Airborne ISR Market

Airborne ISR Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703610 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Airborne ISR Market Size

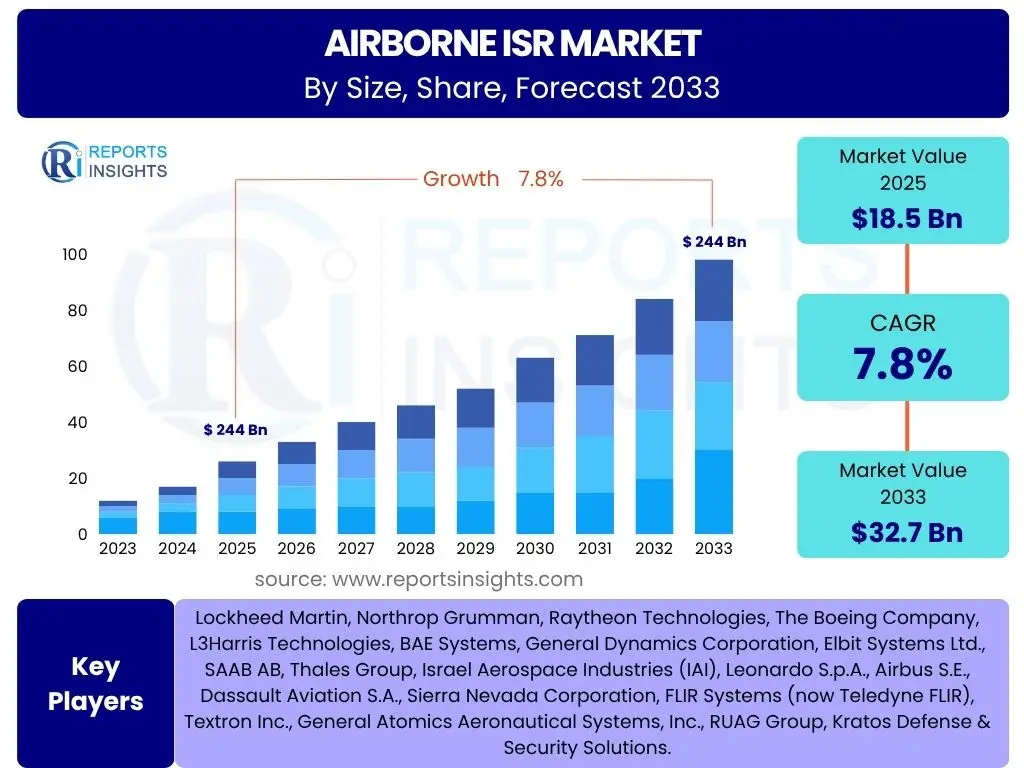

According to Reports Insights Consulting Pvt Ltd, The Airborne ISR Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 32.7 Billion by the end of the forecast period in 2033.

Key Airborne ISR Market Trends & Insights

The Airborne Intelligence, Surveillance, and Reconnaissance (ISR) market is currently undergoing significant transformation, driven by an escalating demand for real-time intelligence and enhanced situational awareness across global defense and security sectors. User inquiries frequently highlight the shift towards multi-domain operations and the increasing sophistication of sensor technologies as primary areas of interest. The integration of advanced analytics, artificial intelligence, and machine learning is also a central theme, indicating a strong market emphasis on efficient data processing and actionable insights from vast amounts of collected information.

Another prominent trend observed in user discussions pertains to the proliferation of unmanned aerial vehicles (UAVs) across various operational altitudes, from tactical short-range drones to high-altitude long-endurance (HALE) platforms. This trend underscores a strategic move towards reducing human risk in hazardous environments while extending mission endurance and coverage. Furthermore, there is a clear interest in the interoperability of diverse ISR assets and the development of secure, resilient communication links, crucial for seamless data sharing and collaborative operations among allied forces and agencies. These trends collectively point to a market prioritizing technological superiority, operational flexibility, and comprehensive intelligence gathering capabilities.

- Increasing integration of AI and Machine Learning for data processing and analysis.

- Proliferation and diversification of Unmanned Aerial Vehicles (UAVs) for extended endurance missions.

- Shift towards multi-domain operations, requiring seamless data fusion across air, land, sea, and cyber.

- Development of advanced sensor technologies, including hyperspectral, synthetic aperture radar (SAR), and signals intelligence (SIGINT).

- Enhanced focus on secure and resilient communication networks for real-time data dissemination.

- Growing demand for actionable intelligence in counter-terrorism and asymmetrical warfare scenarios.

AI Impact Analysis on Airborne ISR

User questions related to the impact of Artificial Intelligence (AI) on Airborne ISR primarily revolve around its capacity to revolutionize data processing, analysis, and decision-making. There is significant interest in how AI can manage the overwhelming volume of data collected by modern ISR platforms, transforming raw inputs into actionable intelligence with unprecedented speed and accuracy. Users express expectations that AI will enable predictive analytics, identify patterns invisible to human operators, and automate routine tasks, thereby enhancing the efficiency and effectiveness of intelligence cycles.

Concerns often raised include the ethical implications of autonomous decision-making by AI-powered systems, the cybersecurity vulnerabilities inherent in increasingly interconnected AI networks, and the significant investment required for AI integration and workforce training. Despite these challenges, there is a widespread belief that AI will be pivotal in future ISR operations, offering capabilities for real-time threat detection, target recognition, and dynamic mission planning that were previously unattainable. The integration of AI is seen not merely as an enhancement but as a fundamental shift in how airborne ISR missions are conceived and executed, providing a substantial competitive advantage.

- Automated data processing and analysis, reducing human cognitive load.

- Enhanced target recognition and classification through deep learning algorithms.

- Predictive intelligence capabilities for anticipating adversary movements and intentions.

- Support for autonomous mission planning and dynamic re-tasking of ISR assets.

- Improved sensor fusion across disparate data sources for comprehensive situational awareness.

- Accelerated decision cycles by providing real-time, actionable insights.

Key Takeaways Airborne ISR Market Size & Forecast

Common user questions regarding key takeaways from the Airborne ISR market size and forecast highlight a clear anticipation of sustained and robust growth throughout the forecast period. The insights gathered suggest that this growth is primarily fueled by persistent global geopolitical instability, rising defense expenditures by nations aiming to bolster their intelligence capabilities, and continuous advancements in sensor and data processing technologies. Users are keenly interested in understanding which technological advancements will serve as the primary growth catalysts, specifically focusing on the maturation of AI, machine learning, and advanced analytics that promise to transform raw data into critical, actionable intelligence at an accelerated pace.

Another significant takeaway is the increasing emphasis on integrated, multi-domain ISR solutions, moving beyond standalone airborne platforms to networked systems that seamlessly share intelligence across air, land, sea, and cyber domains. This reflects a strategic shift towards comprehensive situational awareness and collaborative defense postures. Furthermore, the market's trajectory indicates a strong regional differentiation, with North America and Asia Pacific leading in terms of adoption and investment due to their significant defense budgets and ongoing modernization efforts. The forecast underscores that while technological innovation will drive market expansion, strategic partnerships, and robust cybersecurity measures will be critical for market players to maintain competitive advantage and ensure the integrity of ISR operations.

- The Airborne ISR market is poised for significant and sustained growth, driven by escalating global security challenges.

- Technological innovation, particularly in AI, advanced sensors, and data analytics, is a primary growth engine.

- Increased defense spending and military modernization initiatives globally are key contributors to market expansion.

- A strong trend towards multi-domain integration and networked ISR capabilities is shaping future market development.

- North America and Asia Pacific are expected to remain dominant regions due to high defense investments and technological adoption.

- Strategic collaborations and robust cybersecurity measures are becoming increasingly crucial for market players.

Airborne ISR Market Drivers Analysis

The Airborne ISR market is significantly driven by a confluence of factors primarily centered on evolving global security landscapes and rapid technological advancements. Escalating geopolitical tensions, regional conflicts, and the persistent threat of terrorism necessitate sophisticated and real-time intelligence gathering capabilities, which airborne ISR platforms are uniquely positioned to provide. Nations are increasingly investing in modernizing their defense apparatus, with a particular focus on enhancing surveillance, reconnaissance, and intelligence operations to maintain strategic superiority and ensure national security. This sustained increase in defense budgets directly fuels the demand for advanced airborne ISR systems.

Furthermore, the relentless pace of technological innovation in sensor capabilities, data processing, and communication technologies is a critical driver. Developments in electro-optical/infrared (EO/IR) systems, Synthetic Aperture Radar (SAR), Signals Intelligence (SIGINT), and Hyperspectral Imaging are providing unprecedented levels of fidelity and breadth in data collection. Coupled with advancements in Artificial Intelligence and Machine Learning, these technologies enable more efficient data exploitation, transforming vast quantities of raw data into actionable intelligence with greater speed and accuracy, thereby increasing the operational value of airborne ISR assets.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Geopolitical Instability & Conflicts | +1.2% | Global, particularly Middle East, Eastern Europe, South China Sea | Short to Medium Term (2025-2030) |

| Rising Defense Budgets & Modernization Programs | +0.9% | North America, Asia Pacific, Europe | Medium to Long Term (2025-2033) |

| Technological Advancements in Sensors & AI | +1.5% | Global, especially developed nations | Short to Long Term (2025-2033) |

| Growing Demand for Real-time Intelligence & Situational Awareness | +1.0% | Global | Short to Medium Term (2025-2030) |

| Expansion of Unmanned Systems for ISR Operations | +0.8% | North America, Europe, Asia Pacific | Medium Term (2027-2033) |

Airborne ISR Market Restraints Analysis

Despite the robust growth projections, the Airborne ISR market faces several significant restraints that could impede its full potential. One primary challenge is the exceptionally high cost associated with the development, acquisition, integration, and long-term maintenance of advanced airborne ISR platforms and their sophisticated sensor payloads. These substantial capital outlays can be prohibitive for many nations, particularly those with smaller defense budgets, leading to slower adoption rates or reliance on less capable legacy systems. The complexity of these systems also necessitates significant investments in highly skilled personnel for operation and maintenance, further adding to the total cost of ownership.

Another key restraint involves stringent regulatory frameworks and export control restrictions, particularly for highly sensitive military-grade ISR technologies. International agreements and national policies often limit the transfer of advanced systems, complicating global market expansion and the rapid dissemination of cutting-edge capabilities. Additionally, the increasing congestion of electromagnetic spectrum and the vulnerability of communication links to cyberattacks pose operational challenges. Maintaining secure and reliable data transfer channels in contested environments requires continuous investment in resilient architectures, which adds to operational complexity and cost, potentially slowing down the deployment of new ISR capabilities.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Development & Procurement Costs | -0.7% | Global, particularly developing nations | Long Term (2025-2033) |

| Stringent Regulatory & Export Control Regimes | -0.5% | Global | Medium to Long Term (2025-2033) |

| Cybersecurity Threats & Data Vulnerabilities | -0.4% | Global | Short to Medium Term (2025-2030) |

| Integration & Interoperability Challenges of Legacy Systems | -0.3% | Global | Medium Term (2027-2033) |

| Scarcity of Skilled Personnel for Operations & Maintenance | -0.2% | Global | Long Term (2025-2033) |

Airborne ISR Market Opportunities Analysis

The Airborne ISR market is ripe with opportunities, primarily stemming from the continued integration of emerging technologies and the expansion into new application areas. The increasing maturity of Artificial Intelligence and Machine Learning presents a significant avenue for growth, enabling more sophisticated data analytics, autonomous operations, and predictive intelligence capabilities. This allows for a shift from reactive data collection to proactive threat anticipation, enhancing the strategic value of ISR. Furthermore, the development of swarming drone technologies and collaborative unmanned systems offers potential for unprecedented coverage and endurance, reducing operational costs while expanding mission scope.

Another major opportunity lies in the burgeoning market for commercial and dual-use ISR solutions. As the demand for intelligence extends beyond traditional military applications to areas like disaster management, environmental monitoring, maritime surveillance, and critical infrastructure protection, commercial off-the-shelf (COTS) components and civilian platforms equipped with ISR capabilities are gaining traction. This creates new revenue streams and reduces the reliance on highly specialized military contracts. Additionally, strategic partnerships and collaborations between established defense contractors and agile technology startups can foster innovation, accelerate research and development, and facilitate the rapid deployment of next-generation ISR solutions, capitalizing on complementary expertise and resources.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of Advanced AI/ML & Big Data Analytics | +1.1% | Global | Medium to Long Term (2027-2033) |

| Rise of Commercial & Dual-Use ISR Platforms | +0.8% | North America, Europe, Asia Pacific | Medium Term (2027-2033) |

| Development of Unmanned & Autonomous Systems (e.g., HAPS, Drone Swarms) | +0.9% | Global | Long Term (2028-2033) |

| Increasing Demand for Maritime & Border Surveillance | +0.7% | Coastal Nations, Border Regions | Short to Medium Term (2025-2030) |

| Strategic Partnerships & Collaborative R&D Initiatives | +0.6% | Global | Short to Long Term (2025-2033) |

Airborne ISR Market Challenges Impact Analysis

The Airborne ISR market, while exhibiting strong growth potential, contends with several significant challenges that demand innovative solutions. One primary challenge is managing the sheer volume and velocity of data generated by advanced ISR sensors. This data overload can overwhelm existing processing, exploitation, and dissemination (PED) capabilities, leading to delays in intelligence delivery and potential missed opportunities. Effective data management, secure storage, and real-time analytical tools are critical but often represent complex and costly implementation hurdles, especially for legacy systems not designed for such demands.

Another considerable challenge is ensuring seamless interoperability across diverse platforms, sensors, and communication networks, particularly in multi-national or multi-agency operations. Different systems often operate on disparate standards and protocols, creating data silos and hindering the rapid sharing of critical intelligence. Achieving true interoperability requires substantial investment in open architectures, standardized interfaces, and robust middleware, which can be technologically challenging and politically complex. Furthermore, the persistent and evolving threat of cyberattacks targeting ISR networks and data links presents a constant challenge, necessitating continuous investment in advanced cybersecurity measures to protect sensitive intelligence from espionage and disruption.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Overload & Processing Bottlenecks | -0.6% | Global | Short to Medium Term (2025-2030) |

| Interoperability Issues Across Disparate Systems | -0.5% | Global | Medium Term (2027-2033) |

| Spectrum Congestion & Communication Bandwidth Limitations | -0.4% | Global | Short to Long Term (2025-2033) |

| Skilled Workforce Shortage for Advanced Technologies | -0.3% | Global | Long Term (2028-2033) |

| Ethical & Legal Considerations of Autonomous ISR Systems | -0.2% | Developed Nations | Medium to Long Term (2027-2033) |

Airborne ISR Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Airborne ISR market, offering critical insights into its current state, historical performance, and future growth trajectory. The scope encompasses detailed segmentation across various types, platforms, systems, applications, end-users, and capabilities, providing a granular view of market dynamics. It further delves into regional market trends, competitive landscapes, and the impact of key market drivers, restraints, opportunities, and challenges, equipping stakeholders with a robust foundation for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 32.7 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Lockheed Martin, Northrop Grumman, Raytheon Technologies, The Boeing Company, L3Harris Technologies, BAE Systems, General Dynamics Corporation, Elbit Systems Ltd., SAAB AB, Thales Group, Israel Aerospace Industries (IAI), Leonardo S.p.A., Airbus S.E., Dassault Aviation S.A., Sierra Nevada Corporation, FLIR Systems (now Teledyne FLIR), Textron Inc., General Atomics Aeronautical Systems, Inc., RUAG Group, Kratos Defense & Security Solutions. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Airborne ISR market is meticulously segmented to provide a granular understanding of its diverse components and evolving landscape. This segmentation allows for precise analysis of market dynamics, growth drivers, and opportunities across various technological and operational domains. Key segments include the type of ISR (manned vs. unmanned), the platform utilized (fixed-wing, rotary-wing, or various UAV categories), the specific systems employed (ranging from radar and EO/IR to advanced SIGINT and EW suites), and the broad application areas such as military defense, homeland security, and civil uses. This multi-faceted breakdown highlights the market's complexity and the specialized requirements of different end-users.

- By Type:

- Manned ISR

- Unmanned ISR

- By Platform:

- Fixed-Wing Aircraft

- Rotary-Wing Aircraft

- Unmanned Aerial Vehicles (UAVs)

- High Altitude Long Endurance (HALE)

- Medium Altitude Long Endurance (MALE)

- Tactical UAVs

- Small UAVs (SUAVs)

- By System:

- Radars

- Synthetic Aperture Radar (SAR)

- Ground Moving Target Indication (GMTI)

- Maritime Surveillance Radar (MSR)

- Electro-Optical/Infrared (EO/IR)

- Signals Intelligence (SIGINT)

- Electronic Intelligence (ELINT)

- Communications Intelligence (COMINT)

- Hyperspectral Imaging

- Electronic Warfare (EW) Systems

- Communication & Data Links

- Ground Control Stations (GCS)

- Radars

- By Application:

- Military & Defense

- Border Security

- Counter-Terrorism

- Maritime Patrol

- Target Acquisition

- Reconnaissance

- Surveillance

- Homeland Security

- Critical Infrastructure Protection

- Disaster Management

- Environmental Monitoring

- Military & Defense

- By End User:

- Army

- Navy

- Air Force

- Special Forces

- Coast Guard

- By Capabilities:

- Data Collection

- Data Processing & Exploitation

- Data Communication & Dissemination

Regional Highlights

- North America: This region is anticipated to maintain its dominance in the Airborne ISR market, primarily driven by the substantial defense budget of the United States and its continuous investment in advanced military technologies. The U.S. Department of Defense is a major adopter of cutting-edge ISR solutions, emphasizing capabilities in multi-domain operations, artificial intelligence integration, and high-endurance unmanned platforms. Canada also contributes to regional growth through its defense modernization initiatives and participation in international security efforts. The presence of leading aerospace and defense contractors further solidifies North America's position as a hub for ISR innovation and deployment.

- Europe: Europe represents a significant market, propelled by increasing geopolitical complexities in Eastern Europe and the Middle East, necessitating enhanced surveillance and intelligence capabilities among NATO members and other European nations. Countries like the United Kingdom, France, Germany, and Italy are actively upgrading their ISR fleets, investing in both manned and unmanned systems. Collaborative defense programs and the focus on interoperability among allied forces also drive demand, with a growing emphasis on real-time data sharing and advanced analytics to counter evolving threats and support expeditionary operations.

- Asia Pacific (APAC): The Asia Pacific region is forecast to experience the highest growth rate, fueled by escalating territorial disputes, rising defense expenditures by major economies like China, India, Japan, and South Korea, and the increasing modernization of their armed forces. The demand for maritime surveillance and border security solutions is particularly strong, given the extensive coastlines and complex geopolitical landscape. Investments in indigenous defense production and technology transfer agreements further accelerate the adoption of advanced Airborne ISR capabilities across the region, alongside a keen interest in integrating AI-powered analytics and long-endurance UAVs.

- Middle East and Africa (MEA): The MEA region is characterized by ongoing regional conflicts, counter-terrorism efforts, and significant investments in defense by Gulf Cooperation Council (GCC) countries. This drives a consistent demand for robust Airborne ISR systems to ensure national and regional security. Countries such as Saudi Arabia, UAE, and Israel are leading adopters of advanced surveillance and reconnaissance technologies. While market growth is primarily concentrated in the defense sector, there is an emerging interest in dual-use ISR applications for critical infrastructure protection and border management, particularly in response to illicit activities and regional instabilities.

- Latin America: The Latin American Airborne ISR market is expected to exhibit steady growth, primarily driven by the need for enhanced border control, anti-narcotics operations, and combating illegal mining and deforestation. Nations in this region are increasingly investing in intelligence capabilities to address internal security challenges and cross-border criminal activities. While budget constraints can sometimes limit the scale of acquisitions, there is a consistent demand for cost-effective and versatile ISR platforms, including smaller UAVs and upgraded legacy aircraft equipped with modern sensor suites, to support national security priorities and disaster response efforts.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Airborne ISR Market.- Lockheed Martin

- Northrop Grumman

- Raytheon Technologies

- The Boeing Company

- L3Harris Technologies

- BAE Systems

- General Dynamics Corporation

- Elbit Systems Ltd.

- SAAB AB

- Thales Group

- Israel Aerospace Industries (IAI)

- Leonardo S.p.A.

- Airbus S.E.

- Dassault Aviation S.A.

- Sierra Nevada Corporation

- FLIR Systems (now Teledyne FLIR)

- Textron Inc.

- General Atomics Aeronautical Systems, Inc.

- RUAG Group

- Kratos Defense & Security Solutions

Frequently Asked Questions

What is Airborne ISR and why is it important?

Airborne ISR stands for Airborne Intelligence, Surveillance, and Reconnaissance. It refers to the collection of intelligence data using airborne platforms like manned aircraft and unmanned aerial vehicles (UAVs) equipped with various sensors. This data is crucial for providing real-time situational awareness, supporting military operations, enhancing national security, and informing strategic decision-making by identifying threats, tracking movements, and monitoring activities from an aerial perspective. Its importance stems from its ability to offer persistent, wide-area coverage and high-resolution data collection in various operational environments.

What are the key technologies driving the Airborne ISR market?

The Airborne ISR market is primarily driven by advancements in sensor technologies, including sophisticated Electro-Optical/Infrared (EO/IR) systems, Synthetic Aperture Radar (SAR) with Ground Moving Target Indication (GMTI) capabilities, and Signals Intelligence (SIGINT) solutions. Additionally, the integration of Artificial Intelligence (AI) and Machine Learning (ML) for enhanced data processing, analysis, and fusion is paramount. Secure and high-bandwidth communication links, along with robust data exploitation and dissemination (PED) systems, are also crucial for translating raw data into actionable intelligence in real-time.

How is AI transforming Airborne ISR operations?

AI is fundamentally transforming Airborne ISR by automating the processing and analysis of vast datasets, accelerating the decision-making cycle. It enables predictive intelligence, allowing for the anticipation of adversary actions and optimization of resource deployment. AI-powered algorithms enhance target recognition and classification, improve sensor fusion for comprehensive situational awareness, and support autonomous mission planning. While presenting challenges like data security and ethical considerations, AI's role in deriving actionable insights from complex data is becoming indispensable, significantly enhancing the efficiency and effectiveness of ISR missions.

What are the primary challenges faced by the Airborne ISR market?

The Airborne ISR market faces several challenges, including the massive data overload generated by advanced sensors, which strains existing processing and analysis capabilities. Interoperability issues among diverse platforms and systems often hinder seamless data sharing and collaborative operations. High development and acquisition costs pose a significant barrier, particularly for nations with limited defense budgets. Furthermore, the persistent threat of cyberattacks targeting sensitive ISR networks and the scarcity of skilled personnel required to operate and maintain these complex systems present ongoing hurdles that necessitate continuous innovation and investment.

Which regions are leading the growth in the Airborne ISR market?

North America currently leads the Airborne ISR market due to significant defense spending and technological advancements, primarily driven by the United States. The Asia Pacific region is projected to experience the highest growth rate, fueled by rising defense budgets, increasing geopolitical tensions, and modernization efforts in countries like China, India, and Japan. Europe also holds a substantial market share, with nations investing heavily in ISR capabilities to address evolving security threats. The Middle East and Africa region shows consistent demand driven by ongoing conflicts and counter-terrorism operations, albeit with a more fragmented market landscape.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted