Advertising Market

Advertising Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706502 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Advertising Market Size

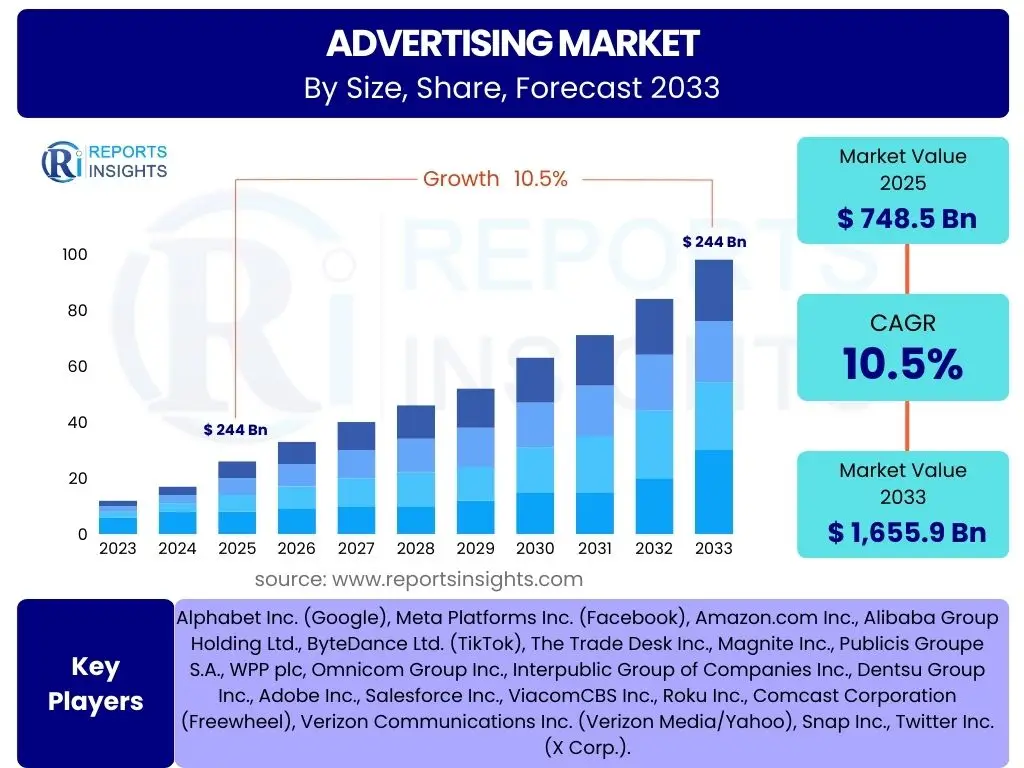

According to Reports Insights Consulting Pvt Ltd, The Advertising Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at US$ 748.5 Billion in 2025 and is projected to reach US$ 1,655.9 Billion by the end of the forecast period in 2033.

Key Advertising Market Trends & Insights

The advertising market is currently undergoing a profound transformation, driven primarily by the rapid advancement of digital technologies and shifting consumer behaviors. A key trend involves the pervasive adoption of data-driven advertising strategies, enabling brands to achieve hyper-personalization and highly targeted campaigns that resonate more effectively with specific audience segments. This shift is moving away from traditional mass media approaches towards more individualized and measurable digital engagements.

Another significant insight points to the increasing dominance of video and mobile advertising formats, fueled by the widespread consumption of content on smartphones and streaming platforms. Furthermore, the rise of retail media networks and connected TV (CTV) advertising presents new avenues for brands to reach consumers directly at the point of purchase or within premium content environments, blurring the lines between commerce and content. Concurrently, privacy regulations and the deprecation of third-party cookies are compelling advertisers to innovate in privacy-preserving measurement and targeting methods, emphasizing first-party data strategies and contextual advertising.

- Digital transformation and data-driven personalization are paramount.

- Video and mobile advertising dominate spending across platforms.

- Emergence of retail media networks and connected TV (CTV) advertising.

- Increasing focus on first-party data and privacy-centric solutions.

- Integration of influencer marketing and authentic content strategies.

- Growth of programmatic advertising across new channels.

AI Impact Analysis on Advertising

Artificial intelligence is profoundly reshaping the advertising landscape, with users frequently querying its capabilities in automation, personalization, and efficiency. AI algorithms are increasingly being deployed to automate laborious tasks such as campaign management, bid optimization, and ad creative generation, thereby freeing up human resources for strategic decision-making. The ability of AI to process vast datasets enables unprecedented levels of audience segmentation and predictive analytics, allowing advertisers to anticipate consumer behavior and deliver highly relevant messages at optimal moments.

Concerns often revolve around the ethical implications of AI in targeting, data privacy, and the potential for algorithmic bias, leading to calls for greater transparency and accountability. However, the overarching expectation is that AI will continue to enhance campaign performance by optimizing spend, improving ad relevance, and delivering measurable ROI. From content creation to fraud detection, AI is becoming an indispensable tool for advertisers aiming to achieve greater precision and scale in their operations, marking a pivotal shift towards intelligent advertising systems.

- Automated campaign management and real-time bid optimization.

- Hyper-personalization of ad content and targeting at scale.

- Enhanced predictive analytics for audience behavior and campaign performance.

- Generative AI for ad copy, visual assets, and video creation.

- Improved fraud detection and brand safety measures.

- Streamlined A/B testing and optimization processes.

Key Takeaways Advertising Market Size & Forecast

The advertising market is on a robust growth trajectory, primarily driven by an accelerated shift towards digital channels and innovative ad technologies. A significant takeaway is the consistent investment across various digital formats, with mobile and video continuing to be primary growth engines. This indicates a sustained confidence in digital platforms for reaching increasingly connected consumers and achieving measurable campaign outcomes, underlining the dynamic nature of consumer media consumption.

Another crucial insight is the growing emphasis on performance-based advertising and measurable ROI, compelling advertisers to adopt more sophisticated analytics and attribution models. The forecast demonstrates not just expansion, but also a fundamental re-alignment of advertising spend towards channels offering higher engagement and conversion potential. This highlights a strategic pivot in the industry towards efficiency, data utility, and integrated customer experiences, signifying a mature yet evolving market.

- Consistent double-digit growth driven by digital adoption.

- Mobile and video advertising are key growth catalysts.

- Increased focus on performance marketing and ROI measurement.

- Significant investment in programmatic and automated ad buying.

- Emerging markets contributing substantially to global expansion.

Advertising Market Drivers Analysis

The global advertising market is propelled by a confluence of technological advancements, evolving consumer behaviors, and strategic business imperatives. A primary driver is the accelerating digital transformation across industries, which has led to increased internet penetration and smartphone adoption worldwide. This pervasive connectivity enables advertisers to reach vast and diverse audiences through a multitude of digital channels, from social media and search engines to streaming platforms and mobile applications, fostering an environment ripe for targeted and interactive advertising campaigns.

Furthermore, the exponential growth of e-commerce has significantly boosted advertising spend. As more retail transactions shift online, businesses are allocating larger portions of their marketing budgets to digital advertising to drive traffic, acquire customers, and build brand presence in the digital storefront. The ability to directly attribute sales to specific ad campaigns in the e-commerce ecosystem provides a strong incentive for increased investment. Additionally, the proliferation of data analytics tools allows advertisers to leverage vast amounts of consumer data, enabling highly personalized and efficient campaigns that yield higher returns on investment and thus encourage greater expenditure.

Finally, the growing sophistication of programmatic advertising technologies has made ad buying and selling more efficient and effective. These platforms automate the process of ad placement, enabling real-time bidding and precise targeting, which maximizes the impact of advertising budgets. The continuous innovation in ad formats, such as immersive experiences (AR/VR ads) and interactive content, also drives consumer engagement and advertiser interest, contributing to the sustained expansion of the market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Digitalization & Internet Penetration | +2.5% | Global, particularly APAC & Latin America | Long-term (2025-2033) |

| Growth of E-commerce & Online Shopping | +2.0% | Global, especially North America & Asia Pacific | Mid to Long-term (2025-2033) |

| Advancements in Data Analytics & AI for Targeting | +1.8% | North America, Europe, Asia Pacific | Mid to Long-term (2025-2033) |

| Rise of Mobile & Video Content Consumption | +1.5% | Global | Long-term (2025-2033) |

| Increased Adoption of Programmatic Advertising | +1.2% | North America, Europe, China | Mid-term (2025-2029) |

Advertising Market Restraints Analysis

Despite robust growth, the advertising market faces several significant restraints that could temper its expansion. One of the most prominent challenges is the increasing stringency of data privacy regulations worldwide, such as GDPR in Europe and CCPA in California. These regulations impose strict rules on data collection, usage, and consent, leading to complexities in audience targeting, data management, and personalized advertising. Advertisers must navigate a fragmented regulatory landscape, which often requires significant investments in compliance, potentially reducing marketing efficiency and increasing operational costs.

Another key restraint is the prevalence of ad fraud, including bot traffic, click farms, and impression fraud. This fraudulent activity siphons off a substantial portion of advertising budgets, leading to wasted spend and inaccurate performance metrics. While industry efforts are underway to combat ad fraud, it remains a persistent issue that erodes advertiser confidence and necessitates continuous investment in verification technologies. Furthermore, the widespread adoption of ad-blocking software by consumers directly impacts ad impression delivery and revenue for publishers and advertisers, particularly in digital channels, forcing a reconsideration of ad delivery methods and formats.

Economic uncertainties and downturns also pose a significant restraint on advertising market growth. During periods of economic contraction, businesses typically reduce discretionary spending, with advertising budgets often being among the first to be cut. This reduction in demand directly impacts ad revenues across all media channels. Moreover, growing consumer ad fatigue and a general aversion to intrusive advertising experiences can lead to reduced engagement rates and a diminished return on ad spend, compelling advertisers to seek less disruptive and more value-driven communication strategies.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Data Privacy Regulations (e.g., GDPR, CCPA) | -1.5% | Europe, North America | Long-term (2025-2033) |

| Prevalence of Ad Fraud & Brand Safety Concerns | -1.2% | Global | Long-term (2025-2033) |

| Rising Adoption of Ad-Blocking Software | -0.8% | Global | Mid to Long-term (2025-2033) |

| Economic Volatility & Recessions | -0.7% | Global | Short-term (2025-2027), Cyclical |

| Consumer Ad Fatigue & Intrusive Ad Experiences | -0.5% | Global | Long-term (2025-2033) |

Advertising Market Opportunities Analysis

The advertising market is ripe with opportunities driven by technological innovation and evolving media consumption habits. A significant opportunity lies in the continued expansion of Connected TV (CTV) advertising, which offers advertisers the ability to deliver targeted ads within premium streaming video content on smart TVs and connected devices. This segment combines the reach of traditional television with the targeting and measurement capabilities of digital, presenting a powerful new avenue for brands to engage with audiences in their living rooms.

Another burgeoning opportunity is the emergence and rapid growth of retail media networks. Major retailers are leveraging their vast first-party consumer data and e-commerce platforms to offer advertising space to brands, both on their own digital properties and increasingly off-site. This allows brands to reach consumers directly at the point of purchase, with highly relevant ads based on purchase history and intent, leading to higher conversion rates and a strong return on investment. The ability to close the loop on attribution directly within the retail ecosystem makes this an increasingly attractive channel.

Furthermore, the advancements in AI and machine learning are creating unprecedented opportunities for hyper-personalization and automation in advertising. AI-driven tools can now generate highly customized ad creatives, optimize campaign performance in real-time, and predict consumer responses with greater accuracy. This enables advertisers to move beyond broad segmentation to truly individualized messaging, enhancing engagement and effectiveness. The shift towards immersive advertising experiences, such as augmented reality (AR) and virtual reality (VR) ads, also presents a novel opportunity for brands to create deeper, more interactive connections with consumers, providing memorable and impactful brand experiences.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Connected TV (CTV) Advertising | +1.8% | North America, Europe, Asia Pacific | Mid to Long-term (2025-2033) |

| Expansion of Retail Media Networks | +1.5% | North America, Europe, Emerging APAC | Mid to Long-term (2025-2033) |

| Advanced AI-driven Hyper-Personalization | +1.3% | Global | Long-term (2025-2033) |

| Programmatic Audio & Podcast Advertising | +1.0% | North America, Europe | Mid-term (2025-2029) |

| Development of Immersive (AR/VR) Advertising | +0.8% | Global, particularly developed markets | Long-term (2028-2033) |

Advertising Market Challenges Impact Analysis

The advertising market faces several critical challenges that demand strategic adaptation and continuous innovation. One significant challenge is the complexity of cross-platform measurement and attribution. As consumers interact with brands across a multitude of devices and channels—from linear TV and social media to mobile apps and in-store experiences—accurately attributing conversions and ROI to specific ad touchpoints becomes increasingly difficult. This fragmentation complicates budget allocation and makes it harder for advertisers to justify spending, hindering optimal campaign performance.

Another pressing challenge is the impending deprecation of third-party cookies, primarily driven by browser changes and privacy regulations. The reliance on third-party cookies for audience targeting, tracking, and measurement has been foundational for digital advertising for decades. Their removal necessitates a fundamental rethinking of how advertisers identify and reach their audiences, pushing the industry towards alternative solutions like first-party data strategies, contextual targeting, and privacy-enhancing technologies such as clean rooms, which require significant investment and adaptation.

Furthermore, maintaining brand safety and combating misinformation in an increasingly vast and rapidly evolving digital content landscape presents a continuous challenge. Brands are highly sensitive to the environments in which their ads appear, striving to avoid association with inappropriate, harmful, or misleading content. Ensuring brand suitability across programmatic channels, particularly on user-generated content platforms, requires sophisticated verification tools and vigilant monitoring. The talent gap in ad-tech and data science also poses a challenge, as the industry struggles to find skilled professionals capable of navigating complex platforms, leveraging advanced analytics, and developing innovative solutions for the future of advertising.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cross-Platform Measurement & Attribution Complexity | -1.0% | Global | Long-term (2025-2033) |

| Deprecation of Third-Party Cookies | -1.5% | Global, especially North America & Europe | Mid-term (2025-2027) |

| Brand Safety & Misinformation Concerns | -0.9% | Global | Long-term (2025-2033) |

| Talent Shortage in Ad-Tech & Data Science | -0.7% | North America, Europe, Developed Asia | Long-term (2025-2033) |

| Increasing Consumer Privacy Expectations | -0.6% | Global | Long-term (2025-2033) |

Advertising Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global advertising market, covering historical performance, current dynamics, and future projections. The scope encompasses detailed market sizing, segmentation analysis across various dimensions, regional insights, and an assessment of the competitive landscape. It aims to deliver actionable intelligence for stakeholders navigating the evolving advertising ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | US$ 748.5 Billion |

| Market Forecast in 2033 | US$ 1,655.9 Billion |

| Growth Rate | 10.5% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Alphabet Inc. (Google), Meta Platforms Inc. (Facebook), Amazon.com Inc., Alibaba Group Holding Ltd., ByteDance Ltd. (TikTok), The Trade Desk Inc., Magnite Inc., Publicis Groupe S.A., WPP plc, Omnicom Group Inc., Interpublic Group of Companies Inc., Dentsu Group Inc., Adobe Inc., Salesforce Inc., ViacomCBS Inc., Roku Inc., Comcast Corporation (Freewheel), Verizon Communications Inc. (Verizon Media/Yahoo), Snap Inc., Twitter Inc. (X Corp.). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The advertising market is meticulously segmented to provide a granular understanding of its diverse components and evolving dynamics. These segmentations allow for a detailed analysis of market performance across various dimensions, including the channels through which advertising is delivered, the formats it takes, the devices consumers use, and the industries it serves. Such detailed breakdowns are crucial for identifying specific growth drivers, emerging opportunities, and competitive landscapes within each niche.

The primary segmentation by medium highlights the ongoing shift from traditional media to digital platforms, with digital encompassing various sub-segments like search, social media, video, and display. Further analysis by format explores the popularity and effectiveness of different creative executions, such as interactive ads or short-form video. Device-based segmentation reflects consumer content consumption patterns, while pricing models and end-use industries offer insights into business models and sector-specific advertising strategies. This multi-faceted approach ensures a comprehensive market overview.

- By Medium:

- Digital (Search, Social Media, Video, Display, Native, Audio)

- Television

- Out-of-Home (OOH)

- Radio

- By Format:

- Text

- Image

- Video

- Audio

- Interactive

- Rich Media

- By Device:

- Desktop

- Mobile (Smartphone, Tablet)

- Connected TV (CTV)

- Digital Out-of-Home (DOOH)

- By Pricing Model:

- Cost Per Mille (CPM)

- Cost Per Click (CPC)

- Cost Per Action (CPA)

- Cost Per Lead (CPL)

- By End-use Industry:

- Retail & Consumer Goods

- Automotive

- BFSI (Banking, Financial Services & Insurance)

- Healthcare & Pharmaceuticals

- Media & Entertainment

- Telecommunications

- Travel & Tourism

- Education

- Others

- By Ad Type:

- Brand Advertising

- Performance Advertising

Regional Highlights

- North America: Continues to be the largest and most mature advertising market, characterized by high digital adoption, advanced ad-tech infrastructure, and significant spending on programmatic, mobile, and video advertising. Strong presence of major tech companies and early adoption of new advertising technologies.

- Europe: A highly regulated market with strong emphasis on data privacy (GDPR), driving innovation in privacy-preserving advertising solutions. Digital advertising, particularly programmatic and social media, is a major growth driver, alongside growing investment in Connected TV (CTV).

- Asia Pacific (APAC): The fastest-growing region, fueled by rapidly increasing internet penetration, mobile-first consumer behavior, and expanding e-commerce markets in countries like China, India, and Southeast Asia. Significant growth in digital video, social commerce, and influencer marketing.

- Latin America: Demonstrating robust growth, especially in digital advertising, driven by rising smartphone penetration and increasing consumption of online video content. Brazil and Mexico are key markets, with a growing interest in programmatic and mobile advertising.

- Middle East and Africa (MEA): An emerging market with significant potential, experiencing rapid digital transformation. Saudi Arabia and UAE lead in digital ad spend, driven by young populations, social media engagement, and increasing e-commerce activities, albeit from a smaller base.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Advertising Market.- Alphabet Inc. (Google)

- Meta Platforms Inc. (Facebook)

- Amazon.com Inc.

- Alibaba Group Holding Ltd.

- ByteDance Ltd. (TikTok)

- The Trade Desk Inc.

- Magnite Inc.

- Publicis Groupe S.A.

- WPP plc

- Omnicom Group Inc.

- Interpublic Group of Companies Inc.

- Dentsu Group Inc.

- Adobe Inc.

- Salesforce Inc.

- ViacomCBS Inc.

- Roku Inc.

- Comcast Corporation (Freewheel)

- Verizon Communications Inc. (Verizon Media/Yahoo)

- Snap Inc.

- Twitter Inc. (X Corp.)

Frequently Asked Questions

What is the projected growth rate of the Advertising Market?

The Advertising Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033, driven largely by digital transformation and evolving consumer media habits.

How will AI impact the future of advertising?

AI is set to revolutionize advertising by enabling hyper-personalization, automating campaign management, improving predictive analytics, generating ad content, and enhancing fraud detection, leading to increased efficiency and ROI.

Which advertising channels are experiencing the fastest growth?

Digital advertising channels, particularly video (including Connected TV), mobile, and social media, are experiencing the fastest growth due to increased online content consumption and advanced targeting capabilities.

What are the main challenges facing the advertising industry?

Key challenges include navigating stringent data privacy regulations, the deprecation of third-party cookies, combating ad fraud, ensuring brand safety in complex digital environments, and addressing the talent gap in ad-tech.

What is the significance of retail media networks in the advertising market?

Retail media networks are significant opportunities as they leverage first-party consumer data and e-commerce platforms to offer highly targeted advertising at the point of purchase, providing strong attribution and high conversion potential for brands.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted