Aircraft Leasing Market

Aircraft Leasing Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708569 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

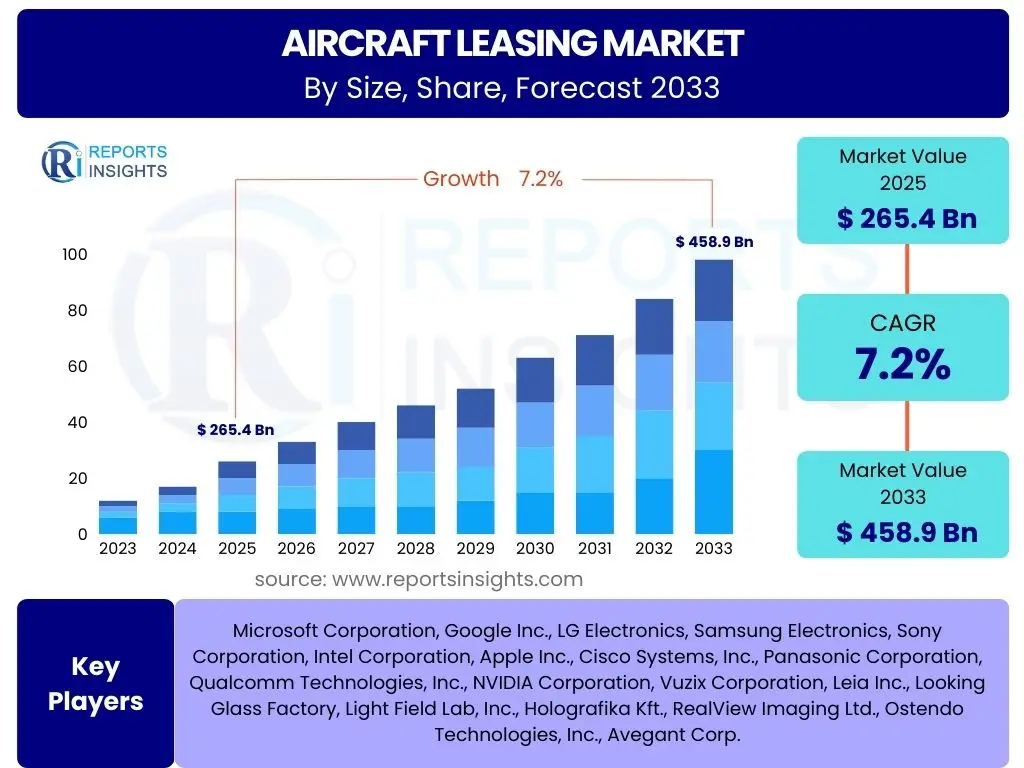

Aircraft Leasing Market Size

According to Reports Insights Consulting Pvt Ltd, The Aircraft Leasing Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2033. The market is estimated at USD 265.4 billion in 2025 and is projected to reach USD 458.9 billion by the end of the forecast period in 2033.

Key Aircraft Leasing Market Trends & Insights

The aircraft leasing market is undergoing significant transformations driven by a confluence of economic, technological, and environmental factors. Stakeholders are increasingly interested in the shift towards more sustainable aviation practices, the impact of new aircraft technologies, and the evolving financial models within the airline industry. There is a strong focus on how geopolitical stability and fluctuating fuel prices influence leasing decisions, alongside the growing demand for modern, fuel-efficient aircraft as airlines seek to optimize operational costs and reduce their carbon footprint. The expansion of low-cost carriers globally and the increasing reliance on leased fleets for operational flexibility further underscore these prevailing trends, shaping the strategic decisions of both lessors and lessees.

User queries frequently revolve around the long-term sustainability of current growth rates, the role of emerging markets in driving demand, and the implications of supply chain disruptions on new aircraft deliveries. The market is keenly observing the integration of digital solutions for fleet management and the potential for new leasing models to emerge as airlines adapt to dynamic market conditions. Additionally, the increasing average age of global aircraft fleets in certain segments necessitates a steady supply of new, leased aircraft, fueling demand for both operating and finance lease options. This pursuit of operational efficiency and financial agility continues to be a central theme for market participants.

- Increased demand for fuel-efficient and new-generation aircraft.

- Growing prevalence of operating lease models for fleet flexibility.

- Expansion of low-cost carriers (LCCs) globally, heavily relying on leased aircraft.

- Focus on sustainable aviation practices and financing for greener fleets.

- Digitalization and advanced analytics for fleet management and maintenance.

AI Impact Analysis on Aircraft Leasing

The integration of Artificial Intelligence (AI) within the aircraft leasing sector is a topic of significant interest, with common user questions focusing on how AI can enhance efficiency, mitigate risks, and create new opportunities. Users are eager to understand AI's potential in predictive maintenance, optimizing lease terms, and improving asset valuation. The core expectation is that AI will provide data-driven insights, moving the industry from reactive to proactive decision-making, thereby reducing operational costs and improving the overall profitability of leased assets. There is also curiosity regarding AI's role in risk assessment, particularly in evaluating lessee financial health and market demand fluctuations.

Key concerns often revolve around data privacy, the accuracy of AI models, and the need for skilled personnel to implement and manage AI-driven solutions. Despite these concerns, there is a clear anticipation that AI will revolutionize how aircraft assets are managed throughout their lifecycle, from initial acquisition and pricing to end-of-lease returns and remarketing. The technology is expected to streamline complex processes, offer better forecasting capabilities for future market conditions, and allow lessors to maintain a competitive edge by offering more tailored and efficient services to their airline clients.

- Enhanced predictive maintenance scheduling, reducing downtime and costs.

- Optimized aircraft valuation and pricing models using advanced analytics.

- Improved risk assessment for lessees and market conditions.

- Streamlined lease contract management and compliance monitoring.

- Data-driven insights for fleet planning and strategic asset acquisition.

Key Takeaways Aircraft Leasing Market Size & Forecast

The Aircraft Leasing Market is poised for substantial and sustained growth through 2033, driven primarily by the global resurgence in air travel demand and airlines' strategic shift towards asset-light business models. The market's expansion reflects an increasing preference among carriers for operational flexibility and reduced capital expenditure, making leasing an attractive alternative to outright aircraft ownership. A significant portion of future growth is expected to come from emerging economies and the continued proliferation of low-cost carriers, which heavily rely on leased fleets to scale operations rapidly and cost-effectively. The forecast underscores a robust environment where lessors play a critical role in facilitating fleet modernization and expansion for airlines worldwide.

A key takeaway from the market size and forecast is the ongoing importance of access to capital and the ability to manage large, diverse aircraft portfolios effectively. As the market expands, lessors capable of offering a wide range of aircraft types, flexible lease structures, and comprehensive support services will be best positioned for success. Furthermore, the increasing focus on sustainability will drive demand for newer, more fuel-efficient aircraft, creating opportunities for lessors to invest in green technologies and support airlines in achieving their environmental objectives. The market's resilience, even amidst geopolitical and economic uncertainties, highlights its fundamental role in supporting the global aviation ecosystem.

- Strong CAGR of 7.2% indicates robust market expansion.

- Market value projected to nearly double from 2025 to 2033.

- Demand fueled by global air travel growth and airline fleet modernization.

- Operating leases expected to remain the dominant lease type.

- Asia Pacific and emerging markets to be key growth engines.

Aircraft Leasing Market Drivers Analysis

The global aircraft leasing market is propelled by several fundamental drivers that reinforce its integral role in the aviation industry. A primary driver is the financial flexibility it offers to airlines, allowing them to expand or modernize their fleets without committing significant capital to outright purchases. This asset-light strategy is particularly attractive to low-cost carriers and airlines operating in volatile markets, enabling them to respond swiftly to demand fluctuations and manage financial risks more effectively. Furthermore, the robust growth in global air passenger traffic, especially in developing economies, continuously stimulates the need for more aircraft, a demand often met through leasing arrangements. The rapid expansion of new routes and the establishment of new airlines globally also contribute significantly to the market's upward trajectory, as these entities often commence operations with leased aircraft to minimize initial investment.

Another crucial driver is the ongoing technological advancements in aircraft manufacturing, leading to the production of more fuel-efficient and environmentally friendly models. Airlines are keen to upgrade their fleets to reduce operating costs and meet increasingly stringent environmental regulations. Leasing provides a cost-effective pathway to access these newer aircraft without the burden of depreciation and disposal. The competitive nature of the airline industry further incentivizes leasing, as carriers seek to maintain modern fleets to attract passengers and enhance operational performance. Lessors, with their extensive access to capital and expertise in fleet management, bridge the gap between aircraft manufacturers and airlines, thereby ensuring a steady supply of modern aircraft across the globe. This synergistic relationship underpins the sustained growth of the aircraft leasing market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Airline Preference for Operational Flexibility | +1.8% | Global, particularly Asia Pacific & Europe | Short to Mid-Term |

| Growing Global Air Passenger Traffic | +2.1% | Asia Pacific, North America, Europe | Mid to Long-Term |

| Fleet Modernization and Fuel Efficiency Demand | +1.5% | Global, developed and emerging markets | Mid to Long-Term |

| Expansion of Low-Cost Carriers (LCCs) | +1.3% | Asia Pacific, Latin America, Europe | Short to Mid-Term |

| Reduced Capital Expenditure for Airlines | +1.0% | Global | Short to Mid-Term |

Aircraft Leasing Market Restraints Analysis

Despite robust growth, the aircraft leasing market faces several significant restraints that could temper its expansion. One major restraint is the cyclical nature of the aviation industry itself, which is highly susceptible to economic downturns, geopolitical instability, and global health crises. Such events can severely impact air travel demand, leading to reduced aircraft utilization, lease payment defaults, and a surplus of available aircraft, which then depresses lease rates. The high capital intensity required for aircraft acquisition also acts as a restraint, as lessors need substantial financing capabilities, often from a limited pool of global banks and financial institutions, making them vulnerable to shifts in interest rates and credit market conditions. Volatility in interest rates, in particular, directly impacts lessors' cost of funds, potentially reducing profitability and their ability to invest in new fleets.

Another crucial restraint stems from regulatory complexities and the varying legal frameworks across different jurisdictions. Aircraft registration, taxation, and repossess rights can differ significantly from country to country, adding layers of legal and operational complexity for lessors operating globally. Furthermore, the increasing focus on environmental regulations and sustainability targets, while also an opportunity, presents a restraint in terms of higher investment costs for newer, greener aircraft and potential asset obsolescence for older, less efficient models. Geopolitical tensions and trade protectionism can also disrupt aircraft delivery schedules and impact cross-border leasing activities, posing significant challenges to the market's stability and growth trajectory. These intertwined factors necessitate careful risk management and strategic planning from market participants.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Economic Downturns and Recessions | -1.5% | Global | Short-Term |

| Fluctuations in Interest Rates and Access to Capital | -1.2% | Global | Short to Mid-Term |

| Geopolitical Instability and Trade Disputes | -1.0% | Specific Regions (e.g., Eastern Europe, Middle East) | Short to Mid-Term |

| Intensifying Environmental Regulations | -0.8% | Europe, North America | Mid to Long-Term |

| Airline Financial Instability and Defaults | -0.7% | Global, particularly emerging markets | Short-Term |

Aircraft Leasing Market Opportunities Analysis

The aircraft leasing market is ripe with opportunities driven by evolving global aviation dynamics and technological advancements. One significant area of opportunity lies in the continued growth of emerging markets, particularly in Asia Pacific, Latin America, and Africa. These regions are experiencing rapid urbanization, expanding middle classes, and increasing demand for air travel, leading to the establishment of new airlines and the expansion of existing ones. Lessors can capitalize on this growth by providing tailored leasing solutions and flexible financing options to these developing carriers, who often lack the capital for outright purchases. Furthermore, the increasing focus on cargo and freight operations, boosted by e-commerce expansion, presents a burgeoning opportunity for lessors specializing in freighter aircraft conversions and leasing, meeting the burgeoning demand for air cargo capacity.

Another key opportunity is the transition towards a more sustainable aviation industry. As airlines commit to ambitious decarbonization targets, there is a growing demand for new-generation, fuel-efficient aircraft that are compatible with Sustainable Aviation Fuels (SAFs). Lessors who strategically invest in these greener fleets can position themselves as preferred partners for environmentally conscious airlines, potentially commanding premium lease rates. Additionally, the increasing average age of global aircraft fleets in certain segments, coupled with manufacturers' backlogs, creates a robust demand for mid-life aircraft leasing and remarketing, ensuring continued utilization and value for these assets. The integration of advanced digital technologies and AI for enhanced fleet management, predictive maintenance, and optimized lease structures also provides lessors with avenues to innovate and offer value-added services, thereby differentiating themselves in a competitive market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Emerging Aviation Markets | +1.7% | Asia Pacific, Latin America, Africa | Mid to Long-Term |

| Demand for Sustainable & Fuel-Efficient Aircraft | +1.4% | Global, particularly Europe & North America | Mid to Long-Term |

| Expansion of Air Cargo and Freighter Conversions | +1.1% | Global | Short to Mid-Term |

| Technological Integration (AI, Big Data) for Fleet Mgmt. | +0.9% | Global | Mid to Long-Term |

| Mid-Life Aircraft Leasing and Remarketing | +0.8% | Global | Short to Mid-Term |

Aircraft Leasing Market Challenges Impact Analysis

The aircraft leasing market, while dynamic, faces a range of challenges that require astute navigation from market participants. A significant challenge is the intense competition among lessors, which can lead to downward pressure on lease rates and thinner profit margins, especially for less common aircraft types or during periods of aircraft oversupply. This competitive landscape necessitates continuous innovation in service offerings and financial structures to retain and attract airline clients. Furthermore, managing the residual value of aircraft is a perennial challenge; factors such as technological obsolescence, changes in market demand, and the overall economic health of airlines can significantly impact an aircraft's value at the end of its lease term. Lessors must employ sophisticated valuation models and remarketing strategies to mitigate these risks effectively. The long-term and capital-intensive nature of aircraft assets also exposes lessors to prolonged market cycles and unforeseen economic shocks.

Another critical challenge involves global supply chain disruptions affecting aircraft manufacturers. Delays in aircraft deliveries due to issues with components, labor shortages, or production bottlenecks can significantly impact lessors' fleet planning and their ability to fulfill lease commitments to airlines. This often leads to increased costs, deferred revenues, and potential penalties. Additionally, the highly regulated nature of the aviation industry, coupled with evolving international sanctions and trade restrictions, introduces compliance complexities and operational hurdles for lessors. Navigating diverse legal jurisdictions for aircraft registration, repossession, and dispute resolution adds another layer of difficulty. The rapid pace of technological change also presents a dual challenge: investing in new, advanced aircraft while managing the gradual obsolescence of older models in their portfolios. These multifaceted challenges demand robust risk management frameworks, diverse financing strategies, and a deep understanding of global aviation dynamics from lessors.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Pressure on Lease Rates | -1.3% | Global | Short to Mid-Term |

| Managing Residual Value and Asset Obsolescence | -1.1% | Global | Mid to Long-Term |

| Global Supply Chain Disruptions and Delivery Delays | -0.9% | Global | Short to Mid-Term |

| Complex Regulatory and Geopolitical Environment | -0.8% | Specific Regions (e.g., Europe, Asia Pacific) | Short to Mid-Term |

| Airline Default Risk and Creditworthiness Assessment | -0.6% | Global | Short-Term |

Aircraft Leasing Market - Updated Report Scope

This report offers a comprehensive and in-depth analysis of the Aircraft Leasing Market, detailing its size, growth trajectory, key trends, and future outlook across various segments and geographies. It provides a strategic overview, exploring the drivers, restraints, opportunities, and challenges shaping the industry. The scope encompasses detailed market projections, competitive landscape analysis, and an assessment of emerging market dynamics, delivering critical insights for stakeholders to make informed business decisions and identify lucrative investment avenues within the aviation finance sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 265.4 billion |

| Market Forecast in 2033 | USD 458.9 billion |

| Growth Rate | 7.2% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | AerCap Holdings N.V., Air Lease Corporation, BOC Aviation Limited, SMBC Aviation Capital, Avolon Holdings Limited, Dubai Aerospace Enterprise (DAE), GECAS (now part of AerCap), CDB Aviation, ICBC Leasing Co. Ltd., Minsheng Financial Leasing, Novus Aviation Capital, Castlelake L.P., ORIX Aviation Systems, ALAFCO Aviation Lease and Finance Company K.S.C.P., Nordic Aviation Capital (NAC), FLY Leasing Limited, Intrepid Aviation, Fuyo General Lease Co., Ltd., Mitsubishi HC Capital Inc., Jackson Square Aviation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Aircraft Leasing Market is strategically segmented to provide a granular view of its diverse components and underlying market dynamics. This detailed segmentation allows for a comprehensive understanding of how different aircraft types, lease structures, and end-user categories contribute to the overall market landscape. By analyzing these segments, stakeholders can identify specific areas of growth, understand evolving airline preferences, and tailor their offerings to meet distinct market needs. The segmentation facilitates targeted investment decisions and competitive positioning, revealing niches and high-growth areas within the broader aviation finance ecosystem.

Each segment is influenced by unique drivers and presents specific opportunities and challenges. For instance, the demand for narrow-body aircraft in operating leases by low-cost carriers in emerging markets represents a particularly vibrant sub-segment. Conversely, wide-body aircraft, often leased by full-service carriers for long-haul international routes, face different market dynamics related to global economic health and international travel restrictions. Understanding these nuances is crucial for both lessors aiming to optimize their portfolios and airlines seeking the most suitable and cost-effective fleet solutions for their operational models. This layered analysis supports a sophisticated approach to market strategy and risk management.

- By Aircraft Type:

- Narrow-Body Aircraft: Predominantly used for short-to-medium haul flights; high demand from LCCs.

- Wide-Body Aircraft: Employed for long-haul international routes; larger capital investment, longer lease terms.

- Regional Jet Aircraft: Servicing regional routes; crucial for connecting smaller markets.

- Turboprop Aircraft: Efficient for short distances and remote access; lower operating costs.

- By Lease Type:

- Operating Lease: Most common; off-balance sheet financing, offers flexibility and lower risk for airlines.

- Finance Lease: Treated as an asset on the airline's balance sheet; provides eventual ownership.

- By End User:

- Full-Service Carriers: Traditional airlines with extensive global networks, seeking diverse fleet solutions.

- Low-Cost Carriers: Aggressive growth, strong preference for standardized fleets (mostly narrow-body) via operating leases.

- Cargo Airlines: Driven by global trade and e-commerce; demand for freighters and converted passenger aircraft.

- Others: Includes charter airlines, business jet operators, and specialized aviation services.

- By Application:

- Passenger Aviation: Directly correlated with air travel demand and tourism.

- Cargo Aviation: Reflects global trade volumes, supply chain needs, and e-commerce growth.

Regional Highlights

- North America: A mature market characterized by large, established lessors and airlines. Strong demand for fleet modernization and replacement of older aircraft. Significant presence of major aviation finance hubs. Stable economic conditions support sustained leasing activity, particularly for both domestic and international routes. The region also exhibits a robust market for mid-life aircraft.

- Europe: A highly competitive market with a strong regulatory framework and a focus on sustainable aviation. Demand is driven by fleet upgrades to meet environmental targets and the growth of budget airlines. Geopolitical stability variations can influence regional demand, but overall, it remains a key leasing hub with a strong emphasis on modern, fuel-efficient aircraft.

- Asia Pacific (APAC): The fastest-growing region for aircraft leasing, fueled by expanding economies, rising middle-class incomes, and a surge in air travel demand. Countries like China, India, and Southeast Asian nations are witnessing substantial fleet expansion and new airline entrants. The region offers significant opportunities for lessors, often involving younger, narrow-body aircraft to serve burgeoning domestic and intra-regional routes.

- Latin America: Experiencing consistent growth, albeit with some economic volatility in specific countries. Increasing air connectivity and the rise of low-cost carriers are key drivers. Lessors often navigate economic fluctuations and local regulatory complexities to tap into this growing market, which shows strong potential for fleet expansion.

- Middle East and Africa (MEA): The Middle East is a hub for major international carriers, driving demand for wide-body aircraft for long-haul routes. Africa is an emerging market with significant untapped potential, characterized by the need for more efficient regional connectivity. Both sub-regions offer growth prospects, with Africa’s market driven by the establishment of new airlines and increased intra-continental travel.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aircraft Leasing Market.- Global Aviation Capital PLC

- Sky Lease Capital

- International Lease Finance Corporation (ILFC)

- Aviation Capital Group (ACG)

- Dubai Aerospace Enterprise (DAE) Ltd.

- GECAS (now part of AerCap)

- Bank of China Aviation

- Mitsubishi UFJ Lease & Finance Company Limited

- Standard Chartered Aviation Finance

- Aercap Holdings NV

- Air Lease Corporation

- BOC Aviation

- SMBC Aviation Capital

- Avolon Holdings Ltd

- CDB Aviation

- ICBC Leasing Co. Ltd.

- Minsheng Financial Leasing Co., Ltd.

- Nordic Aviation Capital

- Orix Aviation Systems Ltd.

- Castlelake Aviation

Frequently Asked Questions

What is aircraft leasing and why is it important?

Aircraft leasing is a financial arrangement where an airline acquires the right to use an aircraft from a lessor for a specified period, typically in exchange for regular payments. It is crucial for the aviation industry as it allows airlines to expand and modernize their fleets without significant upfront capital investment, offering financial flexibility, operational agility, and access to newer, more efficient aircraft. Lessors play a pivotal role in funding aircraft acquisitions and managing asset lifecycles for the global airline industry.

What are the primary types of aircraft leases?

The two primary types of aircraft leases are operating leases and finance leases. An operating lease is a rental agreement where the lessor retains ownership of the aircraft, providing the airline with off-balance sheet financing and flexibility to return the aircraft at the end of the term. A finance lease, conversely, is akin to a loan for the aircraft's purchase, where the lessee (airline) eventually gains ownership and the lease is recorded as an asset and liability on their balance sheet, carrying most of the ownership risks and rewards.

What factors are driving growth in the aircraft leasing market?

Key growth drivers include the continuous increase in global air passenger traffic, particularly in emerging economies, which necessitates fleet expansion. Airlines' preference for asset-light business models to preserve capital and gain operational flexibility is another major factor. Additionally, the demand for newer, more fuel-efficient aircraft for fleet modernization and the expansion of low-cost carriers, which heavily rely on leased fleets, are significant contributors to market growth.

How does AI impact the aircraft leasing industry?

AI is increasingly impacting aircraft leasing by enhancing predictive maintenance, optimizing aircraft valuation and pricing models, and improving risk assessment for lessees. It also streamlines lease contract management and compliance, providing data-driven insights for strategic fleet planning. AI's role is to boost operational efficiency, reduce costs, and offer more precise forecasting capabilities, thereby enabling lessors to make more informed decisions and maintain a competitive edge.

What are the major challenges faced by the aircraft leasing market?

The aircraft leasing market faces several challenges, including intense competition among lessors, which can pressure lease rates and margins. Managing the residual value of aircraft, which is subject to technological obsolescence and market fluctuations, is a perennial concern. Additionally, global supply chain disruptions impacting new aircraft deliveries, the complexities of diverse regulatory environments, and the inherent risks associated with airline financial instability and defaults present significant operational and financial hurdles for lessors.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted