Alumina Market

Alumina Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701443 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

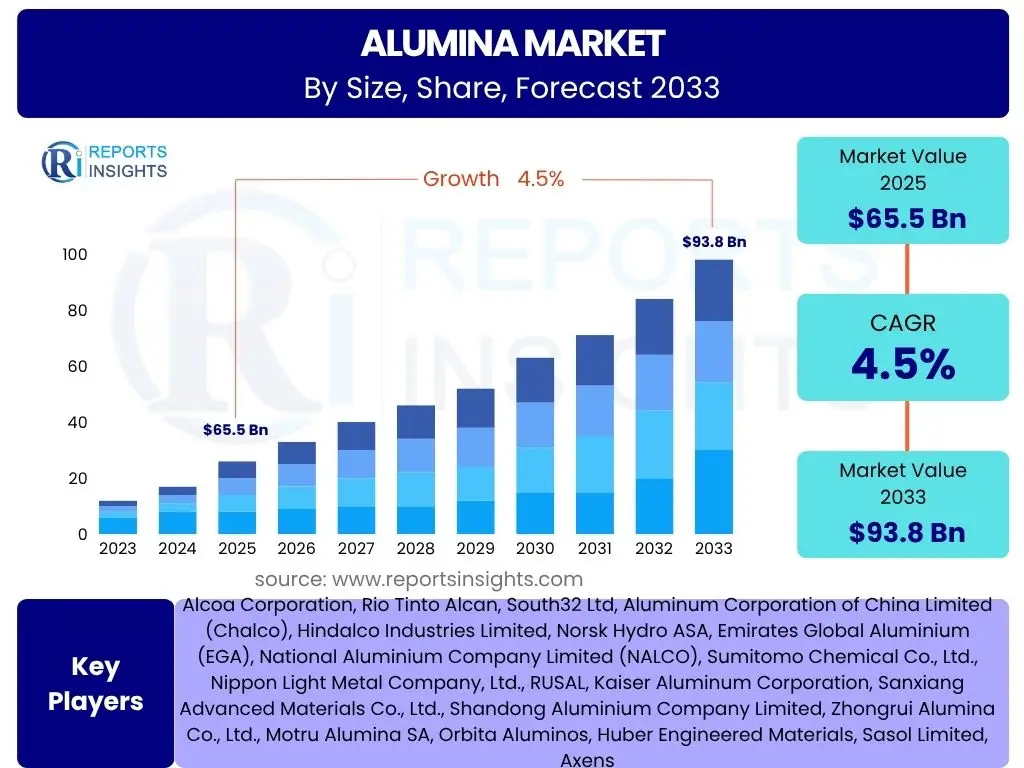

Alumina Market Size

According to Reports Insights Consulting Pvt Ltd, The Alumina Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033. The market is estimated at USD 65.5 Billion in 2025 and is projected to reach USD 93.8 Billion by the end of the forecast period in 2033.

Key Alumina Market Trends & Insights

The global alumina market is experiencing transformative shifts driven by evolving industrial demands and technological advancements. A significant trend is the increasing focus on specialty alumina products, which offer enhanced performance characteristics for advanced applications in sectors like electronics, medical devices, and high-performance ceramics. This shift is a response to the growing need for materials with superior strength, thermal stability, and electrical insulation properties, moving beyond traditional bulk applications.

Another prominent trend is the strong emphasis on sustainable production practices and circular economy principles within the alumina industry. Producers are increasingly investing in technologies that reduce energy consumption, minimize waste generation, and improve the efficiency of bauxite refining processes. The adoption of calcination technologies that require less energy, along with efforts to valorize bauxite residue (red mud) into useful by-products, reflects a broader industry commitment to environmental stewardship and resource optimization. This push for sustainability is not only driven by regulatory pressures but also by consumer and investor demand for responsibly sourced materials.

Furthermore, the market is witnessing robust growth in demand from emerging economies, particularly in the Asia Pacific region. Rapid urbanization, infrastructure development, and industrial expansion in countries like China and India are fueling the consumption of alumina in construction, automotive, and industrial applications. This regional dynamism, coupled with ongoing research and development into new applications for alumina, suggests a continued diversification of market opportunities and a sustained growth trajectory for the coming years.

- Growing demand for specialty alumina in high-tech applications.

- Increasing adoption of sustainable production methods and circular economy initiatives.

- Strong market expansion driven by industrialization and urbanization in emerging economies.

- Technological advancements in alumina processing for improved efficiency and purity.

- Diversification of alumina applications beyond traditional metallurgy, into areas like water treatment and catalysts.

AI Impact Analysis on Alumina

The integration of Artificial Intelligence (AI) and machine learning technologies is set to revolutionize various facets of the alumina production process, enhancing efficiency, optimizing resource utilization, and improving product quality. AI algorithms can analyze vast datasets from plant operations, including sensor data from crushers, mills, digesters, and kilns, to identify patterns and predict potential equipment failures, thereby enabling predictive maintenance. This shift from reactive to proactive maintenance minimizes downtime, reduces operational costs, and extends the lifespan of critical machinery, directly impacting overall plant productivity and output consistency.

Beyond maintenance, AI plays a crucial role in process optimization within alumina refineries. By continuously monitoring and analyzing parameters such as temperature, pressure, concentration, and flow rates, AI systems can dynamically adjust process settings to achieve optimal output and energy efficiency. For instance, AI can fine-tune calcination processes to ensure desired alumina purity and particle size distribution while minimizing fuel consumption. This intelligent automation leads to significant reductions in energy intensity, lower emissions, and more consistent product quality, aligning with both economic and environmental objectives of the industry.

Moreover, AI's capabilities extend to supply chain management and quality control, offering enhanced visibility and precision. AI-powered predictive analytics can forecast demand fluctuations, optimize inventory levels, and streamline logistics, reducing waste and improving responsiveness to market changes. In quality control, machine vision and AI algorithms can detect subtle defects or variations in alumina products that might be imperceptible to human inspection, ensuring high-purity standards are consistently met. While the full integration of AI is still nascent in some areas of alumina production, its potential to drive significant operational efficiencies, reduce environmental footprint, and elevate product standards is undeniable, positioning it as a key technological enabler for future growth.

- Predictive maintenance and fault detection in refining equipment, reducing downtime.

- Optimization of energy consumption in calcination and other processing stages.

- Enhanced quality control through AI-powered anomaly detection and material analysis.

- Improved supply chain visibility and demand forecasting for raw materials and finished products.

- Development of smart sensors and IoT solutions for real-time process monitoring.

Key Takeaways Alumina Market Size & Forecast

The alumina market is poised for steady expansion through 2033, driven by a confluence of traditional industrial demands and emerging high-growth applications. A primary takeaway is the resilience of demand from the metallurgical sector, particularly aluminum production, which remains the largest end-use segment. However, significant growth momentum is expected from non-metallurgical applications, including advanced ceramics, refractories, and specialty chemicals, which are progressively contributing a larger share to the market’s overall revenue and fostering innovation in product development.

Another critical insight is the increasing influence of sustainability and regulatory pressures on market dynamics. Producers are navigating stricter environmental standards, pushing for more eco-friendly production methods and the utilization of renewable energy sources. This emphasis on green alumina production is not merely a compliance issue but also a competitive differentiator, attracting investment and influencing purchasing decisions from downstream industries committed to their own sustainability goals. The ability to produce alumina with a lower carbon footprint will increasingly define market leadership.

Furthermore, regional shifts in manufacturing and consumption patterns are fundamentally reshaping the global alumina trade landscape. The Asia Pacific region is anticipated to be the primary growth engine, fueled by rapid industrialization and infrastructure development. This regional dominance necessitates a flexible global supply chain capable of meeting diverse demands and adapting to geopolitical and economic shifts. Companies that strategically invest in capacity expansion or partnerships within these high-growth geographies are likely to capture significant market share and benefit from the projected growth trajectory.

- Steady growth projected, driven by both traditional aluminum production and emerging non-metallurgical applications.

- Sustainability initiatives and environmental regulations are increasingly shaping production processes and market competitiveness.

- Asia Pacific remains the dominant and fastest-growing region due to industrial expansion and infrastructure projects.

- Innovation in specialty alumina grades is crucial for unlocking new revenue streams in high-tech sectors.

- Market participants are focusing on operational efficiency and supply chain resilience to mitigate economic volatility.

Alumina Market Drivers Analysis

The expansion of the alumina market is significantly propelled by the burgeoning demand for aluminum across various industries. Aluminum, largely produced from alumina, is a lightweight and versatile metal crucial for automotive manufacturing (especially electric vehicles), aerospace, and packaging sectors due to its strength-to-weight ratio and recyclability. The global push for fuel efficiency and reduced carbon emissions in transportation directly translates to higher demand for aluminum, and consequently, alumina.

Beyond traditional metallurgy, the rapid growth in non-metallurgical applications serves as a substantial driver. Alumina’s unique properties, such as high hardness, thermal stability, and electrical insulation, make it indispensable in advanced ceramics for industrial machinery, electronic components, and medical implants. The increasing adoption of high-performance ceramics in diverse sectors, coupled with the rising demand for refractories in high-temperature industrial processes, continues to diversify and strengthen the market for specialty alumina grades.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Aluminum | +1.5% | Global, especially Asia Pacific, North America, Europe | Long-term (2025-2033) |

| Growth in Non-Metallurgical Applications (Ceramics, Refractories) | +1.2% | Global, particularly China, India, Germany, Japan | Mid to Long-term (2027-2033) |

| Rising Infrastructure and Construction Activities | +0.8% | Asia Pacific (China, India, Southeast Asia) | Mid-term (2025-2030) |

| Expanding Automotive and Transportation Sector (EVs) | +0.7% | Global, focusing on North America, Europe, China | Long-term (2026-2033) |

Alumina Market Restraints Analysis

The alumina market faces significant headwinds from volatile energy prices and the substantial energy intensity of the refining process. The Bayer process, which converts bauxite into alumina, is highly energy-intensive, primarily relying on fossil fuels. Fluctuations in natural gas and electricity prices directly impact production costs, squeezing profit margins for alumina producers and potentially leading to higher end-product prices, which can dampen demand in price-sensitive applications. This dependency on energy also makes the industry vulnerable to geopolitical events affecting energy supply chains.

Another major restraint is the increasing stringency of environmental regulations and sustainability mandates. Alumina production generates bauxite residue, commonly known as red mud, which requires careful management and disposal due to its alkaline nature and potential environmental impact. Compliance with evolving regulations for waste disposal, air emissions, and water usage necessitates significant capital investment in advanced treatment technologies and sustainable practices, adding to operational costs and potentially limiting production expansion in regions with strict environmental oversight.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Energy Prices and High Production Costs | -0.9% | Global, particularly Europe, China | Short to Mid-term (2025-2028) |

| Stringent Environmental Regulations and Waste Management | -0.8% | Global, focusing on Europe, Australia, Brazil | Long-term (2025-2033) |

| Supply Chain Disruptions and Geopolitical Instability | -0.6% | Global, especially regions dependent on bauxite imports | Short-term (2025-2026) |

| Substitution by Alternative Materials in Niche Applications | -0.3% | Specific application segments globally | Mid to Long-term (2027-2033) |

Alumina Market Opportunities Analysis

Significant opportunities in the alumina market arise from the increasing adoption of lightweight materials, particularly aluminum, in the electric vehicle (EV) sector. As governments worldwide push for decarbonization and consumers demand more energy-efficient transportation, the demand for lightweighting solutions in EVs is surging. Alumina is a critical precursor for aluminum production, and its role in reducing vehicle weight directly contributes to extending battery range and improving overall EV performance. This trend represents a substantial growth avenue, pushing demand for high-quality, sustainably produced alumina.

Furthermore, advancements in specialty alumina applications, such as in advanced ceramics for high-performance electronics, medical devices, and industrial wear parts, present lucrative opportunities. These applications require alumina with specific properties like ultra-high purity, fine particle size, and tailored crystal structures, commanding premium prices. Investment in research and development to innovate new alumina grades and expand their functional capabilities will unlock new market segments and enhance the value proposition of alumina beyond its traditional uses.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand from Electric Vehicle (EV) Sector | +1.0% | Global, especially China, Europe, North America | Long-term (2026-2033) |

| Expansion in Advanced Ceramics and Electronics | +0.9% | Asia Pacific (Japan, South Korea, China), Europe, North America | Mid to Long-term (2027-2033) |

| Development of Sustainable Production Technologies (Green Alumina) | +0.7% | Global, with emphasis on developed markets | Long-term (2025-2033) |

| Application in Water Treatment and Catalysts | +0.6% | Global, particularly emerging economies with water scarcity issues | Mid-term (2025-2030) |

Alumina Market Challenges Impact Analysis

The alumina market faces significant challenges from geopolitical risks and supply chain vulnerabilities. As bauxite, the primary raw material for alumina, is concentrated in a few key regions, any political instability, trade disputes, or regulatory changes in these bauxite-rich countries can disrupt supply. This concentration of raw material sources makes the entire alumina value chain susceptible to price volatility and supply shortages, impacting production schedules and global market stability. Diversifying sourcing and building resilient logistics networks are critical for mitigating these risks.

Another pressing challenge is the imperative for decarbonization and the high carbon footprint associated with traditional alumina production. The energy-intensive nature of the Bayer process and the subsequent calcination results in substantial greenhouse gas emissions. Meeting increasingly stringent climate targets and consumer demands for sustainable products requires significant investment in renewable energy sources, carbon capture technologies, and process innovations to reduce emissions. This transition represents a substantial financial and technological hurdle for many producers, particularly those relying on older, less efficient facilities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Geopolitical Risks and Bauxite Supply Chain Concentration | -0.7% | Global, affecting major importing regions | Short to Mid-term (2025-2028) |

| High Carbon Footprint and Decarbonization Pressures | -0.6% | Global, particularly in regions with strict climate policies | Long-term (2025-2033) |

| Management and Disposal of Bauxite Residue (Red Mud) | -0.5% | Global, especially regions with large refining operations | Long-term (2025-2033) |

| Intensifying Competition and Price Sensitivity | -0.4% | Global, across all market segments | Ongoing (2025-2033) |

Alumina Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global alumina market, offering a detailed understanding of its current size, historical performance, and future growth projections. It encompasses a thorough examination of key market dynamics, including drivers, restraints, opportunities, and challenges that are shaping the industry landscape. The report segments the market by product type, application, and region, providing granular insights into demand and supply trends across various end-use industries and geographical areas, empowering stakeholders with actionable intelligence for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 65.5 Billion |

| Market Forecast in 2033 | USD 93.8 Billion |

| Growth Rate | 4.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Alcoa Corporation, Rio Tinto Alcan, South32 Ltd, Aluminum Corporation of China Limited (Chalco), Hindalco Industries Limited, Norsk Hydro ASA, Emirates Global Aluminium (EGA), National Aluminium Company Limited (NALCO), Sumitomo Chemical Co., Ltd., Nippon Light Metal Company, Ltd., RUSAL, Kaiser Aluminum Corporation, Sanxiang Advanced Materials Co., Ltd., Shandong Aluminium Company Limited, Zhongrui Alumina Co., Ltd., Motru Alumina SA, Orbita Aluminos, Huber Engineered Materials, Sasol Limited, Axens |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The alumina market is comprehensively segmented to provide a detailed understanding of its diverse applications and product forms, allowing for targeted analysis of market dynamics. This segmentation facilitates a deeper insight into specific growth drivers and consumption patterns across various industries and technological requirements, highlighting the nuances within the broader market. Understanding these distinct segments is crucial for identifying niche opportunities and developing tailored strategies.

- By Product Type: This segment includes various forms of alumina, each with unique properties and applications.

- Calcined Alumina: The most common form, used widely in metallurgical applications (aluminum production) and refractories.

- Tabular Alumina: Characterized by high density and thermal shock resistance, ideal for high-performance refractories and ceramics.

- Fused Alumina: Produced by melting calcined alumina, known for its extreme hardness, making it suitable for abrasives and refractory applications.

- Activated Alumina: A porous form used as a desiccant, adsorbent, and catalyst support in various chemical processes and water treatment.

- Grinding Grade Alumina: Specifically designed for abrasive applications, offering high hardness and consistent particle size.

- Others: Encompasses specialized grades like polishing alumina, dental alumina, and ultra-high purity alumina for niche applications.

- By Application: This segmentation outlines the primary end-use industries and purposes for which alumina is utilized.

- Refractories: Due to its high melting point and chemical stability, alumina is critical for manufacturing heat-resistant materials used in furnaces and kilns.

- Ceramics: Used in technical ceramics for electronic substrates, spark plugs, grinding media, and wear-resistant components due to its hardness and electrical insulation.

- Abrasives: Its extreme hardness makes it an excellent material for grinding wheels, sandpaper, blasting media, and polishing compounds.

- Chemicals: Utilized as a catalyst, catalyst support, adsorbent, and raw material for various aluminum chemicals.

- Metallurgical: Predominantly for primary aluminum production, representing the largest share of alumina consumption.

- Building & Construction: Used in cement, insulation, and as an additive to improve strength and durability.

- Automotive & Transportation: Applied in lightweight components, ceramic brakes, catalytic converters, and spark plugs to enhance fuel efficiency and performance.

- Electrical & Electronics: Essential for substrates in integrated circuits, insulators, and other electronic components requiring high dielectric strength and thermal conductivity.

- Medical: Employed in dental ceramics, prosthetics, and biomedical implants due to its biocompatibility and wear resistance.

- Others: Includes applications in glass, polishes, flame retardants, and consumer goods.

Regional Highlights

- Asia Pacific (APAC): Dominates the global alumina market, primarily driven by robust industrialization, rapid urbanization, and significant infrastructure development in countries like China, India, and Southeast Asian nations. China is the world's largest producer and consumer of alumina, with substantial capacity for both metallurgical and non-metallurgical applications. India's burgeoning construction and automotive sectors also contribute significantly to regional demand. The region benefits from abundant bauxite reserves and ongoing investments in refining capabilities, positioning it as the primary growth engine for the forecast period.

- North America: Represents a mature yet stable market for alumina, characterized by advanced manufacturing capabilities and a strong focus on high-performance materials. The demand is largely driven by the automotive industry (especially the shift towards lightweight EVs), aerospace, and advanced ceramics. The region emphasizes technological innovation and sustainable production methods, with a growing interest in specialty alumina grades for niche, high-value applications.

- Europe: A significant market for specialty alumina and high-quality aluminum products, with strong demand from the automotive, aerospace, and industrial sectors. Countries like Germany, France, and the UK are key consumers, particularly for advanced ceramics and refractories. The European market is highly influenced by stringent environmental regulations and a strong commitment to circular economy principles, driving demand for energy-efficient and low-carbon alumina production.

- Latin America: Holds considerable importance due to its substantial bauxite reserves, particularly in Brazil. The region is a key exporter of alumina, primarily to North America and Europe. While domestic consumption is growing, driven by construction and packaging, its primary role remains a crucial supplier to the global market, with potential for further development in downstream industries.

- Middle East & Africa (MEA): Emerging as a notable region for alumina production and consumption, particularly with the establishment of large-scale aluminum smelters in the Gulf Cooperation Council (GCC) countries. These smelters often integrate backward into alumina refining to ensure raw material security. The region's strategic location and access to energy resources support the growth of the aluminum value chain, driving demand for alumina.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Alumina Market.- Alcoa Corporation

- Rio Tinto Alcan

- South32 Ltd

- Aluminum Corporation of China Limited (Chalco)

- Hindalco Industries Limited

- Norsk Hydro ASA

- Emirates Global Aluminium (EGA)

- National Aluminium Company Limited (NALCO)

- Sumitomo Chemical Co., Ltd.

- Nippon Light Metal Company, Ltd.

- RUSAL

- Kaiser Aluminum Corporation

- Sanxiang Advanced Materials Co., Ltd.

- Shandong Aluminium Company Limited

- Zhongrui Alumina Co., Ltd.

- Motru Alumina SA

- Orbita Aluminos

- Huber Engineered Materials

- Sasol Limited

- Axens

Frequently Asked Questions

What is alumina primarily used for?

Alumina is primarily used as the fundamental raw material for producing aluminum metal, accounting for over 90% of its global consumption. Beyond metallurgy, it is extensively utilized in non-metallurgical applications such as refractories, advanced ceramics, abrasives, and as a chemical feedstock due to its high hardness, excellent thermal stability, and electrical insulating properties.

Which region dominates the global alumina market?

The Asia Pacific region, particularly China and India, dominates the global alumina market in terms of both production and consumption. This dominance is driven by rapid industrialization, extensive infrastructure development, and a booming demand from the region's construction, automotive, and electronic sectors.

What are the key drivers for alumina market growth?

Key drivers for alumina market growth include the increasing global demand for lightweight aluminum in automotive (especially electric vehicles) and aerospace industries, rapid urbanization and infrastructure development, and the growing adoption of specialty alumina in advanced ceramics, refractories, and high-tech electronics applications.

What challenges does the alumina market face?

The alumina market faces several challenges, including volatile energy prices due to the energy-intensive production process, stringent environmental regulations regarding bauxite residue (red mud) disposal, and potential supply chain disruptions linked to the concentration of bauxite reserves in specific regions. Decarbonization pressures also pose a significant long-term challenge.

How is AI impacting the alumina industry?

AI is impacting the alumina industry by enabling predictive maintenance for equipment, optimizing energy consumption in refining processes, enhancing quality control through advanced analytics, and improving supply chain efficiency. These applications lead to reduced operational costs, increased productivity, and more consistent product quality.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted