Anisotropic Conductive Film Market

Anisotropic Conductive Film Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678214 | Last Updated : July 18, 2025 |

Format : ![]()

![]()

![]()

![]()

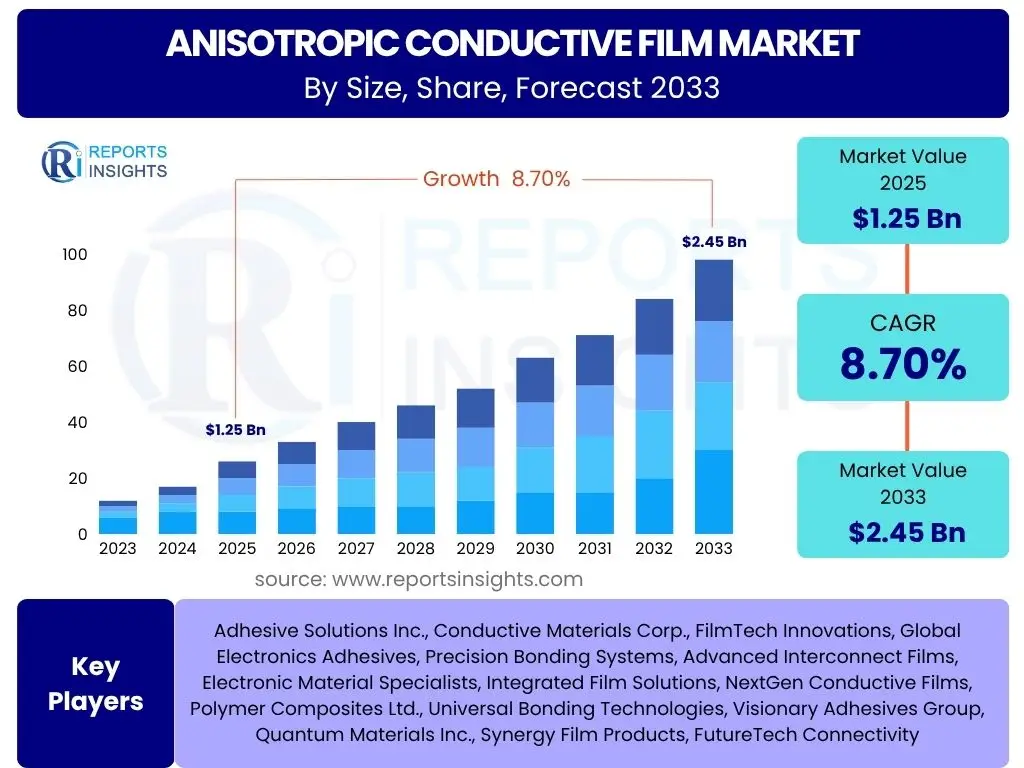

Anisotropic Conductive Film Market is projected to grow at a Compound annual growth rate (CAGR) of 8.5% between 2025 and 2033, valued at USD 450 Million in 2025 and is projected to grow to USD 862.65 Million By 2033 the end of the forecast period.

Key Anisotropic Conductive Film Market Trends & Insights

The Anisotropic Conductive Film (ACF) market is undergoing significant transformation, driven by advancements in electronic device manufacturing and the escalating demand for miniaturized and high-performance components. Key trends include the widespread adoption of flexible electronics, which leverages ACF's ability to create fine-pitch interconnections on flexible substrates without requiring high temperatures. The proliferation of advanced display technologies, such as OLED and micro-LEDs, further fuels market growth, as ACF is critical for their precise bonding requirements. Miniaturization across consumer electronics, automotive systems, and medical devices is a primary catalyst, necessitating compact and reliable interconnection solutions that ACF inherently offers. Furthermore, the push towards sustainability is influencing ACF development, with increasing research into lead-free and eco-friendly compositions, aiming to reduce environmental impact while maintaining performance.

- Miniaturization and high-density packaging in electronics.

- Increasing adoption of flexible and foldable electronic devices.

- Growth in advanced display technologies (OLED, Micro-LED).

- Rising demand from the automotive electronics sector.

- Development of lead-free and environmentally friendly ACF solutions.

- Integration into IoT and wearable technologies.

- Advances in manufacturing processes for ultra-fine pitch bonding.

AI Impact Analysis on Anisotropic Conductive Film

Artificial intelligence (AI) is set to significantly revolutionize various aspects of the Anisotropic Conductive Film (ACF) market, from research and development to manufacturing and quality control. AI's capabilities in data analysis and pattern recognition enable more efficient material discovery, allowing researchers to rapidly screen and optimize new polymer matrices, conductive particles, and adhesive formulations for enhanced performance and specific application requirements. In manufacturing, AI-powered systems can optimize production parameters, predict equipment failures, and ensure consistent quality, leading to higher yields and reduced waste. Furthermore, AI contributes to sophisticated defect detection during the bonding process, improving reliability and throughput. The integration of AI also supports predictive maintenance for bonding equipment, minimizing downtime and increasing operational efficiency across ACF applications. This technological synergy is poised to accelerate innovation and elevate the overall efficacy of ACF in advanced electronic assemblies.

- Accelerated material design and optimization for ACF formulations.

- Enhanced quality control and defect detection in ACF manufacturing.

- Optimization of bonding parameters and process control.

- Predictive maintenance for ACF bonding equipment.

- AI-driven simulation for new ACF applications and performance validation.

- Improved supply chain management through demand forecasting.

Key Takeaways Anisotropic Conductive Film Market Size & Forecast

- The Anisotropic Conductive Film (ACF) market is projected for substantial growth, driven by escalating demand for miniaturized and high-performance electronic components across diverse industries.

- The market is anticipated to exhibit a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033, indicating robust expansion over the forecast period.

- Valued at USD 450 Million in 2025, the market is poised to nearly double, reaching an estimated USD 862.65 Million by 2033, reflecting strong adoption trends.

- Growth is primarily propelled by advancements in display technology, the proliferation of flexible electronics, and increasing applications in automotive and medical sectors.

- The forecast highlights a significant opportunity for market players to capitalize on evolving technological landscapes and expanding end-use industries.

Anisotropic Conductive Film Market Drivers Impact Analysis

The Anisotropic Conductive Film (ACF) market is significantly propelled by several key drivers, each contributing to its expansion and adoption across various industries. A major impetus comes from the relentless trend of miniaturization and high-density packaging in electronic devices. As consumer electronics become thinner, lighter, and more compact, the need for precise, fine-pitch interconnections that ACF provides becomes critical. Concurrently, the burgeoning market for flexible and foldable electronics, including next-generation smartphones, wearables, and displays, heavily relies on ACF's unique bonding capabilities for flexible substrates. Advances in display technologies, such as the widespread adoption of OLED and the emergence of micro-LEDs, demand ACF for their intricate bonding processes. Furthermore, the rapid growth in automotive electronics for advanced driver-assistance systems (ADAS), infotainment, and electric vehicles creates substantial demand for robust and reliable interconnection solutions, a role perfectly suited for ACF.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization in Electronic Devices | +2.5% | Global, particularly Asia Pacific (China, South Korea, Japan) | Short to Long-term |

| Growth of Flexible and Foldable Electronics | +2.0% | Asia Pacific, North America, Europe | Medium to Long-term |

| Advancements in Display Technologies (OLED, Micro-LED) | +1.8% | Asia Pacific (South Korea, China, Japan), Europe | Short to Medium-term |

| Increasing Demand in Automotive Electronics | +1.5% | North America, Europe, Asia Pacific (China, Japan) | Medium to Long-term |

| Proliferation of IoT Devices and Wearable Technology | +0.7% | Global | Medium-term |

| Strict Environmental Regulations (Lead-free Solutions) | +0.5% | Europe, North America, Asia Pacific | Short to Medium-term |

Anisotropic Conductive Film Market Restraints Impact Analysis

Despite its significant growth potential, the Anisotropic Conductive Film (ACF) market faces several restraints that could temper its expansion. One primary challenge is the relatively high manufacturing cost of ACF materials compared to traditional interconnection methods like soldering. This cost factor can be a deterrent for cost-sensitive applications or industries seeking to minimize production expenses. Furthermore, ACF connections often exhibit limited repairability once bonded, making rework and repair processes difficult and potentially leading to increased scrap rates. The performance and reliability of ACF can also be sensitive to environmental conditions, particularly high temperature and humidity, which may limit its application in extreme operating environments. The presence of alternative bonding technologies, such as wire bonding, soldering, and non-conductive adhesives, provides competition and may be preferred in certain scenarios where ACF's unique properties are not essential or its limitations are prohibitive. Intellectual property issues and patent landscapes also contribute to market complexity, potentially hindering innovation and market entry for new players.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Cost Compared to Alternatives | -1.5% | Global, particularly emerging markets | Short to Medium-term |

| Limited Repairability of ACF Bonds | -1.2% | Global, especially in high-value electronics | Short to Medium-term |

| Sensitivity to Environmental Conditions (Temperature, Humidity) | -0.8% | Specific industrial and automotive applications | Medium-term |

| Competition from Alternative Interconnection Technologies | -0.7% | Global | Short to Medium-term |

| Complexities in Process Control and Equipment Calibration | -0.5% | Global, particularly for new entrants | Short-term |

Anisotropic Conductive Film Market Opportunities Impact Analysis

The Anisotropic Conductive Film (ACF) market is ripe with opportunities that promise to accelerate its growth trajectory. The continuous innovation in consumer electronics, especially the expanding market for wearable devices and augmented reality/virtual reality (AR/VR) headsets, presents significant avenues for ACF adoption due to their intricate and compact design requirements. The ongoing global rollout of 5G technology demands high-frequency and high-speed data transmission capabilities, which ACF can facilitate in complex module integration, opening new application areas. Moreover, research and development into advanced materials for ACF, including novel conductive particles and polymer matrices, are creating opportunities for enhanced performance, reliability, and new functionalities. The expansion into untapped geographical markets, particularly in developing economies with burgeoning electronics manufacturing sectors, also represents a substantial growth opportunity. Furthermore, the increasing focus on sustainability in electronics manufacturing is driving demand for eco-friendly and lead-free ACF solutions, fostering innovation and market differentiation for companies offering such products.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Applications in Wearable and AR/VR Devices | +1.8% | Global, particularly North America, Asia Pacific | Medium to Long-term |

| Integration into 5G Module and High-Frequency Applications | +1.5% | Global, especially Asia Pacific, North America | Medium-term |

| Development of Advanced ACF Materials (e.g., Nanomaterials) | +1.2% | Global, R&D intensive regions | Long-term |

| Expansion into New Geographical Markets | +0.8% | Latin America, Middle East & Africa, emerging APAC countries | Medium to Long-term |

| Increasing Demand for Sustainable and Eco-friendly ACF | +0.7% | Europe, North America, developed Asia Pacific | Short to Medium-term |

Anisotropic Conductive Film Market Challenges Impact Analysis

The Anisotropic Conductive Film (ACF) market, while promising, contends with several significant challenges that require innovative solutions. A critical challenge involves achieving ultra-fine pitch bonding, as electronic devices continue to demand increasingly smaller and denser interconnections. This necessitates precise control over conductive particle dispersion and bonding processes, which can be technically complex and expensive to implement at mass production scales. Ensuring long-term reliability and durability of ACF bonds, especially under varying environmental stresses such as temperature cycles and humidity, remains a continuous challenge. Failures in bonds can lead to significant device malfunctions, impacting product reputation and warranty costs. Furthermore, managing the complexities of the global supply chain for raw materials, particularly for specialized conductive particles and polymer resins, poses logistical and cost challenges. The market also faces competition from well-established traditional interconnection methods, requiring ACF to consistently demonstrate superior performance, cost-effectiveness, and process advantages to gain wider adoption. Lastly, the absence of universally accepted standardization for ACF materials and bonding processes can hinder interoperability and limit broader market acceptance.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Ultra-Fine Pitch Bonding | -1.0% | Global, particularly high-tech manufacturing hubs | Short to Medium-term |

| Ensuring Long-Term Reliability and Durability | -0.9% | Global, critical for automotive and medical sectors | Medium to Long-term |

| Managing Supply Chain Complexities for Raw Materials | -0.6% | Global | Short to Medium-term |

| Competition from Traditional Interconnection Methods | -0.5% | Global | Short-term |

| Standardization and Interoperability Issues | -0.4% | Global | Medium to Long-term |

Anisotropic Conductive Film Market - Updated Report Scope

This comprehensive market research report offers a detailed and up-to-date analysis of the Anisotropic Conductive Film market, providing critical insights into its current status, growth drivers, restraints, opportunities, and future outlook. The report covers in-depth segmentation analysis across various types, applications, and end-use industries, alongside a thorough regional assessment to provide a holistic view of the market dynamics. It includes competitive landscape analysis, profiling key industry players and their strategies to help stakeholders make informed decisions. The report's robust methodology, based on extensive primary and secondary research, ensures accuracy and reliability of the forecasts, enabling businesses to identify emerging trends, investment pockets, and market-entry strategies.

| Report Attributes | Report Details |

|---|---|

| Report Name | Anisotropic Conductive Film Market |

| Market Size in 2025 | USD 450 Million |

| Market Forecast in 2033 | USD 862.65 Million |

| Growth Rate | CAGR of 8.5% from 2025 to 2033 |

| Number of Pages | 250 |

| Key Companies Covered | Hitachi Chemical, Dexerials, 3M, H&SHighTech, Btech Corp (ADA Technologies, Inc.), Tesa Tape, U-PAK |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

: Market Product Type Segmentation:-- Chip on Glass

- Chip on Flex

- Chip on Board

- Flex on Glass

- Flex on Flex

- Flex on Board

- Displays

- Automotive

- Aerospace

- Electronic Components

- Others

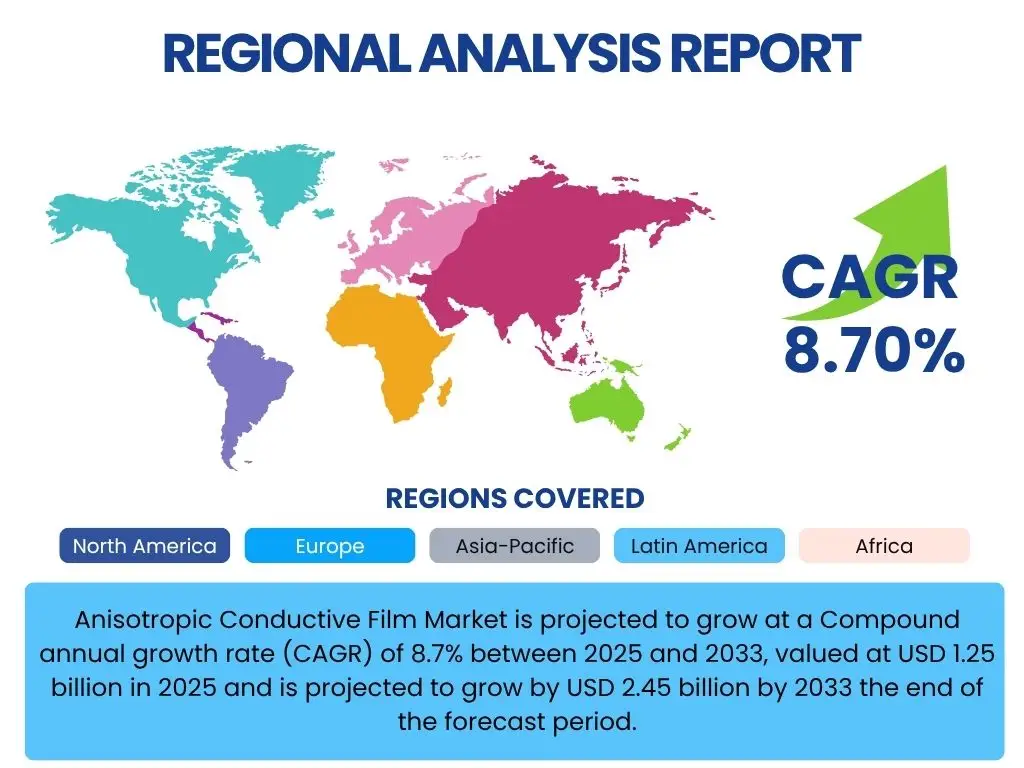

Regional Highlights

The global Anisotropic Conductive Film market demonstrates significant regional variations in growth and adoption, influenced by the presence of major electronics manufacturing hubs, technological advancements, and industrial demand. Asia Pacific stands out as the leading region, driven by countries such as China, South Korea, Japan, and Taiwan, which are at the forefront of consumer electronics manufacturing, display production (OLED, LCD), and semiconductor industries. This region's dominance is further solidified by extensive research and development activities and a vast consumer base for electronic devices, necessitating high volumes of ACF for assembly. North America and Europe represent mature markets with strong innovation ecosystems, particularly in automotive electronics, medical devices, and high-end consumer electronics. These regions focus on advanced applications and high-performance ACF solutions, driven by rigorous quality standards and a demand for sophisticated electronic assemblies. Latin America, the Middle East, and Africa are emerging markets, showing increasing potential due to growing industrialization, rising disposable incomes, and the gradual establishment of electronics manufacturing capabilities. While smaller in market share currently, these regions are anticipated to offer new growth opportunities as their technological infrastructure develops and local demand for electronic products expands.

- Asia Pacific (APAC) is the undisputed leader in the Anisotropic Conductive Film market, primarily due to the concentration of major electronics manufacturing powerhouses like China, South Korea, Japan, and Taiwan. These countries are global hubs for smartphone production, advanced display manufacturing (OLED, LCD), and semiconductor fabrication, all of which are intensive users of ACF for fine-pitch interconnections. The region benefits from a robust supply chain, significant investments in R&D, and a massive consumer market.

- North America exhibits substantial growth, driven by its strong presence in advanced electronics, including automotive (ADAS, EV components), aerospace, medical devices, and high-value consumer electronics. The region is characterized by significant R&D spending and a demand for high-reliability ACF solutions, particularly in defense and specialized industrial applications.

- Europe demonstrates steady growth, propelled by its advanced automotive industry, industrial automation, and a strong focus on innovation in electronic components. Countries like Germany and France are key contributors, emphasizing precision engineering and high-quality electronic assemblies. Environmental regulations also drive demand for lead-free ACF solutions in this region.

- Latin America and the Middle East & Africa (MEA) are emerging markets for ACF, spurred by increasing urbanization, rising consumer electronics adoption, and gradual development of local manufacturing capabilities. While currently smaller, these regions represent future growth avenues as their industrial and technological infrastructures mature.

Top Key Players:

The market research report covers the analysis of key stake holders of the Anisotropic Conductive Film Market. Some of the leading players profiled in the report include -:- Hitachi Chemical

- Dexerials

- 3M

- H&SHighTech

- Btech Corp (ADA Technologies, Inc.)

- Tesa Tape

- U-PAK

Frequently Asked Questions:

What is Anisotropic Conductive Film (ACF)?

Response: Anisotropic Conductive Film (ACF) is an adhesive material containing conductive particles that selectively conduct electricity in one direction (Z-axis) while providing electrical insulation in the plane (X-Y axis). It is primarily used for fine-pitch electrical interconnections and mechanical bonding of electronic components.

What are the primary applications of ACF?

Response: ACF is widely used in connecting display drivers to LCD or OLED panels (Chip on Glass/Flex), bonding flexible printed circuits (FPCs) to rigid boards, and in various applications requiring fine-pitch interconnections in consumer electronics, automotive displays, and medical devices.

How does Anisotropic Conductive Film work?

Response: When heat and pressure are applied during bonding, the conductive particles within the ACF are compressed between the mating electrodes of the components. This creates electrical conductivity along the Z-axis, while the surrounding polymer matrix maintains insulation in the X-Y plane, preventing short circuits.

What are the advantages of using Anisotropic Conductive Film?

Response: Key advantages of ACF include its ability to achieve fine-pitch interconnections, provide both electrical conductivity and mechanical adhesion, offer lead-free bonding solutions, and eliminate the need for solder, thus simplifying manufacturing processes and enabling miniaturization in electronic devices.

What is the future outlook for the Anisotropic Conductive Film market?

Response: The future outlook for the ACF market is highly positive, driven by the increasing demand for flexible electronics, advanced displays (OLED, Micro-LED), automotive electronics, and IoT devices. Continuous advancements in materials science and manufacturing processes are expected to further expand its applications and market growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted