Aircraft Passenger Seat Market

Aircraft Passenger Seat Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706909 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

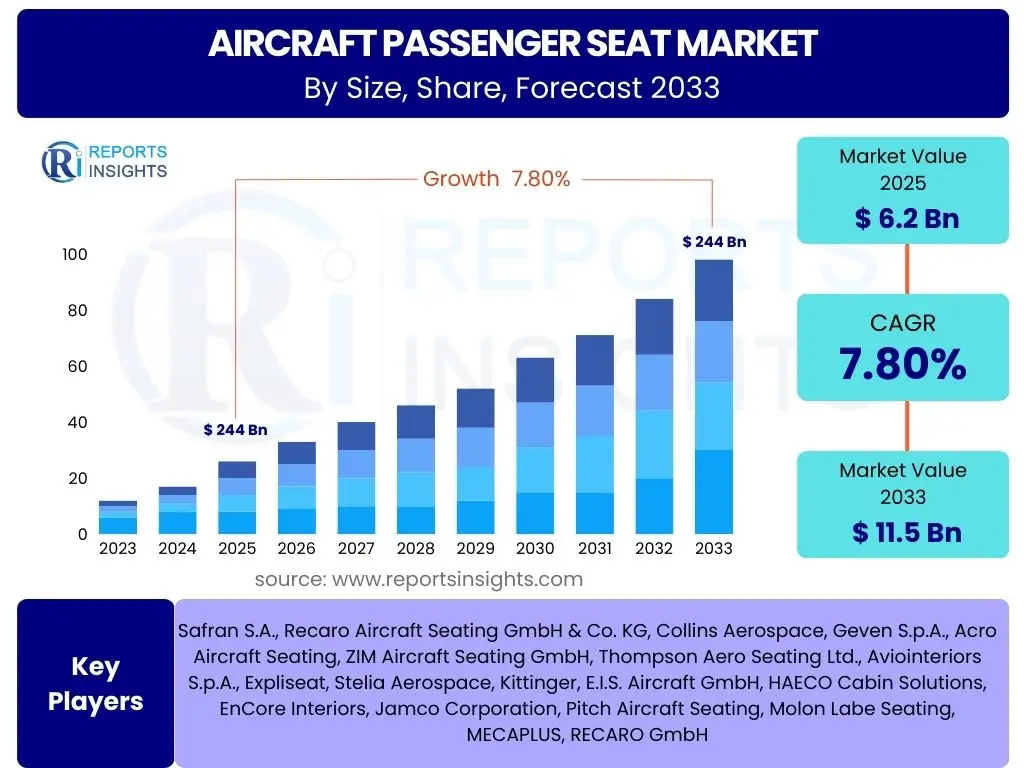

Aircraft Passenger Seat Market Size

According to Reports Insights Consulting Pvt Ltd, The Aircraft Passenger Seat Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 6.2 Billion in 2025 and is projected to reach USD 11.5 Billion by the end of the forecast period in 2033.

Key Aircraft Passenger Seat Market Trends & Insights

The aircraft passenger seat market is undergoing a significant transformation driven by a dual focus on enhancing passenger experience and achieving greater operational efficiencies for airlines. Common user questions often revolve around how manufacturers are balancing the need for increased comfort and advanced in-flight entertainment systems with the critical requirement for lightweighting to reduce fuel consumption and operational costs. This dynamic environment is fostering innovation in material science, design aesthetics, and intelligent cabin solutions.

Current trends indicate a strong emphasis on modular and customizable seating solutions, allowing airlines to quickly reconfigure cabins to meet evolving passenger demands or optimize for specific routes. Furthermore, there is a growing push towards integrating smart technologies within seats, such as advanced connectivity options and ergonomic adjustments, to provide a more personalized and interactive travel experience. Sustainability is also emerging as a pivotal trend, with increasing research and development into eco-friendly materials and manufacturing processes to reduce the environmental footprint of cabin interiors.

- Lightweighting initiatives through advanced composite materials and innovative design structures.

- Integration of advanced In-Flight Entertainment and Connectivity (IFEC) systems for enhanced passenger engagement.

- Increased demand for modular and customizable seat designs to optimize cabin space and airline branding.

- Focus on enhanced passenger comfort, including ergonomic designs, greater recline, and improved lumbar support.

- Development and adoption of sustainable and recyclable materials for seat components.

- Growth in premium economy and business class seating, reflecting passenger willingness to pay for added comfort.

- Implementation of touchless technologies and enhanced hygiene features in response to health concerns.

AI Impact Analysis on Aircraft Passenger Seat

Common user questions related to the impact of Artificial Intelligence (AI) on aircraft passenger seats frequently explore how this technology can revolutionize both the manufacturing process and the in-flight experience. Users are keen to understand how AI can lead to more efficient production, personalized cabin environments, and predictive maintenance capabilities, thereby addressing concerns about operational costs and passenger satisfaction. The integration of AI is seen as a pathway to smarter, more adaptive cabin interiors.

AI's influence extends across several facets of the aircraft passenger seat market, from optimizing the design and engineering phases to improving post-sales support and maintenance. Predictive analytics, powered by AI, can anticipate wear and tear on seat components, enabling proactive maintenance and reducing aircraft downtime. Moreover, AI can facilitate highly personalized cabin experiences, adjusting lighting, temperature, and entertainment options based on individual passenger preferences, potentially enhancing comfort and satisfaction. In manufacturing, AI-driven robotics and quality control systems are improving precision and efficiency, leading to higher quality products and reduced waste.

- Predictive maintenance for seat components, enhancing safety and reducing maintenance downtime.

- AI-driven optimization of seat design for weight reduction, ergonomics, and structural integrity.

- Personalized in-flight entertainment and climate control based on passenger preferences and behavior.

- Automated quality control and inspection during the seat manufacturing process using computer vision and AI.

- Supply chain optimization for seat components, improving inventory management and logistics through AI analytics.

- AI-powered demand forecasting for seat types and configurations, assisting airlines in fleet planning.

- Development of smart seats that adapt to passenger posture and provide real-time comfort adjustments.

Key Takeaways Aircraft Passenger Seat Market Size & Forecast

User inquiries about the key takeaways from the Aircraft Passenger Seat market size and forecast consistently highlight the market's resilience and its deep connection to the broader aviation industry's health. The insights reveal that despite past challenges, sustained growth is anticipated, driven by global fleet expansion, the robust demand for air travel, and continuous innovation in seat design. A significant takeaway is the strategic shift towards solutions that balance passenger comfort with airline operational imperatives.

The forecast indicates a promising trajectory, with a notable emphasis on specific segments such as premium economy and business class, which are increasingly seen as revenue drivers for airlines. Furthermore, the aftermarket segment, encompassing maintenance, repair, and overhaul (MRO) services, is identified as a critical growth area, reflecting the long lifecycle of aircraft and the ongoing need for seat refurbishment and upgrades. Geographically, Asia-Pacific is positioned as a powerhouse, fueled by rapid urbanization and the expansion of air travel networks.

- Market growth is robust, driven by global air passenger traffic recovery and fleet modernization efforts.

- Technological advancements in lightweight materials and smart cabin features are pivotal for innovation.

- The aftermarket segment, particularly MRO and retrofitting, presents significant growth opportunities.

- Increasing focus on premium cabin configurations and customized seating solutions by airlines.

- Asia-Pacific is expected to be a key growth region due to rising disposable incomes and expanding aviation infrastructure.

- Sustainability and enhanced hygiene features are becoming increasingly important considerations in seat design.

Aircraft Passenger Seat Market Drivers Analysis

The global aircraft passenger seat market is significantly propelled by a confluence of factors reflecting the dynamic nature of the aviation industry. A primary driver is the consistent increase in global air passenger traffic, which necessitates the expansion and modernization of airline fleets. As more people travel by air, airlines respond by acquiring new aircraft and upgrading existing ones, directly stimulating demand for new and refurbished passenger seats.

Another crucial driver is the ongoing trend of fleet modernization and replacement by airlines worldwide. Older, less fuel-efficient aircraft are being phased out in favor of newer models that offer enhanced operational efficiency and passenger comfort. This transition involves significant investments in cabin interiors, including advanced seating solutions. Furthermore, the rising demand for premium cabin experiences, such as business and first-class seating, as well as the rapidly growing premium economy segment, encourages airlines to invest in higher-value, feature-rich seats, thereby increasing market value.

Technological advancements in seat design and materials also serve as potent drivers. Innovations in lightweight composite materials, ergonomic designs, and integrated in-flight entertainment and connectivity (IFEC) systems enhance passenger comfort while contributing to fuel efficiency, a critical factor for airlines. Moreover, the expansion of low-cost carriers (LCCs) in emerging markets, coupled with their specific requirements for durable, high-density seating, adds another layer of demand to the market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Air Passenger Traffic Growth | +2.3% | Global | Medium-to-Long Term (2025-2033) |

| Fleet Modernization and Expansion | +1.8% | North America, Asia-Pacific, Europe | Short-to-Medium Term (2025-2029) |

| Rising Demand for Premium Cabins | +1.5% | Global, particularly North America, Europe, Asia-Pacific | Medium-to-Long Term (2025-2033) |

| Advancements in Seat Technology and Materials | +1.2% | Global | Ongoing |

Aircraft Passenger Seat Market Restraints Analysis

Despite the positive growth trajectory, the aircraft passenger seat market faces several significant restraints that could impede its expansion. One of the most prominent is the high cost associated with research and development, manufacturing, and obtaining certifications for new seat designs. The stringent safety and airworthiness regulations imposed by aviation authorities globally, such as the FAA and EASA, necessitate extensive testing and compliance procedures, adding considerable expense and time to product development cycles.

Another key restraint is the inherent volatility of raw material prices, particularly for advanced composites and specialized alloys used in seat construction. Fluctuations in the global supply chain, geopolitical tensions, and economic downturns can lead to unpredictable material costs, impacting manufacturers' profit margins and potentially increasing the final price of seats for airlines. This economic sensitivity makes long-term planning and investment more challenging for market participants.

Furthermore, the long product lifecycle of aircraft, combined with airlines' cautious investment strategies due to tight profit margins, can slow down the adoption of new seat technologies. Airlines often prioritize the refurbishment and repair of existing seats over the procurement of entirely new ones, especially during periods of economic uncertainty. This can limit the opportunities for new seat sales, pushing manufacturers to focus more on the aftermarket segment, which, while lucrative, has different dynamics than initial OEM installations.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Certification Costs and Stringent Regulations | -1.1% | Global | Ongoing |

| Fluctuating Raw Material Prices and Supply Chain Vulnerabilities | -0.8% | Global | Short-to-Medium Term (2025-2029) |

| Airline Profitability Pressures and Capital Expenditure Constraints | -0.9% | Global | Medium Term (2025-2030) |

| Long Product Lifecycle of Aircraft and Seat Components | -0.7% | Global | Long Term (2025-2033) |

Aircraft Passenger Seat Market Opportunities Analysis

Despite the challenges, the aircraft passenger seat market is ripe with opportunities that could significantly fuel its growth trajectory. One major avenue for expansion lies in the extensive retrofitting and cabin refurbishment market. As airlines look to extend the operational life of their existing fleets and enhance passenger experience without investing in entirely new aircraft, the demand for modern, upgraded seating solutions for older planes presents a substantial opportunity for manufacturers.

The burgeoning Maintenance, Repair, and Overhaul (MRO) segment for aircraft cabin interiors also offers considerable potential. With a large global fleet, the continuous need for seat repair, re-upholstery, and component replacement ensures a steady revenue stream for seat manufacturers and specialized MRO providers. Furthermore, the growing focus on sustainability within the aviation industry is creating new opportunities for developing and marketing eco-friendly seat materials and designs that align with airlines' environmental objectives and passenger preferences for greener travel.

Beyond retrofitting and MRO, the increasing trend towards customization and personalization of cabin interiors by airlines provides another lucrative niche. Airlines are seeking unique seating configurations and branding elements to differentiate their services, creating demand for bespoke and modular seat designs. Additionally, the rapid urbanization and expansion of regional air connectivity, particularly in emerging markets, will necessitate new aircraft and, consequently, new seating solutions for shorter-haul flights, opening new geographical markets for seat suppliers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Aircraft Retrofitting and Cabin Modernization Programs | +1.9% | North America, Europe, Asia-Pacific | Medium-to-Long Term (2025-2033) |

| Expansion of MRO Services for Aircraft Seats | +1.7% | Global | Ongoing |

| Development and Adoption of Sustainable Materials | +1.4% | Global | Medium-to-Long Term (2025-2033) |

| Increased Demand for Cabin Customization and Personalization | +1.1% | Global | Short-to-Medium Term (2025-2029) |

Aircraft Passenger Seat Market Challenges Impact Analysis

The aircraft passenger seat market, while dynamic, faces several significant challenges that require strategic navigation from manufacturers and suppliers. One persistent challenge is the intense competition among a relatively small number of established players. This high level of competition often leads to pricing pressures, forcing manufacturers to innovate constantly and differentiate their products through features, quality, and service, which can impact profitability and market share for less agile companies.

Another critical challenge stems from the inherent complexity of the global supply chain for aircraft seat components. Sourcing specialized materials, electronic components, and intricate mechanical parts from diverse international suppliers introduces risks related to logistics delays, quality control, and geopolitical instability. Any disruption in this chain can severely impact production schedules and delivery times, leading to financial penalties and reputational damage for seat manufacturers.

Furthermore, the long design and certification cycles for new aircraft models mean that seat manufacturers must commit significant resources to research and development far in advance of actual order fulfillment. This protracted lead time, coupled with the need for substantial upfront investment in tooling and production facilities, poses a financial risk, particularly if aircraft orders are delayed or cancelled. The need to balance innovation with financial prudence and production efficiency remains a continuous challenge in this capital-intensive industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition Among Key Players | -1.2% | Global | Ongoing |

| Complex Global Supply Chain Logistics and Disruptions | -0.9% | Global | Short-to-Medium Term (2025-2029) |

| Long Design and Certification Lead Times | -0.8% | Global | Long Term (2025-2033) |

| Skilled Labor Shortages and Talent Retention | -0.6% | North America, Europe | Medium Term (2025-2030) |

Aircraft Passenger Seat Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the Aircraft Passenger Seat Market, providing critical insights into its current state, historical performance, and future projections. The report meticulously details market size, growth rates, key trends, and the impact of various market dynamics such as drivers, restraints, opportunities, and challenges. It further segments the market by aircraft type, seat class, material, end-use, and key features, offering a granular view of market opportunities across diverse segments and geographical regions. The aim is to provide stakeholders with actionable intelligence for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.2 Billion |

| Market Forecast in 2033 | USD 11.5 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 268 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Safran S.A., Recaro Aircraft Seating GmbH & Co. KG, Collins Aerospace, Geven S.p.A., Acro Aircraft Seating, ZIM Aircraft Seating GmbH, Thompson Aero Seating Ltd., Aviointeriors S.p.A., Expliseat, Stelia Aerospace, Kittinger, E.I.S. Aircraft GmbH, HAECO Cabin Solutions, EnCore Interiors, Jamco Corporation, Pitch Aircraft Seating, Molon Labe Seating, MECAPLUS, RECARO GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Aircraft Passenger Seat Market is comprehensively segmented to provide a detailed understanding of its diverse components and drivers. This segmentation allows for a granular analysis of market dynamics, enabling stakeholders to identify specific growth areas and tailor strategies effectively. The key segments are defined by various criteria including the type of aircraft, the class of seating, the materials used in manufacturing, the end-user application, and specific product features.

Each segment offers unique insights into demand patterns and technological requirements. For instance, the demand for wide-body aircraft seats differs significantly from that for regional jets, both in terms of design complexity and volume. Similarly, the material segment reflects ongoing innovation in lightweighting and durability, while the end-use segment highlights the critical balance between original equipment manufacturing (OEM) and the robust aftermarket (MRO) sector, which is vital for sustained market activity and revenue generation.

- By Aircraft Type

- Narrow-body

- Wide-body

- Regional Jet

- Business Jet

- By Seat Class

- Economy Class

- Premium Economy Class

- Business Class

- First Class

- By Material

- Aluminum Alloys

- Composite Materials

- Steel Alloys

- Others

- By End-Use

- OEM (Original Equipment Manufacturer)

- Aftermarket (Maintenance, Repair, and Overhaul)

- By Feature

- Fixed

- Reclining

- Convertible

- Ergonomic

- Smart/Connected

Regional Highlights

- North America: This region holds a significant share of the aircraft passenger seat market, primarily driven by a large existing fleet, a mature aviation industry, and substantial investments in aircraft modernization and MRO activities. The presence of major airlines, aircraft manufacturers, and a strong focus on premium cabin enhancements contribute to its robust market position.

- Europe: Europe represents another key market, characterized by established aviation players and a strong emphasis on innovation in sustainable materials and advanced cabin designs. The region's airlines are consistently investing in fleet renewal and cabin refurbishment to enhance passenger comfort and comply with evolving environmental regulations, driving demand for new seating solutions.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region in the aircraft passenger seat market. This growth is fueled by a rapidly expanding middle class, increasing disposable incomes, and the consequent surge in air passenger traffic. Significant investments in new airport infrastructure and fleet expansion by regional carriers, particularly in countries like China, India, and Southeast Asian nations, are creating immense demand for passenger seats.

- Latin America: This region exhibits steady growth, driven by increasing air connectivity within and between countries, the expansion of low-cost carriers, and ongoing efforts to modernize national fleets. While smaller in market size compared to North America or APAC, the opportunities for market penetration and expansion are notable as air travel becomes more accessible.

- Middle East and Africa (MEA): The MEA region is experiencing growth propelled by the strategic geographic location of its major airlines, which serve as global hubs, and significant investments in fleet expansion to accommodate growing international passenger traffic. The demand for premium and luxurious seating is particularly high in the Middle East, reflecting the focus of regional carriers on high-end travel experiences. Africa's market is emerging, driven by increasing regional connectivity and fleet upgrades.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aircraft Passenger Seat Market.- Safran S.A.

- Recaro Aircraft Seating GmbH & Co. KG

- Collins Aerospace

- Geven S.p.A.

- Acro Aircraft Seating

- ZIM Aircraft Seating GmbH

- Thompson Aero Seating Ltd.

- Aviointeriors S.p.A.

- Expliseat

- Stelia Aerospace

- Kittinger

- E.I.S. Aircraft GmbH

- HAECO Cabin Solutions

- EnCore Interiors

- Jamco Corporation

- Pitch Aircraft Seating

- Molon Labe Seating

- MECAPLUS

- RECARO GmbH

Frequently Asked Questions

Analyze common user questions about the Aircraft Passenger Seat market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Aircraft Passenger Seat Market?

The Aircraft Passenger Seat Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% from 2025 to 2033, reaching an estimated USD 11.5 Billion by the end of the forecast period.

What are the primary factors driving the growth of the Aircraft Passenger Seat Market?

Key drivers include the continuous increase in global air passenger traffic, extensive fleet modernization and expansion programs by airlines, the rising demand for premium cabin configurations, and ongoing technological advancements in seat design and materials.

How are technological advancements influencing the Aircraft Passenger Seat Market?

Technological advancements are driving innovation in lightweight materials for fuel efficiency, the integration of advanced in-flight entertainment and connectivity (IFEC) systems, ergonomic designs for enhanced passenger comfort, and the adoption of smart features and sustainable materials.

Which regions are expected to show significant growth in the Aircraft Passenger Seat Market?

Asia Pacific (APAC) is anticipated to be the fastest-growing region due to rising disposable incomes and significant investments in aviation infrastructure and fleet expansion. North America and Europe also remain strong markets driven by fleet modernization and MRO activities.

What are the main challenges faced by participants in the Aircraft Passenger Seat Market?

Major challenges include high certification costs and stringent regulatory requirements, volatile raw material prices and complex global supply chains, intense competition among established players, and the long design and certification lead times for new products.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted