Aircraft Positioning system Market

Aircraft Positioning system Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700578 | Last Updated : July 25, 2025 |

Format : ![]()

![]()

![]()

![]()

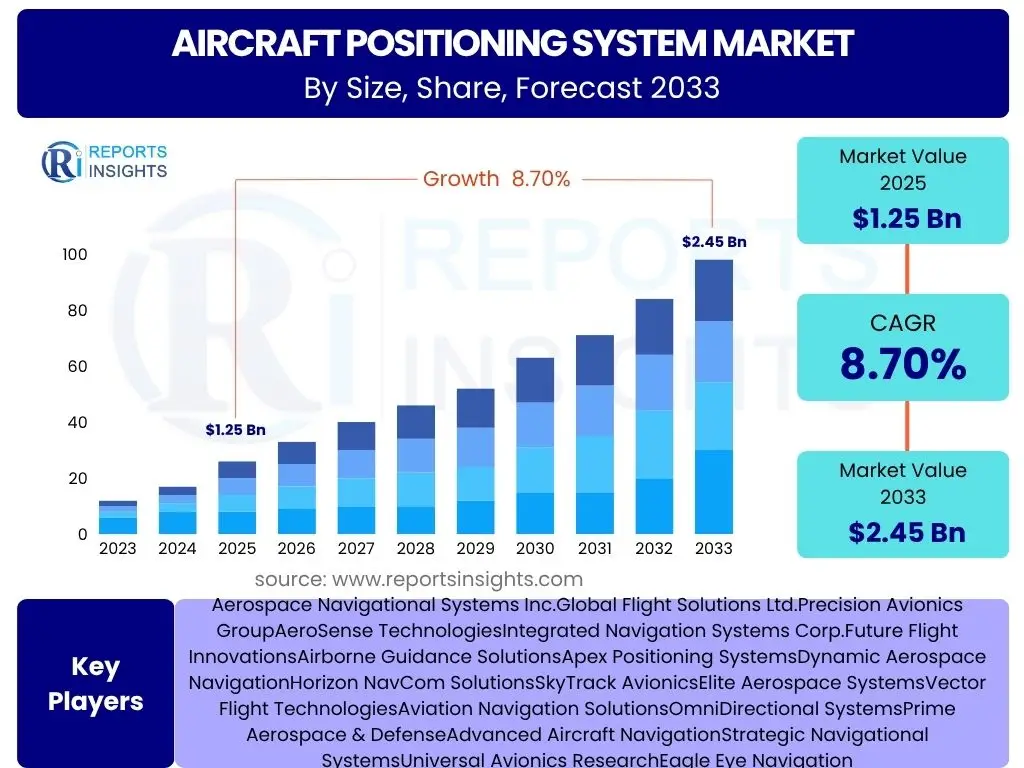

Aircraft Positioning system Market Size

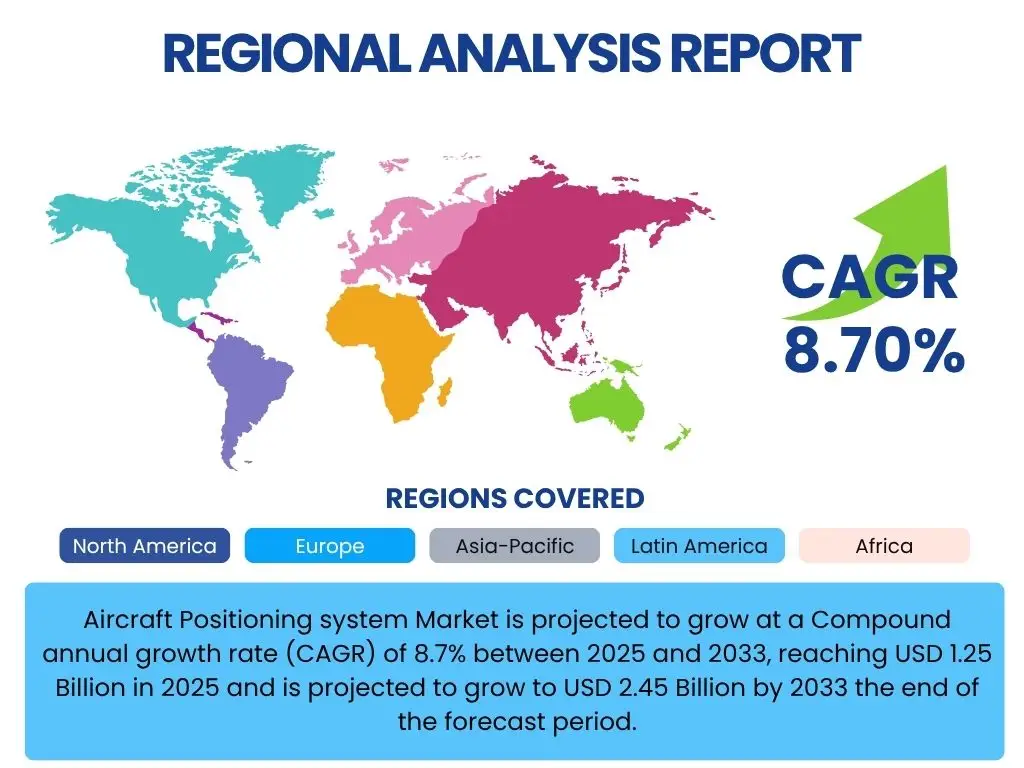

Aircraft Positioning system Market is projected to grow at a Compound annual growth rate (CAGR) of 8.7% between 2025 and 2033, reaching USD 1.25 Billion in 2025 and is projected to grow to USD 2.45 Billion by 2033 the end of the forecast period.

Key Aircraft Positioning system Market Trends & Insights

The Aircraft Positioning System Market is experiencing dynamic shifts driven by advancements in navigation technologies, increasing air traffic, and stringent safety regulations. Key trends include the widespread adoption of Global Navigation Satellite System (GNSS) integration, a growing emphasis on precision landing systems, and the development of sophisticated inertial navigation solutions. The market is also seeing a surge in demand for miniaturized and highly accurate positioning units for unmanned aerial vehicles (UAVs) and urban air mobility (UAM) platforms. Furthermore, the incorporation of artificial intelligence and machine learning for enhanced data processing and predictive maintenance is becoming a significant trend, alongside the push for real-time tracking and connectivity across global airspace.

- Integration of advanced GNSS technologies for enhanced accuracy.

- Miniaturization and lightweight design of positioning systems for UAVs.

- Increased focus on precision approach and landing systems.

- Emergence of AI and machine learning for predictive navigation.

- Development of resilient navigation systems to counter GPS jamming.

- Growth in demand for autonomous flight capabilities.

- Evolution of communication and data link technologies for real-time updates.

- Adoption of sensor fusion for improved positional integrity.

AI Impact Analysis on Aircraft Positioning system

Artificial Intelligence (AI) is set to profoundly transform the Aircraft Positioning System Market by enhancing precision, reliability, and autonomy. AI algorithms can process vast amounts of data from various sensors, including GNSS, inertial measurement units (IMUs), and vision systems, to provide more accurate and robust positional information, even in challenging environments where traditional GPS signals might be compromised. This capability is crucial for future autonomous aircraft and urban air mobility operations, where precise navigation without human intervention is paramount. AI also facilitates predictive maintenance of positioning system components, reducing downtime and improving operational efficiency, while enabling adaptive navigation and dynamic route optimization based on real-time environmental data and traffic conditions.

- Enhanced data fusion from multiple sensors for superior accuracy.

- Predictive analytics for system maintenance and failure prevention.

- Adaptive navigation and real-time route optimization.

- Improved resilience against signal interference and spoofing.

- Facilitation of autonomous flight capabilities through intelligent decision-making.

- Development of advanced anomaly detection in navigation data.

Key Takeaways Aircraft Positioning system Market Size & Forecast

- The Aircraft Positioning System Market is poised for significant growth, projected to nearly double its valuation by 2033.

- Strong market expansion is driven by increasing air travel, stringent safety regulations, and technological advancements.

- The integration of Global Navigation Satellite Systems (GNSS) and Inertial Navigation Systems (INS) is crucial for precision and redundancy.

- Emerging technologies like AI and machine learning are enhancing system accuracy and resilience.

- Demand from commercial aviation, military aircraft, and the rapidly growing Unmanned Aerial Vehicle (UAV) sector is propelling market growth.

- North America and Asia Pacific are anticipated to be dominant regions due to high aviation activity and defense investments.

Aircraft Positioning system Market Drivers Analysis

The Aircraft Positioning System Market is propelled by a confluence of critical factors, each contributing significantly to its expansion and technological evolution. The escalating volume of air traffic globally necessitates more precise and reliable navigation solutions to ensure airspace efficiency and safety. Furthermore, the continuous modernization of existing aircraft fleets and the procurement of new, advanced aircraft, particularly those equipped for autonomous operations, are driving the integration of cutting-edge positioning technologies. Stricter regulatory mandates for air safety and navigation accuracy, imposed by aviation authorities worldwide, also compel airlines and aircraft manufacturers to adopt sophisticated positioning systems. The burgeoning Unmanned Aerial Vehicle (UAV) and Urban Air Mobility (UAM) sectors present new demands for miniaturized, highly accurate, and resilient positioning solutions, further fueling market growth. Finally, ongoing advancements in sensor technology and data processing capabilities are continuously enhancing the performance and reliability of these systems, making them indispensable for modern aviation.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Air Traffic and Demand for Air Travel: The continuous growth in commercial and passenger air travel globally necessitates more efficient and accurate air traffic management, directly increasing the demand for advanced positioning systems to ensure safety and optimize flight paths. | +2.1% | Mid to Long-term | |

| Strict Aviation Safety Regulations and Standards: Global aviation authorities are continuously imposing stringent regulations and standards for navigation accuracy, redundancy, and reliability, compelling airlines and manufacturers to invest in state-of-the-art positioning technologies. | +1.8% | Short to Mid-term | |

| Modernization of Aircraft Fleets and New Aircraft Deliveries: The replacement of aging aircraft with new, technologically advanced models that integrate sophisticated navigation and positioning systems, along with the consistent delivery of new aircraft, drives market demand. | +1.9% | Mid to Long-term | |

| Growth of Unmanned Aerial Vehicles (UAVs) and Urban Air Mobility (UAM): The rapid expansion of UAV applications across various industries and the emerging concept of UAM require highly precise, compact, and resilient positioning systems for autonomous operation. | +2.3% | Mid to Long-term | |

| Technological Advancements in GNSS and INS: Continuous innovations in Global Navigation Satellite Systems (GNSS) like GPS, GLONASS, Galileo, and BeiDou, coupled with advancements in Inertial Navigation Systems (INS), offer improved accuracy, resilience, and integration capabilities. | +1.5% | Short to Mid-term |

Aircraft Positioning system Market Restraints Analysis

Despite the robust growth drivers, the Aircraft Positioning System Market faces several significant restraints that could impede its full potential. The high upfront cost associated with acquiring and integrating advanced positioning systems, especially for smaller airlines or private aircraft owners, presents a considerable barrier. These systems often involve complex hardware, specialized software, and extensive calibration, contributing to elevated installation expenses. Furthermore, the inherent technical complexities of these systems, including the need for constant updates, recalibrations, and specialized maintenance, add to the operational burden. Cybersecurity threats, particularly to GNSS signals and data links, pose a persistent challenge, requiring continuous investment in robust security measures. Lastly, regulatory hurdles and the slow pace of standardization across different regions can delay the adoption of new technologies, impacting market expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Maintenance Costs: The significant capital outlay required for purchasing and installing advanced positioning systems, coupled with ongoing maintenance, calibration, and software update expenses, can be a deterrent, especially for smaller operators. | -1.5% | Short to Mid-term | |

| Technical Complexities and Integration Challenges: Integrating highly sophisticated positioning systems with legacy aircraft avionics and ensuring seamless interoperability across diverse platforms can be technically challenging and time-consuming, requiring specialized expertise. | -1.2% | Short to Mid-term | |

| Vulnerability to Cyber Threats and Signal Interference: Aircraft positioning systems, especially those relying on GNSS, are susceptible to jamming, spoofing, and other cyber-attacks, which can compromise navigation accuracy and aircraft safety, necessitating continuous investment in security measures. | -1.8% | Long-term | |

| Stringent Certification Processes and Regulatory Hurdles: The rigorous and lengthy certification processes required for new aviation technologies, particularly navigation systems, can delay market entry and widespread adoption of innovative solutions. | -1.0% | Mid to Long-term |

Aircraft Positioning system Market Opportunities Analysis

The Aircraft Positioning System Market is ripe with compelling opportunities for growth and innovation, driven by evolving aviation paradigms and technological breakthroughs. The burgeoning Unmanned Aerial Vehicle (UAV) market, spanning defense, commercial, and consumer applications, presents a vast and untapped segment demanding specialized, miniaturized, and highly accurate positioning solutions. Similarly, the nascent Urban Air Mobility (UAM) sector, envisioning air taxis and drone deliveries in urban environments, will require extremely precise and resilient navigation capabilities for safe and autonomous operation. Advancements in sensor technology, including sophisticated inertial sensors and LiDAR, along with the proliferation of satellite constellations, offer avenues for developing more robust and redundant positioning systems. Furthermore, the potential for data monetization through real-time positional data and the growth in military modernization programs worldwide provide additional revenue streams and significant market expansion prospects.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of the Unmanned Aerial Vehicle (UAV) Market: The increasing adoption of drones across various sectors, from defense and surveillance to logistics and agriculture, creates a significant demand for compact, lightweight, and highly accurate positioning systems for autonomous flight. | +2.5% | Mid to Long-term | |

| Emergence of Urban Air Mobility (UAM) and Autonomous Aircraft: The development of air taxis, cargo drones, and other UAM platforms necessitates hyper-accurate and resilient positioning systems to ensure safe and efficient operation in complex urban airspace. | +2.2% | Long-term | |

| Advancements in Sensor Fusion and Multi-Constellation GNSS Receivers: The integration of diverse sensor data (e.g., IMU, vision, LiDAR) with signals from multiple GNSS constellations enhances accuracy, robustness, and redundancy, opening new product development avenues. | +1.7% | Short to Mid-term | |

| Growth in Military Modernization and Defense Spending: Increased defense budgets globally, focused on upgrading military aircraft with advanced navigation and targeting systems, present a lucrative opportunity for manufacturers of high-precision positioning solutions. | +1.9% | Mid to Long-term | |

| Demand for Data Monetization and Value-Added Services: The ability to collect and analyze precise positional data from aircraft can lead to new business models, offering value-added services such as predictive analytics for air traffic, fleet management optimization, and enhanced logistics. | +1.0% | Long-term |

Aircraft Positioning system Market Challenges Impact Analysis

The Aircraft Positioning System Market faces a unique set of challenges that require continuous innovation and strategic responses from industry players. One of the primary concerns is the vulnerability to Global Navigation Satellite System (GNSS) signal degradation, jamming, and spoofing, which can severely compromise navigational integrity and necessitate robust backup systems. The rapid pace of technological change often leads to issues of interoperability between new and legacy systems, creating complex integration hurdles for existing aircraft fleets. Furthermore, the global shortage of skilled aerospace engineers and technicians proficient in advanced navigation systems poses a significant constraint on research, development, and maintenance efforts. The high costs associated with research and development for next-generation, more resilient positioning technologies, coupled with the long certification cycles, further complicate market dynamics. Lastly, geopolitical tensions and trade restrictions can disrupt supply chains and hinder the global deployment of advanced positioning solutions, impacting market growth and stability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| GNSS Signal Vulnerabilities (Jamming/Spoofing): The reliance on GNSS signals makes positioning systems susceptible to intentional or unintentional interference, jamming, and spoofing, which can severely degrade accuracy and safety, demanding robust anti-jamming and anti-spoofing measures. | -1.7% | Ongoing | |

| Interoperability and Standardization Issues: Ensuring seamless communication and data exchange between diverse positioning systems, avionics, and air traffic control infrastructure from different manufacturers and generations remains a complex challenge, hindering broader adoption. | -1.1% | Mid-term | |

| Shortage of Skilled Workforce: A deficit of highly specialized engineers and technicians with expertise in advanced navigation systems, AI integration, and cybersecurity for aviation poses a challenge for innovation, deployment, and maintenance. | -0.8% | Long-term | |

| High Research & Development (R&D) Costs and Long Product Cycles: Developing cutting-edge, highly resilient, and certified positioning systems requires substantial R&D investments and lengthy product development and certification timelines, impacting market responsiveness. | -0.9% | Mid to Long-term | |

| Geopolitical Tensions and Supply Chain Disruptions: Global political instability, trade disputes, and supply chain vulnerabilities can affect the availability of critical components and raw materials, impacting production and delivery schedules for positioning systems. | -1.4% | Short to Mid-term |

Aircraft Positioning system Market - Updated Report Scope

The updated report scope for the Aircraft Positioning System Market provides a comprehensive overview of the industry's historical performance, current landscape, and future projections. It delves into critical market attributes, offering detailed insights into market sizing, growth rates, and key trends that are shaping the competitive environment. The report also meticulously segments the market by various parameters, providing granular analysis of each component, technology, application, and aircraft type. Furthermore, it identifies and profiles the leading industry players, offering a strategic understanding of their market presence, product portfolios, and competitive strategies across major geographical regions. This exhaustive scope ensures that stakeholders gain actionable intelligence for informed decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 2.45 Billion |

| Growth Rate | 8.7% CAGR from 2025 to 2033 |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Aerospace Navigational Systems Inc. Global Flight Solutions Ltd. Precision Avionics Group AeroSense Technologies Integrated Navigation Systems Corp. Future Flight Innovations Airborne Guidance Solutions Apex Positioning Systems Dynamic Aerospace Navigation Horizon NavCom Solutions SkyTrack Avionics Elite Aerospace Systems Vector Flight Technologies Aviation Navigation Solutions OmniDirectional Systems Prime Aerospace & Defense Advanced Aircraft Navigation Strategic Navigational Systems Universal Avionics Research Eagle Eye Navigation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Aircraft Positioning System Market is comprehensively segmented to provide granular insights into its various dimensions, enabling stakeholders to understand the market's structure and identify specific growth areas. This segmentation helps in analyzing market dynamics across different technologies, components, applications, and aircraft types, reflecting the diverse needs of the aviation industry. Each segment plays a crucial role in the overall market landscape, driven by unique factors and contributing to the market's trajectory. Understanding these segments is vital for strategic planning, product development, and market penetration, ensuring that businesses can tailor their offerings to specific industry requirements and capitalize on emerging opportunities.By Component: This segment differentiates the market based on the physical and software elements that constitute an aircraft positioning system. Each component category serves a distinct function, contributing to the overall accuracy, reliability, and functionality of the system. Understanding the demand and technological advancements within each component is crucial for manufacturers and integrators to innovate and optimize their offerings, ensuring seamless interoperability and robust performance.

- Hardware:

- Receivers

- Antennas

- Inertial Measurement Units (IMUs)

- Processors

- Sensors

- Displays

- Software:

- Navigation Software

- Data Processing Software

- Interface Software

- Services:

- Integration

- Maintenance

- Upgrades

- Training

By Technology: This segment categorizes positioning systems based on the underlying technological principles they employ for navigation. The market sees a mix of established and emerging technologies, each offering unique advantages in terms of accuracy, resilience, and operational capabilities. The interplay between these technologies, especially the development of hybrid systems, is a key driver for enhanced performance and reliability in diverse operational environments, addressing challenges such as signal degradation and loss.

- Global Navigation Satellite System (GNSS):

- GPS

- GLONASS

- Galileo

- BeiDou

- Inertial Navigation System (INS):

- Ring Laser Gyro (RLG)

- Fiber Optic Gyro (FOG)

- MEMS Gyro

- Hybrid Systems

- Ground-Based Augmentation Systems (GBAS)

- Satellite-Based Augmentation Systems (SBAS)

By Application: The market for aircraft positioning systems is also segmented by their specific operational uses across the aviation domain. Each application demands varying levels of precision, reliability, and functionality, tailoring the design and integration of positioning technologies. From ensuring safe flight paths and accurate mapping to aiding in search and rescue missions and optimizing fleet operations, the diversity of applications underscores the indispensable role of these systems in modern aviation.

- Navigation & Guidance

- Mapping & Surveying

- Surveillance

- Search & Rescue

- Precision Landing

- Fleet Management

By Aircraft Type: This segmentation focuses on the different categories of aircraft that utilize positioning systems, highlighting the varying requirements and market demand across commercial, military, and general aviation sectors. The specific design, size, and operational environment of each aircraft type influence the choice and configuration of positioning systems, driving tailored solutions for performance, weight, and integration complexity.

- Commercial Aircraft:

- Narrow-body

- Wide-body

- Regional Jets

- Military Aircraft:

- Fighter Jets

- Transport Aircraft

- Helicopters

- Special Mission Aircraft

- Unmanned Aerial Vehicles (UAVs):

- Fixed-wing UAVs

- Rotary-wing UAVs

- General Aviation Aircraft

Regional Highlights

The Aircraft Positioning System Market demonstrates distinct characteristics and growth patterns across key geographical regions, driven by factors such as aviation infrastructure development, defense spending, technological adoption, and air traffic volume. Each region presents a unique landscape of opportunities and challenges for market participants.North America stands as a dominant region in the Aircraft Positioning System Market, primarily due to the presence of major aircraft manufacturers, a robust defense sector, and significant investments in advanced aerospace technologies. The United States and Canada are at the forefront of adopting cutting-edge navigation solutions, driven by their extensive aviation infrastructure, high volume of commercial air traffic, and ongoing modernization of military fleets. The region's emphasis on aviation safety standards, coupled with pioneering research and development in autonomous flight and Urban Air Mobility (UAM), further fuels the demand for highly precise and resilient positioning systems. Government initiatives and defense contracts also play a crucial role in market growth, fostering innovation and technological advancements in the sector.

Europe represents another significant market for aircraft positioning systems, characterized by its mature aviation industry and stringent regulatory environment. Countries like the United Kingdom, Germany, France, and Italy are key contributors, driven by their established aerospace manufacturing capabilities and continued investment in commercial and military aviation. The region's commitment to enhancing air traffic management systems and integrating next-generation navigation technologies like Galileo (Europe's GNSS) boosts market demand. Additionally, European research initiatives focused on advanced avionics, low-altitude airspace management for drones, and future air mobility concepts create a strong ecosystem for the adoption and development of sophisticated positioning solutions. The emphasis on interoperability and standardization across European airspace also contributes to the consistent demand for upgraded systems.

Asia Pacific (APAC) is projected to be the fastest-growing region in the Aircraft Positioning System Market, propelled by the rapid expansion of its commercial aviation sector, increasing passenger traffic, and significant investments in airport infrastructure. Countries such as China, India, Japan, and Australia are witnessing a surge in new aircraft procurements and fleet modernization programs to cater to the escalating demand for air travel. The growing defense budgets in several APAC nations, aimed at enhancing military capabilities and surveillance, also contribute substantially to the market. Furthermore, the burgeoning manufacturing base in countries like China, coupled with their focus on developing indigenous aerospace technologies and Unmanned Aerial Vehicles (UAVs), positions APAC as a high-potential market for future growth. The region's willingness to adopt new technologies rapidly drives the demand for advanced and integrated positioning systems.

Latin America is expected to exhibit steady growth in the Aircraft Positioning System Market, driven by increasing investments in aviation infrastructure and fleet modernization across countries like Brazil, Mexico, and Argentina. While not as large as North America or APAC, the region's expanding commercial aviation sector, coupled with ongoing efforts to enhance air safety and efficiency, creates a consistent demand for reliable positioning systems. Military modernization programs, though smaller in scale, also contribute to market uptake. The focus is often on upgrading existing aircraft with more cost-effective yet robust navigation solutions.

Middle East and Africa (MEA) represents a developing but promising market for aircraft positioning systems. The Middle East, in particular, is witnessing substantial investments in its aviation sector, including the development of new airports and the expansion of national carriers, leading to a demand for advanced aircraft and associated navigation technologies. Countries like UAE, Saudi Arabia, and Qatar are key players, driven by their strategic geographical location and ambitious aviation hubs. In Africa, while the market is still nascent, increasing air travel, coupled with a focus on improving aviation safety and connectivity, is gradually driving the adoption of modern positioning systems, especially in key economic hubs and for military applications.

Top Key Players:

The market research report covers the analysis of key stake holders of the Aircraft Positioning system Market. Some of the leading players profiled in the report include -

- Aerospace Navigational Systems Inc.

- Global Flight Solutions Ltd.

- Precision Avionics Group

- AeroSense Technologies

- Integrated Navigation Systems Corp.

- Future Flight Innovations

- Airborne Guidance Solutions

- Apex Positioning Systems

- Dynamic Aerospace Navigation

- Horizon NavCom Solutions

- SkyTrack Avionics

- Elite Aerospace Systems

- Vector Flight Technologies

- Aviation Navigation Solutions

- OmniDirectional Systems

- Prime Aerospace & Defense

- Advanced Aircraft Navigation

- Strategic Navigational Systems

- Universal Avionics Research

- Eagle Eye Navigation

Frequently Asked Questions:

What is an Aircraft Positioning System?

An Aircraft Positioning System is a sophisticated suite of technologies and sensors designed to precisely determine an aircraft's location, velocity, and orientation in three-dimensional space. It utilizes various methods, including satellite-based navigation (like GPS), inertial navigation, and ground-based aids, to provide highly accurate real-time positional data crucial for flight navigation, air traffic control, and safe operation.

What is the projected growth rate for the Aircraft Positioning System Market?

The Aircraft Positioning System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. This growth is driven by increasing air traffic, stringent safety regulations, and continuous advancements in navigation technologies across commercial, military, and emerging aviation sectors.

What are the key technologies used in Aircraft Positioning Systems?

Key technologies commonly employed in Aircraft Positioning Systems include Global Navigation Satellite Systems (GNSS) such as GPS, GLONASS, Galileo, and BeiDou, which provide satellite-derived position information. Inertial Navigation Systems (INS), comprising gyroscopes and accelerometers, offer autonomous positioning by measuring motion. Hybrid systems combine GNSS and INS for enhanced accuracy and redundancy, while Ground-Based Augmentation Systems (GBAS) and Satellite-Based Augmentation Systems (SBAS) improve GNSS precision.

How is AI impacting the Aircraft Positioning System Market?

Artificial Intelligence (AI) is significantly impacting the Aircraft Positioning System Market by enabling more accurate data fusion from multiple sensors, providing predictive maintenance insights, and facilitating adaptive navigation. AI algorithms enhance resilience against signal interference, improve anomaly detection, and are crucial for the development of fully autonomous flight capabilities, leading to safer and more efficient air operations.

Which regions are key contributors to the Aircraft Positioning System Market?

North America and Asia Pacific are the dominant regions in the Aircraft Positioning System Market. North America benefits from a strong aerospace industry and significant defense spending, while Asia Pacific is driven by rapid growth in commercial aviation and increasing investments in new aircraft and infrastructure. Europe also holds a substantial market share due to its mature aviation sector and focus on advanced navigation technologies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted