Air Brake Market

Air Brake Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708700 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

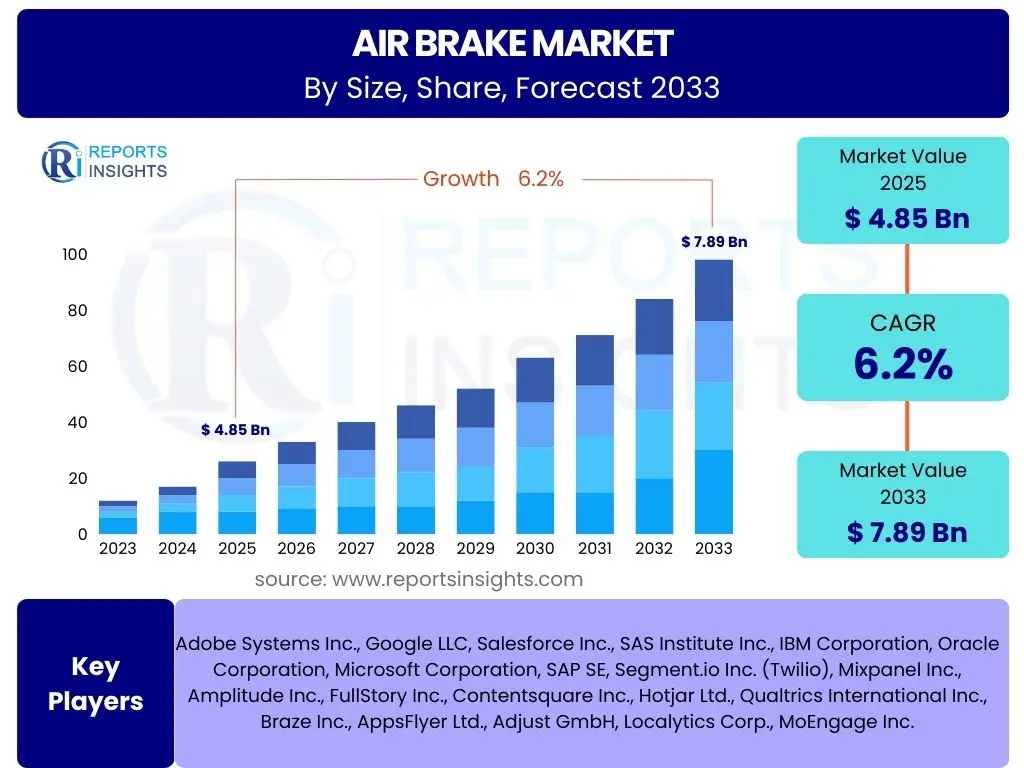

Air Brake Market Size

According to Reports Insights Consulting Pvt Ltd, The Air Brake Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033. The market is estimated at USD 4.85 billion in 2025 and is projected to reach USD 7.89 billion by the end of the forecast period in 2033.

Key Air Brake Market Trends & Insights

Analysis of user inquiries reveals a strong interest in how evolving vehicle technology and stringent safety regulations are shaping the air brake market. Users frequently question the adoption of advanced braking systems, the integration of smart technologies, and the industry's response to sustainability demands. There is also significant curiosity about the impact of electric vehicles and autonomous driving on traditional air brake designs and functionalities. These inquiries highlight a market in flux, driven by innovation and regulatory pressure, moving towards more efficient, safer, and technologically integrated braking solutions.

The market is witnessing a fundamental shift towards more sophisticated and electronically controlled braking systems. This includes the widespread adoption of Electronic Braking Systems (EBS) and advanced Antilock Braking Systems (ABS) that offer superior control and shorter stopping distances compared to conventional pneumatic systems. Furthermore, the push for vehicle electrification is influencing air brake design, with a focus on energy efficiency and seamless integration with electric drivetrains. The ongoing development of lightweight materials also contributes to fuel efficiency and reduced emissions, aligning with global environmental objectives.

- Growing integration of Electronic Braking Systems (EBS) and advanced ABS technology.

- Increased demand for lightweight air brake components to enhance fuel efficiency.

- Development of regenerative braking systems compatible with electric and hybrid vehicles.

- Focus on predictive maintenance solutions through sensor integration and IoT.

- Strict government regulations mandating advanced safety features in commercial vehicles.

- Emergence of intelligent air brake systems capable of communication with ADAS.

- Shift towards modular and standardized air brake system designs for easier maintenance.

AI Impact Analysis on Air Brake

User questions regarding the influence of Artificial Intelligence on air brakes often center on themes such as enhanced safety, predictive maintenance capabilities, and the role of AI in autonomous braking systems. There is considerable interest in how AI algorithms can optimize braking performance, anticipate potential failures, and contribute to the overall reliability of commercial vehicle operations. Concerns are also raised about data security, system complexity, and the regulatory frameworks required for AI-driven safety-critical systems, indicating a desire for robust and trustworthy implementations.

The integration of AI is poised to revolutionize air brake systems by transforming them from purely mechanical or electro-pneumatic components into intelligent, adaptive safety modules. AI algorithms can process vast amounts of data from vehicle sensors, including speed, load, road conditions, and driver inputs, to optimize braking force distribution in real-time, thereby improving stability and reducing stopping distances. This predictive capability extends to maintenance, allowing for early detection of wear and tear, reducing unplanned downtime, and extending component lifespan. As autonomous vehicles advance, AI will be critical in enabling highly responsive and safe automated braking decisions, ensuring seamless interaction within complex operational environments.

- Predictive maintenance for air brake components, anticipating failures before they occur.

- Optimized braking performance through real-time analysis of driving conditions and vehicle load.

- Enhanced safety features by enabling faster response times and precision control in emergency braking.

- Integration with Advanced Driver-Assistance Systems (ADAS) for semi-autonomous and autonomous braking.

- Reduced wear and tear on brake components due to intelligent application of braking force.

- Data analytics for fleet management, providing insights into braking patterns and efficiency.

- Facilitation of adaptive cruise control and collision avoidance systems by intelligent brake actuation.

Key Takeaways Air Brake Market Size & Forecast

Analysis of common user questions regarding the Air Brake market size and forecast highlights a consensus on sustained growth, driven primarily by an increasing global commercial vehicle fleet and stringent safety mandates. Users are keen to understand the primary growth accelerators, such as expanding logistics industries and infrastructure development, particularly in emerging economies. There is also significant attention paid to how technological advancements, including electrification and smart braking systems, will influence market trajectory and valuation over the coming decade.

The market is poised for robust expansion, reflecting the indispensable nature of air brakes in heavy and medium-duty commercial vehicles. Forecasts indicate a steady increase in demand, underpinned by global trade growth, urbanization, and a corresponding rise in freight transportation volumes. While traditional pneumatic systems will continue to hold a substantial share, the projected growth is heavily influenced by the accelerating adoption of advanced electronic and smart braking solutions that offer superior safety, efficiency, and integration capabilities. Strategic investments in research and development by key players will be pivotal in shaping the market's technological landscape and achieving the projected valuations.

- The Air Brake Market is on a clear growth trajectory, projected to exceed USD 7.8 billion by 2033.

- Commercial vehicle production and expanding logistics sectors are primary market growth engines.

- Technological advancements, particularly in EBS and smart braking, are critical for market expansion.

- Emerging economies present significant untapped potential for market penetration and growth.

- Regulatory emphasis on vehicle safety and emissions reduction continues to drive innovation.

- The aftermarket segment is expected to maintain a steady revenue stream due to maintenance needs.

- Integration with electrification and autonomous driving technologies will redefine future market offerings.

Air Brake Market Drivers Analysis

The Air Brake Market is significantly propelled by several key factors that underpin its sustained growth. Paramount among these drivers is the continuous expansion of the global commercial vehicle industry, particularly in developing regions, fueled by economic growth, increased trade activities, and a burgeoning e-commerce sector. Coupled with this, the implementation of more stringent safety regulations worldwide mandates the inclusion of advanced braking systems in new vehicles, creating a non-discretionary demand for sophisticated air brake technologies. Furthermore, technological advancements leading to enhanced performance, durability, and integration with modern vehicle architectures are consistently pushing market demand upwards, offering superior solutions to fleet operators and vehicle manufacturers alike.

These drivers collectively contribute to a favorable market environment. The global surge in urbanization and infrastructure development projects necessitates a larger fleet of heavy-duty vehicles, each requiring reliable and efficient air braking systems. Vehicle manufacturers are increasingly incorporating cutting-on-edge braking solutions to meet regulatory compliance and consumer expectations for safety and operational efficiency. The ongoing innovation in materials science and electronic control units also plays a crucial role, allowing for the development of lighter, more responsive, and more durable air brake components. This continuous cycle of demand, regulation, and technological progression ensures a positive outlook for the air brake market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increase in Commercial Vehicle Production | +1.8% | Asia Pacific, North America, Europe | Short to Mid-term (2025-2029) |

| Stringent Vehicle Safety Regulations | +1.5% | Europe, North America, Asia Pacific (China, India) | Mid to Long-term (2027-2033) |

| Technological Advancements in Braking Systems (EBS, ABS) | +1.3% | Global | Mid to Long-term (2027-2033) |

| Expansion of Logistics and Freight Transportation | +1.0% | Asia Pacific, Latin America, Middle East & Africa | Short to Mid-term (2025-2029) |

| Growing Demand for Electric and Hybrid Commercial Vehicles | +0.8% | Europe, North America, China | Mid to Long-term (2028-2033) |

Air Brake Market Restraints Analysis

Despite its robust growth prospects, the Air Brake Market faces several significant restraints that could temper its expansion. One primary challenge is the high initial cost associated with advanced air braking systems, particularly those integrated with electronic controls and smart technologies. This can be a deterrent for small and medium-sized fleet operators, especially in price-sensitive markets, who may opt for more basic and less expensive alternatives. Another significant restraint is the volatility in raw material prices, such as steel, aluminum, and rubber, which directly impacts manufacturing costs and, consequently, the final product price. Economic downturns and geopolitical instability can further exacerbate these cost pressures and reduce overall demand for new vehicles, subsequently affecting the air brake market.

Furthermore, the complexity of maintaining and repairing sophisticated air brake systems requires specialized expertise and diagnostic tools, leading to higher operational costs for vehicle owners. This complexity also poses a barrier to entry for smaller service providers, centralizing maintenance to authorized dealerships, which may not be readily accessible in all regions. The emergence of alternative braking technologies, particularly hydraulic braking systems for lighter commercial vehicles, also presents a competitive restraint. Lastly, the long replacement cycles for commercial vehicles mean that once an air brake system is installed, it typically remains in service for many years, limiting the recurring sales of new systems to the OEM segment and shifting emphasis to the aftermarket, which operates at different profit margins.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost of Advanced Braking Systems | -0.7% | Developing Regions (Asia Pacific, Latin America, MEA) | Short to Mid-term (2025-2029) |

| Volatility in Raw Material Prices | -0.5% | Global | Short-term (2025-2026) |

| Complexity of Maintenance and Repair | -0.4% | Global (esp. areas with limited specialized technicians) | Mid to Long-term (2027-2033) |

| Long Commercial Vehicle Replacement Cycles | -0.3% | Global | Long-term (2029-2033) |

| Economic Slowdown and Geopolitical Instability | -0.6% | Europe, North America, parts of Asia Pacific | Short to Mid-term (2025-2027) |

Air Brake Market Opportunities Analysis

The Air Brake Market is presented with several promising opportunities that are anticipated to fuel future growth and innovation. The rapid expansion of e-commerce and logistics services globally, especially in emerging economies, necessitates a larger and more efficient fleet of commercial vehicles, thereby increasing demand for air braking systems. Furthermore, the global push towards vehicle electrification and the development of hybrid commercial vehicles open new avenues for specialized air brake systems that can seamlessly integrate with electric powertrains and incorporate regenerative braking functionalities. This technological shift creates a demand for advanced components that are energy-efficient and optimized for new vehicle architectures.

Beyond new vehicle sales, significant opportunities exist in the retrofit and aftermarket segments, driven by the need to upgrade existing commercial vehicle fleets with modern safety and efficiency features. As regulations become stricter and technology advances, many older vehicles will require enhancements to meet new standards. The increasing adoption of Advanced Driver-Assistance Systems (ADAS) and autonomous driving technologies also presents a substantial opportunity, as air brakes are critical components in these systems, requiring sophisticated electronic controls and rapid response capabilities. These developments not only expand the market but also drive innovation in terms of system integration and intelligent functionalities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing E-commerce and Logistics Sector | +1.2% | Asia Pacific, North America, Europe | Short to Mid-term (2025-2029) |

| Electrification and Hybridization of Commercial Vehicles | +1.0% | Europe, North America, China | Mid to Long-term (2027-2033) |

| Integration with Advanced Driver-Assistance Systems (ADAS) | +0.9% | Global | Mid to Long-term (2028-2033) |

| Expansion in Emerging Markets | +0.8% | Latin America, Middle East & Africa, Southeast Asia | Mid to Long-term (2027-2033) |

| Retrofit Market for Advanced Safety Features | +0.7% | North America, Europe | Mid-term (2026-2030) |

Air Brake Market Challenges Impact Analysis

The Air Brake Market encounters several significant challenges that require strategic navigation from industry participants. One prominent challenge is the increasing complexity of integrating air brake systems with various electronic control units (ECUs), ADAS, and emerging autonomous driving platforms. This complexity demands higher precision in manufacturing, sophisticated software development, and seamless interoperability, which can lead to extended development cycles and increased production costs. Furthermore, cybersecurity threats are becoming a critical concern, as connected braking systems could be vulnerable to malicious attacks, potentially compromising vehicle safety and functionality. Ensuring robust cybersecurity measures while maintaining system integrity is an ongoing and evolving challenge for manufacturers.

Another substantial challenge stems from the need for standardization across different vehicle manufacturers and regions. Lack of uniform standards can hinder global market penetration and increase the cost of compliance for multinational players. Additionally, the rapid pace of technological change requires continuous investment in research and development, which can strain resources, particularly for smaller market players. Adapting existing manufacturing processes to accommodate new materials and intelligent components also presents an operational hurdle. Lastly, the availability of a skilled workforce capable of designing, manufacturing, and servicing these advanced systems remains a persistent challenge, particularly as the technology becomes more sophisticated and interconnected.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration Complexity with ADAS and Autonomous Systems | -0.8% | Global | Mid to Long-term (2027-2033) |

| Cybersecurity Risks for Connected Braking Systems | -0.6% | Global | Mid to Long-term (2028-2033) |

| Lack of Standardization Across Regions/OEMs | -0.5% | Global | Long-term (2029-2033) |

| High R&D Investment and Rapid Technological Obsolescence | -0.4% | Global | Mid-term (2026-2030) |

| Shortage of Skilled Workforce for Advanced Systems | -0.3% | North America, Europe, parts of Asia Pacific | Long-term (2029-2033) |

Air Brake Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global Air Brake Market, offering strategic insights into market dynamics, segmentation, regional trends, and competitive landscape from 2019 to 2033. It examines the market size, growth drivers, restraints, opportunities, and challenges, incorporating the latest technological advancements and regulatory impacts. The report aims to equip stakeholders with critical data and forecasts to make informed business decisions, covering detailed breakdowns by component, vehicle type, sales channel, and regional performance. Emphasis is placed on emerging trends such as electrification, intelligent braking systems, and the influence of AI on future market development.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.85 Billion |

| Market Forecast in 2033 | USD 7.89 Billion |

| Growth Rate | 6.2% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Knorr-Bremse, ZF Commercial Vehicle Control Systems (formerly WABCO), Robert Bosch GmbH, Haldex, Bendix Commercial Vehicle Systems LLC, Meritor Inc., BorgWarner Inc. (Delphi Technologies), Continental AG, Sorl Auto Parts, Wabtec Corporation, AxleTech International, Federal-Mogul LLC (Tenneco), SAF-HOLLAND, WABCO India Limited, Accuride Corporation, PACCAR Inc., Tata AutoComp Systems Ltd., Mahindra CIE Automotive Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Air Brake Market is meticulously segmented to provide a granular understanding of its diverse components and applications. These segmentations allow for a detailed analysis of market dynamics, identifying key areas of growth, technological shifts, and consumer preferences across different product categories and end-use sectors. The classifications by type, component, vehicle type, and sales channel offer a comprehensive view, enabling stakeholders to pinpoint specific market opportunities and challenges. This structured approach ensures that the report captures the intricate interplay of various factors driving or restraining market performance.

Understanding these segments is crucial for strategic planning, as each segment exhibits unique growth patterns and demand drivers. For instance, the distinction between disc and drum air brakes highlights the adoption trends for different braking technologies, while the component-level breakdown identifies critical manufacturing and supply chain areas. Similarly, segmenting by vehicle type underscores the varying requirements for heavy-duty versus medium-duty commercial vehicles and trailers, reflecting differing operational demands and regulatory landscapes. The sales channel segmentation further differentiates between original equipment installation and the aftermarket, each representing distinct business models and market dynamics.

- By Type:

- Disc Air Brake: Increasingly preferred for heavy-duty applications due to superior heat dissipation and consistent performance.

- Drum Air Brake: Continues to be widely used, particularly in cost-sensitive markets and for certain vehicle types due to its robust and reliable nature.

- By Component:

- Compressor: Essential for generating compressed air, a critical part of the system.

- Air Tank/Reservoir: Stores compressed air for brake actuation and auxiliary systems.

- Brake Chambers: Convert air pressure into mechanical force to apply the brakes.

- Valves (Foot, Hand, Relay, etc.): Control the flow and pressure of air within the braking system.

- Slack Adjusters: Maintain proper clearance between the brake shoes/pads and the drum/rotor.

- Brake Linings/Pads: Friction materials that engage with the drum or rotor to slow down the vehicle.

- Others: Includes air dryers, hoses, fittings, pressure sensors, and electronic control units (ECUs).

- By Vehicle Type:

- Heavy-Duty Commercial Vehicles (Trucks, Buses): The largest segment, driven by freight and public transport demands.

- Medium-Duty Commercial Vehicles (Trucks, Buses): Significant for local logistics and smaller public transport roles.

- Trailers: Essential for commercial haulage, requiring independent air brake systems.

- By Sales Channel:

- OEM (Original Equipment Manufacturer): Sales to vehicle manufacturers for new vehicle assembly.

- Aftermarket: Replacement parts and components sold for maintenance and repair of existing vehicles.

Regional Highlights

The global Air Brake Market exhibits diverse growth patterns and adoption rates across various geographical regions, influenced by economic development, regulatory frameworks, and commercial vehicle fleet sizes. North America and Europe represent mature markets characterized by stringent safety regulations, high technological adoption, and a strong presence of key market players. These regions are at the forefront of integrating advanced electronic braking systems and exploring AI-driven functionalities. The demand here is largely driven by fleet upgrades, technological mandates, and a robust logistics sector. Meanwhile, Asia Pacific stands out as the fastest-growing market, propelled by rapid industrialization, expanding e-commerce, and increasing commercial vehicle production in countries like China and India. The sheer volume of new vehicle sales and the ongoing infrastructure development projects in this region create immense opportunities for air brake manufacturers.

Latin America and the Middle East & Africa regions are also witnessing gradual growth, primarily due to economic recovery, investment in infrastructure, and the expansion of trade activities. While these markets may lag in terms of immediate technological adoption compared to developed regions, they offer significant potential for basic and mid-range air braking systems, particularly as safety standards slowly evolve and local manufacturing capabilities improve. The dynamics across these regions underscore the global nature of the air brake market, with different areas presenting distinct opportunities and challenges that require tailored strategic approaches for market penetration and sustainable growth.

- North America: A mature market with high adoption of advanced braking systems, driven by strict safety regulations and technological innovation in heavy-duty trucks and buses.

- Europe: Leading in the implementation of advanced electronic braking systems (EBS) and sustainable transport solutions, with strong regulatory impetus for safety and emissions.

- Asia Pacific: The fastest-growing region due to increasing commercial vehicle production, rapid industrialization, and infrastructure development in countries like China and India.

- Latin America: Emerging market with growth spurred by expanding logistics, mining activities, and the gradual upgrade of commercial vehicle fleets.

- Middle East & Africa (MEA): Growing steadily with investments in transport infrastructure and increasing demand for commercial vehicles across various sectors, though technology adoption is slower.

- China: Dominant in Asia Pacific, being the largest manufacturer and consumer of commercial vehicles, driving massive demand for air brakes.

- India: Experiencing significant growth in its commercial vehicle sector, leading to increased demand for air brake systems, especially in the aftermarket.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Air Brake Market.- Knorr-Bremse

- ZF Commercial Vehicle Control Systems (formerly WABCO)

- Robert Bosch GmbH

- Haldex

- Bendix Commercial Vehicle Systems LLC

- Meritor Inc.

- BorgWarner Inc. (Delphi Technologies)

- Continental AG

- Sorl Auto Parts

- Wabtec Corporation

- AxleTech International

- Federal-Mogul LLC (Tenneco)

- SAF-HOLLAND

- WABCO India Limited

- Accuride Corporation

- PACCAR Inc.

- Tata AutoComp Systems Ltd.

- Mahindra CIE Automotive Limited

Frequently Asked Questions

What is an air brake system?

An air brake system is a type of friction brake for vehicles, primarily heavy commercial vehicles, that uses compressed air to operate the brakes. It typically consists of a compressor, air tanks, control valves, and brake chambers that convert air pressure into mechanical force to engage brake shoes or pads.

How large is the global Air Brake Market expected to be by 2033?

The global Air Brake Market is projected to reach an estimated value of USD 7.89 billion by the end of 2033, growing at a Compound Annual Growth Rate (CAGR) of 6.2% from 2025.

What are the primary drivers for the Air Brake Market growth?

Key drivers include the increase in global commercial vehicle production, stringent vehicle safety regulations, continuous technological advancements in braking systems like EBS and ABS, and the expansion of the logistics and freight transportation sectors worldwide.

How is AI impacting the Air Brake Market?

AI is transforming air brake systems by enabling predictive maintenance, optimizing braking performance through real-time data analysis, enhancing safety features for faster response, and facilitating integration with Advanced Driver-Assistance Systems (ADAS) and autonomous driving functionalities.

Which regions are leading the growth in the Air Brake Market?

Asia Pacific is the fastest-growing region, driven by significant commercial vehicle production and industrialization, while North America and Europe remain key markets due to high technological adoption and strict safety mandates.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted