Aircraft Carbon Brake Disc Market

Aircraft Carbon Brake Disc Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708175 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

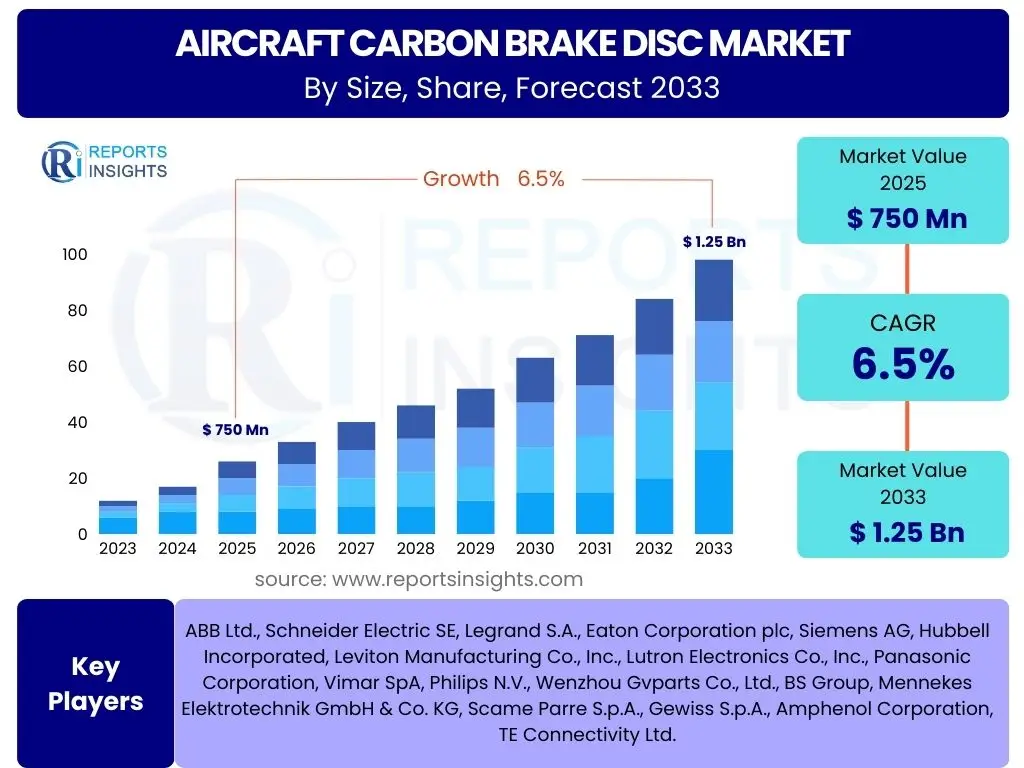

Aircraft Carbon Brake Disc Market Size

According to Reports Insights Consulting Pvt Ltd, The Aircraft Carbon Brake Disc Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. This robust growth is attributed to several factors including the increasing global air traffic, the expansion of commercial aircraft fleets, and the ongoing demand for lightweight and high-performance braking systems in the aviation industry. The advanced properties of carbon brake discs, such as superior heat resistance, durability, and reduced weight compared to traditional steel brakes, continue to drive their adoption across various aircraft segments, from commercial airliners to military jets and business aviation.

The market is estimated at USD 750 million in 2025 and is projected to reach USD 1.25 billion by the end of the forecast period in 2033. This significant upward trajectory reflects sustained investment in new aircraft deliveries, the modernization of existing fleets, and a growing emphasis on maintenance, repair, and overhaul (MRO) activities that necessitate the replacement of wear-and-tear components like brake discs. The aerospace sector's recovery post-pandemic, coupled with a focus on operational efficiency and safety, underpins the positive market outlook for carbon brake discs, making them an indispensable component in modern aircraft design.

Key Aircraft Carbon Brake Disc Market Trends & Insights

Common user inquiries regarding the Aircraft Carbon Brake Disc market consistently focus on the evolving technological landscape, the impact of sustainability efforts, and shifts in demand patterns across different aircraft types. Users are keen to understand how manufacturers are innovating to enhance performance and longevity, whether new material compositions are emerging, and how the global supply chain for these critical components is adapting to increased demand and geopolitical dynamics. The emphasis on fuel efficiency, driven by environmental regulations and airline operational costs, is a recurring theme, highlighting the importance of lightweight components like carbon brake discs.

Insights reveal a strong push towards advanced manufacturing techniques, including automation and digital twins, to improve production efficiency and reduce costs. There is also a growing interest in predictive maintenance capabilities for carbon brakes, aiming to optimize replacement cycles and minimize aircraft downtime. Furthermore, the expansion of low-cost carriers and regional aviation is creating a differentiated demand for durable and cost-effective braking solutions, influencing product development and market strategies. The integration of carbon brake discs in newer generation aircraft models, designed for enhanced range and passenger capacity, solidifies their market position and drives sustained growth.

- Increased adoption in new generation commercial and business aircraft.

- Focus on lightweighting and enhanced fuel efficiency through advanced material formulations.

- Growing demand for MRO services and aftermarket replacement parts.

- Advancements in manufacturing processes, including automation and digital quality control.

- Development of longer-lasting and more heat-resistant carbon brake materials.

- Emphasis on supply chain resilience and localized production capabilities.

AI Impact Analysis on Aircraft Carbon Brake Disc

Users frequently ask about the practical applications of Artificial Intelligence (AI) in the aircraft carbon brake disc sector, specifically how AI can improve design, manufacturing, and maintenance. Questions often revolve around AI's ability to optimize material properties, predict component failure, and streamline production processes. There is a clear interest in understanding how AI can contribute to enhanced safety, reduced operational costs, and faster innovation cycles within the highly regulated aerospace industry. The potential for AI to analyze vast datasets related to brake performance, wear patterns, and environmental conditions is a key area of inquiry, suggesting a desire for more data-driven decision-making.

AI's influence on aircraft carbon brake discs is anticipated across several critical areas. In design and engineering, AI-driven simulations can optimize material composition and structural integrity, leading to lighter yet more robust brake discs. During manufacturing, AI can enhance process control, identify defects earlier, and optimize production schedules, thereby improving quality and efficiency. Crucially, in the operational phase, AI-powered predictive maintenance algorithms can analyze real-time sensor data from aircraft brakes to forecast wear and tear, recommend optimal service intervals, and prevent unscheduled downtime, extending the lifespan of components and ensuring maximum safety. This data-centric approach will transform how carbon brake discs are managed throughout their lifecycle.

- Optimized material design and composition through AI-driven simulations.

- Enhanced manufacturing process control and defect detection using machine vision and AI analytics.

- Predictive maintenance for carbon brake discs, forecasting wear and tear to optimize replacement schedules.

- Supply chain optimization, improving inventory management and logistics for raw materials and finished products.

- Automated quality assurance and inspection, reducing human error and increasing throughput.

- Real-time performance monitoring and anomaly detection during flight operations.

Key Takeaways Aircraft Carbon Brake Disc Market Size & Forecast

Common user questions regarding key takeaways from the Aircraft Carbon Brake Disc market size and forecast center on understanding the primary growth catalysts, the segments offering the most promising opportunities, and the underlying factors contributing to market resilience. Users seek concise insights into where the market is headed, what key indicators to monitor, and which aspects present the most significant investment potential. The overarching interest is in identifying the crucial drivers that will sustain the projected growth and distinguishing between short-term fluctuations and long-term structural shifts in demand for advanced braking solutions.

The market for aircraft carbon brake discs is poised for significant expansion, primarily fueled by a surge in global commercial and military aircraft deliveries and the consistent need for MRO services. The inherent advantages of carbon materials, such as superior thermal performance and lighter weight, continue to make them the preferred choice for modern aircraft, reinforcing their market dominance. While economic uncertainties and supply chain challenges present headwinds, the fundamental demand for air travel and defense modernization ensures a stable growth trajectory. Strategic investments in R&D for next-generation materials and manufacturing processes will be crucial for companies aiming to capitalize on emerging opportunities and maintain a competitive edge throughout the forecast period.

- Robust growth in the market is driven by increasing global air traffic and new aircraft deliveries.

- Superior performance characteristics of carbon brakes ensure continued preference over traditional alternatives.

- The aftermarket segment (MRO) presents a substantial and stable revenue stream.

- Technological advancements in material science and manufacturing are key to sustaining market competitiveness.

- Asia Pacific is expected to emerge as a primary growth region due to fleet expansion.

- Emphasis on fuel efficiency and safety regulations underpins long-term demand.

Aircraft Carbon Brake Disc Market Drivers Analysis

The Aircraft Carbon Brake Disc Market is significantly propelled by the continuous expansion of global commercial aviation, characterized by an increasing demand for new aircraft deliveries and the expansion of existing fleets. As airlines worldwide strive to meet growing passenger and cargo traffic, the procurement of modern, fuel-efficient aircraft directly translates into higher demand for advanced components like carbon brake discs. These discs are integral to the performance and safety specifications of contemporary airliners, driving their adoption as standard equipment. Furthermore, the inherent advantages of carbon brakes, including their lighter weight and superior thermal management capabilities compared to steel, contribute directly to improved fuel efficiency and reduced operational costs for airlines, making them a compelling choice.

Beyond new aircraft, the robust growth in the Maintenance, Repair, and Overhaul (MRO) sector also acts as a powerful driver. As aircraft age and accumulate flight hours, components like brake discs undergo wear and tear, necessitating regular inspection, repair, and replacement. This recurring demand from the aftermarket segment provides a stable and consistent revenue stream for carbon brake disc manufacturers. Additionally, stringent safety regulations and the relentless pursuit of enhanced aircraft performance by aviation authorities and operators globally further solidify the market's foundation. The need for reliable, high-performance braking systems that can withstand extreme conditions during takeoff and landing drives innovation and continuous upgrade cycles, favoring advanced carbon composite solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Commercial Aircraft Deliveries | +1.5% | Global, particularly APAC & North America | Long-term |

| Growing Demand for Lightweight & Fuel-Efficient Aircraft | +1.0% | Global | Mid to Long-term |

| Expansion of MRO Activities and Aftermarket Demand | +0.8% | Global, especially mature markets | Long-term |

| Strict Aviation Safety Standards & Regulations | +0.7% | Global | Ongoing |

Aircraft Carbon Brake Disc Market Restraints Analysis

Despite the strong growth drivers, the Aircraft Carbon Brake Disc Market faces several significant restraints that could temper its expansion. One of the primary inhibitors is the high initial manufacturing cost associated with carbon brake discs. The complex production processes, specialized raw materials, and energy-intensive carbonization and graphitization stages contribute to a significantly higher unit cost compared to traditional steel brakes. This elevated cost can be a barrier for some aircraft operators, particularly those managing older fleets or operating on tighter budgets, leading them to defer upgrades or opt for less expensive alternatives where permissible. The capital expenditure required for production facilities and ongoing research and development also adds to the overall cost structure, impacting market accessibility.

Another substantial restraint is the extensive and time-consuming certification process required for new aerospace components. Before a new carbon brake disc design or material can be implemented, it must undergo rigorous testing and meet stringent regulatory approvals from aviation authorities worldwide, such as the FAA and EASA. This process can take several years and involve substantial investment, delaying market entry for innovative products and increasing development costs. Furthermore, the inherent fragility of carbon composites during certain operational phases, and the need for specialized handling and maintenance, can add to operational complexities and costs for airlines, creating a cautious approach to adoption for some stakeholders. Supply chain vulnerabilities, particularly concerning critical raw materials like carbon fibers, can also pose a restraint, leading to price volatility and potential production delays.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs of Carbon Discs | -0.8% | Global | Long-term |

| Lengthy & Stringent Certification Processes | -0.7% | Global | Ongoing |

| Competition from Advanced Steel Brake Solutions | -0.5% | Certain aircraft segments, developing regions | Mid-term |

| Supply Chain Volatility for Raw Materials | -0.4% | Global | Short to Mid-term |

Aircraft Carbon Brake Disc Market Opportunities Analysis

Significant opportunities exist within the Aircraft Carbon Brake Disc Market, particularly stemming from the burgeoning demand for military and defense aircraft. Global geopolitical dynamics are leading many nations to modernize their air forces, investing in new fighter jets, transport aircraft, and surveillance platforms, all of which increasingly incorporate advanced carbon braking systems for their superior performance and durability in demanding operational environments. This specialized segment provides a high-value market for manufacturers, often with longer product lifecycles and dedicated maintenance contracts, contributing to sustained revenue streams. The continuous upgrade and retrofit market for existing military fleets also presents a valuable avenue for growth, as older aircraft are equipped with newer, more efficient braking technologies to extend their operational lifespan.

Furthermore, the expanding regional jet and business jet segments offer promising growth opportunities. As air travel becomes more decentralized and business aviation continues its robust recovery, the demand for smaller, more agile aircraft is on the rise. These aircraft benefit immensely from the weight-saving and high-performance characteristics of carbon brake discs, which contribute to improved operational efficiency and reduced fuel consumption, critical factors for operators in these highly competitive sectors. Technological advancements in carbon material science and manufacturing processes also unlock new opportunities, allowing for the development of even lighter, more durable, and cost-effective brake discs. Innovations such as enhanced surface treatments or novel composite structures can lead to performance breakthroughs, expanding the addressable market and attracting new customers seeking cutting-edge solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand from Military & Defense Sector | +1.2% | North America, Europe, Asia Pacific | Long-term |

| Growth in Regional & Business Jet Segments | +0.9% | Global, particularly North America & Europe | Mid to Long-term |

| Technological Advancements in Carbon Composite Materials | +0.8% | Global | Ongoing |

| Expansion into Retrofit and Upgrade Markets for Existing Fleets | +0.7% | Global | Long-term |

Aircraft Carbon Brake Disc Market Challenges Impact Analysis

The Aircraft Carbon Brake Disc Market faces significant challenges, particularly related to the high initial investment required for research and development (R&D) and the subsequent capital expenditures for manufacturing facilities. Innovating and producing advanced carbon composite materials for aerospace applications demands substantial financial commitment, coupled with specialized expertise and equipment. This high entry barrier can deter new entrants and limits the competitive landscape, potentially slowing down the pace of innovation for certain applications. Furthermore, the volatility of raw material prices, specifically for high-grade carbon fibers and precursors, poses a constant challenge. Fluctuations in these prices can directly impact manufacturing costs, profit margins, and the overall competitiveness of carbon brake discs against alternative braking solutions, requiring agile supply chain management and strategic procurement.

Another critical challenge is managing the intellectual property (IP) landscape, which is highly complex and fiercely protected within the aerospace industry. The development of advanced carbon brake disc technologies often involves proprietary processes and patented designs, leading to potential legal disputes and limiting market access for companies without extensive IP portfolios. Navigating these IP intricacies requires significant legal resources and strategic foresight. Additionally, the industry is perpetually challenged by the need to balance performance enhancements with cost-effectiveness and durability. While carbon brakes offer superior performance, the continuous pressure to reduce total cost of ownership for airlines and operators drives manufacturers to seek innovative ways to extend product lifespan and lower maintenance costs without compromising safety or performance. This intricate balancing act demands continuous technological refinement and efficient production strategies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High R&D Investment & Capital Expenditure | -0.6% | Global | Long-term |

| Raw Material Price Volatility & Sourcing | -0.5% | Global | Short to Mid-term |

| Intense Intellectual Property Protection & Litigation | -0.4% | Global | Ongoing |

| Balancing Performance, Cost, & Durability | -0.3% | Global | Long-term |

Aircraft Carbon Brake Disc Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Aircraft Carbon Brake Disc Market, covering crucial market dynamics, segmentation analysis, regional insights, and competitive landscape. The scope encompasses detailed market sizing, forecasting, and trend analysis, offering stakeholders a clear understanding of growth opportunities, challenges, and key strategic imperatives within the industry. Emphasis is placed on recent technological advancements, regulatory impacts, and the evolving demand across various aircraft types and end-user segments to provide a holistic market perspective.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 750 Million |

| Market Forecast in 2033 | USD 1.25 Billion |

| Growth Rate | 6.5% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Leading Carbon Composite Manufacturer A, Aerospace Brake Systems Inc., Global Braking Solutions LLC, Advanced Aerospace Materials Co., Composite Tech Innovations Ltd., Aviation Components Group, Precision Brake Engineering, NextGen Aerospace Parts, Integrated Flight Systems, High-Performance Carbon Products, Elite Aircraft Braking, Global Composites & Aviation, Specialized Braking Technologies, Premier Aerospace Components, International Flight Gear Corp. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Aircraft Carbon Brake Disc Market is comprehensively segmented to provide a granular view of its dynamics and opportunities. This segmentation allows for a detailed understanding of how different factors, such as aircraft type, application, and end-user, influence demand and market growth. By analyzing these distinct categories, stakeholders can identify key areas of investment, target specific market niches, and develop tailored strategies to capitalize on evolving industry trends. The breakdown facilitates a clearer interpretation of market behavior, highlighting varying adoption rates and technological preferences across the diverse aviation landscape.

The market is primarily segmented by Aircraft Type, differentiating between the needs of Commercial Aircraft, Military Aircraft, Business Jets, and Regional Jets, each with unique performance requirements and procurement cycles. Application segmentation, typically covering Main Landing Gear and Nose Landing Gear, further refines the analysis by focusing on specific operational roles of the brake discs. The End-User segment distinguishes between Original Equipment Manufacturers (OEMs) and the Aftermarket/Maintenance, Repair, and Overhaul (MRO) sector, reflecting the distinct market dynamics for new installations versus replacement parts. Finally, Sales Channels, encompassing Direct and Indirect Sales, provide insight into distribution strategies, while regional segmentation offers a geographical perspective on market size and growth trajectories.

- By Aircraft Type:

- Commercial Aircraft

- Military Aircraft

- Business Jets

- Regional Jets

- By Application:

- Main Landing Gear

- Nose Landing Gear

- By End-User:

- Original Equipment Manufacturer (OEM)

- Aftermarket/Maintenance, Repair, and Overhaul (MRO)

- By Sales Channel:

- Direct Sales

- Indirect Sales

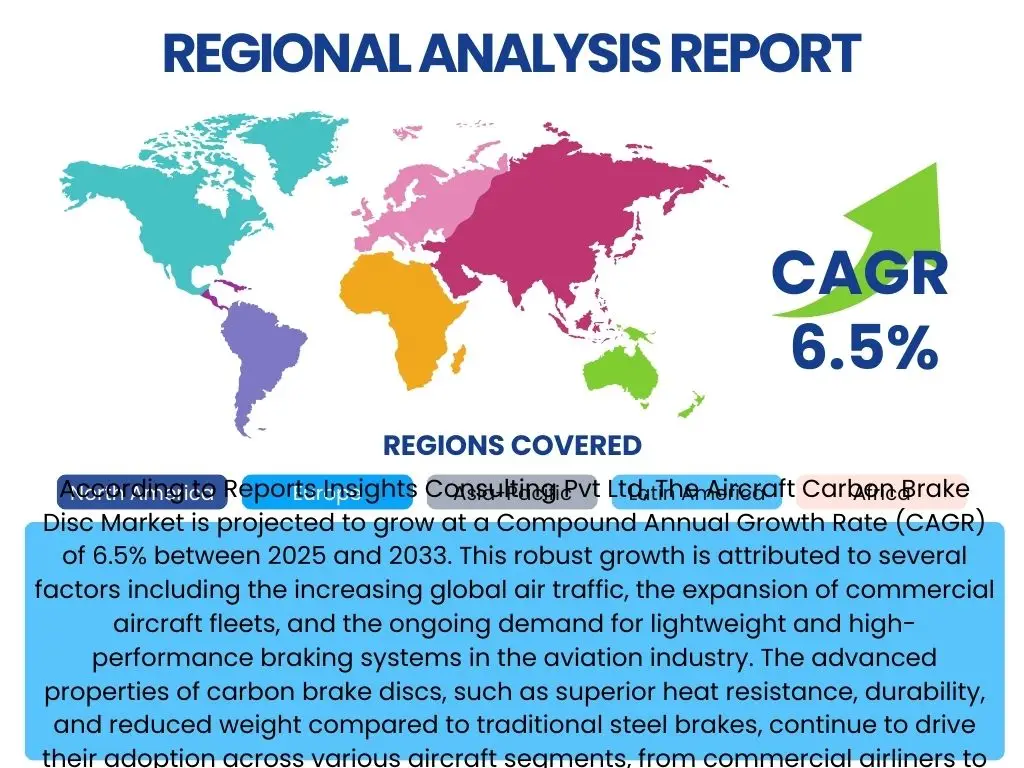

Regional Highlights

North America holds a significant share in the Aircraft Carbon Brake Disc Market, driven by the presence of major aircraft manufacturers, a robust defense sector, and a high volume of commercial air traffic. The region benefits from substantial investments in aerospace R&D, continuous fleet modernization programs, and a well-established MRO infrastructure. The stringent safety regulations and a strong emphasis on technological innovation also contribute to the widespread adoption of high-performance carbon brake discs. The United States, in particular, leads in military aircraft production and has a vast commercial aviation industry, ensuring sustained demand for advanced braking solutions for both new deliveries and aftermarket services.

Europe represents another key region, characterized by a mature aerospace industry and a strong focus on sustainable aviation. Countries like France, Germany, and the UK are home to prominent aircraft OEMs and a network of specialized component manufacturers. The region's commitment to reducing carbon emissions and improving fuel efficiency drives the demand for lightweight components such as carbon brake discs. Furthermore, a significant number of active commercial aircraft and a well-developed MRO ecosystem contribute to a steady aftermarket demand. European defense spending, although varied, also provides a consistent market for military aircraft carbon brake applications.

Asia Pacific (APAC) is projected to be the fastest-growing region in the Aircraft Carbon Brake Disc Market throughout the forecast period. This growth is primarily fueled by rapid economic expansion, increasing disposable incomes, and the consequent surge in air passenger traffic, particularly in countries like China and India. These nations are heavily investing in expanding their commercial aircraft fleets and developing their domestic aerospace manufacturing capabilities. The region's burgeoning defense budgets and strategic geopolitical imperatives also contribute to the demand for advanced military aircraft equipped with carbon braking systems. The establishment of new airports and the expansion of existing aviation infrastructure further support the robust growth trajectory in APAC.

Latin America and the Middle East & Africa (MEA) regions, while smaller in market share, are experiencing gradual growth. Latin America's market is influenced by the expansion of low-cost carriers and increasing regional air travel, leading to fleet modernization efforts. The MEA region benefits from significant investments in aviation infrastructure, particularly in the Middle East, driven by its strategic location as a global travel hub and the growth of its national carriers. Both regions also see demand from defense modernization efforts. However, market growth can be influenced by economic stability, geopolitical factors, and the pace of aviation infrastructure development in these areas.

- North America: Dominant market share due to large OEM presence, high commercial air traffic, and strong defense sector. Significant R&D investment and fleet modernization.

- Europe: Mature aerospace industry, focus on sustainable aviation and fuel efficiency, robust MRO market, and significant commercial fleet operations.

- Asia Pacific (APAC): Fastest-growing region, driven by economic growth, burgeoning air passenger traffic, fleet expansion, and increasing defense spending in countries like China and India.

- Latin America: Gradual growth from increasing regional air travel, low-cost carrier expansion, and fleet modernization.

- Middle East & Africa (MEA): Growing aviation infrastructure investment, increasing air travel, and defense modernization initiatives, particularly in the Middle East.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aircraft Carbon Brake Disc Market.- Leading Carbon Composite Manufacturer A

- Aerospace Brake Systems Inc.

- Global Braking Solutions LLC

- Advanced Aerospace Materials Co.

- Composite Tech Innovations Ltd.

- Aviation Components Group

- Precision Brake Engineering

- NextGen Aerospace Parts

- Integrated Flight Systems

- High-Performance Carbon Products

- Elite Aircraft Braking

- Global Composites & Aviation

- Specialized Braking Technologies

- Premier Aerospace Components

- International Flight Gear Corp.

- Aerotech Materials Solutions

- Carbon Systems Aerospace

- Flight Dynamics Components

- Performance Aircraft Brakes

- Universal Aviation Systems

Frequently Asked Questions

What is the projected growth rate for the Aircraft Carbon Brake Disc Market?

The Aircraft Carbon Brake Disc Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033, driven by increasing aircraft deliveries and demand for high-performance, lightweight braking solutions.

What are the primary drivers of the Aircraft Carbon Brake Disc Market?

Key drivers include the increase in commercial aircraft deliveries, growing demand for fuel-efficient aircraft, expansion of MRO activities, and stringent aviation safety standards that favor advanced carbon braking systems.

How does AI impact the manufacturing and maintenance of aircraft carbon brake discs?

AI impacts the sector by optimizing material design, enhancing manufacturing process control, enabling predictive maintenance to forecast wear, and streamlining supply chain management, ultimately improving efficiency and safety.

Which region is expected to lead market growth for aircraft carbon brake discs?

Asia Pacific (APAC) is projected to be the fastest-growing region, fueled by rapid economic expansion, increasing air passenger traffic, significant fleet expansions, and growing defense budgets in countries like China and India.

What are the main challenges faced by the Aircraft Carbon Brake Disc Market?

Major challenges include the high initial manufacturing costs, lengthy and stringent certification processes, volatility in raw material prices, and complex intellectual property landscapes requiring significant R&D investment.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted