Aircraft Enclosure Market

Aircraft Enclosure Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701241 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

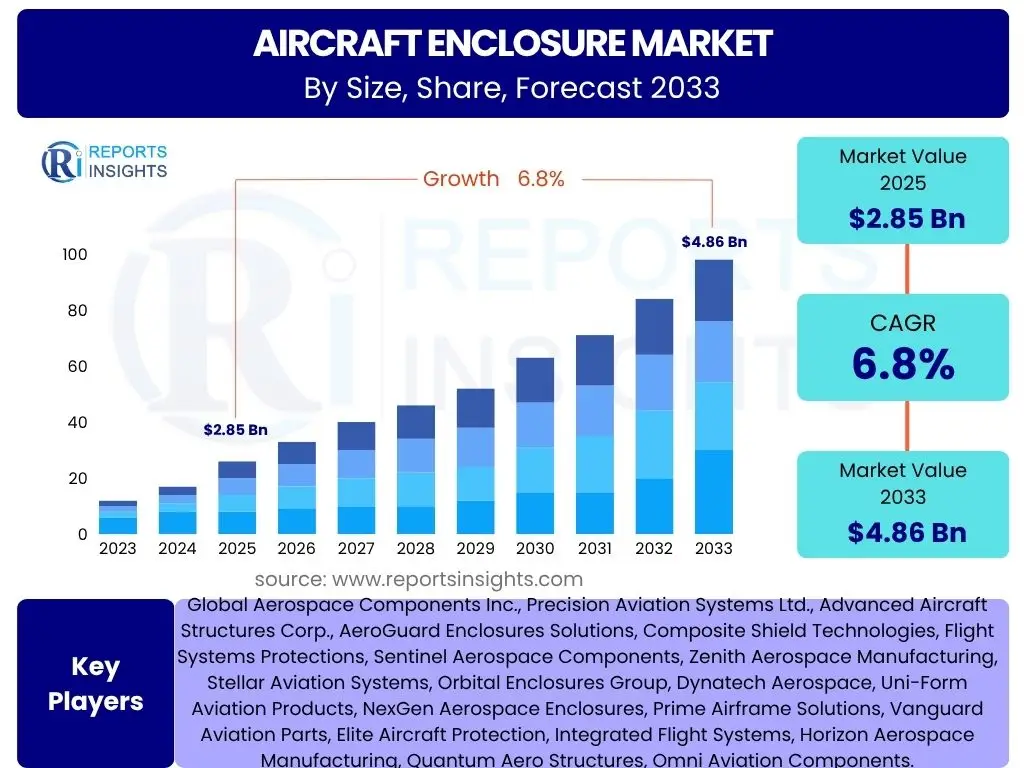

Aircraft Enclosure Market Size

According to Reports Insights Consulting Pvt Ltd, The Aircraft Enclosure Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 2.85 billion in 2025 and is projected to reach USD 4.86 billion by the end of the forecast period in 2033.

This projected growth reflects a steady expansion driven by increasing global air travel demand, modernization of existing aircraft fleets, and the continuous development of advanced aerospace technologies. The market's valuation in 2025 is a testament to the ongoing investment in both commercial and military aviation sectors, where enclosures play a critical role in protecting vital systems and components while contributing to overall aircraft performance and safety. The inherent need for robust, lightweight, and high-performance enclosures across various aircraft types underscores the market's fundamental importance.

The upward trajectory towards 2033 indicates a sustained period of innovation and demand. As new aircraft programs are launched and existing ones undergo retrofits and upgrades, the requirement for sophisticated enclosures that can withstand extreme operational conditions, minimize weight, and integrate complex systems will continue to escalate. Furthermore, advancements in materials science and manufacturing processes are enabling the production of more efficient and durable enclosures, further stimulating market growth and contributing to the significant increase in market value over the forecast period.

Key Aircraft Enclosure Market Trends & Insights

Common user inquiries concerning the Aircraft Enclosure market often revolve around the adoption of lightweight materials, the integration of smart technologies, and the impact of advanced manufacturing processes on design and functionality. Users are keenly interested in how these trends are shaping the performance characteristics, cost-effectiveness, and sustainability of aircraft enclosures. They frequently seek information on the latest material innovations and the practical applications of digital integration within enclosure systems, particularly regarding enhanced monitoring, thermal management, and structural integrity.

The market is experiencing a significant shift towards advanced composite materials, such as carbon fiber reinforced polymers (CFRPs), and lightweight metallic alloys. This trend is primarily driven by the imperative to reduce overall aircraft weight, which directly translates to improved fuel efficiency, lower operational costs, and reduced emissions. Manufacturers are actively investing in research and development to create enclosures that offer superior strength-to-weight ratios, ensuring robust protection without compromising aircraft performance. Furthermore, the modular design of enclosures is gaining traction, allowing for easier maintenance, upgrades, and customization, thereby extending the service life of aircraft components and reducing downtime.

Another prominent trend is the increasing integration of smart functionalities into aircraft enclosures. This includes embedded sensors for real-time temperature, vibration, and pressure monitoring, enabling predictive maintenance and enhancing operational safety. Active thermal management systems are also being incorporated to optimize the operating environment for sensitive avionics and electronic systems. Additionally, additive manufacturing (3D printing) is revolutionizing the production of complex enclosure geometries, allowing for intricate designs, reduced material waste, and rapid prototyping, which significantly shortens development cycles and offers unprecedented design flexibility.

- Emphasis on advanced lightweight composite materials for fuel efficiency.

- Integration of smart sensors for real-time monitoring and predictive maintenance.

- Development of active thermal management systems within enclosures.

- Adoption of additive manufacturing (3D printing) for complex geometries and rapid prototyping.

- Growing demand for modular and customizable enclosure designs.

AI Impact Analysis on Aircraft Enclosure

User queries regarding the impact of Artificial Intelligence (AI) on the Aircraft Enclosure market frequently explore AI's role in design optimization, predictive maintenance, and quality control. Users are interested in how AI can enhance the efficiency and reliability of enclosures, reduce development cycles, and contribute to overall aircraft safety. Key concerns often include the data privacy implications of AI-driven systems and the necessary infrastructure for effective AI deployment in aerospace manufacturing and operations.

AI is poised to revolutionize the design and engineering of aircraft enclosures through generative design tools. These AI algorithms can rapidly explore a vast number of design permutations, optimizing for specific criteria such as weight, strength, thermal conductivity, and acoustic properties. This iterative design process significantly reduces development time and identifies novel, more efficient geometries that traditional human design might miss. Furthermore, AI-powered simulations can predict material behavior under various stresses and environmental conditions with higher accuracy, leading to more robust and reliable enclosure designs from the outset, minimizing the need for extensive physical prototyping.

In manufacturing and operations, AI's impact extends to enhanced quality assurance and predictive maintenance. AI-driven vision systems can conduct automated, high-precision inspections of manufactured enclosures, detecting microscopic defects far more consistently than human inspectors. For in-service enclosures, AI algorithms analyze data from integrated sensors (as mentioned in trends), identifying subtle anomalies that may indicate impending failures. This enables proactive maintenance scheduling, reducing unplanned downtime and enhancing the safety and longevity of aircraft components. AI also plays a role in optimizing supply chain logistics for enclosure components, improving inventory management and ensuring timely delivery of critical materials.

- AI-driven generative design for optimal enclosure geometries and material use.

- Enhanced predictive maintenance through AI analysis of sensor data from enclosures.

- Automated quality inspection and defect detection using AI vision systems.

- Optimization of manufacturing processes and supply chain logistics for enclosure components via AI.

- Development of "smart" enclosures with AI-enabled self-monitoring and adaptive capabilities.

Key Takeaways Aircraft Enclosure Market Size & Forecast

Common user questions regarding key takeaways from the Aircraft Enclosure market size and forecast typically focus on identifying the most significant growth drivers, the primary factors influencing market expansion, and the regions poised for substantial growth. Users are looking for concise summaries of where the market is headed, what innovations are most impactful, and which segments present the most lucrative opportunities for investment or strategic focus. They seek an overarching understanding of the market’s trajectory and the underlying forces at play.

The primary takeaway from the market size and forecast analysis is the consistent and robust growth anticipated for aircraft enclosures, driven predominantly by the continuous expansion of global air passenger traffic and the subsequent increase in new aircraft deliveries. This strong demand from both commercial and military aviation sectors underpins the market's positive outlook. Furthermore, the imperative for enhanced fuel efficiency and operational longevity is accelerating the adoption of advanced materials and smart technologies within enclosures, making them integral components for next-generation aircraft designs and retrofits alike.

Another crucial insight is the increasing emphasis on innovation within the enclosure manufacturing landscape. Manufacturers are not merely producing protective shells but are integrating complex functionalities such as advanced thermal management, electromagnetic shielding, and structural health monitoring. This evolution from passive components to active systems highlights a transformative period in the market, where value is increasingly derived from technological sophistication and performance optimization. The market will also see significant regional variations in growth, with Asia-Pacific emerging as a key growth hub due to burgeoning aerospace manufacturing capabilities and increasing fleet expansions.

- Consistent growth propelled by rising global air travel and new aircraft deliveries.

- Strong demand for lightweight and high-performance enclosures across commercial and military sectors.

- Significant innovation in smart features and advanced materials driving market value.

- Asia-Pacific expected to be a major growth region due to fleet expansion and manufacturing.

- Increasing integration of multi-functional capabilities transforming enclosures into critical active systems.

Aircraft Enclosure Market Drivers Analysis

The Aircraft Enclosure Market is significantly propelled by several key drivers that collectively contribute to its growth trajectory. These drivers largely stem from the inherent demands of the aerospace industry, which continuously seeks improvements in performance, safety, and efficiency. The ongoing modernization of existing aircraft fleets and the robust pipeline of new aircraft orders are fundamental forces shaping the demand for sophisticated enclosures capable of protecting vital avionics, engine components, and cabin systems from harsh operational environments while minimizing weight.

A primary driver is the accelerating pace of global air passenger and cargo traffic. This surge necessitates the production of new aircraft and the maintenance of existing fleets, directly boosting the demand for both new and replacement enclosures. Concurrently, the increasing focus on fuel efficiency and emission reduction is compelling aircraft manufacturers to adopt lighter and more durable materials for all components, including enclosures. This pressure drives innovation in advanced composites and alloys, which offer superior strength-to-weight ratios compared to traditional materials.

Furthermore, the growing complexity of onboard electronic systems and avionics demands more sophisticated enclosures capable of providing advanced thermal management, electromagnetic shielding, and vibration isolation. The defense sector's continuous investment in advanced military aircraft and unmanned aerial vehicles (UAVs) also contributes significantly, as these platforms require extremely rugged and specialized enclosures to ensure the reliability and integrity of critical systems in demanding operational conditions. These factors collectively create a fertile ground for sustained market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Air Traffic & New Aircraft Deliveries | +1.8% | Global, particularly APAC & North America | Short- to Mid-term (2025-2030) |

| Growing Demand for Lightweight Materials & Fuel Efficiency | +1.5% | Global, led by North America & Europe | Mid- to Long-term (2026-2033) |

| Technological Advancements in Avionics & Electronics | +1.2% | North America, Europe, Asia (Japan, South Korea) | Short- to Mid-term (2025-2030) |

| Rising Defense Spending & Military Aircraft Modernization | +1.0% | North America, Europe, Middle East, Asia | Short- to Long-term (2025-2033) |

| Growth in Aircraft MRO (Maintenance, Repair, Overhaul) Activities | +0.8% | Global, particularly APAC, Europe, North America | Mid- to Long-term (2027-2033) |

Aircraft Enclosure Market Restraints Analysis

Despite the positive growth outlook, the Aircraft Enclosure Market faces several significant restraints that could impede its expansion. These challenges often stem from the highly regulated and capital-intensive nature of the aerospace industry, alongside inherent complexities in material science and manufacturing processes. Understanding these impediments is crucial for stakeholders to develop effective mitigation strategies and ensure sustained market development.

One of the primary restraints is the stringent regulatory and certification landscape. Aircraft components, including enclosures, must adhere to incredibly rigorous safety and performance standards set by aviation authorities such as the FAA and EASA. The lengthy and costly certification processes for new materials or enclosure designs can significantly delay market entry and increase development expenses, thereby deterring innovation, especially for smaller players. Furthermore, the high initial investment required for research, development, and specialized manufacturing equipment acts as a substantial barrier to entry, limiting competition and potentially slowing down technological advancements.

Another significant challenge involves the volatility of raw material prices and the complexities of global supply chains. The specialized materials used in aircraft enclosures, such as high-grade aluminum alloys, titanium, and advanced composites, are subject to price fluctuations and potential supply disruptions due to geopolitical events, trade policies, or natural disasters. Such volatility can impact production costs and lead times, affecting manufacturers' profitability and their ability to meet demand. The inherent long product development and life cycles in aerospace also mean that design changes are infrequent and costly, limiting rapid adaptation to new technologies or market demands compared to other industries.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Regulatory Compliance & Certification Costs | -1.5% | Global, particularly North America & Europe | Short- to Long-term (2025-2033) |

| High Research & Development (R&D) and Manufacturing Costs | -1.3% | Global | Short- to Long-term (2025-2033) |

| Volatility in Raw Material Prices & Supply Chain Disruptions | -1.0% | Global, dependent on material sources | Short-term (2025-2027) |

| Long Product Development & Qualification Cycles | -0.8% | Global | Mid- to Long-term (2027-2033) |

| Economic Downturns & Geopolitical Instability | -0.7% | Global, dependent on specific regions | Short-term (2025-2026) |

Aircraft Enclosure Market Opportunities Analysis

Despite existing restraints, the Aircraft Enclosure Market presents significant opportunities for growth and innovation. These opportunities arise from evolving technological landscapes, increasing demand for customized solutions, and the expansion into new market segments. Capitalizing on these avenues can enable market players to enhance their competitive edge and foster sustainable growth within the aerospace industry.

One notable opportunity lies in the burgeoning demand for specialized and customized enclosure solutions. As aircraft designs become more modular and integrate diverse electronic systems, there is a growing need for enclosures that can be tailored to specific spatial constraints, thermal requirements, and electromagnetic compatibility standards. This opens doors for manufacturers offering bespoke design, advanced materials, and sophisticated integration services, moving beyond standardized products to high-value, application-specific solutions. Furthermore, the increasing adoption of sustainable manufacturing practices, including recycling aerospace-grade materials and implementing energy-efficient production processes, represents an opportunity to meet environmental regulations and appeal to eco-conscious airlines and governments.

The aftermarket (MRO) sector offers a substantial growth opportunity, particularly as the global aircraft fleet ages and requires more extensive maintenance, repair, and overhaul activities. This creates consistent demand for replacement and upgraded enclosures, even in periods of slower new aircraft production. Additionally, the rapid proliferation of Unmanned Aerial Vehicles (UAVs) and advanced air mobility (AAM) platforms, including electric vertical takeoff and landing (eVTOL) aircraft, presents a nascent but highly promising market. These emerging aerospace segments require lightweight, durable, and often highly specialized enclosures for their unique operational profiles, offering new revenue streams for agile manufacturers who can innovate quickly and meet novel design challenges. The integration of advanced sensor technologies and connectivity within enclosures for condition monitoring further enhances their value proposition.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Customized & Application-Specific Enclosures | +1.6% | Global, especially North America & Europe | Mid- to Long-term (2027-2033) |

| Expansion of Aftermarket (MRO) Services | +1.4% | Global, particularly APAC & Europe | Short- to Long-term (2025-2033) |

| Emergence of UAVs & Advanced Air Mobility (AAM) Platforms | +1.3% | North America, Europe, Asia (China, Japan) | Mid- to Long-term (2028-2033) |

| Adoption of Sustainable Manufacturing & Recyclable Materials | +1.1% | Europe, North America | Long-term (2030-2033) |

| Integration of Smart Features & IoT for Predictive Monitoring | +0.9% | Global | Short- to Mid-term (2025-2029) |

Aircraft Enclosure Market Challenges Impact Analysis

While the Aircraft Enclosure Market offers significant opportunities, it also confronts a range of challenges that can hinder its progress and profitability. These challenges are often complex and interconnected, requiring strategic foresight and robust operational capabilities to overcome. Addressing these impediments effectively is crucial for maintaining market competitiveness and ensuring sustained growth.

One pervasive challenge is the increasing complexity of material sourcing and supply chain management. The aerospace industry relies on a global network of specialized suppliers for advanced materials and components used in enclosures. Disruptions due to geopolitical tensions, trade disputes, natural disasters, or pandemics can severely impact production schedules and material availability. This necessitates sophisticated risk management strategies, including diversification of suppliers and closer collaboration across the value chain. Furthermore, the persistent shortage of skilled labor, particularly in advanced manufacturing, engineering, and composite fabrication, poses a significant hurdle. This shortage can lead to increased labor costs, production bottlenecks, and a slower pace of innovation, impacting the overall efficiency and growth potential of the market.

Another critical challenge involves the escalating costs associated with compliance and continuous innovation. As aircraft systems become more integrated and technologically advanced, enclosures must meet more rigorous performance standards, including enhanced electromagnetic compatibility (EMC), thermal management, and vibration dampening. Achieving these standards often requires significant investments in R&D, specialized testing facilities, and highly precise manufacturing processes, which can increase the final product cost. Moreover, cybersecurity threats are becoming a growing concern for "smart" enclosures that integrate sensors and connectivity, necessitating robust security protocols to protect sensitive data and prevent unauthorized access or tampering, adding another layer of complexity and cost to development and deployment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Material Sourcing & Supply Chain Disruptions | -1.4% | Global | Short- to Mid-term (2025-2028) |

| Skilled Labor Shortage in Advanced Manufacturing | -1.2% | Global, particularly North America & Europe | Mid- to Long-term (2027-2033) |

| High Cost of Advanced R&D and Manufacturing Processes | -1.0% | Global | Long-term (2029-2033) |

| Cybersecurity Risks for Connected/Smart Enclosures | -0.9% | Global | Mid- to Long-term (2028-2033) |

| Environmental Compliance & Disposal Challenges for Composites | -0.7% | Europe, North America | Long-term (2030-2033) |

Aircraft Enclosure Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Aircraft Enclosure Market, covering historical data, current market dynamics, and future projections. It delves into critical market trends, drivers, restraints, opportunities, and challenges influencing market growth from 2025 to 2033. The scope includes detailed segmentation analysis by material, aircraft type, application, and component type, alongside an exhaustive regional outlook and profiles of key market participants. The report also integrates an AI impact analysis, offering insights into technological transformations shaping the industry's future.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.85 Billion |

| Market Forecast in 2033 | USD 4.86 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Aerospace Components Inc., Precision Aviation Systems Ltd., Advanced Aircraft Structures Corp., AeroGuard Enclosures Solutions, Composite Shield Technologies, Flight Systems Protections, Sentinel Aerospace Components, Zenith Aerospace Manufacturing, Stellar Aviation Systems, Orbital Enclosures Group, Dynatech Aerospace, Uni-Form Aviation Products, NexGen Aerospace Enclosures, Prime Airframe Solutions, Vanguard Aviation Parts, Elite Aircraft Protection, Integrated Flight Systems, Horizon Aerospace Manufacturing, Quantum Aero Structures, Omni Aviation Components. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Aircraft Enclosure Market is extensively segmented to provide a granular understanding of its diverse components and dynamics. This segmentation facilitates a detailed analysis of market behavior across various materials, aircraft types, applications, and specific component categories, offering clarity on growth opportunities and key market influences within each sub-segment. Such detailed categorization helps in identifying niche markets, understanding technological preferences, and assessing demand patterns across different aviation sectors.

The segmentation by material highlights the evolving preferences from traditional aluminum and titanium alloys towards advanced composite materials due to their superior strength-to-weight ratios and resistance to fatigue and corrosion. This shift is crucial for achieving fuel efficiency targets and extending the operational lifespan of aircraft. Furthermore, segmenting by aircraft type provides insights into demand variations across commercial aviation, military programs, general aviation, and emerging sectors like UAVs and AAM, each with distinct enclosure requirements based on their operational environment and functional needs.

Application-based segmentation distinguishes between demand arising from new aircraft production (OEM) and the aftermarket (MRO) sector. The OEM segment is driven by new aircraft orders and technological advancements in design, while the MRO segment is influenced by fleet aging, maintenance cycles, and upgrades, representing a stable and continuous source of demand. Finally, the component type segmentation offers a precise view of the market for enclosures designed for specific aircraft systems, such as avionics, engines, or cabin interiors, reflecting the specialized requirements for protecting highly sensitive or critical equipment.

- By Material: Aluminum Alloys, Titanium Alloys, Composite Materials (Carbon Fiber Composites, Glass Fiber Composites, Hybrid Composites), Other Materials (High-Performance Plastics, Specialty Alloys).

- By Aircraft Type: Commercial Aircraft (Narrow-Body, Wide-Body, Regional Jets), Military Aircraft (Fighter, Transport, Bomber, Special Mission), General Aviation Aircraft, Business Jets, Helicopters, Unmanned Aerial Vehicles (UAVs), Advanced Air Mobility (AAM) Aircraft.

- By Application: New Aircraft Production (OEM), Aftermarket (MRO).

- By Component Type: Avionics Enclosures, Engine Component Enclosures, Cabin & Cargo Enclosures, Landing Gear Enclosures, Auxiliary Power Unit (APU) Enclosures, Battery Enclosures, Hydraulic System Enclosures, Environmental Control System (ECS) Enclosures.

Regional Highlights

- North America: This region is a dominant force in the Aircraft Enclosure Market, driven by a robust aerospace and defense industry, significant R&D investments, and a large number of aircraft manufacturers and airlines. The U.S. remains a key market for both commercial and military aircraft enclosures, with a strong focus on advanced materials and integrated smart systems. Canada also contributes to regional growth through its established aerospace sector.

- Europe: Europe represents another major market, fueled by leading aerospace countries such as France, Germany, and the UK, which house major aircraft and engine manufacturers. The region's emphasis on sustainable aviation and innovation in composite materials drives demand for lightweight and environmentally friendly enclosures. Stringent safety regulations and ongoing fleet modernization initiatives further bolster market growth.

- Asia Pacific (APAC): The APAC region is projected to exhibit the highest growth rate, primarily due to the rapid expansion of air travel, increasing defense budgets, and growing domestic aircraft manufacturing capabilities in countries like China, India, and Japan. Significant investments in airport infrastructure and new airline establishments are creating a substantial demand for both commercial and military aircraft, directly impacting the enclosure market.

- Latin America: This region demonstrates steady growth, driven by increasing air passenger traffic, fleet expansions by regional airlines, and some indigenous aerospace manufacturing capabilities, particularly in Brazil. The market here is largely influenced by imports and collaborations with international aerospace companies, focusing on cost-effective and durable enclosure solutions.

- Middle East and Africa (MEA): The MEA region is experiencing growth propelled by ambitious airline expansion plans, substantial investments in aviation infrastructure, and rising defense expenditures, particularly in the Gulf Cooperation Council (GCC) countries. The demand for advanced aircraft, especially wide-body commercial jets and military aircraft, drives the need for sophisticated and resilient enclosures in this region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aircraft Enclosure Market.- Aerospace Composites Solutions

- Global Aviation Components

- Precision Aircraft Structures

- AeroGuard Enclosures Solutions

- Composite Shield Technologies

- Flight Systems Protections

- Sentinel Aerospace Components

- Zenith Aerospace Manufacturing

- Stellar Aviation Systems

- Orbital Enclosures Group

- Dynatech Aerospace

- Uni-Form Aviation Products

- NexGen Aerospace Enclosures

- Prime Airframe Solutions

- Vanguard Aviation Parts

- Elite Aircraft Protection

- Integrated Flight Systems

- Horizon Aerospace Manufacturing

- Quantum Aero Structures

- Omni Aviation Components

Frequently Asked Questions

Analyze common user questions about the Aircraft Enclosure market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth of the Aircraft Enclosure Market?

The Aircraft Enclosure Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% from 2025 to 2033, reaching an estimated USD 4.86 billion by 2033 from USD 2.85 billion in 2025.

What are the primary trends shaping the Aircraft Enclosure Market?

Key trends include the increasing adoption of lightweight composite materials for fuel efficiency, the integration of smart sensors for predictive maintenance, the rise of additive manufacturing for complex designs, and a growing demand for modular and customizable enclosure solutions.

How is AI impacting the Aircraft Enclosure industry?

AI significantly impacts the industry by enabling generative design for optimal enclosure geometries, enhancing predictive maintenance through data analysis, automating quality inspection processes, and optimizing manufacturing and supply chain logistics for components.

What are the main drivers for the Aircraft Enclosure Market's expansion?

Major drivers include the increasing global air traffic and new aircraft deliveries, the growing demand for lightweight materials to improve fuel efficiency, ongoing technological advancements in avionics, and rising defense spending for military aircraft modernization programs.

Which regions are key to the growth of the Aircraft Enclosure Market?

North America and Europe are established markets driven by strong aerospace sectors, while Asia Pacific is projected for the highest growth due to burgeoning air travel and manufacturing capabilities. Latin America and MEA also contribute through fleet expansion and defense investments.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted