All Solid State Lithium Battery Market

All Solid State Lithium Battery Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707899 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

All Solid State Lithium Battery Market Size

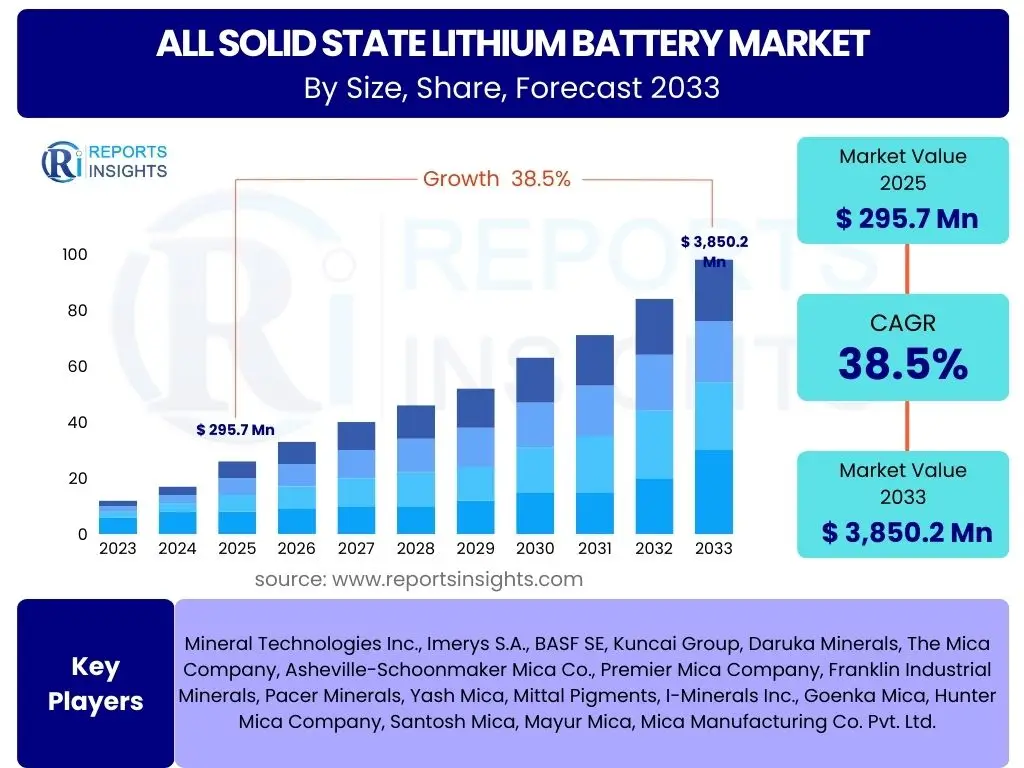

According to Reports Insights Consulting Pvt Ltd, The All Solid State Lithium Battery Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 38.5% between 2025 and 2033. The market is estimated at USD 295.7 Million in 2025 and is projected to reach USD 3,850.2 Million by the end of the forecast period in 2033.

Key All Solid State Lithium Battery Market Trends & Insights

The All Solid State Lithium Battery market is undergoing a rapid transformation driven by a confluence of technological advancements and increasing demand for superior energy storage solutions. Common user inquiries often revolve around the core innovations that are pushing this market forward, such as improvements in electrolyte materials, manufacturing processes, and safety features. Users are keen to understand how these batteries overcome the limitations of traditional lithium-ion technology, particularly concerning energy density, charging speed, and thermal stability. The integration of solid electrolytes is a primary area of interest, as it promises to eliminate the fire risks associated with liquid electrolytes, thereby enhancing overall battery safety and reliability.

Furthermore, significant interest is observed in the miniaturization capabilities of all solid state batteries and their potential to power a new generation of compact and high-performance electronic devices. The pursuit of higher energy densities remains a paramount trend, aiming to extend the range of electric vehicles (EVs) and the operational life of portable electronics. Material science breakthroughs, including the development of novel ceramic, polymer, and sulfide-based solid electrolytes, are critical to achieving these performance enhancements. These materials are being optimized for ionic conductivity, mechanical strength, and chemical stability, directly addressing interface resistance and volume change challenges. The market is also witnessing a strong trend toward strategic collaborations between automotive manufacturers, battery developers, and material suppliers to accelerate commercialization and scale up production capabilities, indicating a shared vision for the future of energy storage.

- Enhanced safety due to the elimination of flammable liquid electrolytes.

- Significant increases in energy density for extended range and operational life.

- Faster charging capabilities, reducing charge times for electric vehicles and portable devices.

- Advancements in solid electrolyte materials, including sulfide, oxide, and polymer types.

- Growing investment in manufacturing process scalability and cost reduction.

- Increasing adoption in diverse applications beyond electric vehicles, such as consumer electronics and aerospace.

- Strategic partnerships and collaborations across the value chain to accelerate development.

AI Impact Analysis on All Solid State Lithium Battery

User questions regarding the impact of Artificial Intelligence (AI) on the All Solid State Lithium Battery market frequently explore how AI can accelerate material discovery, optimize manufacturing processes, and enhance battery performance. There is a strong interest in understanding how advanced computational methods, machine learning algorithms, and predictive analytics are being leveraged to overcome the inherent complexities of solid-state battery development. Users often seek insights into AI's role in identifying new solid electrolyte materials with improved ionic conductivity and stability, which is a major bottleneck in current research. Furthermore, the application of AI in simulating battery behavior under various conditions, predicting degradation pathways, and optimizing cell design for maximum efficiency and lifespan is a key area of inquiry, highlighting the perceived potential of AI to revolutionize R&D cycles.

The integration of AI extends beyond laboratory research into the manufacturing phase, where it is anticipated to play a crucial role in enhancing production efficiency and quality control. Users are interested in how AI-driven analytics can monitor and adjust manufacturing parameters in real time, reducing defects and improving yield rates for complex solid-state battery fabrication. Additionally, AI's capability to develop more sophisticated Battery Management Systems (BMS) for all solid state batteries is a significant area of focus. These advanced BMS can utilize machine learning to predict battery health, optimize charging and discharging cycles, and prevent potential issues, thereby maximizing the safety and longevity of the batteries in practical applications. Overall, the consensus among user inquiries points towards AI as a transformative technology, enabling faster innovation, more efficient production, and superior performance for all solid state lithium batteries.

- Accelerated discovery and screening of novel solid electrolyte materials through machine learning.

- Optimization of manufacturing parameters and processes to improve production efficiency and yield.

- Predictive modeling of battery performance, lifespan, and degradation mechanisms.

- Enhanced Battery Management Systems (BMS) for improved safety and operational efficiency.

- Real-time quality control and defect detection during the battery fabrication process.

- Simulation of complex electrochemical reactions to refine cell design and material composition.

Key Takeaways All Solid State Lithium Battery Market Size & Forecast

Common user questions regarding key takeaways from the All Solid State Lithium Battery market size and forecast frequently center on understanding the magnitude of growth, the primary drivers behind this expansion, and the critical factors that will influence its future trajectory. Users are particularly interested in identifying the main application areas expected to fuel demand and the technological breakthroughs essential for achieving the projected market valuations. The insights gathered suggest a strong emphasis on the transformational potential of this technology in the electric vehicle sector, where enhanced safety, higher energy density, and faster charging capabilities are highly sought after. The forecast indicates not just growth, but a profound shift in energy storage paradigms, contingent upon successful commercialization and mass production scale-up.

The rapid Compound Annual Growth Rate (CAGR) projected for the market signifies a high-confidence outlook from industry experts, reflecting the substantial research and development investments currently underway globally. Users are keen to know if the forecasted growth is sustainable, how regulatory frameworks might impact adoption, and whether the inherent challenges of cost and manufacturing complexity can be effectively mitigated within the forecast period. The key takeaway emphasizes that while the path to widespread adoption involves significant hurdles, the intrinsic benefits of all solid state batteries over conventional lithium-ion technologies—particularly in terms of safety and performance—create an undeniable market pull. This suggests a future where these batteries become a cornerstone of sustainable energy solutions, driven by continuous innovation and strategic industry alliances.

- The market is poised for exceptional growth, driven by superior safety and performance attributes.

- Electric Vehicles (EVs) represent the most significant application segment and primary growth catalyst.

- Key technological advancements in solid electrolytes and manufacturing scalability are crucial for realizing the forecast.

- Investments in research and development, coupled with strategic partnerships, are accelerating commercialization efforts.

- Cost reduction and overcoming manufacturing complexities remain critical factors for widespread adoption.

- The long-term forecast indicates a substantial shift towards all solid state battery technology across various industries.

All Solid State Lithium Battery Market Drivers Analysis

The All Solid State Lithium Battery market is significantly propelled by an escalating global demand for energy storage solutions that offer enhanced safety, higher performance, and environmental sustainability. A primary driver is the inherent safety advantage of solid electrolytes, which eliminate the risk of thermal runaway and fire associated with flammable liquid electrolytes in conventional lithium-ion batteries. This is particularly critical for high-energy applications like electric vehicles and grid storage, where safety incidents can have severe consequences. Furthermore, the continuous pursuit of higher energy density to extend the range of EVs and the operational life of portable electronic devices acts as a powerful catalyst, as solid-state technology promises to surpass the theoretical limits of current battery chemistries. The ability to achieve faster charging rates and operate across a wider temperature range without compromising performance further enhances their appeal.

Additionally, the increasing focus on decarbonization and the transition to electric mobility worldwide are creating immense pressure for battery innovation. Government incentives, stringent emission regulations, and growing consumer awareness regarding environmental impact are accelerating the adoption of electric vehicles, directly fueling the demand for advanced battery technologies like all solid state batteries. Investment in battery research and development by major automotive manufacturers and tech giants underscores the strategic importance of this technology. These investments aim not only to improve performance but also to reduce manufacturing costs and achieve economies of scale, making all solid state batteries more competitive and accessible to a broader market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Enhanced Safety (Elimination of Flammable Electrolytes) | +8.2% | Global, particularly EV-heavy regions | Short to Medium Term |

| Higher Energy Density for Extended Range/Usage | +7.5% | Global, especially automotive and consumer electronics | Medium to Long Term |

| Faster Charging Capabilities | +6.8% | North America, Europe, Asia Pacific | Medium Term |

| Growing Demand for Electric Vehicles (EVs) | +9.1% | Asia Pacific (China), Europe, North America | Short to Long Term |

| Miniaturization for Compact Devices | +3.0% | Asia Pacific (Japan, South Korea), North America | Short to Medium Term |

All Solid State Lithium Battery Market Restraints Analysis

Despite their significant potential, the All Solid State Lithium Battery market faces several formidable restraints that could temper its growth trajectory. A primary impediment is the high manufacturing cost associated with current production methods. The intricate processes required to fabricate solid electrolytes and ensure stable interfaces between electrode and electrolyte layers are complex and expensive, making all solid state batteries significantly pricier than their liquid-ion counterparts. This cost disparity presents a considerable challenge for mass market adoption, especially in price-sensitive segments like mainstream electric vehicles. Furthermore, the inherent complexity of manufacturing these batteries at scale, ensuring consistent quality and performance across large batches, remains a significant hurdle. Current production techniques are often geared towards small-scale laboratory settings, and scaling up to industrial volumes without compromising quality or dramatically increasing costs is a complex engineering and materials science problem.

Another critical restraint involves the technical challenges related to interface resistance and material compatibility. Achieving low interfacial resistance between the solid electrolyte and electrodes is crucial for high power and efficient energy transfer, yet it remains difficult to maintain stable contact over repeated charge-discharge cycles. Issues such as volume changes of electrode materials during cycling can lead to the formation of voids or cracks, compromising the interface and battery performance. Additionally, the availability and cost of specific raw materials required for advanced solid electrolytes, such as certain rare earth elements or specialized polymers, could become supply chain bottlenecks as production scales. These technical and economic challenges necessitate continuous research and development, as well as significant capital investment, before all solid state batteries can fully penetrate the mainstream market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs | -7.5% | Global | Short to Medium Term |

| Complex Manufacturing Processes and Scalability Issues | -6.0% | Global | Short to Medium Term |

| Technical Challenges (Interface Resistance, Dendrite Formation) | -5.8% | Global | Short to Medium Term |

| Limited Material Availability and Supply Chain Vulnerabilities | -4.2% | Asia Pacific, Europe | Medium Term |

| Long Development Cycles and High R&D Investment | -3.5% | Global | Short to Medium Term |

All Solid State Lithium Battery Market Opportunities Analysis

The All Solid State Lithium Battery market is rich with significant opportunities for growth and innovation, driven by evolving technological landscapes and expanding application horizons. One of the most prominent opportunities lies in the expansion into new, high-value applications beyond traditional electric vehicles and consumer electronics. Sectors such as aerospace and defense, medical devices, and large-scale grid energy storage are particularly attractive due to their stringent demands for safety, reliability, and long cycle life, where the inherent advantages of solid-state batteries can command a premium. The development of customized battery solutions for these niche markets can provide early revenue streams and further validate the technology's capabilities, fostering broader adoption. Furthermore, the potential for solid-state batteries to facilitate advanced urban air mobility (UAM) and drone technologies, which require lightweight, high-power, and safe energy sources, presents a burgeoning area for market penetration.

Another crucial opportunity stems from continuous material science innovation and strategic collaborations. The ongoing research into novel solid electrolyte materials, including advanced polymers, ceramics, and sulfide-based compounds, aims to overcome existing limitations such as ionic conductivity and interface stability, paving the way for next-generation battery performance. Companies that invest in proprietary material development and intellectual property will gain a significant competitive edge. Moreover, strategic partnerships between battery manufacturers, automotive OEMs, and material suppliers can accelerate R&D, de-risk commercialization, and streamline the path to mass production, allowing for shared expertise and resource optimization. The growing global emphasis on sustainable energy and the circular economy also opens opportunities for developing robust recycling infrastructure for solid-state battery components, which will be essential for long-term environmental sustainability and resource efficiency within the industry.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New High-Value Applications (Aerospace, Medical) | +7.0% | North America, Europe, Asia Pacific | Medium to Long Term |

| Material Innovation and Advanced Solid Electrolyte Development | +8.5% | Global R&D Hubs (Japan, USA, Germany) | Short to Long Term |

| Strategic Partnerships and Joint Ventures | +6.2% | Global (cross-regional collaborations) | Short to Medium Term |

| Development of Recycling and Circular Economy Infrastructure | +4.0% | Europe, North America, Japan | Long Term |

| Government Funding and Regulatory Support for Green Technologies | +5.5% | Europe, North America, China | Short to Medium Term |

All Solid State Lithium Battery Market Challenges Impact Analysis

The All Solid State Lithium Battery market, while promising, contends with several significant challenges that require sustained innovation and investment to overcome. A critical technical challenge is the high interfacial resistance that often forms between the solid electrolyte and electrode materials. This resistance hinders the movement of lithium ions, reducing power output and overall battery performance, particularly at high charge/discharge rates. Maintaining stable, low-resistance interfaces over many charge-discharge cycles is crucial, yet difficult, as electrode materials expand and contract, potentially causing delamination or crack formation. Another significant concern is the suppression of lithium dendrite formation, particularly with lithium metal anodes. While solid electrolytes are expected to physically block dendrites, imperfections or localized stresses can still lead to short circuits, diminishing battery safety and cycle life, especially at high current densities.

Beyond these technical hurdles, manufacturing scalability and cost reduction remain overarching challenges. Current fabrication methods for solid-state batteries are complex and expensive, often involving specialized equipment and multi-step processes that are not yet amenable to high-volume, cost-effective production. Achieving economies of scale comparable to conventional lithium-ion batteries requires significant breakthroughs in manufacturing efficiency and automation. Furthermore, thermal management in all solid state batteries, though less prone to thermal runaway than liquid electrolytes, still presents challenges. Efficient heat dissipation is necessary to maintain optimal operating temperatures, prevent performance degradation, and ensure long-term reliability, especially in high-power applications. Overcoming these multifaceted challenges demands coordinated efforts across materials science, engineering, and manufacturing to unlock the full potential and widespread commercialization of this transformative battery technology.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Interfacial Resistance at Electrode/Electrolyte | -6.5% | Global | Short to Medium Term |

| Suppression of Lithium Dendrite Formation | -5.0% | Global | Short to Medium Term |

| Scalability of Manufacturing Processes and Cost Reduction | -7.0% | Global | Short to Medium Term |

| Maintaining Mechanical Stability during Cycling | -4.8% | Global | Short to Medium Term |

| Thermal Management and Heat Dissipation Issues | -3.5% | Global | Medium Term |

All Solid State Lithium Battery Market - Updated Report Scope

This report provides an in-depth analysis of the All Solid State Lithium Battery Market, offering a comprehensive understanding of its current size, growth dynamics, key trends, and future projections. It covers detailed segmentation across various battery types, electrolyte materials, applications, capacities, and power outputs, providing a granular view of market opportunities and challenges. The scope encompasses a thorough examination of market drivers, restraints, opportunities, and challenges, along with a competitive landscape analysis profiling major industry players. The report aims to furnish stakeholders with actionable insights to navigate market complexities and capitalize on emerging growth avenues, making it an essential resource for strategic decision-making in the evolving energy storage sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 295.7 Million |

| Market Forecast in 2033 | USD 3,850.2 Million |

| Growth Rate | 38.5% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Toyota, Samsung SDI, LG Energy Solution, Solid Power, QuantumScape, SK On, Panasonic, CATL, Ilika, Factorial Energy, StoreDot, ProLogium, Honda, BMW, Ford, Hyundai, Nio, Contemporary Amperex Technology Co. Limited, Northvolt, Blue Solutions (Bolloré) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The All Solid State Lithium Battery market is rigorously segmented to provide a detailed and granular understanding of its diverse components and growth avenues. This segmentation allows for precise market sizing, trend identification, and strategic planning across various technological and application landscapes. By dissecting the market along key parameters such as battery type, electrolyte composition, end-use application, capacity, and power output, stakeholders can pinpoint specific growth drivers, competitive niches, and emerging opportunities. This detailed breakdown ensures that the analysis captures the nuances of a rapidly evolving technology, from small-scale applications in wearables to high-power demands in electric vehicles, reflecting the varied performance requirements and technical challenges inherent in each segment.

Understanding these segments is crucial for market participants looking to tailor their product development, investment strategies, and market entry approaches. For instance, the distinction between thin-film and bulk solid-state batteries highlights different manufacturing complexities and target applications, with thin-films often favored for micro-electronics due to their compact size, while bulk batteries aim for higher energy density in larger applications. Similarly, the categorization by electrolyte type—polymer, sulfide, oxide, or hybrid—reflects the ongoing material science race to find the optimal balance between ionic conductivity, stability, and cost. Each segment carries distinct market dynamics, regulatory considerations, and competitive landscapes, making a comprehensive segmentation analysis indispensable for informed decision-making within this transformative industry.

- By Battery Type:

- Thin-Film All Solid State Battery

- Bulk All Solid State Battery

- By Electrolyte Type:

- Polymer Solid Electrolyte

- Sulfide Solid Electrolyte

- Oxide Solid Electrolyte

- Hybrid Solid Electrolyte

- By Application:

- Electric Vehicles (EVs)

- Consumer Electronics

- Aerospace & Defense

- Medical Devices

- Grid Energy Storage

- Industrial

- By Capacity:

- Below 20 mAh

- 20-500 mAh

- Above 500 mAh

- By Power Output:

- Below 20W

- 20-100W

- Above 100W

Regional Highlights

The global All Solid State Lithium Battery market exhibits distinct regional dynamics, influenced by varying levels of technological advancement, investment in R&D, manufacturing capabilities, and regulatory support for electric mobility and advanced energy storage. Asia Pacific, particularly countries like China, Japan, and South Korea, is expected to dominate the market. This region boasts a robust ecosystem of battery manufacturers, significant government backing for EV adoption and battery innovation, and a strong presence in consumer electronics manufacturing, driving both supply and demand for advanced battery technologies. Japan, in particular, has been a pioneer in solid-state battery research, with major automotive and electronics companies leading the charge in development and patenting. China's sheer scale of EV production and ambitious electrification targets further solidify its position as a key growth engine for all solid state batteries, focusing on both domestic production and global market share.

North America and Europe represent other significant and rapidly growing markets for All Solid State Lithium Batteries. These regions are characterized by substantial investments in electric vehicle infrastructure, stringent environmental regulations, and a strong emphasis on energy independence and sustainable technologies. The United States and Germany, for instance, are home to numerous startups and established automotive giants actively collaborating with battery developers to integrate solid-state technology into future EV models. Government initiatives and funding programs aimed at boosting domestic battery production and research further stimulate market growth in these regions. While Latin America, the Middle East, and Africa are currently nascent markets, they hold long-term potential as their respective economies develop and as investments in renewable energy and electric transportation infrastructure expand. The global race to commercialize all solid state batteries is intensely regional, with strategic alliances and technological breakthroughs often originating from these key innovation hubs.

- Asia Pacific: Dominant region driven by extensive manufacturing capabilities, strong government support for EVs, and pioneering R&D in Japan, South Korea, and China. High demand from consumer electronics andautomotive sectors.

- North America: Significant growth propelled by increasing EV adoption, substantial R&D investments, and strategic partnerships between tech companies and automotive OEMs. Focus on advanced battery technology for national security and economic competitiveness.

- Europe: Rapid expansion fueled by ambitious decarbonization goals, stringent emission standards, and robust investment in battery gigafactories. Germany, France, and the UK are key players, driving both innovation and integration into their automotive industries.

- Latin America & Middle East and Africa (MEA): Emerging markets with long-term growth potential, contingent on infrastructure development, renewable energy initiatives, and increasing adoption of electric vehicles. Early-stage investments in sustainable technologies are gradually creating opportunities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the All Solid State Lithium Battery Market.- Toyota

- Samsung SDI

- LG Energy Solution

- Solid Power

- QuantumScape

- SK On

- Panasonic

- CATL

- Ilika

- Factorial Energy

- StoreDot

- ProLogium

- Honda

- BMW

- Ford

- Hyundai

- Nio

- Contemporary Amperex Technology Co. Limited

- Northvolt

- Blue Solutions (Bolloré)

Frequently Asked Questions

What are All Solid State Lithium Batteries?

All Solid State Lithium Batteries (ASSLBs) are a type of battery technology that utilizes a solid electrolyte instead of a liquid or polymer gel electrolyte, typically found in conventional lithium-ion batteries. This fundamental change enhances safety by eliminating flammable components and promises higher energy density, faster charging capabilities, and a longer lifespan.

Why are All Solid State Batteries considered safer than traditional lithium-ion batteries?

All Solid State Batteries are considered safer because they replace the flammable liquid organic electrolyte with a non-flammable solid material. This significantly reduces the risk of thermal runaway, overheating, and fire incidents that can occur with traditional lithium-ion batteries, especially during overcharging or physical damage.

When are All Solid State Lithium Batteries expected to be commercially available for electric vehicles?

While some niche applications may see earlier adoption, widespread commercial availability of All Solid State Lithium Batteries for mainstream electric vehicles is generally anticipated in the late 2020s to early 2030s. Several leading automotive manufacturers and battery developers are targeting this timeframe, with initial deployments expected in premium or specialized EV models.

What are the primary challenges in the development and commercialization of All Solid State Batteries?

Key challenges include high manufacturing costs, complexities in scaling up production, achieving stable and low-resistance interfaces between the solid electrolyte and electrodes, suppressing lithium dendrite formation, and ensuring long-term cyclability and performance across a wide range of temperatures. Material science and engineering innovations are crucial to overcome these hurdles.

Which applications will benefit most from All Solid State Lithium Batteries?

Electric vehicles (EVs) are expected to be the largest beneficiary due to the demand for longer range, faster charging, and enhanced safety. Other high-value applications include consumer electronics requiring smaller, safer, and higher-density batteries, as well as aerospace, medical devices, and grid energy storage, where reliability and extended operational life are paramount.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted