Alumina and Bauxite Market

Alumina and Bauxite Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705825 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

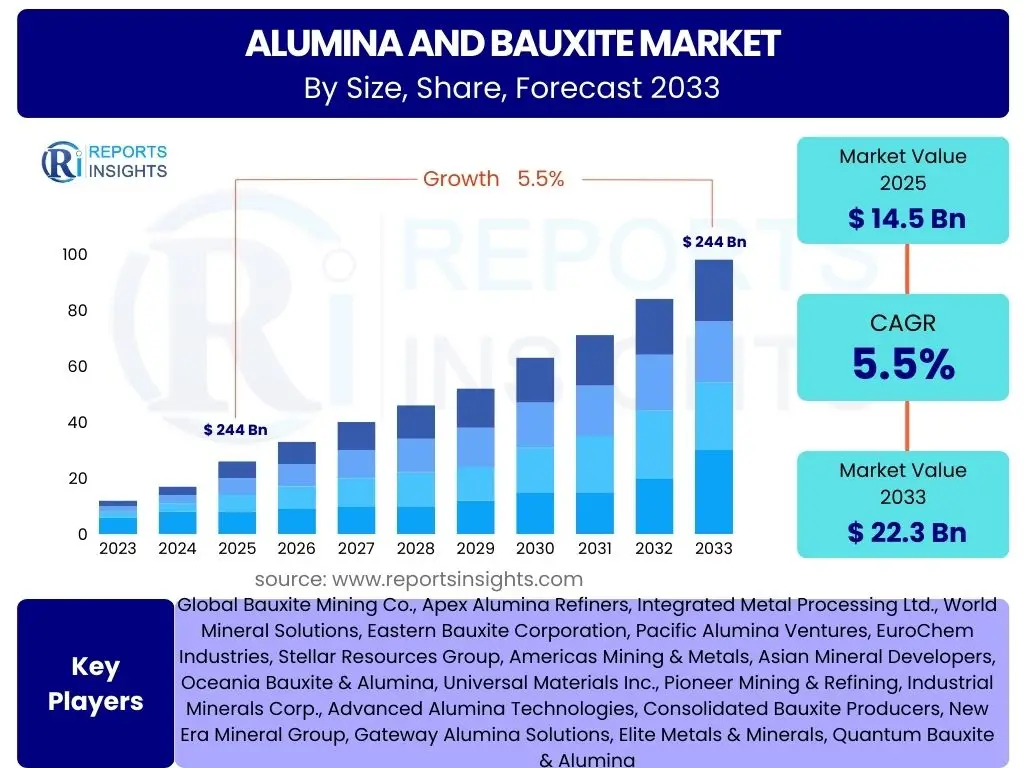

Alumina and Bauxite Market Size

According to Reports Insights Consulting Pvt Ltd, The Alumina and Bauxite Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2025 and 2033. The market is estimated at USD 14.5 Billion in 2025 and is projected to reach USD 22.3 Billion by the end of the forecast period in 2033.

Key Alumina and Bauxite Market Trends & Insights

The Alumina and Bauxite market is witnessing significant transformations driven by evolving industrial demands, increasing sustainability concerns, and advancements in processing technologies. Users frequently inquire about the primary drivers of market growth, the influence of environmental regulations, and the role of new technologies in optimizing production and consumption. Key trends indicate a sustained demand from the construction, automotive, and packaging sectors, alongside a growing emphasis on lightweight materials and circular economy principles.

Furthermore, geopolitical shifts and supply chain vulnerabilities are prompting industry players to diversify sourcing and invest in resilient logistics. The integration of advanced analytics and automation within mining and refining operations is emerging as a critical trend, aiming to enhance efficiency and reduce operational costs. The market is also responding to global initiatives for carbon emission reduction, leading to increased research and development in greener production methods and the utilization of bauxite residue.

- Growing demand from the construction and infrastructure sectors globally.

- Increasing adoption of lightweight materials in the automotive and aerospace industries.

- Rising focus on sustainable mining practices and bauxite residue utilization.

- Technological advancements in alumina refining processes to improve efficiency.

- Expansion of the packaging industry, particularly for food and beverage applications.

- Shifting supply chain dynamics due to geopolitical factors and trade policies.

AI Impact Analysis on Alumina and Bauxite

User queries regarding the impact of Artificial intelligence (AI) on the Alumina and Bauxite sector frequently revolve around operational optimization, cost reduction, and enhanced safety. AI is poised to revolutionize various stages of the value chain, from exploration and mining to processing and logistics. Its application promises more precise resource identification, optimized mining plans, and predictive maintenance for heavy machinery, thereby minimizing downtime and maximizing output.

Beyond mining, AI algorithms can refine the bauxite refining process, leading to improved alumina quality and reduced energy consumption. In logistics, AI-powered systems can optimize transport routes and inventory management, ensuring a more efficient and responsive supply chain. While there are concerns about initial investment costs and workforce retraining, the long-term benefits of AI in terms of efficiency gains, sustainability improvements, and competitive advantage are widely recognized, positioning it as a transformative force within the industry.

- Enhanced exploration and resource modeling through AI-driven data analysis.

- Optimization of mining operations with autonomous vehicles and AI-powered equipment.

- Predictive maintenance for machinery, reducing unplanned downtime and operational costs.

- Improved process control and quality assurance in alumina refining through machine learning.

- Supply chain optimization and demand forecasting for better inventory management.

- Enhanced safety protocols and risk assessment in hazardous mining environments.

Key Takeaways Alumina and Bauxite Market Size & Forecast

Analysis of common user questions regarding the Alumina and Bauxite market size and forecast reveals a keen interest in understanding the primary growth catalysts, potential market volatility, and strategic investment areas. The market's sustained growth is fundamentally driven by robust demand from key industrial sectors such as construction, automotive, and packaging, alongside emerging applications in renewable energy infrastructure. Future projections indicate that Asian Pacific economies will continue to be significant demand centers, propelled by rapid urbanization and industrial expansion.

Despite potential headwinds from regulatory changes and energy price fluctuations, the market demonstrates resilience, underpinned by the essential nature of alumina and bauxite in diverse manufacturing processes. Stakeholders are increasingly focusing on innovations that enhance production efficiency, embrace sustainable practices, and fortify supply chain robustness. This strategic emphasis is expected to mitigate risks and unlock new growth avenues, making the sector attractive for long-term investments focused on technological advancement and environmental stewardship.

- The market is poised for steady growth driven by global industrial development.

- Emerging economies, particularly in Asia Pacific, will be crucial growth engines.

- Sustainability and circular economy principles are becoming key market differentiators.

- Technological advancements in mining and refining are essential for competitive advantage.

- Supply chain resilience and diversification are paramount in a volatile geopolitical landscape.

- Increased investment in bauxite exploration and alumina production capacity is anticipated.

Alumina and Bauxite Market Drivers Analysis

The Alumina and Bauxite market is significantly propelled by several key factors. The global increase in urbanization and infrastructure development, particularly in emerging economies, directly translates to higher demand for aluminum, which relies heavily on alumina production. Additionally, the automotive sector's shift towards lightweight materials to improve fuel efficiency and support electric vehicles creates a strong pull for aluminum and, consequently, for its primary raw materials. These fundamental demands underpin the sustained growth trajectory of the market.

Beyond these, the burgeoning packaging industry, driven by rising consumerism and the need for versatile, recyclable materials, further contributes to the market's expansion. Innovations in aluminum alloys and processing technologies also open new application areas, indirectly boosting demand for alumina and bauxite. The interplay of these factors creates a dynamic and robust demand landscape, influencing investment decisions across the value chain and shaping regional market dynamics.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Industrialization and Urbanization | +Insert Here% | Asia Pacific, Latin America, Africa | Long-term (2025-2033) |

| Growth in Construction and Infrastructure Development | +Insert Here% | Global, particularly China, India, Southeast Asia | Long-term (2025-2033) |

| Increasing Demand from Electric Vehicle (EV) Sector | +Insert Here% | North America, Europe, China | Mid to Long-term (2027-2033) |

| Rise in Packaging Industry Demand | +Insert Here% | Global, particularly developing markets | Mid to Long-term (2026-2033) |

Alumina and Bauxite Market Restraints Analysis

Despite promising growth drivers, the Alumina and Bauxite market faces several significant restraints that could impede its expansion. Stringent environmental regulations and increasingly ambitious carbon emission targets imposed by governments worldwide pose considerable challenges for miners and refiners. Compliance often requires substantial capital expenditure for upgrading facilities and adopting cleaner technologies, which can impact profitability and deter new investments. These regulatory hurdles vary significantly by region, creating complex operational landscapes for global players.

Furthermore, the inherent volatility of energy prices directly affects production costs, as both bauxite mining and alumina refining are highly energy-intensive processes. Fluctuations in oil and gas prices can lead to unpredictable operational expenses, impacting pricing strategies and overall market stability. Geopolitical tensions and evolving trade policies also present a major restraint, potentially disrupting established supply chains and leading to higher logistical costs or even raw material shortages. Navigating these external economic and political factors requires robust risk management strategies and diversified sourcing.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Environmental Regulations and Carbon Emission Targets | +Insert Here% | Europe, North America, Australia | Long-term (2025-2033) |

| Volatility in Energy Prices | +Insert Here% | Global | Short to Mid-term (2025-2028) |

| Geopolitical Tensions and Trade Policies | +Insert Here% | Global, particularly major producing and consuming nations | Short to Mid-term (2025-2029) |

| High Capital Expenditure for New Projects | +Insert Here% | Global | Long-term (2025-2033) |

Alumina and Bauxite Market Opportunities Analysis

The Alumina and Bauxite market is ripe with opportunities that can foster significant growth and innovation. The increasing global emphasis on lightweight materials, particularly within the automotive and aerospace sectors, presents a substantial avenue for market expansion. As manufacturers seek to improve fuel efficiency and reduce emissions, the demand for aluminum, and by extension alumina, is set to rise, opening doors for specialized and high-purity product offerings. This trend is further amplified by the rapid growth of the electric vehicle market, where aluminum plays a crucial role in battery casings and structural components.

Another major opportunity lies in the burgeoning focus on the circular economy and recycling initiatives. Developing efficient technologies for recycling aluminum from end-of-life products not only reduces reliance on primary raw materials but also addresses environmental concerns, creating a sustainable value proposition. Furthermore, technological advancements in bauxite processing and alumina refining, such as the development of novel extraction methods or more energy-efficient furnaces, can significantly lower production costs and enhance market competitiveness. Untapped bauxite reserves in emerging economies, coupled with improved exploration techniques, also present strategic opportunities for resource diversification and long-term supply security, provided infrastructure and regulatory frameworks are supportive.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Lightweight Materials in Automotive and Aerospace | +Insert Here% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Increasing Focus on Circular Economy and Recycling | +Insert Here% | Europe, North America, Japan | Long-term (2026-2033) |

| Development of Advanced Processing Technologies | +Insert Here% | Global, particularly R&D hubs | Mid to Long-term (2027-2033) |

| Untapped Bauxite Reserves in Emerging Economies | +Insert Here% | Africa, Southeast Asia, Latin America | Long-term (2028-2033) |

Alumina and Bauxite Market Challenges Impact Analysis

The Alumina and Bauxite market confronts various challenges that necessitate careful strategic navigation. A significant hurdle is the industry's concentrated dependence on specific mining regions for bauxite supply, which makes it vulnerable to geopolitical instabilities, labor disputes, or localized environmental issues. This geographic concentration poses risks to supply chain continuity and can lead to price volatility, impacting global market stability and the operational planning of major consumers.

Another pressing challenge is the effective management of waste and tailings generated during bauxite mining and alumina refining. The environmental impact and regulatory scrutiny associated with red mud disposal, for instance, demand innovative and cost-effective solutions. Furthermore, intense competition from substitute materials, such as plastics or composites in certain applications, continuously pressures the market to maintain cost-effectiveness and demonstrate superior performance. Lastly, the industry faces a growing challenge of skilled labor shortages, particularly in specialized mining and processing roles, which can hinder operational efficiency and the adoption of advanced technologies, thereby impacting overall productivity and expansion plans.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Dependence on Specific Mining Regions | +Insert Here% | Australia, Guinea, Brazil, China | Long-term (2025-2033) |

| Managing Waste and Tailings (Red Mud) | +Insert Here% | Global, particularly major refining hubs | Long-term (2025-2033) |

| Intense Competition from Substitute Materials | +Insert Here% | Global, particularly in packaging and automotive | Mid to Long-term (2026-2033) |

| Skilled Labor Shortages | +Insert Here% | Global, particularly developed economies | Long-term (2025-2033) |

Alumina and Bauxite Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global Alumina and Bauxite market, providing an in-depth analysis of market size, trends, drivers, restraints, opportunities, and challenges. It offers a detailed segmentation analysis based on product type, application, end-use industry, and grade, alongside a thorough regional and country-level assessment. The report also highlights the competitive landscape, profiling key players and their strategic initiatives, enabling stakeholders to make informed business decisions and identify emerging market avenues.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 14.5 Billion |

| Market Forecast in 2033 | USD 22.3 Billion |

| Growth Rate | 5.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Bauxite Mining Co., Apex Alumina Refiners, Integrated Metal Processing Ltd., World Mineral Solutions, Eastern Bauxite Corporation, Pacific Alumina Ventures, EuroChem Industries, Stellar Resources Group, Americas Mining & Metals, Asian Mineral Developers, Oceania Bauxite & Alumina, Universal Materials Inc., Pioneer Mining & Refining, Industrial Minerals Corp., Advanced Alumina Technologies, Consolidated Bauxite Producers, New Era Mineral Group, Gateway Alumina Solutions, Elite Metals & Minerals, Quantum Bauxite & Alumina |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Alumina and Bauxite market is segmented to provide a granular understanding of its diverse components, allowing for targeted analysis of supply and demand dynamics across various product forms, applications, end-use industries, and quality grades. This segmentation is crucial for identifying specific growth pockets, assessing competitive landscapes within niches, and formulating precise strategic responses to evolving market needs. Each segment is characterized by unique demand drivers and market characteristics, reflecting the versatility of these essential raw materials.

Understanding these distinct segments enables stakeholders to pinpoint opportunities for product differentiation, market entry, and value chain optimization. For instance, the demand for metallurgical grade alumina is primarily driven by the aluminum smelting industry, whereas non-metallurgical grades find applications in diverse sectors like refractories, abrasives, and chemicals, each with its own growth trajectory and regulatory landscape. Analyzing these segments individually provides a comprehensive view of the market's current state and future potential.

- By Product

- Alumina

- Bauxite

- By Application

- Metallurgical

- Refractory

- Abrasives

- Chemicals

- Cement

- Others

- By End-Use Industry

- Automotive

- Construction

- Packaging

- Electronics

- Aviation

- Others

- By Grade

- Metallurgical Grade

- Non-Metallurgical Grade

Regional Highlights

- North America: Characterized by significant demand from the automotive, aerospace, and packaging sectors. Focus on lightweighting trends and advanced manufacturing. Investments in recycling infrastructure are prominent.

- Europe: Driven by strict environmental regulations pushing for sustainable production and increased recycling rates. Strong demand from construction and chemical industries. Research and development in advanced materials and processing.

- Asia Pacific (APAC): The largest and fastest-growing market due to rapid industrialization, urbanization, and robust growth in construction, automotive, and consumer goods industries in countries like China, India, and Southeast Asia. Major production hub for both bauxite and alumina.

- Latin America: Possesses substantial bauxite reserves, particularly in Brazil and Jamaica, making it a crucial supplier region. Growing domestic demand from construction and infrastructure projects.

- Middle East and Africa (MEA): Emerging as a key region for bauxite mining and alumina refining investments, leveraging rich mineral resources and access to energy. Developing downstream aluminum industries are boosting demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Alumina and Bauxite Market.- Global Bauxite Mining Co.

- Apex Alumina Refiners

- Integrated Metal Processing Ltd.

- World Mineral Solutions

- Eastern Bauxite Corporation

- Pacific Alumina Ventures

- EuroChem Industries

- Stellar Resources Group

- Americas Mining & Metals

- Asian Mineral Developers

- Oceania Bauxite & Alumina

- Universal Materials Inc.

- Pioneer Mining & Refining

- Industrial Minerals Corp.

- Advanced Alumina Technologies

- Consolidated Bauxite Producers

- New Era Mineral Group

- Gateway Alumina Solutions

- Elite Metals & Minerals

- Quantum Bauxite & Alumina

Frequently Asked Questions

Analyze common user questions about the Alumina and Bauxite market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the primary use of alumina in the global market?

The primary use of alumina (aluminum oxide) in the global market is for the production of aluminum metal. Approximately 90% of all alumina produced is smelted to create primary aluminum, which is then used in various industries such as automotive, construction, packaging, and aerospace due to its lightweight and corrosion-resistant properties. The remaining portion of alumina, known as non-metallurgical alumina, serves diverse applications including refractories, abrasives, ceramics, and chemicals.

How is bauxite processed to extract alumina?

Bauxite is primarily processed to extract alumina through the Bayer process. This method involves crushing the bauxite ore and then dissolving the aluminum-bearing minerals using a hot, concentrated caustic soda (sodium hydroxide) solution under high pressure. This dissolution forms a sodium aluminate solution. Impurities, such as iron oxides and silicates, remain as insoluble red mud, which is separated. The purified sodium aluminate solution is then cooled, and alumina hydrate crystals precipitate out. These crystals are subsequently heated to very high temperatures (calcined) to remove water, resulting in anhydrous alumina powder.

What factors primarily influence bauxite and alumina prices?

Several key factors influence bauxite and alumina prices. Global demand for aluminum, driven by growth in end-use industries like construction, automotive, and packaging, is a primary determinant. Supply-side factors, including the availability of bauxite reserves, mining costs, energy prices (as both processes are energy-intensive), and geopolitical stability in major producing regions (e.g., Australia, Guinea, Brazil), significantly impact pricing. Additionally, freight costs, environmental regulations, and the operational status of major refineries and smelters contribute to price volatility.

What are the key environmental concerns associated with alumina production?

The primary environmental concern associated with alumina production is the generation and disposal of bauxite residue, commonly known as red mud. Red mud is highly alkaline and contains various heavy metals, posing risks to soil and water if not managed properly. Other concerns include significant energy consumption leading to greenhouse gas emissions, land disturbance from bauxite mining, and the potential for water pollution from processing chemicals. The industry is actively investing in technologies for red mud neutralization, beneficial reuse, and carbon capture to mitigate these impacts.

What is the future outlook for the Alumina and Bauxite market?

The future outlook for the Alumina and Bauxite market is positive, driven by sustained global industrial growth and increasing demand for aluminum in lightweighting applications and sustainable packaging. Emerging economies, particularly in Asia Pacific, are expected to lead demand growth. While challenges such as environmental regulations, energy costs, and supply chain vulnerabilities persist, ongoing technological advancements in mining and refining, coupled with a growing focus on circular economy principles and AI integration, are anticipated to enhance efficiency, reduce environmental footprints, and open new avenues for market expansion. Strategic investments in resource diversification and sustainable practices will be crucial for long-term resilience.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted