Aluminium Scandium Market

Aluminium Scandium Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705233 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

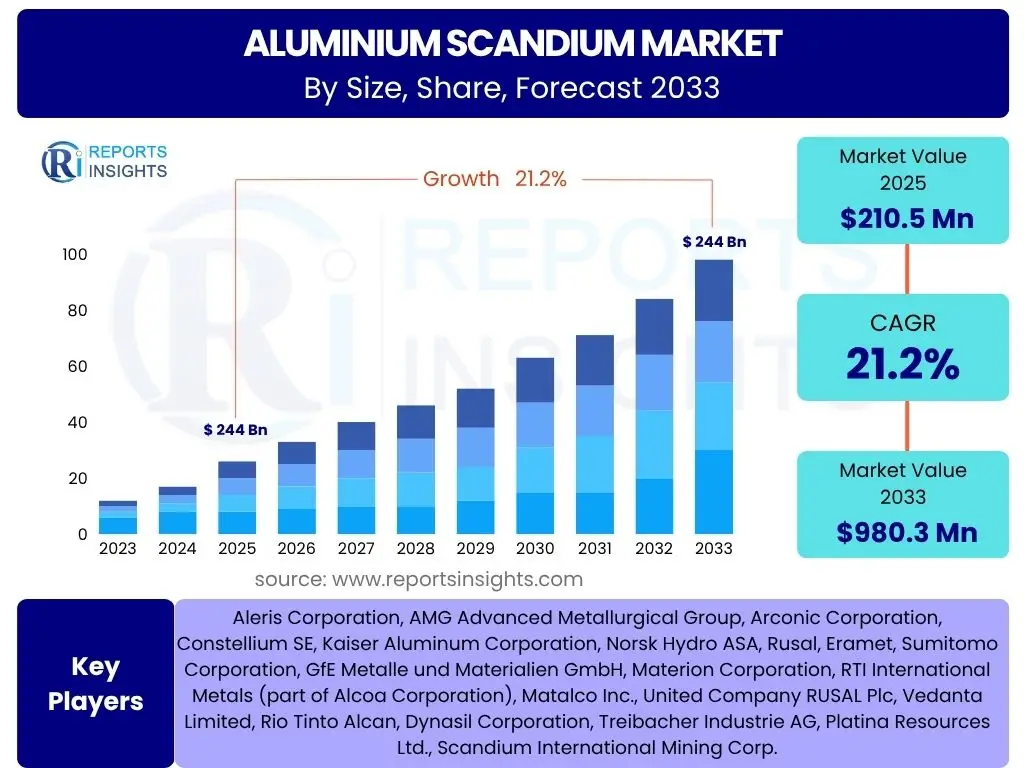

Aluminium Scandium Market Size

According to Reports Insights Consulting Pvt Ltd, The Aluminium Scandium Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.2% between 2025 and 2033. The market is estimated at USD 210.5 Million in 2025 and is projected to reach USD 980.3 Million by the end of the forecast period in 2033.

The substantial growth trajectory is underpinned by the increasing demand for high-performance, lightweight materials across several advanced industries. Aluminium Scandium alloys offer superior strength-to-weight ratio, enhanced weldability, and improved corrosion resistance compared to conventional aluminium alloys, making them highly desirable for critical applications. The market's expansion is particularly fueled by ongoing innovations in material science and engineering, alongside a broader industry push towards efficiency and sustainability.

Key Aluminium Scandium Market Trends & Insights

Users frequently inquire about the evolving landscape of the Aluminium Scandium market, seeking insights into the dominant trends shaping its future. Common questions revolve around the adoption rates in aerospace, the emergence of new application areas, and the impact of manufacturing advancements. The market is increasingly characterized by a strong emphasis on lightweighting initiatives across diverse sectors, driven by fuel efficiency targets in transportation and performance optimization in defense and sports equipment. Furthermore, advancements in alloy manufacturing techniques and the exploration of more sustainable scandium sourcing are pivotal trends influencing market dynamics and accessibility.

- Growing adoption in aerospace and defense sectors for structural components due to exceptional strength-to-weight ratio.

- Increasing integration into high-performance sports equipment, including cycling, baseball bats, and lacrosse sticks, for improved durability and reduced weight.

- Emergence of Aluminium Scandium alloys in the automotive industry, particularly for electric vehicle (EV) chassis and battery casings, to enhance range and performance.

- Advancements in additive manufacturing (3D printing) technologies are enabling the creation of complex geometries with Aluminium Scandium alloys, expanding design possibilities.

- Intensified research and development efforts aimed at reducing scandium extraction costs and improving alloy fabrication processes to enhance market viability.

- Rising focus on circular economy principles, leading to initiatives for recycling Aluminium Scandium alloys and exploring alternative, sustainable scandium sources.

AI Impact Analysis on Aluminium Scandium

User inquiries concerning the impact of Artificial Intelligence (AI) on the Aluminium Scandium market often focus on its potential to accelerate material discovery, optimize production processes, and enhance supply chain efficiency. There is significant interest in how AI can overcome current challenges such as high production costs and limited scandium availability. Users anticipate that AI-driven simulations and data analytics will play a crucial role in predicting alloy properties, designing novel Aluminium Scandium compositions, and streamlining manufacturing workflows, thereby unlocking new efficiencies and applications.

AI's influence extends beyond initial research, offering transformative capabilities for quality control, predictive maintenance of manufacturing equipment, and demand forecasting within the Aluminium Scandium supply chain. By leveraging machine learning algorithms, producers can gain deeper insights into market fluctuations, optimize inventory management, and identify potential disruptions before they occur. This integration of AI is expected to significantly reduce material waste, lower operational costs, and ultimately make Aluminium Scandium alloys more competitive and accessible for a broader range of industrial applications, thereby accelerating market growth and innovation.

- Accelerated materials discovery and alloy design through AI-powered simulations and data analysis, identifying optimal Aluminium Scandium compositions.

- Optimization of manufacturing processes, including casting, welding, and heat treatment, leading to reduced production costs and improved material properties.

- Enhanced quality control and defect detection in Aluminium Scandium components using machine vision and AI algorithms, ensuring higher reliability.

- Predictive maintenance for production equipment, minimizing downtime and increasing operational efficiency in Aluminium Scandium alloy manufacturing facilities.

- Improved supply chain management and demand forecasting for scandium and Aluminium Scandium alloys, reducing volatility and ensuring material availability.

- Development of smart materials with tailored properties for specific applications through AI-driven material engineering.

Key Takeaways Aluminium Scandium Market Size & Forecast

Common questions from users regarding key takeaways from the Aluminium Scandium market size and forecast typically highlight the market's rapid growth potential, the primary drivers behind this expansion, and the long-term outlook for its adoption across various industries. Insights suggest a significant transition from niche applications to more widespread industrial use, driven by the alloys' superior performance characteristics. The market is poised for robust expansion, reflecting increasing investments in advanced materials research and development, particularly in sectors prioritizing lightweighting and high-performance capabilities.

The forecast indicates a sustained high growth rate, underscoring the alloy's critical role in future technological advancements and sustainable engineering solutions. While challenges related to cost and supply persist, ongoing innovations in extraction and processing are expected to mitigate these hurdles, further enhancing market accessibility and driving broader adoption. The strategic importance of Aluminium Scandium in defense and aerospace, coupled with its emerging utility in automotive and sports, positions it as a transformative material with considerable market momentum.

- The Aluminium Scandium market is projected for substantial growth, indicating strong confidence in its long-term potential.

- Aerospace and defense sectors remain primary demand drivers, seeking high-strength, lightweight solutions.

- Emerging applications in electric vehicles and sports equipment are diversifying the market and contributing to expansion.

- Technological advancements in production and recycling are crucial for overcoming cost and supply challenges.

- The market is transitioning from specialized, high-cost applications to more widespread industrial adoption, driven by performance benefits.

- Strategic investments in research and development are accelerating the commercial viability and accessibility of Aluminium Scandium alloys.

Aluminium Scandium Market Drivers Analysis

The Aluminium Scandium market is primarily driven by the escalating global demand for lightweight and high-strength materials, particularly within the aerospace and defense industries. These sectors continuously seek innovative solutions to reduce weight without compromising structural integrity, aiming for improved fuel efficiency, enhanced performance, and increased payload capacity. The unique properties of Aluminium Scandium alloys, such as their superior strength-to-weight ratio, excellent fatigue resistance, and improved weldability, make them ideal for these demanding applications. Furthermore, the burgeoning electric vehicle sector is increasingly exploring these alloys to extend battery range and optimize vehicle performance, adding another significant impetus to market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing demand for lightweight materials in aerospace and defense | +7.5% | North America, Europe, Asia Pacific (China, India) | 2025-2033 |

| Growing adoption in Electric Vehicles (EVs) for enhanced range and performance | +5.2% | Asia Pacific (China), Europe, North America | 2027-2033 |

| Advancements in additive manufacturing (3D printing) technologies | +4.8% | Global, particularly developed economies | 2025-2033 |

| Expansion into high-performance sports equipment | +2.1% | North America, Europe, parts of Asia Pacific | 2025-2030 |

| Technological innovations in alloy composition and processing | +1.6% | Global | 2025-2033 |

Aluminium Scandium Market Restraints Analysis

Despite its promising growth, the Aluminium Scandium market faces several significant restraints that could impede its full potential. The most prominent barrier is the high cost associated with scandium extraction and purification. Scandium is a rare earth element, and its limited availability, coupled with complex and energy-intensive extraction processes, translates into a high raw material cost, which directly impacts the overall alloy price. This elevated cost makes Aluminium Scandium alloys less competitive for widespread commercial applications where traditional aluminium alloys or other materials suffice. Furthermore, the volatility in scandium supply chains, often influenced by geopolitical factors and a limited number of primary producers, poses a risk to consistent and predictable market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High production cost of scandium and Aluminium Scandium alloys | -6.0% | Global | 2025-2033 |

| Limited global supply of scandium | -4.5% | Global, especially for new entrants | 2025-2030 |

| Competition from other high-performance lightweight materials (e.g., carbon fiber composites, titanium alloys) | -3.2% | Global | 2025-2033 |

| Complex and specialized manufacturing processes required for alloys | -2.0% | Global | 2025-2030 |

| Lack of standardized recycling infrastructure for Aluminium Scandium alloys | -1.5% | Global | 2028-2033 |

Aluminium Scandium Market Opportunities Analysis

The Aluminium Scandium market is rich with opportunities stemming from ongoing technological advancements and the increasing demand for high-performance materials in diverse sectors. A significant opportunity lies in the development of more cost-effective and environmentally friendly scandium extraction technologies. Innovations in co-production from existing mining waste or bauxite residues could substantially increase supply and lower prices, making Aluminium Scandium alloys more accessible for broader commercial applications. Furthermore, the exploration of new application areas beyond traditional aerospace and defense, such as medical implants, consumer electronics, and specialized industrial equipment, presents substantial avenues for market expansion. The growing focus on lightweighting in the general automotive sector, especially for components beyond the chassis, could also open up mass-market opportunities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technological breakthroughs in low-cost scandium extraction and purification | +6.0% | Global, particularly Australia, North America, Europe | 2026-2033 |

| Expansion into new application areas (e.g., medical, consumer electronics, specialized industrial) | +4.7% | Global | 2027-2033 |

| Development of closed-loop recycling systems for Aluminium Scandium alloys | +3.5% | Europe, North America, Asia Pacific | 2028-2033 |

| Government initiatives and funding for advanced material research and development | +2.8% | North America, Europe, China | 2025-2033 |

| Strategic partnerships and collaborations across the value chain | +1.9% | Global | 2025-2030 |

Aluminium Scandium Market Challenges Impact Analysis

The Aluminium Scandium market faces several formidable challenges that could hinder its growth and wider adoption. A significant challenge is the inherent supply chain vulnerability associated with scandium, given its limited primary sources and the geopolitical sensitivities of these regions. Any disruption in mining or processing can severely impact the availability and pricing of the raw material, creating uncertainty for manufacturers. Furthermore, scaling up production of Aluminium Scandium alloys to meet projected demand presents a substantial hurdle, as it requires significant capital investment in specialized facilities and expertise. Developing and qualifying new alloys for critical applications also involves lengthy and expensive certification processes, particularly in highly regulated industries like aerospace.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply chain vulnerability and geopolitical risks associated with scandium sources | -4.0% | Global | 2025-2033 |

| Scalability of production to meet increasing demand | -3.5% | Global | 2025-2030 |

| Long and costly qualification and certification processes for new applications | -2.8% | Global, particularly highly regulated sectors | 2025-2033 |

| Fluctuating raw material prices (scandium, aluminium) | -2.1% | Global | 2025-2033 |

| Limited awareness and technical expertise among potential end-users | -1.0% | Emerging markets, niche sectors | 2025-2030 |

Aluminium Scandium Market - Updated Report Scope

This comprehensive market research report delves into the Aluminium Scandium market, offering a detailed analysis of its current landscape, historical performance, and future projections. The report provides an in-depth examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. It incorporates a thorough assessment of industry trends, the competitive environment, and the impact of technological advancements, including Artificial Intelligence, on market dynamics. The scope is designed to provide stakeholders with actionable insights to inform strategic decision-making and investment planning within the Aluminium Scandium industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 210.5 Million |

| Market Forecast in 2033 | USD 980.3 Million |

| Growth Rate | 21.2% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Aleris Corporation, AMG Advanced Metallurgical Group, Arconic Corporation, Constellium SE, Kaiser Aluminum Corporation, Norsk Hydro ASA, Rusal, Eramet, Sumitomo Corporation, GfE Metalle und Materialien GmbH, Materion Corporation, RTI International Metals (part of Alcoa Corporation), Matalco Inc., United Company RUSAL Plc, Vedanta Limited, Rio Tinto Alcan, Dynasil Corporation, Treibacher Industrie AG, Platina Resources Ltd., Scandium International Mining Corp. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Aluminium Scandium market is comprehensively segmented to provide a granular understanding of its diverse facets and varying demand drivers. This segmentation allows for precise analysis of market performance across different applications, end-use industries, product forms, and scandium content levels. Each segment exhibits unique growth dynamics influenced by specific technological requirements, cost considerations, and regulatory landscapes. Understanding these distinct segments is crucial for identifying targeted growth strategies and investment opportunities within the broader market.

The application segment, particularly aerospace and defense, continues to dominate due to the critical need for lightweight, high-strength materials in aircraft and missile components. However, the rapidly expanding automotive sector, especially within electric vehicle manufacturing, is poised for significant growth, driven by the need to extend battery range and improve vehicle performance. Segmentation by form highlights the increasing importance of powders for additive manufacturing, reflecting a shift towards more complex and customized component production. Geographical segmentation reveals varying adoption rates and strategic priorities across key regions, influencing regional market growth trajectories.

- By Application:

- Aerospace & Defense

- Aircraft Structures

- Missile Components

- Satellite Parts

- Sports Equipment

- Baseball Bats

- Bicycle Frames

- Lacrosse Sticks

- Ski Poles

- Automotive

- Chassis Components

- Battery Housings

- Engine Parts (specialized)

- Consumer Electronics

- Mobile Device Casings

- Laptop Components

- Other Industrial Applications

- Aerospace & Defense

- By End-Use Industry:

- Aviation

- Military

- Automotive

- Sports & Recreation

- Electronics

- Industrial Manufacturing

- By Form:

- Forged Alloys

- Extruded Alloys

- Cast Alloys

- Powders (for Additive Manufacturing)

- By Scandium Content:

- Low Scandium Alloys (0.1-0.3 wt%)

- Medium Scandium Alloys (0.3-0.6 wt%)

- High Scandium Alloys (>0.6 wt%)

- By Region:

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Regional Highlights

- North America: This region is a leading market for Aluminium Scandium, primarily driven by robust demand from its advanced aerospace and defense industries. The United States, in particular, is a significant consumer due to its extensive military spending and strong innovation in aircraft manufacturing. Increasing investments in electric vehicle development and high-performance sports equipment also contribute to the region's market growth.

- Europe: Europe represents a substantial market share, fueled by its well-established automotive, aerospace, and defense sectors. Countries like France, Germany, and the UK are key contributors, focusing on sustainable lightweighting solutions and advanced material research. Regulations promoting fuel efficiency and reduced emissions further accelerate the adoption of Aluminium Scandium alloys.

- Asia Pacific (APAC): The APAC region is poised for the fastest growth, primarily driven by the rapid expansion of its automotive (especially EV), electronics, and emerging aerospace industries in countries like China, Japan, and India. Increased manufacturing capabilities, government support for advanced materials, and a growing consumer electronics market contribute significantly to the demand for Aluminium Scandium.

- Latin America: This region is an emerging market for Aluminium Scandium, with potential growth linked to expanding industrial sectors and increasing adoption of lightweight materials in niche applications. The aerospace and defense sectors, though smaller than in North America or Europe, represent a growing area of interest.

- Middle East and Africa (MEA): The MEA region is expected to witness steady growth, driven by growing investments in defense, aerospace, and infrastructure projects. The increasing focus on diversifying economies and developing local manufacturing capabilities presents opportunities for the adoption of advanced materials like Aluminium Scandium.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aluminium Scandium Market.- Aleris Corporation

- AMG Advanced Metallurgical Group

- Arconic Corporation

- Constellium SE

- Kaiser Aluminum Corporation

- Norsk Hydro ASA

- Rusal

- Eramet

- Sumitomo Corporation

- GfE Metalle und Materialien GmbH

- Materion Corporation

- RTI International Metals (part of Alcoa Corporation)

- Matalco Inc.

- United Company RUSAL Plc

- Vedanta Limited

- Rio Tinto Alcan

- Dynasil Corporation

- Treibacher Industrie AG

- Platina Resources Ltd.

- Scandium International Mining Corp.

Frequently Asked Questions

What is Aluminium Scandium alloy?

Aluminium Scandium (Al-Sc) alloy is a high-performance material combining aluminium with a small amount of scandium (typically 0.1% to 0.6% by weight). This addition significantly enhances the alloy's strength, weldability, corrosion resistance, and fatigue life while maintaining low density, making it ideal for lightweight applications.

Why is Aluminium Scandium expensive?

The high cost of Aluminium Scandium alloys primarily stems from the scarcity and complex extraction of scandium. Scandium is a rare earth element, typically produced as a byproduct of other mining operations, leading to limited supply and high purification costs. These factors contribute significantly to the overall price of the finished alloy.

What are the main applications of Aluminium Scandium alloys?

Aluminium Scandium alloys are predominantly used in high-performance applications where lightweighting and strength are critical. Key applications include aerospace and defense (aircraft structures, missile components), high-end sports equipment (bicycle frames, baseball bats), and increasingly, the automotive sector, especially for electric vehicle components.

What is the future outlook for the Aluminium Scandium market?

The future outlook for the Aluminium Scandium market is highly positive, driven by increasing demand for lightweight, high-strength materials across various industries. While cost and supply remain challenges, ongoing advancements in extraction technologies and the diversification of applications into rapidly growing sectors like electric vehicles suggest robust and sustained market expansion over the forecast period.

Who are the major producers of Aluminium Scandium alloys?

Major producers of Aluminium Scandium alloys and key players in the market include leading global aluminium and specialty metals companies. These firms are involved in various stages of the value chain, from scandium extraction and refining to the production of specialized Aluminium Scandium alloys for diverse industrial applications.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted