Airborne Digital Battlefield Market

Airborne Digital Battlefield Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700998 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

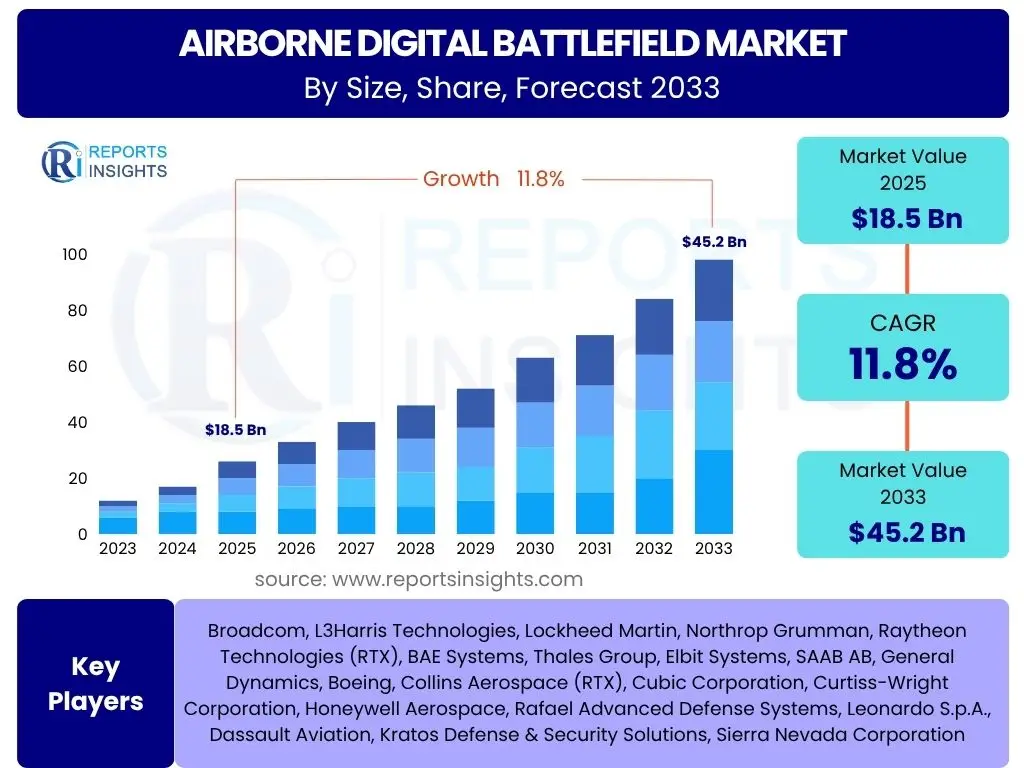

Airborne Digital Battlefield Market Size

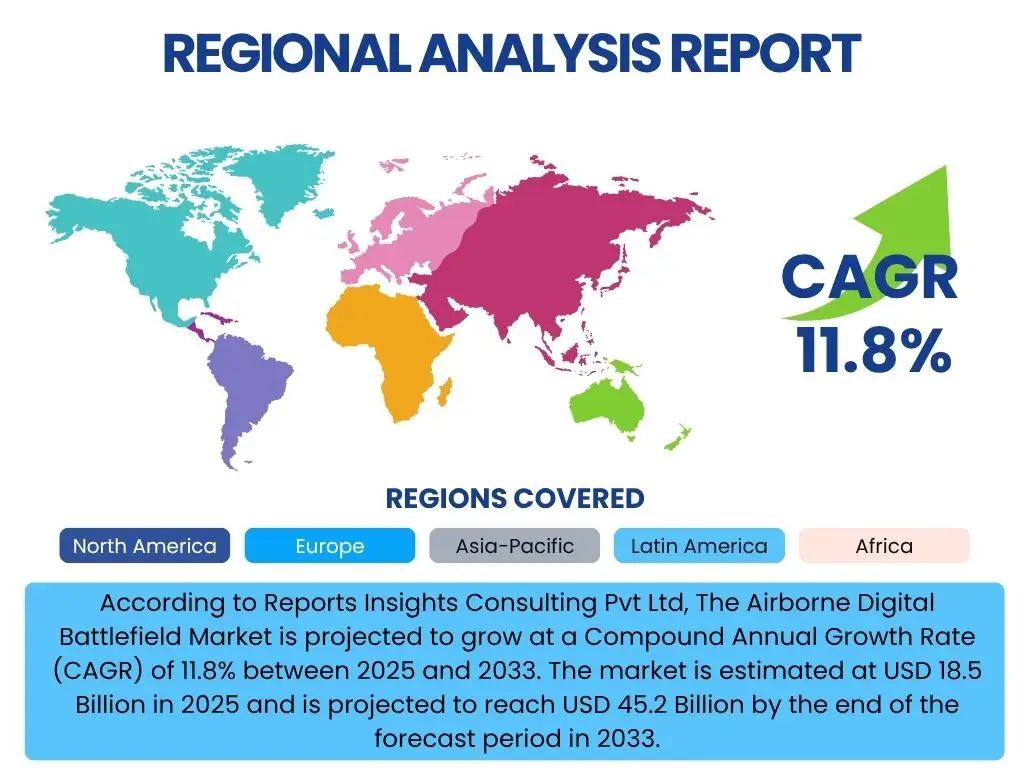

According to Reports Insights Consulting Pvt Ltd, The Airborne Digital Battlefield Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.8% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 45.2 Billion by the end of the forecast period in 2033.

Key Airborne Digital Battlefield Market Trends & Insights

The Airborne Digital Battlefield Market is witnessing transformative shifts driven by the imperative for enhanced situational awareness, rapid decision-making, and seamless connectivity in complex operational environments. Common inquiries often revolve around the convergence of advanced technologies, the push for multi-domain integration, and the evolving nature of aerial combat. Users frequently seek to understand how concepts like networked warfare and real-time intelligence are being actualized through airborne platforms, and the implications for military superiority. There is also significant interest in the transition from traditional, siloed systems to an interconnected digital ecosystem that allows for dynamic resource allocation and coordinated responses across air, land, sea, space, and cyber domains.

Another area of consistent user inquiry pertains to the increasing sophistication of data processing and analytics at the edge. The sheer volume of information collected by airborne sensors necessitates advanced processing capabilities directly on the platform to reduce latency and improve responsiveness. This trend is closely linked to the demand for autonomous and semi-autonomous systems that can operate with minimal human intervention, thereby reducing cognitive load on operators and accelerating mission execution. Furthermore, the market is profoundly influenced by the geopolitical landscape, driving defense budgets towards modernization efforts that prioritize digital transformation within airborne platforms.

- Integration of Artificial Intelligence and Machine Learning (AI/ML) for predictive analytics and autonomous operations.

- Expansion of Manned-Unmanned Teaming (MUM-T) capabilities for enhanced combat effectiveness and reduced risk.

- Development of secure, resilient, and high-bandwidth communication networks for real-time data sharing across platforms.

- Increased demand for multi-domain command and control systems to synchronize operations across air, land, sea, space, and cyber.

- Focus on modular, open system architectures (MOSA) to facilitate rapid upgrades and interoperability.

- Miniaturization and integration of advanced sensors (e.g., electronic warfare, SIGINT, EO/IR) on diverse airborne platforms.

- Adoption of cloud and edge computing paradigms for distributed data processing and decentralized decision-making.

AI Impact Analysis on Airborne Digital Battlefield

User queries regarding the impact of Artificial Intelligence on the Airborne Digital Battlefield consistently highlight themes of operational efficiency, enhanced cognitive capabilities, and the future of autonomous warfare. There is a strong interest in how AI can process vast amounts of sensor data more rapidly than human operators, identify patterns, and offer predictive insights to commanders, thereby accelerating the OODA (Observe, Orient, Decide, Act) loop. Concerns also frequently emerge about the ethical implications of AI in combat, the reliability of AI algorithms in high-stakes environments, and the necessary balance between human oversight and machine autonomy. Users seek clarity on how AI can transition from a supportive tool to an integral, decision-making component within airborne systems.

Furthermore, inquiries often delve into the practical applications of AI, such as its role in advanced threat detection, target recognition, and electronic warfare. The potential for AI to optimize mission planning, dynamic re-routing, and resource allocation in real-time is a recurring topic. There is an expectation that AI will significantly reduce the workload on aircrew, allowing them to focus on higher-level strategic objectives rather than routine tasks. The long-term vision of an AI-driven airborne digital battlefield includes systems that can learn, adapt, and evolve their strategies in response to dynamic threats, leading to a new era of cognitive superiority in aerial warfare.

- Enhanced Situational Awareness: AI algorithms process real-time sensor data from multiple sources (radar, EO/IR, SIGINT) to create comprehensive, fused situational pictures, identifying threats and opportunities faster than human analysis.

- Predictive Maintenance and Logistics: AI-driven diagnostics predict equipment failures and optimize maintenance schedules for airborne platforms, increasing operational readiness and reducing downtime.

- Autonomous Navigation and Maneuvering: AI enables advanced autonomous flight capabilities, including obstacle avoidance, precise navigation in GPS-denied environments, and complex evasive maneuvers.

- Advanced Threat Detection and Targeting: AI improves the speed and accuracy of target recognition, classification, and engagement, especially against stealthy or rapidly moving targets.

- Cognitive Electronic Warfare: AI algorithms can rapidly identify, classify, and counter complex and adaptive enemy electronic warfare systems, optimizing jamming and deception techniques.

- Optimized Resource Allocation: AI systems dynamically allocate resources (e.g., sensor modes, weapon systems, communication bandwidth) based on mission objectives and evolving battlefield conditions.

- Manned-Unmanned Teaming (MUM-T) Augmentation: AI facilitates seamless communication and coordination between manned aircraft and unmanned aerial vehicles (UAVs), enabling swarm tactics and distributed operations.

Key Takeaways Airborne Digital Battlefield Market Size & Forecast

Common user questions regarding the key takeaways from the Airborne Digital Battlefield market size and forecast often focus on understanding the primary growth catalysts and the overarching strategic importance of this domain. Users are particularly interested in identifying what drives the substantial projected growth and how this market contributes to future defense capabilities. There is a desire to grasp the most critical factors that will shape its trajectory over the next decade, from technological advancements to geopolitical influences. The insights sought frequently aim to clarify where the most significant investments are being made and which technological areas are experiencing the most rapid evolution.

Furthermore, users consistently inquire about the implications of the market's expansion for military readiness and operational effectiveness. They seek to understand how the integration of digital technologies in airborne platforms translates into tangible advantages on the battlefield, such as improved decision-making speed, enhanced survivability, and the ability to conduct more complex, multi-domain operations. The forecast's significance lies in highlighting the shift towards highly networked, data-centric aerial warfare, underscoring the necessity for robust digital infrastructure and advanced analytical capabilities within airborne systems to maintain a competitive edge against evolving threats.

- The Airborne Digital Battlefield Market is poised for significant expansion, driven by increasing defense modernization initiatives globally.

- Technological convergence, particularly in AI, big data, and secure communications, is a fundamental catalyst for market growth.

- The emphasis on real-time situational awareness and networked combat operations is transforming aerial warfare paradigms.

- Investments in resilient and interoperable digital architectures for airborne platforms are becoming paramount for national security.

- The market's growth reflects a strategic shift towards leveraging data and connectivity for cognitive superiority in the air domain.

Airborne Digital Battlefield Market Drivers Analysis

The Airborne Digital Battlefield market is primarily propelled by the global escalation in defense budgets, particularly among major military powers, aimed at modernizing existing air forces and acquiring advanced airborne platforms. This increased spending is a direct response to rising geopolitical tensions and the emergence of sophisticated asymmetric threats, necessitating superior aerial reconnaissance, command and control, and combat capabilities. The drive for enhanced situational awareness across all domains—air, land, sea, space, and cyber—further fuels demand for advanced digital solutions that can fuse disparate data streams into a unified operational picture. This integration is critical for rapid, informed decision-making in dynamic combat environments.

Technological advancements in areas such as C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance) systems are also significant drivers. Innovations in sensor technology, secure communication protocols, high-speed data processing, and artificial intelligence are enabling new levels of performance for airborne platforms. The widespread adoption of networked warfare concepts, where individual platforms act as nodes in a broader digital ecosystem, necessitates the development of robust and resilient digital battlefield architectures. This shift from platform-centric to network-centric operations is a core driver, emphasizing interoperability and seamless data exchange among diverse airborne assets and ground-based systems.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Defense Budgets & Modernization Initiatives | +2.5% | Global (North America, APAC, Europe) | Short to Long-term (2025-2033) |

| Rising Geopolitical Tensions & Need for Superiority | +2.0% | Global (Europe, APAC, Middle East) | Short to Mid-term (2025-2029) |

| Advancements in C4ISR & Sensor Technologies | +1.8% | North America, Europe, Israel | Mid to Long-term (2027-2033) |

| Demand for Enhanced Situational Awareness & Data Fusion | +1.5% | Global | Short to Long-term (2025-2033) |

| Shift Towards Network-Centric & Multi-Domain Operations | +1.2% | Global (NATO, Five Eyes nations) | Mid to Long-term (2028-2033) |

Airborne Digital Battlefield Market Restraints Analysis

The Airborne Digital Battlefield market faces several significant restraints that could impede its growth trajectory. High development, integration, and procurement costs associated with advanced digital systems are primary barriers. Military budgets, while increasing, still operate under fiscal constraints, making the adoption of cutting-edge, capital-intensive technologies challenging for some nations. The complexity of integrating disparate systems from various vendors onto existing and new airborne platforms presents considerable technical hurdles, often leading to extended development cycles and unforeseen expenses. Ensuring seamless interoperability between legacy systems and new digital architectures is a persistent and costly challenge.

Cybersecurity threats represent another substantial restraint. As airborne platforms become increasingly networked and data-dependent, they become more vulnerable to sophisticated cyberattacks aimed at disrupting communications, corrupting data, or gaining control of critical systems. Protecting these digital battlefields from adversarial exploitation requires continuous investment in robust cybersecurity measures, which adds to the overall cost and complexity. Furthermore, the stringent regulatory and certification processes required for military aviation systems can delay the introduction of new technologies. The shortage of skilled personnel proficient in advanced digital technologies, artificial intelligence, and cybersecurity within military forces also poses a significant bottleneck, impacting both development and operational capabilities.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Development & Integration Costs | -1.8% | Global (Developing Nations) | Short to Long-term (2025-2033) |

| Cybersecurity Threats & Vulnerabilities | -1.5% | Global | Short to Long-term (2025-2033) |

| Complex Interoperability Challenges | -1.3% | Global | Mid to Long-term (2027-2033) |

| Stringent Regulatory & Certification Processes | -1.0% | North America, Europe | Short to Mid-term (2025-2029) |

| Shortage of Skilled Personnel | -0.8% | Global | Mid to Long-term (2027-2033) |

Airborne Digital Battlefield Market Opportunities Analysis

The Airborne Digital Battlefield market presents substantial growth opportunities driven by the accelerating integration of Artificial Intelligence and Machine Learning (AI/ML) into airborne platforms. This offers avenues for developing more autonomous systems, enhancing predictive capabilities, and optimizing decision-making processes, leading to revolutionary advancements in aerial combat and intelligence gathering. The continuous evolution of 5G and future 6G communication technologies also opens up possibilities for ultra-low latency, high-bandwidth data transfer, enabling more robust real-time data sharing and distributed network operations across the digital battlefield. This will facilitate more complex Manned-Unmanned Teaming (MUM-T) scenarios and truly networked aerial platforms.

Furthermore, the increasing adoption of edge computing, where data processing occurs closer to the source (i.e., on the airborne platform), reduces reliance on centralized ground stations and improves responsiveness, especially in contested environments. This decentralized approach enhances resilience and allows for faster mission execution. Opportunities also exist in the development of modular, open system architectures (MOSA), which promise to lower integration costs, reduce vendor lock-in, and accelerate the fielding of new capabilities. International collaborations and joint ventures between defense contractors and technology firms will also unlock new markets and foster innovation, leveraging diverse expertise to address complex digital battlefield challenges.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Integration of AI & ML in Autonomous Systems | +2.2% | Global (North America, Europe, APAC) | Mid to Long-term (2027-2033) |

| Emergence of 5G & 6G for High-Bandwidth Connectivity | +1.9% | Global | Mid to Long-term (2028-2033) |

| Adoption of Edge Computing for Real-time Processing | +1.7% | Global | Short to Long-term (2025-2033) |

| Development of Modular Open System Architectures (MOSA) | +1.5% | North America, Europe | Mid to Long-term (2027-2033) |

| Expansion of Manned-Unmanned Teaming (MUM-T) Concepts | +1.3% | Global | Short to Long-term (2025-2033) |

Airborne Digital Battlefield Market Challenges Impact Analysis

The Airborne Digital Battlefield market faces several formidable challenges that could hinder its full potential realization. Interoperability remains a critical hurdle, as integrating diverse legacy systems with new digital technologies from various manufacturers across different platforms is inherently complex. This lack of seamless communication and data exchange can limit the effectiveness of networked operations and create information silos, undermining the concept of a unified digital battlefield. Furthermore, the sheer volume and velocity of data generated by modern airborne sensors lead to significant data overload challenges. Processing, analyzing, and securely transmitting this massive influx of information in real-time, especially in bandwidth-constrained environments, requires highly advanced infrastructure and sophisticated algorithms that are still under development.

Ethical considerations concerning the use of Artificial Intelligence, particularly in autonomous decision-making for lethal operations, present a significant societal and regulatory challenge. Establishing robust frameworks and ensuring human oversight in AI-driven systems is paramount but complex. Supply chain vulnerabilities, especially for critical microelectronics and specialized components from global sources, pose risks to production schedules and national security. The rapid pace of technological obsolescence in the digital realm also means that significant investments in current technologies could become outdated quickly, necessitating continuous and costly upgrades to maintain a technological edge. Overcoming these challenges will require sustained innovation, strategic partnerships, and adaptive policy frameworks.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Interoperability & Legacy System Integration Issues | -1.7% | Global | Short to Long-term (2025-2033) |

| Data Overload & Processing Complexity | -1.4% | Global | Short to Mid-term (2025-2029) |

| Ethical & Regulatory Concerns for AI in Combat | -1.2% | Global (Western Nations) | Mid to Long-term (2027-2033) |

| Supply Chain Vulnerabilities & Geopolitical Dependencies | -1.0% | Global (particularly APAC, North America) | Short to Mid-term (2025-2029) |

| Rapid Technological Obsolescence & Need for Continuous Upgrades | -0.9% | Global | Short to Long-term (2025-2033) |

Airborne Digital Battlefield Market - Updated Report Scope

This market research report offers a comprehensive analysis of the Airborne Digital Battlefield Market, providing detailed insights into its current size, historical performance, and future growth projections. The scope encompasses a thorough examination of market drivers, restraints, opportunities, and challenges, along with an in-depth impact analysis of Artificial Intelligence. The study segments the market by component, platform, application, and technology, delivering granular insights into each category's dynamics. It also highlights regional trends and profiles key industry players, offering a holistic view of the market landscape to aid strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 45.2 Billion |

| Growth Rate | 11.8% CAGR |

| Number of Pages | 257 |

| Key Trends | >|

| Segments Covered | >|

| Key Companies Covered | Broadcom, L3Harris Technologies, Lockheed Martin, Northrop Grumman, Raytheon Technologies (RTX), BAE Systems, Thales Group, Elbit Systems, SAAB AB, General Dynamics, Boeing, Collins Aerospace (RTX), Cubic Corporation, Curtiss-Wright Corporation, Honeywell Aerospace, Rafael Advanced Defense Systems, Leonardo S.p.A., Dassault Aviation, Kratos Defense & Security Solutions, Sierra Nevada Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Airborne Digital Battlefield market is meticulously segmented to provide a granular understanding of its diverse components and applications. This segmentation highlights the various technological solutions, operational platforms, and functional areas that collectively define the digital transformation of aerial warfare. Each segment plays a crucial role in enabling advanced capabilities, from processing vast amounts of battlefield data to ensuring secure, real-time communication across disparate assets. The intricate interdependencies between hardware, software, and services underpin the overall functionality and effectiveness of the modern airborne digital battlefield, reflecting a holistic approach to military modernization.

Understanding these segments is vital for stakeholders to identify key growth areas, technological priorities, and investment opportunities. The breakdown by component provides insight into the infrastructure elements powering digital operations. Platform segmentation reveals the various aerial assets incorporating these digital systems, ranging from advanced fighter jets to sophisticated unmanned aerial vehicles. Application-based segmentation clarifies the specific operational functions enhanced by digital capabilities, such as surveillance, command, and electronic warfare. Finally, technology segmentation highlights the foundational innovations, like AI and cybersecurity, that are driving the market's evolution and shaping future aerial combat scenarios.

- By Component: This segment includes the essential building blocks of the airborne digital battlefield.

- Hardware: Encompasses the physical infrastructure such as processors, servers, displays, antennas, routers, switches, and secure storage units crucial for onboard data processing and connectivity.

- Software: Covers the critical applications and operating systems, including C4ISR software, data analytics software, AI/ML algorithms, cybersecurity solutions, and mission planning tools that enable digital operations.

- Services: Includes vital support functions like system integration, ongoing maintenance and technical support, and comprehensive training and consulting to ensure operational readiness and effective utilization.

- By Platform: This segment categorizes the various aerial vehicles integrating digital battlefield technologies.

- Aircraft: Includes advanced fighter jets, long-range bombers, transport aircraft, and specialized mission aircraft equipped with digital systems for enhanced combat and support roles.

- UAVs (Unmanned Aerial Vehicles): Covers a range from High-Altitude Long Endurance (HALE) and Medium-Altitude Long Endurance (MALE) drones to tactical UAVs and loitering munitions, increasingly operating autonomously within the digital network.

- Satellites: Pertains to communication, reconnaissance, and navigation satellites that provide critical backbone connectivity and data relay capabilities for airborne platforms.

- Helicopters: Includes attack helicopters, utility helicopters, and reconnaissance helicopters integrated with digital systems for enhanced situational awareness and mission effectiveness.

- By Application: This segment outlines the specific military functions and operations benefiting from digital battlefield capabilities.

- Surveillance & Reconnaissance: Involves the collection and analysis of intelligence through advanced sensors and digital processing for real-time situational awareness.

- Command & Control (C2): Focuses on enabling seamless decision-making, tasking, and coordination across airborne assets and joint forces.

- Electronic Warfare (EW): Deals with digital capabilities for jamming, deception, and protection against adversarial electronic threats.

- Navigation & Targeting: Enhances precision in aerial navigation and weapon targeting through advanced digital systems.

- Communication & Networking: Ensures secure, high-bandwidth data exchange and voice communication within the digital battlefield ecosystem.

- Intelligence Gathering: Encompasses the comprehensive collection, processing, and dissemination of various forms of intelligence from airborne platforms.

- By Technology: This segment focuses on the underlying technological innovations driving the market.

- Artificial Intelligence & Machine Learning: Powers autonomous systems, predictive analytics, advanced threat detection, and intelligent decision support.

- Big Data Analytics: Enables the processing and interpretation of vast datasets collected from airborne sensors for actionable insights.

- Cloud & Edge Computing: Facilitates distributed data processing and storage, enhancing resilience and reducing latency for airborne operations.

- Internet of Things (IoT) & Connectivity: Connects various sensors, devices, and platforms into a cohesive digital network.

- Cybersecurity: Provides essential protection for digital systems, networks, and data against sophisticated cyber threats.

- Advanced Sensor Fusion: Integrates data from multiple sensor types to create a more comprehensive and accurate picture of the operational environment.

- Digital Twinning: Involves creating virtual models of physical assets to simulate performance, optimize operations, and predict maintenance needs.

Regional Highlights

- North America: This region dominates the Airborne Digital Battlefield Market, primarily driven by substantial defense expenditures from the United States, continuous technological advancements, and the presence of leading defense contractors and research institutions. The focus on developing next-generation air superiority platforms, integrating AI into combat systems, and advancing networked operations ensures North America remains at the forefront of innovation and adoption.

- Europe: Europe represents a significant market, propelled by ongoing military modernization programs among NATO members and key European nations. There is a strong emphasis on enhancing interoperability, developing collaborative defense capabilities, and investing in advanced C4ISR systems. Nations like the UK, France, and Germany are key contributors, focusing on integrating sophisticated digital solutions into their air forces.

- Asia Pacific (APAC): The APAC region is projected to exhibit the highest growth rate in the Airborne Digital Battlefield Market, fueled by escalating geopolitical tensions, increasing defense budgets in countries like China, India, and Japan, and the rapid adoption of advanced military technologies. The focus on strengthening air defense capabilities and modernizing existing fleets against regional threats is a significant driver.

- Latin America: While a smaller market compared to other regions, Latin America is gradually investing in modernizing its air force capabilities, driven by needs for border security, counter-narcotics operations, and regional stability. Adoption of digital battlefield solutions is selective but growing, often through collaborations or acquisitions from major defense suppliers.

- Middle East & Africa (MEA): The MEA region is a dynamic market influenced by ongoing conflicts, counter-terrorism efforts, and strategic military alliances. Significant defense spending, particularly from Gulf Cooperation Council (GCC) countries, fuels the demand for advanced airborne surveillance, command, and communication systems. The focus is on enhancing aerial intelligence capabilities and strengthening national security.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Airborne Digital Battlefield Market.- Broadcom

- L3Harris Technologies

- Lockheed Martin

- Northrop Grumman

- Raytheon Technologies (RTX)

- BAE Systems

- Thales Group

- Elbit Systems

- SAAB AB

- General Dynamics

- Boeing

- Collins Aerospace (RTX)

- Cubic Corporation

- Curtiss-Wright Corporation

- Honeywell Aerospace

- Rafael Advanced Defense Systems

- Leonardo S.p.A.

- Dassault Aviation

- Kratos Defense & Security Solutions

- Sierra Nevada Corporation

Frequently Asked Questions

Analyze common user questions about the Airborne Digital Battlefield market and generate a concise list of summarized FAQs reflecting key topics and concerns.What defines the Airborne Digital Battlefield Market?

The Airborne Digital Battlefield Market encompasses advanced technologies and systems integrated into airborne platforms to create a networked, data-centric combat environment. It aims to enhance situational awareness, decision-making speed, and operational effectiveness through real-time information exchange, advanced sensors, AI, and secure communications.

What are the primary drivers influencing market growth?

Key drivers include increasing global defense expenditures for military modernization, escalating geopolitical tensions necessitating superior aerial capabilities, advancements in C4ISR technologies, and the strategic shift towards network-centric and multi-domain warfare concepts.

How is Artificial Intelligence transforming this market?

AI significantly impacts the market by enabling enhanced situational awareness through data fusion, facilitating predictive maintenance, powering autonomous navigation, improving threat detection and targeting, and optimizing resource allocation, leading to more intelligent and responsive airborne systems.

Which geographical regions are leading the adoption of Airborne Digital Battlefield technologies?

North America currently leads the market due to significant defense investments and technological innovation. The Asia Pacific region is projected for the highest growth, driven by increasing defense budgets and military modernization efforts, while Europe maintains a strong presence through collaborative defense initiatives.

What are the main challenges faced by the Airborne Digital Battlefield Market?

Major challenges include high development and integration costs, complex interoperability issues with legacy systems, managing vast amounts of data (data overload), critical cybersecurity vulnerabilities, ethical considerations surrounding AI in combat, and the rapid obsolescence of technology.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted