Aluminum Fluoride Market

Aluminum Fluoride Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708952 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Aluminum Fluoride Market Size

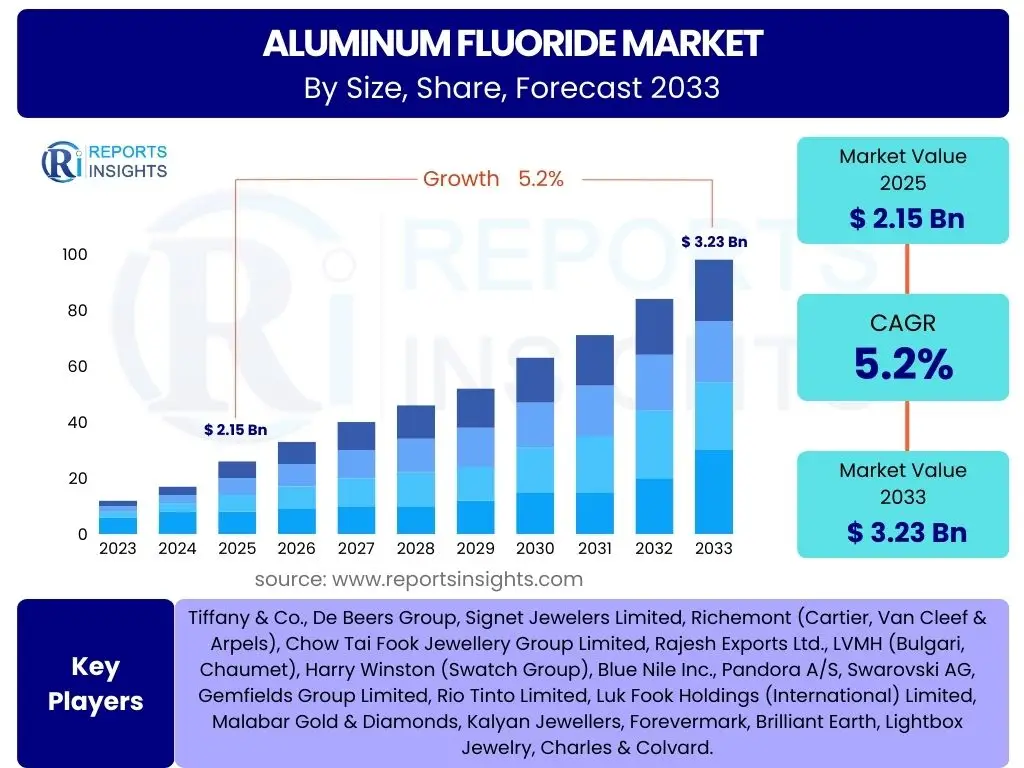

According to Reports Insights Consulting Pvt Ltd, The Aluminum Fluoride Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.2% between 2025 and 2033. The market is estimated at USD 2.15 Billion in 2025 and is projected to reach USD 3.23 Billion by the end of the forecast period in 2033.

Key Aluminum Fluoride Market Trends & Insights

The Aluminum Fluoride market is currently shaped by several dynamic trends reflecting global industrial shifts and technological advancements. A primary driving force is the consistent growth in primary aluminum production, particularly evident in emerging economies and sectors demanding lightweight materials. This sustained demand for aluminum, crucial for sectors like automotive, aerospace, and construction, directly underpins the need for aluminum fluoride as an essential electrolyte additive in the Hall-Héroult smelting process.

Beyond traditional applications, there is an increasing emphasis on process efficiency and environmental sustainability within the aluminum industry. This includes research into more energy-efficient smelting technologies and a growing interest in recycling and circular economy principles, which indirectly influences the demand dynamics and purity requirements for aluminum fluoride. Furthermore, regional shifts in industrial capacity and the ongoing development of specialized applications in ceramics and glass are contributing to new market opportunities and competitive landscapes.

- Persistent demand from the global primary aluminum smelting industry.

- Growing focus on energy efficiency and reducing carbon footprint in aluminum production.

- Emergence of advanced manufacturing techniques for high-purity aluminum fluoride.

- Increasing application in specialized fields such as ceramics, optical fibers, and battery components.

- Regional shifts in aluminum production capacity, particularly towards Asia-Pacific.

AI Impact Analysis on Aluminum Fluoride

The integration of Artificial Intelligence (AI) across various industrial sectors is increasingly influencing the Aluminum Fluoride market, primarily through optimizing production processes and enhancing supply chain management. Users often inquire about how AI can lead to more efficient chemical synthesis, better quality control, and predictive maintenance for complex manufacturing equipment. AI-driven solutions are being explored to minimize energy consumption during aluminum fluoride production and to improve the purity and consistency of the final product, addressing critical user concerns about operational costs and product quality.

Furthermore, AI plays a pivotal role in demand forecasting and supply chain optimization, helping manufacturers anticipate market fluctuations and manage raw material procurement more effectively. This addresses user expectations regarding supply chain resilience and cost management, especially given the volatility of raw material prices like fluorospar. AI also offers significant potential in accelerating research and development for new applications or improved production methods, fostering innovation within the industry and potentially leading to novel uses for aluminum fluoride in advanced materials.

- Process Optimization: AI algorithms can analyze real-time data from production facilities to optimize reaction conditions, energy consumption, and yield rates in aluminum fluoride manufacturing.

- Predictive Maintenance: AI-powered systems can forecast equipment failures in smelting plants and fluoride production facilities, minimizing downtime and maintenance costs.

- Quality Control: AI vision systems and data analytics can ensure higher purity and consistency of aluminum fluoride products by detecting anomalies early in the production cycle.

- Supply Chain Management: AI enhances demand forecasting, logistics, and raw material procurement, leading to more resilient and cost-effective supply chains for aluminum fluoride.

- Research and Development: AI can accelerate the discovery of new catalysts or production pathways, and identify novel applications for aluminum fluoride in advanced materials.

Key Takeaways Aluminum Fluoride Market Size & Forecast

Understanding the core insights from the Aluminum Fluoride market size and forecast helps stakeholders make informed strategic decisions. A significant takeaway is the market's stable growth trajectory, primarily fueled by the indispensable role of aluminum fluoride in primary aluminum production. The projected Compound Annual Growth Rate (CAGR) indicates a consistent expansion, reassuring investors and manufacturers about long-term demand. Users frequently seek reassurance regarding the market's stability and the factors underpinning its future expansion, particularly in the context of global economic shifts.

Another crucial insight is the impact of regional industrialization, especially in Asia-Pacific, which continues to be a major consumption hub for aluminum and, consequently, aluminum fluoride. The forecast highlights the importance of strategic regional investments and localized supply chain developments. The market's resilience, even amidst raw material price fluctuations and environmental scrutiny, underscores its foundational importance to the global aluminum industry, suggesting that innovation in sustainable production and application efficiency will be key differentiators moving forward.

- The market is poised for steady growth driven by the foundational demand from the primary aluminum industry.

- Asia-Pacific remains the leading consumption region, offering significant expansion opportunities.

- Technological advancements in aluminum smelting and fluoride production will enhance efficiency and drive market value.

- Sustainability initiatives and raw material sourcing stability are becoming critical factors influencing market dynamics.

- The indispensable nature of aluminum fluoride in aluminum production ensures consistent demand throughout the forecast period.

Aluminum Fluoride Market Drivers Analysis

The growth of the Aluminum Fluoride market is intrinsically linked to the expansion and technological evolution of the global aluminum industry. A primary driver is the increasing demand for primary aluminum, fueled by its widespread use in lightweight applications across the automotive, aerospace, and construction sectors. As governments and industries push for fuel efficiency and reduced emissions, the adoption of aluminum for structural components continues to rise, directly increasing the need for aluminum fluoride as a critical electrolyte component in its production.

Furthermore, ongoing industrialization and urbanization in emerging economies, particularly in Asia-Pacific, are leading to substantial investments in infrastructure and manufacturing, thereby boosting aluminum consumption. This regional growth significantly contributes to the overall demand for aluminum fluoride. Additionally, technological advancements in aluminum smelting processes aimed at improving energy efficiency and reducing operational costs also implicitly drive demand for high-quality aluminum fluoride, as process optimization often relies on precise chemical inputs.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Primary Aluminum Production | +1.8% | Asia Pacific, North America, Europe | Long-term (5-8 years) |

| Increasing Demand for Lightweight Materials (Automotive, Aerospace) | +1.5% | Global, particularly developed economies | Mid-term (3-5 years) |

| Industrialization and Urbanization in Emerging Economies | +1.2% | China, India, Southeast Asia | Long-term (5-8 years) |

| Technological Advancements in Aluminum Smelting Efficiency | +0.7% | Global | Mid-term (3-5 years) |

Aluminum Fluoride Market Restraints Analysis

Despite its critical role, the Aluminum Fluoride market faces several significant restraints that can impede its growth trajectory. One of the most prominent challenges is the volatility and scarcity of raw materials, specifically fluorospar. Fluctuations in the price and availability of fluorospar, largely sourced from a limited number of regions, can directly impact production costs and the overall stability of the supply chain for aluminum fluoride manufacturers. This creates uncertainty and can compress profit margins for producers, addressing user concerns about supply chain resilience.

Stringent environmental regulations governing the production and handling of fluorides also pose a considerable restraint. Compliance with strict emission standards, waste disposal protocols, and safety measures often necessitates significant capital investment in advanced pollution control technologies and operational adjustments, leading to increased production costs. Furthermore, the high energy consumption associated with both aluminum fluoride production and the subsequent aluminum smelting process creates cost pressures and environmental scrutiny, acting as a brake on market expansion, especially in regions with high energy prices or strict carbon emission targets.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility and Scarcity of Raw Materials (Fluorospar) | -1.3% | Global, particularly China, Mexico, South Africa | Short-term (1-3 years) |

| Stringent Environmental Regulations and Compliance Costs | -1.0% | Europe, North America, specific regions in Asia | Mid-term (3-5 years) |

| High Energy Consumption in Production and Smelting | -0.8% | Global, especially energy-intensive regions | Mid-term (3-5 years) |

| Intense Competition and Price Pressure | -0.5% | Global | Short-term (1-3 years) |

Aluminum Fluoride Market Opportunities Analysis

Despite the challenges, the Aluminum Fluoride market presents several compelling opportunities for growth and innovation. A significant opportunity lies in the burgeoning trend of aluminum recycling and the circular economy. As the global focus shifts towards sustainability, the demand for recycled aluminum is increasing, which, while reducing the need for primary aluminum, simultaneously creates demand for high-purity and specialized aluminum fluoride to ensure the quality of recycled metal alloys. This offers new avenues for product development and market penetration for manufacturers.

Furthermore, advancements in production technologies aimed at enhancing efficiency and reducing the environmental footprint of aluminum fluoride manufacturing itself represent a substantial opportunity. Innovations in synthesis methods, energy recovery, and waste treatment can lower operational costs and improve market competitiveness. The exploration of new and niche applications beyond traditional aluminum smelting, such as in advanced battery technologies, specialized ceramics, and optical materials, also provides diversification opportunities, allowing market players to tap into high-value segments and mitigate reliance on a single end-use industry. Expansion into underserved or rapidly developing regional markets, particularly in parts of Asia, Africa, and Latin America with growing industrial bases, also presents fertile ground for market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Aluminum Recycling and Circular Economy | +1.1% | Europe, North America, Japan | Mid-term (3-5 years) |

| Technological Innovations in Production (e.g., lower energy processes) | +0.9% | Global | Long-term (5-8 years) |

| Emergence of New Niche Applications (e.g., Batteries, Advanced Ceramics) | +0.8% | Global | Long-term (5-8 years) |

| Expansion into Underserved Emerging Markets | +0.6% | Southeast Asia, Latin America, Africa | Mid-term (3-5 years) |

Aluminum Fluoride Market Challenges Impact Analysis

The Aluminum Fluoride market faces several significant challenges that can hinder its progress and profitability. A major hurdle is the potential for supply chain disruptions, which can stem from geopolitical tensions, natural disasters, or trade restrictions affecting the movement of raw materials like fluorospar or the final product. Such disruptions can lead to price volatility, increased lead times, and an inability to meet demand, directly impacting manufacturers' operational stability and profitability. Users are particularly concerned about the resilience of global supply chains in a volatile economic environment.

Another critical challenge is the escalating cost of environmental compliance and the increasing scrutiny of industrial emissions. As regulations become more stringent globally, companies are required to invest heavily in advanced pollution control technologies and sustainable practices, which adds to the operational expenditure. Furthermore, the inherent energy intensity of aluminum fluoride production and its primary end-use in aluminum smelting poses an ongoing challenge, particularly with rising global energy prices and the urgent need for decarbonization. This pressure necessitates continuous innovation in energy-efficient production methods, which can be capital-intensive and time-consuming.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions and Geopolitical Risks | -1.1% | Global, particularly major trade routes | Short-term (1-3 years) |

| Rising Environmental Compliance Costs and Emission Standards | -0.9% | Europe, North America, China | Mid-term (3-5 years) |

| Volatile Energy Prices and Decarbonization Pressures | -0.7% | Global | Mid-term (3-5 years) |

| Availability of Skilled Labor for Specialized Chemical Production | -0.4% | Global, specialized industrial hubs | Long-term (5-8 years) |

Aluminum Fluoride Market - Updated Report Scope

This report provides a comprehensive analysis of the global Aluminum Fluoride market, covering historical trends, current market dynamics, and future projections. It delves into various market segments, including different product types and diverse application areas, offering an in-depth understanding of the market's structure and growth potential. The scope also includes a detailed regional analysis, identifying key growth pockets and competitive landscapes, along with profiles of leading market participants to provide a holistic view of the industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.15 Billion |

| Market Forecast in 2033 | USD 3.23 Billion |

| Growth Rate | 5.2% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Solvay S.A., Honjo Chemical Co. Ltd., Fluorsid S.p.A., Derivados del Flúor, Ltd., Xingfu Chemical, Gulf Fluor, Aluminium Bahrain B.S.C. (ALBA), Merck KGaA, Avantor, Inc., Stella Chemifa Corporation, JSPL (Jindal Steel & Power Ltd.), China National BlueStar (Group) Co, Ltd., RUSAL, Nippon Light Metal Co. Ltd., Shandong Dongyue Chemical Co. Ltd., Tanfac Industries Ltd., Henan Prosper Chemical Co. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Aluminum Fluoride market is comprehensively segmented to provide granular insights into its various facets, enabling a detailed understanding of demand and supply dynamics across different product forms and end-use industries. The primary segmentation by type distinguishes between dry and wet aluminum fluoride, each catering to specific industrial requirements in terms of purity, handling, and application methodology. Dry aluminum fluoride, often preferred for its higher purity and easier handling, typically finds extensive use in the primary aluminum smelting process, while wet forms might be utilized in specific chemical processes or intermediate applications where solution form is beneficial.

Further segmentation by application highlights the diverse end-use sectors driving the market. The aluminum smelting industry remains the dominant consumer due to aluminum fluoride's critical role as an electrolyte component. However, other industrial applications such as in ceramics, where it acts as a flux or opacifying agent, and in glass manufacturing, for enhancing optical properties, are also significant and represent growing niche markets. This detailed segmentation allows for a precise evaluation of market size, growth rates, and future potential within each category, offering a clear roadmap for strategic planning and investment decisions across the value chain.

- By Type:

- Dry Aluminum Fluoride

- Wet Aluminum Fluoride

- By Application:

- Aluminum Smelting

- Ceramics

- Glass

- Other Industrial Applications (e.g., optical fibers, specialized alloys, catalyst production)

- By Region:

- North America

- Europe

- Asia Pacific (APAC)

- Latin America

- Middle East & Africa (MEA)

Regional Highlights

- Asia Pacific (APAC): Dominates the global Aluminum Fluoride market, primarily driven by the colossal primary aluminum production capacity in countries like China and India. Rapid industrialization, urbanization, and infrastructure development across Southeast Asia further fuel the demand. The region is also witnessing significant investments in new smelting facilities and an increasing adoption of lightweight materials in automotive and construction sectors.

- Europe: A mature market characterized by stringent environmental regulations and a strong focus on sustainable production practices. Demand is stable, supported by established aluminum industries, but growth is tempered by capacity limitations and high energy costs. Innovation in eco-friendly production methods and high-purity aluminum fluoride for specialized applications are key regional trends.

- North America: Exhibits steady demand driven by the automotive, aerospace, and packaging industries. The region focuses on advanced manufacturing processes and efficiency improvements in aluminum production. Strategic investments in recycling infrastructure and a shift towards domestic sourcing of critical materials are shaping the market.

- Middle East & Africa (MEA): Emerging as a significant hub for primary aluminum production due to abundant and affordable energy resources (natural gas). Countries like Bahrain, UAE, and Saudi Arabia are home to large-scale smelters, leading to substantial demand for aluminum fluoride. The region is attracting foreign investments and is poised for considerable growth in the forecast period.

- Latin America: Presents moderate growth opportunities, primarily influenced by the region's raw material availability and developing industrial base. Countries such as Brazil and Argentina contribute to both aluminum production and consumption, with potential for further expansion in the long term, contingent on economic stability and industrial investment.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aluminum Fluoride Market.- Solvay S.A.

- Honjo Chemical Co. Ltd.

- Fluorsid S.p.A.

- Derivados del Flúor, Ltd.

- Xingfu Chemical

- Gulf Fluor

- Aluminium Bahrain B.S.C. (ALBA)

- Merck KGaA

- Avantor, Inc.

- Stella Chemifa Corporation

- JSPL (Jindal Steel & Power Ltd.)

- China National BlueStar (Group) Co, Ltd.

- RUSAL

- Nippon Light Metal Co. Ltd.

- Shandong Dongyue Chemical Co. Ltd.

- Tanfac Industries Ltd.

- Henan Prosper Chemical Co. Ltd.

Frequently Asked Questions

What is aluminum fluoride primarily used for?

Aluminum fluoride is primarily used as an essential additive in the electrolyte bath for the production of primary aluminum through the Hall-Héroult smelting process. It helps lower the melting point of alumina and increases the electrical conductivity of the electrolyte.

What are the key drivers for the Aluminum Fluoride market's growth?

The key drivers include the growing global demand for primary aluminum, increasing use of lightweight materials in industries like automotive and aerospace, and rapid industrialization in emerging economies, particularly in Asia-Pacific.

Which region dominates the Aluminum Fluoride market?

The Asia Pacific region, led by countries such as China and India, currently dominates the global Aluminum Fluoride market due to its extensive primary aluminum production capacities and ongoing industrial expansion.

What challenges does the Aluminum Fluoride market face?

Major challenges include the volatility and scarcity of raw materials like fluorospar, stringent environmental regulations impacting production costs, high energy consumption in manufacturing, and potential disruptions in global supply chains.

How does AI impact the Aluminum Fluoride industry?

AI significantly impacts the industry by optimizing production processes for higher efficiency and lower energy consumption, enhancing quality control, enabling predictive maintenance for equipment, and improving supply chain management and demand forecasting.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted