Advanced Distribution Management System Market

Advanced Distribution Management System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701479 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

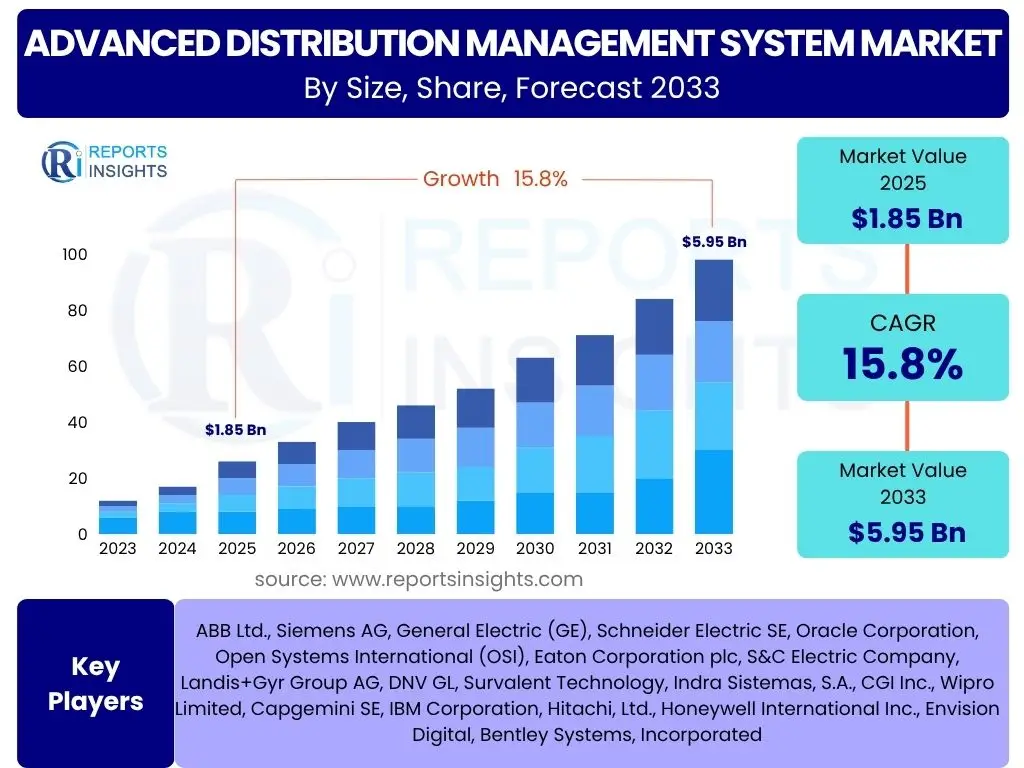

Advanced Distribution Management System Market Size

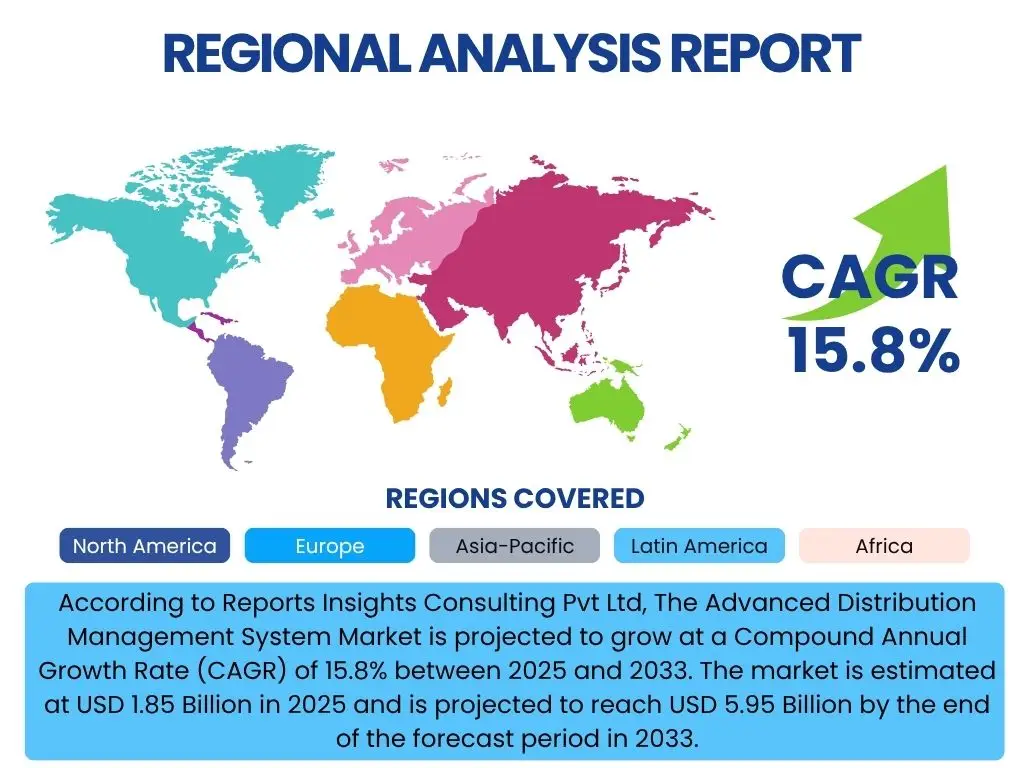

According to Reports Insights Consulting Pvt Ltd, The Advanced Distribution Management System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.8% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 5.95 Billion by the end of the forecast period in 2033.

Key Advanced Distribution Management System Market Trends & Insights

The Advanced Distribution Management System (ADMS) market is currently experiencing a transformative phase, driven by an imperative for enhanced grid resilience, efficiency, and the integration of diverse energy sources. Common user questions often revolve around how ADMS is evolving to meet the demands of a modern energy landscape, including what new functionalities are emerging and how traditional utility operations are being redefined. Key insights suggest a strong movement towards more dynamic, predictive, and integrated grid management solutions that can handle the complexities introduced by renewable energy and distributed generation.

This evolution is not merely about incremental improvements but a fundamental shift towards intelligence at the grid edge. Utilities are actively seeking solutions that offer real-time visibility and control, enabling them to respond proactively to grid anomalies and optimize energy flow. The emphasis is shifting from reactive management to predictive maintenance and automated operations, fundamentally altering how power is delivered and consumed. This paradigm shift underscores the critical role of ADMS in ensuring energy security and optimizing infrastructure investments for future-ready grids.

- Increased integration of Distributed Energy Resources (DERs) and electric vehicle (EV) charging infrastructure.

- Growing adoption of cloud-based ADMS solutions for scalability, flexibility, and reduced operational costs.

- Enhanced focus on cybersecurity measures to protect critical infrastructure from evolving threats.

- Development of predictive analytics and machine learning capabilities for proactive grid management.

- Emphasis on grid modernization initiatives to improve reliability, efficiency, and resiliency against extreme weather events.

AI Impact Analysis on Advanced Distribution Management System

Common inquiries regarding the impact of Artificial Intelligence (AI) on Advanced Distribution Management Systems (ADMS) frequently explore how AI can augment traditional ADMS functionalities, the benefits it offers in terms of operational efficiency and predictive capabilities, and potential concerns related to data quality and algorithmic bias. Users are keen to understand how AI transitions ADMS from a reactive system to a highly proactive and self-optimizing platform, capable of handling the increasing complexity of modern grids. The consensus points towards AI as a pivotal technology for unlocking the full potential of smart grid investments.

AI's influence in ADMS is profound, enabling utilities to move beyond rule-based automation to intelligence-driven decision-making. This includes leveraging machine learning for more accurate load forecasting, predictive maintenance, and real-time anomaly detection. Furthermore, AI contributes significantly to optimizing the dispatch and integration of renewable energy sources, ensuring grid stability despite intermittent generation. While opportunities abound, concerns related to data privacy, the need for robust AI governance, and the development of explainable AI models remain key discussion points for widespread adoption.

- Enables predictive analytics for fault detection and prevention, reducing outage durations significantly.

- Optimizes real-time load balancing and demand-side management, improving grid efficiency.

- Facilitates advanced forecasting of renewable energy generation and consumption patterns.

- Enhances cybersecurity through AI-powered anomaly detection and threat response capabilities.

- Automates complex grid operations, such as network reconfiguration and restoration processes, improving responsiveness.

Key Takeaways Advanced Distribution Management System Market Size & Forecast

Analyses of common user questions regarding the Advanced Distribution Management System (ADMS) market size and forecast reveal a strong interest in understanding the primary growth drivers, the segments poised for the most significant expansion, and the long-term strategic implications for utilities and technology providers. Users seek concise insights into what factors will predominantly shape market trajectory and where the most lucrative opportunities lie over the forecast period. The overarching theme is the recognition of ADMS as an indispensable tool for grid modernization.

The market forecast underscores a robust growth trajectory, propelled by the urgent need for enhanced grid reliability, the increasing penetration of distributed energy resources, and the overarching digitalization initiatives within the energy sector. Key takeaways highlight the pivotal role of software and services components in driving market value, as well as the escalating importance of cloud-based deployment models. Geographically, Asia Pacific and North America are identified as dominant and rapidly expanding regions, driven by significant infrastructure investments and smart grid mandates, respectively.

- The ADMS market is poised for substantial growth, driven by global smart grid investments and grid modernization efforts.

- Increased integration of renewable energy and distributed generation necessitates advanced control capabilities provided by ADMS.

- Cloud-based ADMS solutions are gaining significant traction due to their scalability, cost-effectiveness, and ease of deployment.

- North America and Asia Pacific are expected to remain key growth regions, fueled by regulatory support and infrastructure upgrades.

- Cybersecurity and data privacy remain critical considerations for ADMS deployments, influencing vendor solutions and utility adoption strategies.

Advanced Distribution Management System Market Drivers Analysis

The Advanced Distribution Management System (ADMS) market is propelled by several critical drivers that reflect the evolving demands of modern electricity grids. One of the primary forces is the escalating global focus on grid modernization and the imperative to enhance energy efficiency and reliability. As populations grow and reliance on electricity intensifies, utilities face immense pressure to minimize outages, optimize power flow, and integrate new energy sources seamlessly. ADMS provides the sophisticated tools necessary to address these challenges, offering comprehensive solutions for real-time monitoring, control, and automation of distribution networks.

Another significant driver is the rapid proliferation of Distributed Energy Resources (DERs), including rooftop solar, wind farms, and battery storage systems. The bidirectional flow of power introduced by DERs adds complexity to grid management, requiring advanced systems like ADMS to ensure stability, optimize dispatch, and manage voltage fluctuations effectively. Furthermore, stringent government regulations and initiatives worldwide are mandating smart grid technologies and cybersecurity enhancements, which inherently include ADMS functionalities. These mandates provide a regulatory push for utilities to invest in robust ADMS solutions, thereby accelerating market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Aging grid infrastructure & modernization initiatives | +4.5% | Global (North America, Europe, Asia Pacific) | Short to Mid-term (2025-2030) |

| Rising demand for reliable and efficient power supply | +3.8% | Global (Emerging & Developed Economies) | Long-term (2025-2033) |

| Integration of Distributed Energy Resources (DERs) | +3.2% | Europe, North America, Asia Pacific (Australia, Japan) | Mid to Long-term (2026-2033) |

| Government regulations and mandates for smart grids | +2.5% | Europe, North America, parts of Asia Pacific (China, India) | Short to Mid-term (2025-2031) |

Advanced Distribution Management System Market Restraints Analysis

Despite its significant growth potential, the Advanced Distribution Management System (ADMS) market faces several notable restraints that could temper its expansion. A primary concern is the substantial initial investment required for ADMS implementation. Deploying these sophisticated systems involves not only software procurement but also significant expenditure on hardware upgrades, network infrastructure, and system integration, which can be a prohibitive factor for smaller utilities or those operating with limited capital budgets. The complexity of these projects also contributes to higher upfront costs, extending project timelines and increasing financial risk.

Another significant restraint is the challenge of integrating ADMS with legacy systems that are often prevalent in older utility infrastructures. Many utilities operate with disparate, proprietary systems for various functions, making seamless data exchange and interoperability a complex technical hurdle. This lack of standardization can lead to prolonged deployment cycles, data inconsistencies, and suboptimal system performance, necessitating extensive customization and integration efforts. Furthermore, growing cybersecurity concerns associated with interconnected smart grid systems present a significant challenge, as utilities must invest heavily in robust security measures to protect sensitive grid data and operational control from sophisticated cyber threats, adding to the overall cost and complexity of ADMS deployment.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial investment costs and long ROI periods | -3.0% | Global (Particularly developing economies) | Short to Mid-term (2025-2030) |

| Interoperability challenges with legacy infrastructure | -2.5% | Global (Utilities with aged infrastructure) | Mid-term (2026-2032) |

| Cybersecurity concerns and data privacy risks | -1.8% | Global | Long-term (2025-2033) |

Advanced Distribution Management System Market Opportunities Analysis

The Advanced Distribution Management System (ADMS) market is rich with opportunities stemming from the ongoing transformation of the energy landscape. A significant opportunity lies in the burgeoning development of microgrids and smart cities, which require highly sophisticated and integrated control systems to manage localized generation, consumption, and storage efficiently. ADMS solutions are central to enabling the intelligence and automation necessary for these advanced energy ecosystems, offering new avenues for deployment beyond traditional utility distribution networks. This expansion into new energy paradigms represents a substantial market for innovation and growth.

Another compelling opportunity is the increasing demand for energy storage integration within distribution networks. As renewable energy sources become more prevalent, energy storage systems are crucial for managing intermittency and ensuring grid stability. ADMS can play a vital role in optimizing the charging and discharging of these storage units, maximizing their benefits for grid reliability and efficiency. Furthermore, the emergence of cloud-based ADMS solutions is opening up new markets by offering more flexible, scalable, and cost-effective deployment options, particularly appealing to smaller utilities or those seeking to avoid large upfront capital expenditures. This shift to cloud-native platforms facilitates quicker adoption and continuous updates, enhancing overall system agility.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of microgrids and smart cities | +3.5% | North America, Europe, Asia Pacific | Mid to Long-term (2026-2033) |

| Emergence of cloud-based ADMS solutions | +3.0% | Global | Short to Mid-term (2025-2030) |

| Demand for energy storage integration | +2.7% | Global (Particularly regions with high DER penetration) | Mid-term (2027-2032) |

| Expansion into emerging economies | +2.0% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2028-2033) |

Advanced Distribution Management System Market Challenges Impact Analysis

The Advanced Distribution Management System (ADMS) market faces several critical challenges that can impede its smooth adoption and optimal performance. One significant hurdle is the persistent lack of a skilled workforce capable of deploying, operating, and maintaining these complex systems. The advanced nature of ADMS, incorporating elements of IT, OT (Operational Technology), data science, and power engineering, demands a highly specialized skillset that is currently in short supply within many utilities. This talent gap can lead to delayed implementations, operational inefficiencies, and an over-reliance on external consultants, adding to project costs and timelines.

Another substantial challenge revolves around data privacy and security issues. ADMS platforms collect and process vast amounts of real-time operational data, including sensitive customer consumption patterns and critical infrastructure details. Ensuring the confidentiality, integrity, and availability of this data against increasingly sophisticated cyber threats is paramount. Any breach could have severe consequences, from operational disruptions to public distrust and regulatory penalties. Consequently, utilities must invest significantly in robust cybersecurity frameworks and comply with evolving data protection regulations, which adds complexity and cost to ADMS deployments. Furthermore, organizational resistance to adopting new technologies, often rooted in traditional operational paradigms and fear of change, can slow down the pace of ADMS implementation, requiring extensive change management efforts and cultural shifts within utilities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lack of skilled workforce for deployment and operation | -2.5% | Global | Short to Mid-term (2025-2030) |

| Data privacy and security issues | -2.0% | Global | Long-term (2025-2033) |

| Resistance to adopting new technologies and change management | -1.5% | Global (Especially traditional utilities) | Short to Mid-term (2025-2029) |

Advanced Distribution Management System Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Advanced Distribution Management System (ADMS) market, offering a detailed understanding of its current size, historical performance, and future growth projections. The scope includes a thorough examination of market trends, key drivers, restraints, opportunities, and challenges influencing market dynamics. It meticulously segments the market by component, deployment, end-user, and application, providing granular insights into each category. Furthermore, the report offers a detailed regional analysis, highlighting key market performances across major geographies, alongside profiles of leading market participants to provide a holistic view of the competitive landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 5.95 Billion |

| Growth Rate | 15.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ABB Ltd., Siemens AG, General Electric (GE), Schneider Electric SE, Oracle Corporation, Open Systems International (OSI), Eaton Corporation plc, S&C Electric Company, Landis+Gyr Group AG, DNV GL, Survalent Technology, Indra Sistemas, S.A., CGI Inc., Wipro Limited, Capgemini SE, IBM Corporation, Hitachi, Ltd., Honeywell International Inc., Envision Digital, Bentley Systems, Incorporated |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Advanced Distribution Management System (ADMS) market is meticulously segmented to provide a granular understanding of its diverse components and applications. This segmentation allows for precise market analysis, highlighting growth opportunities and competitive dynamics within specific sub-sectors. The primary segmentation categories include components, deployment models, end-users, and various applications that define the functional scope of ADMS solutions.

Each segment reflects distinct market drivers, adoption patterns, and technological requirements. For instance, the 'Component' segment differentiates between the software modules that form the core of ADMS and the critical services required for its successful implementation and ongoing operation. Similarly, 'Deployment' options signify the evolving preferences of utilities towards traditional on-premises solutions versus modern cloud-based architectures. This comprehensive segmentation is crucial for stakeholders to identify niche markets, tailor strategies, and address specific client needs effectively.

- By Component: This segment includes the core Software modules, which are the intelligent backbone of ADMS, and Services, encompassing crucial aspects like consulting, integration, and ongoing support and maintenance.

- By Deployment: This categorizes ADMS solutions based on their hosting environment, either On-premises installations managed by the utility or flexible, scalable Cloud-based deployments.

- By End User: This segment differentiates between the primary users of ADMS, predominantly Utilities (including both Public and Private entities) and a growing category of Commercial & Industrial sectors.

- By Application: This covers the specific functionalities and operational benefits provided by ADMS, such as Fault Detection, Localization & Isolation (FDIR), Outage Management System (OMS), Network Optimization, Grid Monitoring & Control, Load Management & Forecasting, Volt/VAR Optimization (VVO), and Distributed Energy Resource Management (DERM).

Regional Highlights

- North America: This region is a leading market for ADMS, driven by significant investments in smart grid infrastructure upgrades, aging grid modernization initiatives, and the increasing integration of renewable energy sources. The presence of major technology providers and a strong regulatory push for grid reliability and resilience further bolster market growth.

- Europe: Europe represents a robust market with a strong emphasis on renewable energy integration, energy efficiency mandates, and carbon emission reduction targets. Countries like Germany, the UK, and France are actively deploying ADMS to manage complex distribution networks and support the transition to a low-carbon energy system.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market, propelled by rapid urbanization, industrialization, and substantial investments in new power infrastructure, particularly in emerging economies like China, India, and Southeast Asian countries. The region's increasing energy demand and focus on smart city initiatives are key growth catalysts.

- Latin America: This region is experiencing steady growth in the ADMS market, driven by the need to improve grid reliability, reduce technical losses, and integrate a growing share of renewable energy, especially in countries like Brazil and Mexico.

- Middle East and Africa (MEA): The MEA region is witnessing increasing adoption of ADMS, primarily due to ambitious smart grid projects, diversification of energy sources, and government initiatives aimed at modernizing power infrastructure to support economic growth and address rising energy demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Advanced Distribution Management System Market.- ABB Ltd.

- Siemens AG

- General Electric (GE)

- Schneider Electric SE

- Oracle Corporation

- Open Systems International (OSI)

- Eaton Corporation plc

- S&C Electric Company

- Landis+Gyr Group AG

- DNV GL

- Survalent Technology

- Indra Sistemas, S.A.

- CGI Inc.

- Wipro Limited

- Capgemini SE

- IBM Corporation

- Hitachi, Ltd.

- Honeywell International Inc.

- Envision Digital

- Bentley Systems, Incorporated

Frequently Asked Questions

Analyze common user questions about the Advanced Distribution Management System market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is an Advanced Distribution Management System (ADMS)?

An Advanced Distribution Management System (ADMS) is a software platform used by electric utilities to manage, control, and optimize the operation of their distribution networks. It integrates functionalities from Outage Management Systems (OMS), Distribution Management Systems (DMS), and Supervisory Control and Data Acquisition (SCADA) systems, providing real-time situational awareness, fault detection, restoration capabilities, and advanced applications for grid optimization.

Why is ADMS important for modern grids?

ADMS is crucial for modern grids because it enhances reliability, efficiency, and resilience. It enables utilities to handle the complexities introduced by Distributed Energy Resources (DERs), manage fluctuating demand, minimize outage durations, and improve overall operational performance. Its advanced analytics and automation capabilities are essential for smart grid evolution and energy security.

How does AI enhance ADMS capabilities?

AI enhances ADMS by enabling predictive analytics for fault identification, optimizing real-time energy flow, improving load forecasting accuracy, and facilitating automated decision-making for grid operations. It also strengthens cybersecurity by detecting anomalous patterns and supports the intelligent integration and management of variable renewable energy sources, moving ADMS towards self-healing and self-optimizing grids.

What are the main challenges in ADMS adoption?

Key challenges in ADMS adoption include high initial investment costs, complexity in integrating ADMS with existing legacy utility systems, ensuring robust cybersecurity measures against evolving threats, and the lack of a skilled workforce capable of managing and optimizing these advanced platforms. Organizational resistance to change can also impede smooth implementation.

Which regions are leading in ADMS implementation?

North America and Europe are currently leading in ADMS implementation due to significant investments in grid modernization and smart grid initiatives. However, the Asia Pacific region is rapidly emerging as a high-growth market, driven by rapid urbanization, increasing energy demand, and government efforts to develop resilient and efficient power infrastructure.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted