Aerospace and Defense C class Part Market

Aerospace and Defense C class Part Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705939 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

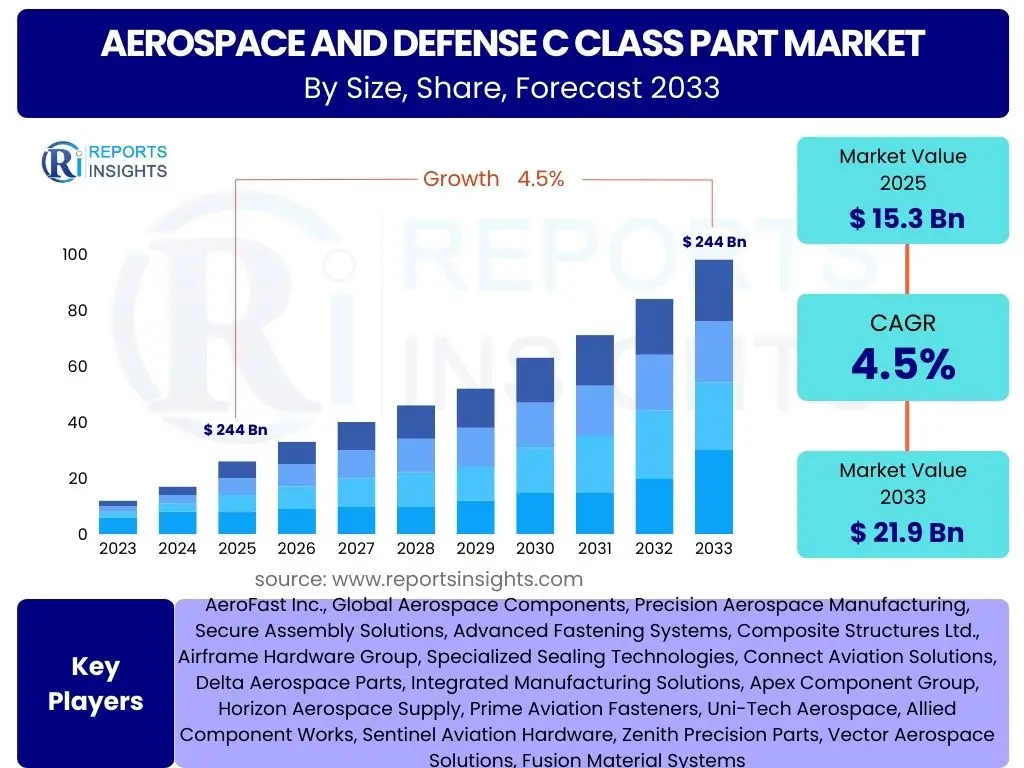

Aerospace and Defense C class Part Market Size

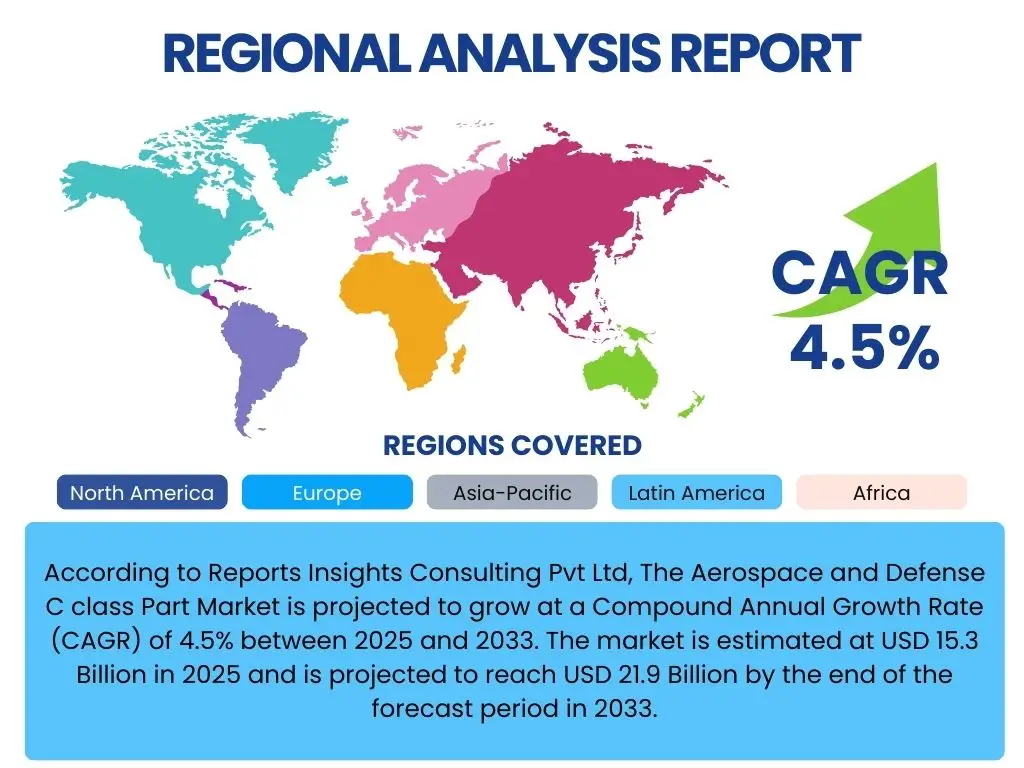

According to Reports Insights Consulting Pvt Ltd, The Aerospace and Defense C class Part Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033. The market is estimated at USD 15.3 Billion in 2025 and is projected to reach USD 21.9 Billion by the end of the forecast period in 2033.

Key Aerospace and Defense C class Part Market Trends & Insights

Market stakeholders and industry participants frequently seek comprehensive understanding of the evolving landscape within the Aerospace and Defense C-class Part sector. Common inquiries address the adoption of advanced manufacturing technologies, the increasing focus on supply chain resilience, and the strategic implications of digitalization across the value chain. There is a strong interest in how sustainability initiatives and the development of new materials are impacting design, production, and procurement processes for these essential components. Furthermore, questions often arise regarding the influence of global geopolitical shifts and defense budget allocations on the overall demand and market dynamics.

The market is witnessing a profound transformation driven by the imperative to enhance operational efficiency, reduce lead times, and ensure robust component availability. This includes a significant shift towards localized supply chains and collaborative manufacturing models to mitigate external vulnerabilities. The demand for lightweight, high-performance C-class parts is consistently rising, propelled by the ongoing development of next-generation aircraft and the stringent requirements of modern defense systems. Innovation in material science and processing techniques is therefore paramount, as is the integration of predictive analytics for optimized maintenance and component life cycle management.

- Increased adoption of Additive Manufacturing (3D Printing) for complex geometries and rapid prototyping.

- Growing emphasis on supply chain digitalization and transparency through blockchain and IoT.

- Development and utilization of advanced, lightweight materials for enhanced performance and fuel efficiency.

- Escalating demand for maintenance, repair, and overhaul (MRO) C-class parts driven by aging aircraft fleets.

- Integration of smart C-class parts with embedded sensors for real-time performance monitoring.

- Strict regulatory compliance and certification requirements driving demand for high-reliability components.

- Strategic localization of manufacturing to reduce geopolitical supply chain risks.

AI Impact Analysis on Aerospace and Defense C class Part

Users frequently inquire about the transformative potential and practical applications of Artificial Intelligence (AI) within the Aerospace and Defense C-class Part domain. Common questions pertain to how AI can optimize design processes, enhance manufacturing precision, and improve quality control for these critical components. There is also significant interest in AI's role in predictive maintenance, inventory management, and strengthening the overall supply chain resilience for C-class parts, addressing concerns about lead times and component availability. Stakeholders aim to understand the tangible benefits, implementation challenges, and ethical considerations associated with AI adoption in this highly regulated industry.

The integration of AI in the C-class parts market is primarily focused on achieving higher levels of automation, precision, and efficiency across the product lifecycle. AI-driven generative design tools are enabling the creation of optimized component geometries that reduce material usage and improve structural integrity. In manufacturing, AI-powered robotics and vision systems are enhancing assembly accuracy and accelerating inspection processes, significantly reducing defects. Furthermore, AI algorithms are being deployed to analyze vast datasets from operational aircraft, predicting component failures and enabling proactive maintenance, thereby extending the lifespan of C-class parts and minimizing downtime. This intelligent automation contributes to cost savings and improved safety within the aerospace and defense sectors.

- Optimized component design through AI-powered generative design tools, leading to lighter and stronger parts.

- Enhanced quality inspection and defect detection using AI-driven vision systems in manufacturing.

- Predictive maintenance analytics for C-class parts, reducing unplanned downtime and extending component lifespan.

- Automated inventory management and supply chain optimization for improved part availability and reduced logistics costs.

- Robotics and automation integration in C-class part assembly and manufacturing, increasing precision and efficiency.

- Development of digital twins for real-time monitoring and simulation of C-class part performance.

- Faster material characterization and selection for C-class parts using AI-driven material science.

Key Takeaways Aerospace and Defense C class Part Market Size & Forecast

Industry professionals and investors consistently seek concise, actionable insights regarding the future trajectory of the Aerospace and Defense C-class Part market. Primary inquiries center on the core factors driving its expansion, the potential for technological disruption, and the segments poised for significant growth. There is a strong desire to understand the macro-economic and geopolitical influences that could shape the market's performance, along with the strategic implications for businesses operating within this specialized sector. The focus is on identifying lucrative opportunities and critical challenges to inform long-term planning and investment decisions.

The Aerospace and Defense C-class Part market is anticipated to exhibit steady growth, primarily fueled by the increasing global demand for new aircraft, both commercial and military, and the continuous need for MRO activities. Technological advancements, particularly in additive manufacturing and advanced materials, are poised to transform production methodologies and part capabilities, creating new market segments. While geopolitical tensions and supply chain volatility present notable challenges, the underlying growth drivers related to fleet modernization, defense spending, and aerospace innovation are expected to sustain market expansion. Companies prioritizing efficiency, digital integration, and supply chain resilience are best positioned to capitalize on emerging opportunities.

- Consistent growth projected due to rising aircraft deliveries and sustained MRO demand.

- Technological advancements, particularly in additive manufacturing, will redefine production and part capabilities.

- The market is driven by both commercial aviation expansion and increasing global defense spending.

- Supply chain resilience and localized production are becoming critical competitive differentiators.

- Sustainability initiatives are influencing material choices and manufacturing processes for C-class parts.

- Digital transformation across the aerospace value chain is enhancing efficiency and traceability of components.

- North America and Asia Pacific are expected to remain key growth regions due to robust aerospace industries.

Aerospace and Defense C class Part Market Drivers Analysis

The growth of the Aerospace and Defense C-class Part market is fundamentally propelled by several interconnected factors. A primary driver is the robust demand for new aircraft from commercial airlines and the continuous modernization efforts within global military forces. This necessitates a steady supply of precision-engineered C-class parts for initial aircraft assembly. Furthermore, the extensive maintenance, repair, and overhaul (MRO) activities required for aging aircraft fleets worldwide represent a significant and enduring source of demand for replacement C-class components, ensuring the ongoing airworthiness and operational safety of existing fleets.

Technological advancements also serve as a crucial catalyst, with innovations in materials science, manufacturing processes like additive manufacturing, and digital design tools leading to the development of higher-performance, lighter, and more durable C-class parts. These innovations enable aircraft manufacturers to achieve better fuel efficiency and reduced operational costs. Additionally, the increasing complexity of modern aircraft systems, including advanced avionics and intricate mechanical assemblies, escalates the demand for a diverse range of specialized C-class parts, each engineered to meet stringent performance and reliability standards in demanding operational environments.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Aircraft Deliveries | +1.5% | North America, Asia Pacific, Europe | Long-term (2025-2033) |

| Growing MRO Activities Worldwide | +1.2% | Global | Continuous |

| Rising Defense Spending and Modernization Programs | +0.8% | North America, Europe, Middle East & Africa | Mid to Long-term |

| Advancements in Materials and Manufacturing Technologies | +0.7% | Global, particularly developed economies | Ongoing, Transformative |

| Demand for Lightweight and Fuel-Efficient Aircraft | +0.5% | Global | Long-term |

Aerospace and Defense C class Part Market Restraints Analysis

Despite robust growth drivers, the Aerospace and Defense C-class Part market faces significant restraints that can impede its expansion. One prominent challenge is the inherent volatility of raw material prices, such as aluminum, titanium, and specialized alloys. Fluctuations in these commodity markets directly impact manufacturing costs for C-class parts, potentially leading to increased end-product prices and impacting profitability for suppliers. Furthermore, the highly complex and often geographically dispersed global supply chains for aerospace components introduce vulnerabilities, including geopolitical tensions, trade disputes, and natural disasters, which can cause significant disruptions and delays in part delivery.

Another critical restraint involves stringent regulatory compliance and lengthy certification processes. Aerospace and defense C-class parts must adhere to extremely rigorous quality, safety, and performance standards (e.g., AS9100, NADCAP). Obtaining and maintaining these certifications is time-consuming and expensive, posing a significant barrier to entry for new players and adding to the cost burden for existing manufacturers. The industry also grapples with a shortage of skilled labor, particularly in specialized manufacturing processes and precision engineering, which can limit production capacity and innovation, potentially leading to delays in meeting market demand and driving up labor costs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.9% | Global | Continuous |

| Stringent Regulatory and Certification Processes | -0.8% | Global, especially North America, Europe | Long-term |

| Supply Chain Disruptions and Geopolitical Instability | -0.7% | Global | Mid-term |

| Shortage of Skilled Workforce and Talent | -0.5% | North America, Europe, Asia Pacific | Long-term |

| High Research and Development Costs | -0.3% | Global | Continuous |

Aerospace and Defense C class Part Market Opportunities Analysis

Significant opportunities exist within the Aerospace and Defense C-class Part market, primarily driven by the ongoing shift towards advanced manufacturing technologies. The increasing adoption of additive manufacturing (3D printing) offers the potential for rapid prototyping, production of complex geometries, and on-demand manufacturing of specialized C-class parts. This technology can significantly reduce lead times, minimize material waste, and enable the creation of optimized parts that are lighter and stronger, thereby enhancing aircraft performance. Furthermore, the digitalization of the entire supply chain through technologies like IoT, AI, and blockchain presents an opportunity to improve transparency, traceability, and efficiency, addressing historical challenges related to inventory management and component authenticity.

Emerging markets, particularly in Asia Pacific and Latin America, present substantial growth opportunities due to expanding commercial aviation sectors and increasing defense investments. As these regions develop their aerospace capabilities and acquire new aircraft, the demand for both initial C-class parts and subsequent MRO components will rise considerably. Additionally, the growing emphasis on sustainability across the aerospace industry creates a demand for C-class parts made from eco-friendly materials or through environmentally conscious manufacturing processes. Companies that invest in green technologies and sustainable production methods can gain a competitive advantage and capture a segment of this evolving market, aligning with global environmental objectives.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Additive Manufacturing (3D Printing) | +1.1% | Global | Long-term (2025-2033) |

| Digitalization of Supply Chains (IoT, Blockchain) | +0.9% | Global | Mid to Long-term |

| Growing Demand from Emerging Markets | +0.8% | Asia Pacific, Latin America, Middle East | Long-term |

| Focus on Sustainable Materials and Production | +0.6% | North America, Europe | Mid to Long-term |

| Modernization and Upgrade of Legacy Aircraft | +0.5% | Global | Continuous |

Aerospace and Defense C class Part Market Challenges Impact Analysis

The Aerospace and Defense C-class Part market is confronted by several complex challenges that necessitate strategic responses from industry players. Geopolitical instability and trade protectionism pose significant threats, as they can disrupt international supply chains, restrict access to critical materials, and impact market demand through changes in defense policies or trade agreements. The highly interconnected nature of the global aerospace supply chain makes it particularly vulnerable to such external shocks, leading to increased lead times and procurement complexities. Additionally, the constant threat of cyberattacks targeting intellectual property and operational systems presents a considerable risk, demanding robust cybersecurity measures to protect sensitive design data and manufacturing processes.

Another pressing challenge is managing the intricate balance between cost efficiency and the uncompromised quality and reliability required for aerospace components. C-class parts, though small, are critical for aircraft safety and performance, meaning any compromise in quality is unacceptable. This mandates rigorous quality control, extensive testing, and high manufacturing precision, which can drive up production costs. Furthermore, complying with evolving environmental regulations and achieving sustainability goals, such as reducing carbon footprints and managing waste, adds another layer of complexity to manufacturing processes. Companies must invest in cleaner technologies and sustainable practices while maintaining competitive pricing, which is a significant operational and financial hurdle.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Geopolitical Instability and Trade Protectionism | -1.0% | Global | Mid-term |

| Ensuring Quality and Reliability Amid Cost Pressures | -0.8% | Global | Continuous |

| Supply Chain Resilience and Risk Management | -0.7% | Global | Long-term |

| Cybersecurity Threats and Data Protection | -0.6% | Global | Continuous |

| Meeting Evolving Environmental and Sustainability Regulations | -0.4% | North America, Europe | Long-term |

Aerospace and Defense C class Part Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Aerospace and Defense C-class Part market, covering historical data, current market dynamics, and future growth projections from 2025 to 2033. It offers a detailed examination of market size, trends, drivers, restraints, opportunities, and challenges influencing the industry. The report also includes an exhaustive segmentation analysis across various types, materials, applications, and end-uses, providing granular insights into key market components. Furthermore, it delivers a thorough regional analysis, identifying prominent growth markets and their unique characteristics, alongside a competitive landscape assessment featuring profiles of leading market participants and an AI impact analysis to highlight technological influences.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.3 Billion |

| Market Forecast in 2033 | USD 21.9 Billion |

| Growth Rate | 4.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | AeroFast Inc., Global Aerospace Components, Precision Aerospace Manufacturing, Secure Assembly Solutions, Advanced Fastening Systems, Composite Structures Ltd., Airframe Hardware Group, Specialized Sealing Technologies, Connect Aviation Solutions, Delta Aerospace Parts, Integrated Manufacturing Solutions, Apex Component Group, Horizon Aerospace Supply, Prime Aviation Fasteners, Uni-Tech Aerospace, Allied Component Works, Sentinel Aviation Hardware, Zenith Precision Parts, Vector Aerospace Solutions, Fusion Material Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Aerospace and Defense C-class Part market is meticulously segmented to provide a granular understanding of its diverse components and dynamics. This segmentation facilitates detailed analysis of market performance across various dimensions, enabling stakeholders to identify specific growth areas and strategic opportunities. The classification by type encompasses the wide array of small, critical components, including fasteners, seals, connectors, and other standard hardware, each serving distinct functional requirements within aircraft and defense systems. This delineation helps in understanding the demand patterns and technological advancements specific to each category of C-class parts.

Further segmentation by material, application, and end-use provides deeper insights into the technological evolution and supply chain dynamics of the market. The material segment examines the use of traditional metals, advanced composites, and polymers, reflecting the ongoing pursuit of lightweight and high-performance solutions. Application-based segmentation highlights the demand across key aircraft sections like airframes, engines, interiors, and avionics, showcasing where specific C-class parts are most crucial. Finally, end-use segmentation differentiates demand from original equipment manufacturers (OEMs), maintenance, repair, and overhaul (MRO) providers, and the aftermarket, illustrating the varying requirements and procurement cycles across the value chain. This comprehensive segmentation is crucial for targeted market strategies and product development.

- By Type: Fasteners, Seals, Connectors, Standard Hardware, Others.

- By Material: Metals (Aluminum Alloys, Titanium Alloys, Stainless Steel, High-Performance Alloys), Composites, Polymers, Ceramics, Others.

- By Application: Airframe, Engine, Interior, Avionics, Landing Gear, Hydraulics.

- By End-Use: Original Equipment Manufacturers (OEMs), Maintenance, Repair, and Overhaul (MRO), Aftermarket.

- By Platform: Commercial Aircraft, Military Aircraft, Helicopters, Spacecraft, Unmanned Aerial Vehicles (UAVs).

Regional Highlights

- North America: Expected to maintain a dominant share due to the presence of major aerospace OEMs, high defense spending, and advanced R&D capabilities in the United States. Significant demand from commercial and military aircraft production and MRO activities.

- Europe: A key market driven by established aerospace players like Airbus, robust defense budgets, and a strong focus on sustainable aviation technologies. Countries such as France, Germany, and the UK are prominent contributors.

- Asia Pacific (APAC): Projected to be the fastest-growing region, fueled by expanding commercial airline fleets, increasing air passenger traffic, and rising defense expenditures in countries like China, India, and Japan. Investment in local aerospace manufacturing capabilities is also increasing.

- Latin America: Showing steady growth influenced by fleet modernization initiatives and new aircraft acquisitions, though at a comparatively slower pace than APAC. Brazil stands out as a significant regional player.

- Middle East and Africa (MEA): Experiencing growth driven by substantial investments in new aircraft by prominent airlines and increasing defense spending, particularly in the Middle East, along with strategic geographic positioning for MRO hubs.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aerospace and Defense C class Part Market.- AeroFast Inc.

- Global Aerospace Components

- Precision Aerospace Manufacturing

- Secure Assembly Solutions

- Advanced Fastening Systems

- Composite Structures Ltd.

- Airframe Hardware Group

- Specialized Sealing Technologies

- Connect Aviation Solutions

- Delta Aerospace Parts

- Integrated Manufacturing Solutions

- Apex Component Group

- Horizon Aerospace Supply

- Prime Aviation Fasteners

- Uni-Tech Aerospace

- Allied Component Works

- Sentinel Aviation Hardware

- Zenith Precision Parts

- Vector Aerospace Solutions

- Fusion Material Systems

Frequently Asked Questions

What is the projected growth rate for the Aerospace and Defense C-class Part market?

The Aerospace and Defense C-class Part market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033, reaching an estimated USD 21.9 Billion by 2033.

What are the primary drivers of the Aerospace and Defense C-class Part market?

Key drivers include increasing global aircraft deliveries, rising maintenance, repair, and overhaul (MRO) activities for aging fleets, growing defense spending, and continuous advancements in materials and manufacturing technologies like additive manufacturing.

How does AI impact the Aerospace and Defense C-class Part market?

AI impacts the market by optimizing component design, enhancing quality inspection, enabling predictive maintenance for parts, and improving supply chain efficiency through automation and data analytics, leading to more precise and durable components.

Which regions are key contributors to the Aerospace and Defense C-class Part market?

North America and Europe are significant mature markets due to established aerospace industries and high defense budgets, while Asia Pacific is projected to be the fastest-growing region driven by expanding commercial aviation and defense investments.

What are the main challenges faced by the Aerospace and Defense C-class Part market?

Major challenges include volatile raw material prices, stringent regulatory and certification processes, potential supply chain disruptions due to geopolitical instability, managing cost pressures while maintaining high quality standards, and cybersecurity threats to intellectual property.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted