, leading to more durable and biocompatible implants.

- Increasing adoption of minimally invasive surgical techniques for implant placement, reducing recovery times and patient discomfort.

- Growing prevalence of sports-related injuries and degenerative joint diseases, driving demand for reconstructive solutions.

- Shift towards personalized medicine and patient-specific implants, leveraging advanced manufacturing techniques like 3D printing.

- Integration of smart technologies, such as sensors in implants, for real-time monitoring of performance and healing.

- Emergence of bio-integrative and regenerative scaffolds designed to promote natural tissue regrowth and long-term stability.

AI Impact Analysis on Artificial Tendon and Ligament

Artificial Intelligence (AI) is poised to significantly transform the Artificial Tendon and Ligament market by revolutionizing various stages from design and manufacturing to patient care. Users are keen to understand how AI can optimize material selection, predict implant performance, and personalize surgical plans. The expectation is that AI will enhance the precision of implant design, leading to better patient-specific outcomes and reduced failure rates. Concerns often revolve around data privacy, regulatory complexities in validating AI-driven medical devices, and the need for robust clinical evidence to support AI's utility in this sensitive medical field. Despite these challenges, the potential for AI to accelerate research, improve diagnostics, and streamline treatment pathways is widely acknowledged.

- AI-driven material discovery and optimization: Accelerates the identification and development of novel biomaterials with superior properties for artificial tendons and ligaments.

- Personalized implant design: AI algorithms analyze patient-specific anatomical data and biomechanical loads to create custom implants, improving fit and function.

- Predictive analytics for surgical outcomes: AI can forecast patient recovery times and potential complications based on pre-operative data, aiding surgical planning.

- Robotic-assisted surgery integration: AI enhances the precision and autonomy of robotic systems used for implant placement, potentially reducing human error.

- Image analysis for diagnosis and monitoring: AI improves the accuracy of MRI/CT scans in diagnosing tendon/ligament injuries and post-operative implant monitoring.

- Supply chain optimization: AI can predict demand and optimize inventory for implant manufacturers, ensuring timely availability.

Key Takeaways Artificial Tendon and Ligament Market Size & Forecast

The Artificial Tendon and Ligament market is on a robust growth trajectory, primarily fueled by an escalating global burden of orthopedic injuries and an aging population requiring advanced surgical interventions. The projected significant increase in market value underscores the expanding adoption of synthetic and bio-engineered solutions as viable alternatives to traditional grafting methods. This growth is intrinsically linked to ongoing technological advancements in biomaterials and surgical techniques, which are enhancing implant durability, biocompatibility, and overall patient outcomes. The forecast indicates sustained innovation and a broadening application scope, solidifying the market's position as a critical component of orthopedic healthcare.

- Significant market expansion anticipated, driven by increasing incidence of musculoskeletal injuries and an aging demographic.

- Technological advancements in biomaterials and surgical methods are pivotal drivers of market growth and product efficacy.

- Growing preference for artificial solutions due to advantages such as reduced donor site morbidity and consistent mechanical properties.

- Emerging economies present substantial growth opportunities due to improving healthcare infrastructure and rising disposable incomes.

- The market is poised for continued innovation, focusing on bio-integration and long-term functional stability of implants.

Artificial Tendon and Ligament Market Drivers Analysis

The increasing global prevalence of orthopedic injuries, including sports-related trauma and degenerative conditions, stands as a primary driver for the Artificial Tendon and Ligament market. As participation in sports and recreational activities continues to rise across all age groups, so does the incidence of ligament and tendon ruptures, creating a consistent demand for effective repair and reconstruction solutions. Similarly, an aging global population is increasingly susceptible to age-related degeneration of connective tissues, contributing to the need for durable and functional artificial alternatives when natural tissues are compromised or insufficient for repair.

Technological advancements in biomaterials and surgical techniques significantly propel market growth. The development of new polymers, composites, and bio-integrative materials offers enhanced mechanical strength, biocompatibility, and long-term durability, making artificial implants a more attractive option. Innovations in minimally invasive surgical procedures also facilitate faster patient recovery, reduce post-operative complications, and improve overall patient satisfaction, thereby increasing the acceptance and adoption of these advanced medical devices. These material and procedural improvements directly translate into improved functional outcomes for patients.

Furthermore, rising awareness among patients and healthcare professionals regarding the benefits of artificial tendons and ligaments over traditional autograft or allograft procedures is boosting market demand. Artificial implants eliminate donor site morbidity, reduce the risk of disease transmission, and offer consistent mechanical properties, which are often unpredictable with biological grafts. The growing healthcare expenditure, particularly in developed regions, supports the adoption of high-cost, high-value medical technologies, further contributing to the expansion of this specialized market segment.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Incidence of Orthopedic Injuries | +1.2% | Global, particularly North America, Europe, APAC | 2025-2033 (Long-term) |

| Aging Population & Degenerative Conditions | +0.9% | North America, Europe, East Asia | 2025-2033 (Long-term) |

| Advancements in Biomaterials & Surgical Techniques | +1.5% | Global, Led by Developed Economies | 2025-2030 (Medium-term) |

| Growing Awareness and Preference for Artificial Solutions | +0.8% | Developed & Emerging Markets | 2028-2033 (Medium-to-Long-term) |

Artificial Tendon and Ligament Market Restraints Analysis

The high cost associated with artificial tendon and ligament procedures poses a significant restraint on market growth, particularly in developing economies or healthcare systems with limited reimbursement policies. The advanced materials, sophisticated manufacturing processes, and specialized surgical expertise required for these implants contribute to their premium pricing. This economic barrier can limit patient access, especially for those without comprehensive insurance coverage, and may lead healthcare providers to opt for less expensive, traditional treatment alternatives, even if they are less ideal in certain clinical scenarios. Consequently, cost-effectiveness remains a critical consideration influencing market adoption.

Stringent regulatory approval processes represent another considerable hurdle for market expansion. Medical devices, especially implants designed for long-term integration within the human body, undergo rigorous testing and clinical trials to ensure their safety and efficacy. These extensive regulatory pathways, which vary significantly across different countries and regions, can be time-consuming and expensive for manufacturers. Delays in obtaining approvals can defer product launches, limit market entry for new innovations, and add to the overall development cost, thus slowing down the pace of market penetration and technological dissemination.

Furthermore, concerns regarding potential complications and the lack of extensive long-term clinical data for newer artificial implants act as significant restraints. While advancements have been made, issues such as infection, implant rejection, mechanical failure, or adverse tissue reactions can still occur, impacting patient outcomes and surgeon confidence. The relatively newer nature of some advanced artificial tendon and ligament technologies means that long-term studies spanning decades, which are crucial for establishing ultimate durability and biological integration, are still ongoing or limited. This absence of comprehensive long-term evidence can create hesitation among orthopedic surgeons and patients when considering artificial solutions over more established biological grafts.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Procedures | -0.7% | Global, More Pronounced in Emerging Markets | 2025-2033 (Long-term) |

| Stringent Regulatory Approval Processes | -0.5% | North America, Europe, Key APAC Markets | 2025-2030 (Medium-term) |

| Risk of Complications & Limited Long-Term Data | -0.6% | Global | 2025-2033 (Long-term) |

| Competition from Traditional Grafting Techniques | -0.4% | Global | 2025-2030 (Short-to-Medium-term) |

Artificial Tendon and Ligament Market Opportunities Analysis

The continuous development of advanced biomaterials presents a substantial opportunity for the Artificial Tendon and Ligament market. Research is ongoing to create materials that not only mimic the biomechanical properties of natural tendons and ligaments but also promote true biological integration and cellular ingrowth. This includes bio-absorbable polymers, composite scaffolds, and smart materials that can respond to physiological cues. Such innovations promise to significantly reduce complications, enhance long-term functional stability, and open new avenues for regenerative solutions, making artificial implants an even more compelling option for orthopedic reconstruction.

Emerging markets, particularly in Asia Pacific, Latin America, and parts of the Middle East and Africa, offer significant growth opportunities. These regions are experiencing rapid improvements in healthcare infrastructure, increasing disposable incomes, and a growing awareness of advanced medical treatments. As healthcare access expands and medical tourism thrives, the demand for sophisticated orthopedic solutions, including artificial tendons and ligaments, is expected to surge. Manufacturers can leverage these burgeoning markets by developing cost-effective solutions tailored to local healthcare systems and patient needs, fostering new revenue streams and market penetration.

Furthermore, the expanding applications beyond primary reconstruction into revision surgeries and pediatric orthopedics represent a key opportunity. As the number of initial implant procedures rises, so does the need for revision surgeries due to various factors like wear-and-tear or re-injury, creating a continuous demand for advanced revision options. Additionally, specialized artificial solutions for pediatric patients, who have unique growth and development considerations, are an underdeveloped segment with high potential. Tailored products addressing these specific patient populations can unlock significant untapped market potential and improve long-term outcomes for a broader demographic.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-integrating & Regenerative Materials | +1.0% | Global | 2028-2033 (Medium-to-Long-term) |

| Expansion into Emerging Markets | +1.3% | Asia Pacific, Latin America, MEA | 2025-2033 (Long-term) |

| Growing Applications in Revision Surgeries & Pediatrics | +0.8% | Global | 2025-2033 (Long-term) |

| Personalized Medicine & 3D Printing Technologies | +0.7% | Developed Economies | 2025-2030 (Medium-term) |

Artificial Tendon and Ligament Market Challenges Impact Analysis

One significant challenge facing the Artificial Tendon and Ligament market is the inherent complexity of replicating the natural biomechanical properties of native tissues. Tendons and ligaments are highly specialized structures with anisotropic properties, varying stiffness along their length, and dynamic responses to stress and strain. Engineering artificial counterparts that precisely mimic these intricate characteristics, while also ensuring long-term durability and biocompatibility, remains a formidable technical hurdle. Achieving perfect integration with host tissues and avoiding mechanical failure over decades of use requires continuous, intensive research and development efforts.

Another critical challenge is the risk of post-operative complications, including infection, inflammation, and immunogenic reactions. While artificial implants are designed to be biocompatible, the introduction of any foreign material into the body carries an inherent risk of adverse responses. Infections at the surgical site can lead to implant failure, prolonged hospitalization, and additional surgical interventions. Similarly, chronic inflammation or adverse immune responses to implant materials can compromise integration and functionality. Mitigating these risks requires meticulous surgical techniques, advanced antimicrobial coatings, and continuous material science improvements, adding to development and procedural costs.

Furthermore, competition from established biological alternatives, such as autografts (tissue from the patient's own body) and allografts (tissue from a donor), poses a constant market challenge. While artificial implants offer advantages like eliminating donor site morbidity and ensuring consistent material properties, many surgeons still prefer biological grafts due to their proven long-term clinical track record and the perception of natural integration. Overcoming this preference requires substantial clinical evidence demonstrating superior or equivalent long-term outcomes for artificial solutions, which can be time-consuming and expensive to generate. Educating both surgeons and patients on the comparative benefits and risks of artificial options is crucial for wider adoption.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Biomechanical Replication | -0.8% | Global | 2025-2033 (Long-term) |

| Risk of Post-operative Complications (e.g., Infection) | -0.7% | Global | 2025-2030 (Medium-term) |

| Long-term Clinical Validation & Evidence Generation | -0.6% | Global | 2028-2033 (Long-term) |

| Ethical & Social Acceptance Issues for Synthetic Implants | -0.3% | Varies by Region | 2025-2030 (Short-to-Medium-term) |

Artificial Tendon and Ligament Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Artificial Tendon and Ligament market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. The scope encompasses a thorough examination of market size, growth drivers, restraints, opportunities, and challenges affecting the industry from 2019 to 2033, with a specific focus on the forecast period from 2025 to 2033. It highlights key technological advancements, their impact, and strategic recommendations for stakeholders navigating this evolving medical device sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.35 Billion |

| Market Forecast in 2033 | USD 4.67 Billion |

| Growth Rate | 8.9% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Ortho Innovations, BioStruct Solutions, Advanced Surgical Prosthetics, SynthoBio Medical, OrthoRegen Technologies, Biomaterial Dynamics, Medi-Syntex Corporation, Future Ortho Devices, Connective Tissue Engineering Inc., Restorative Biologics, Integrated Medical Solutions, Precision Bio-Implants, Apex OrthoMed, Vanguard BioTech, OrthoBridge Systems, NeoLigamentics, ArthroPlast Technologies, FlexiLife Medical, StrongLink Orthopedics, Titanium BioEngineered |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Artificial Tendon and Ligament market is comprehensively segmented to provide granular insights into its diverse components, facilitating a deeper understanding of specific product categories, material preferences, application areas, and end-user adoption patterns. This segmentation analysis helps identify high-growth sub-segments and niche markets, allowing stakeholders to tailor their strategies effectively. Each segment reflects distinct market dynamics influenced by technological maturity, clinical demand, and regional healthcare infrastructure, collectively contributing to the overall market landscape.

- By Product Type: Artificial Tendons, Artificial Ligaments

- By Material: Polymer-based (e.g., Polyester, Polyethylene Terephthalate, Polyurethane), Carbon Fiber-based, Composite Materials, Biological (e.g., Collagen, Silk-based), Hybrid Materials

- By Application: Knee Injuries (ACL, PCL, MCL, LCL reconstruction), Shoulder Injuries (Rotator Cuff repair, AC joint reconstruction), Ankle Injuries (Lateral Ligament reconstruction, Achilles Tendon repair), Hip Injuries, Other Extremities (Elbow, Wrist, Fingers)

- By End-User: Hospitals, Ambulatory Surgical Centers, Orthopedic Clinics, Specialty Surgery Centers

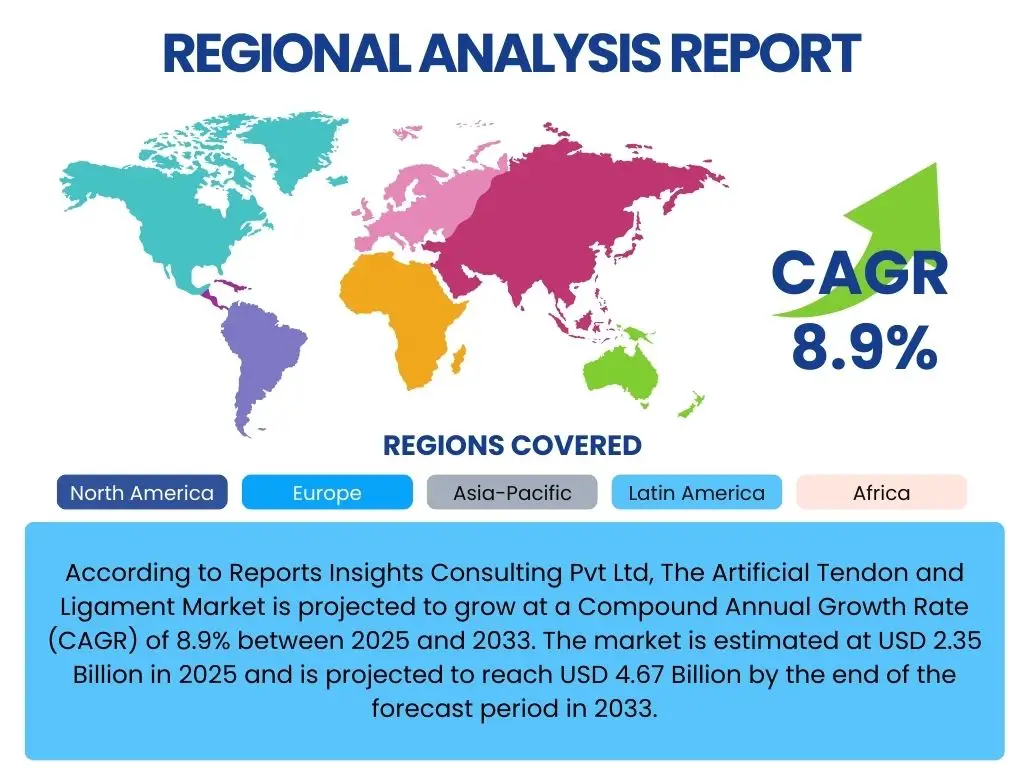

Regional Highlights

Geographic analysis reveals diverse market landscapes for artificial tendons and ligaments, primarily driven by varying healthcare expenditures, demographic trends, and adoption rates of advanced medical technologies. North America currently dominates the market, benefiting from a well-established healthcare infrastructure, high incidence of sports injuries, and a strong presence of key market players engaged in continuous innovation. The region's robust reimbursement policies and high awareness among patients and medical professionals further contribute to its leading position, particularly in the adoption of premium and cutting-edge artificial implants.

Europe represents a significant market, characterized by an aging population prone to degenerative joint conditions and a strong emphasis on minimally invasive surgical techniques. Countries like Germany, the UK, and France are at the forefront, driven by advanced medical research, a high prevalence of orthopedic ailments, and supportive government initiatives for healthcare innovation. The region's focus on quality of life and active lifestyles among its elderly population also fuels the demand for effective and long-lasting reconstructive solutions.

The Asia Pacific (APAC) region is projected to exhibit the fastest growth over the forecast period. This surge is attributed to rapidly improving healthcare infrastructure, increasing medical tourism, a large and growing patient pool, and rising disposable incomes. Countries such as China, India, Japan, and South Korea are investing heavily in healthcare, leading to greater access to advanced orthopedic procedures. The rising prevalence of sports participation and road traffic accidents in these populous nations also contributes significantly to the escalating demand for artificial tendons and ligaments, making APAC a lucrative market for future expansion. Latin America and the Middle East & Africa (MEA) are also emerging as promising regions, with improving healthcare access and growing awareness driving modest yet significant market expansion.

- North America: Dominant market share due to advanced healthcare infrastructure, high sports injury rates, and presence of major industry players. High adoption of innovative products.

- Europe: Strong market driven by an aging population, prevalence of degenerative conditions, and focus on minimally invasive surgeries. Significant research and development activities.

- Asia Pacific (APAC): Fastest growing region, fueled by improving healthcare access, increasing disposable incomes, and a large patient pool. Emerging medical tourism and rising awareness.

- Latin America: Growing market with increasing healthcare investments and improving economic conditions, leading to greater access to orthopedic treatments.

- Middle East & Africa (MEA): Developing market driven by improving healthcare infrastructure, government initiatives for health sector growth, and rising awareness about advanced medical solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Artificial Tendon and Ligament Market.- Global Ortho Innovations

- BioStruct Solutions

- Advanced Surgical Prosthetics

- SynthoBio Medical

- OrthoRegen Technologies

- Biomaterial Dynamics

- Medi-Syntex Corporation

- Future Ortho Devices

- Connective Tissue Engineering Inc.

- Restorative Biologics

- Integrated Medical Solutions

- Precision Bio-Implants

- Apex OrthoMed

- Vanguard BioTech

- OrthoBridge Systems

- NeoLigamentics

- ArthroPlast Technologies

- FlexiLife Medical

- StrongLink Orthopedics

- Titanium BioEngineered

Frequently Asked Questions

What are artificial tendons and ligaments?

Artificial tendons and ligaments are synthetic or bio-engineered implants designed to replace or augment damaged or ruptured natural connective tissues in the human body. They are primarily used in orthopedic surgeries to restore stability and function, particularly following sports injuries, trauma, or degenerative conditions when natural tissue grafts are unsuitable or unavailable.

What is the market growth forecast for artificial tendons and ligaments?

The Artificial Tendon and Ligament Market is projected for substantial growth, estimated to reach USD 4.67 Billion by 2033 from USD 2.35 Billion in 2025, demonstrating a Compound Annual Growth Rate (CAGR) of 8.9% during the forecast period. This growth is driven by increasing orthopedic injuries and technological advancements.

What are the primary applications of artificial tendons and ligaments?

The primary applications include reconstruction of knee ligaments (such as ACL, PCL, MCL, LCL), repair of shoulder injuries (like rotator cuff tears), ankle ligament reconstruction, Achilles tendon repair, and interventions for injuries in the hip, elbow, wrist, and fingers. They are crucial for restoring joint stability and mobility.

What materials are commonly used in artificial tendons and ligaments?

Commonly used materials include various polymers such as Polyester (e.g., Polyethylene Terephthalate - PET) and Polyurethane, as well as Carbon Fiber. Advanced implants also incorporate composite materials and hybrid designs that combine synthetic components with biological elements like collagen or silk-based scaffolds for enhanced bio-integration.

What are the key drivers of the artificial tendon and ligament market?

Key drivers include the rising global incidence of orthopedic injuries, an aging population more susceptible to degenerative joint conditions, significant advancements in biomaterials and surgical techniques, and growing patient and clinician awareness regarding the benefits of artificial solutions over traditional grafts.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted