Advanced Aerospace Material Market

Advanced Aerospace Material Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709350 | Last Updated : December 08, 2025 |

Format : ![]()

![]()

![]()

![]()

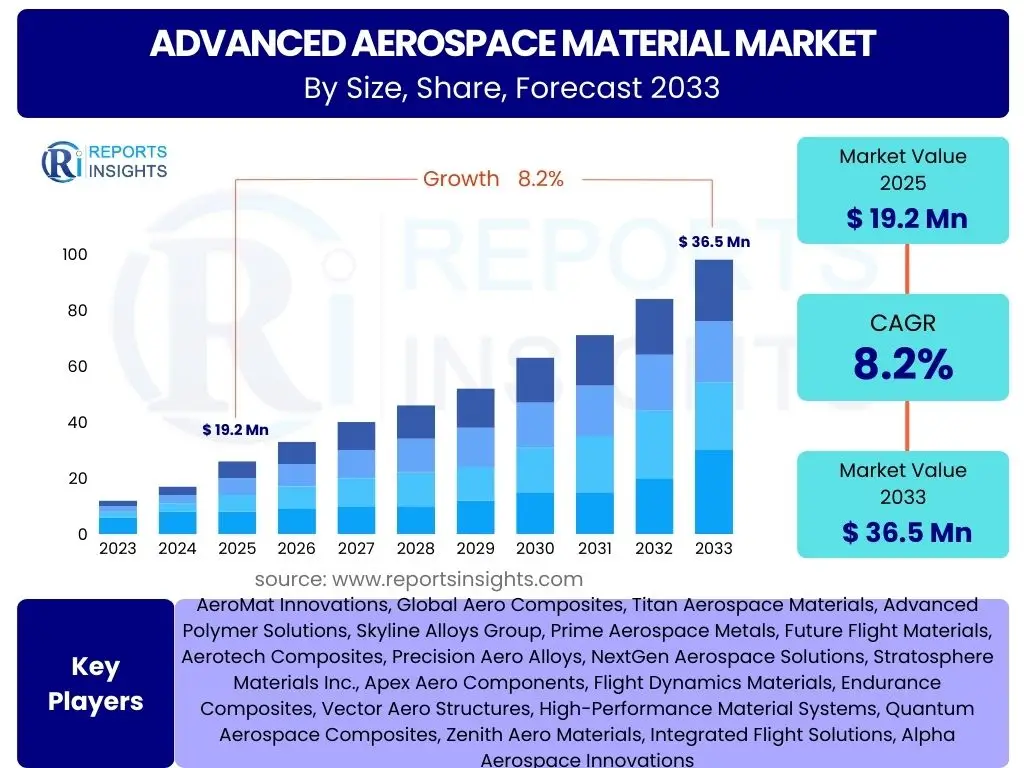

Advanced Aerospace Material Market Size

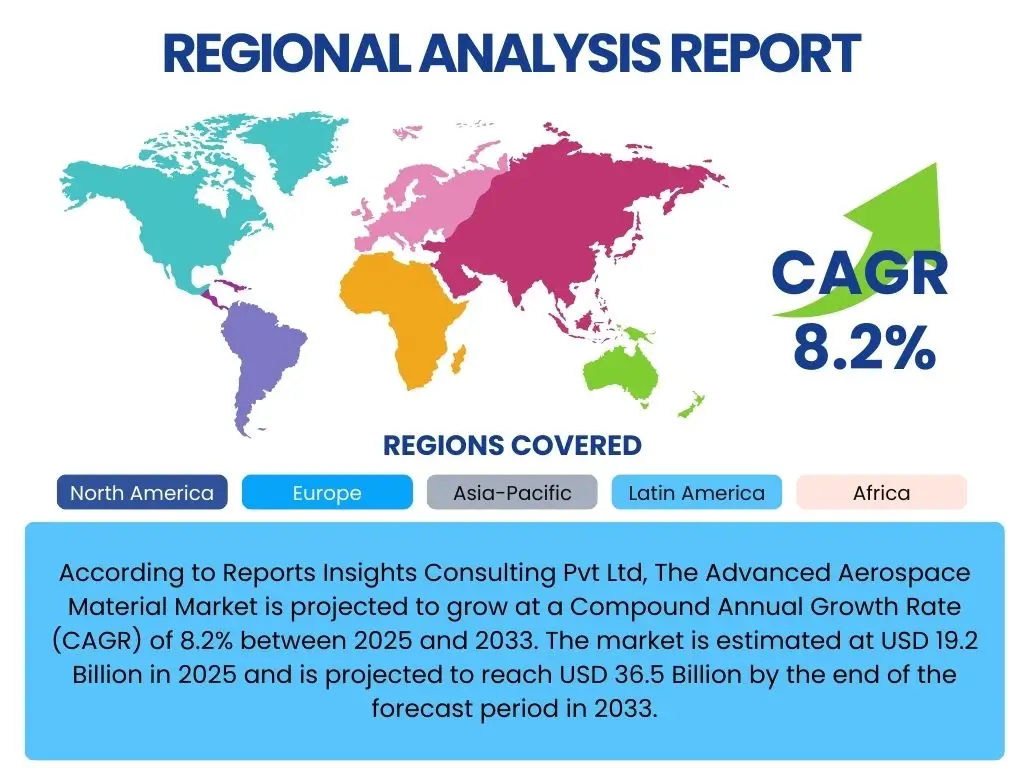

According to Reports Insights Consulting Pvt Ltd, The Advanced Aerospace Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2025 and 2033. The market is estimated at USD 19.2 Billion in 2025 and is projected to reach USD 36.5 Billion by the end of the forecast period in 2033.

Key Advanced Aerospace Material Market Trends & Insights

The Advanced Aerospace Material market is experiencing dynamic shifts driven by an escalating demand for lightweight, high-performance, and sustainable solutions across the global aerospace industry. Key inquiries consistently highlight the emergence of new material classes, the integration of smart functionalities, and the imperative for environmentally conscious manufacturing processes. Stakeholders are particularly interested in how these trends will influence material selection, supply chain resilience, and the overall performance characteristics of next-generation aircraft and spacecraft. The industry is actively pursuing innovations that offer superior strength-to-weight ratios, enhanced thermal resistance, and improved durability to meet increasingly stringent operational and regulatory requirements.

Furthermore, there is a pronounced focus on the scalability of advanced material production, especially for composite materials and advanced alloys, to support large-scale manufacturing objectives for both commercial and defense sectors. The drive towards reducing operational costs and fuel consumption is a persistent theme, with material advancements playing a critical role in achieving these efficiencies. Additionally, the adoption of digital technologies, such as simulation and modeling, is becoming a foundational trend, accelerating the design, testing, and qualification of novel materials. This convergence of material science and digital engineering is setting new benchmarks for innovation and market competitiveness.

- Escalating demand for lightweight, high-performance composites in new aircraft programs.

- Growing adoption of additive manufacturing for complex aerospace components.

- Increasing focus on sustainable and recyclable aerospace materials.

- Integration of smart materials with self-healing and sensing capabilities.

- Advancements in high-temperature superalloys for next-generation propulsion systems.

- Digitalization of material design and qualification processes, including simulation and AI.

AI Impact Analysis on Advanced Aerospace Material

The integration of Artificial Intelligence (AI) in the Advanced Aerospace Material sector is a subject of intense interest and inquiry, with users keen to understand its transformative potential across the entire material lifecycle. Common questions revolve around AI's ability to accelerate material discovery, optimize manufacturing processes, enhance quality control, and predict material performance under extreme conditions. AI algorithms are proving instrumental in sifting through vast datasets of material properties, simulating molecular structures, and identifying novel compositions with desired aerospace characteristics far more rapidly than traditional experimental methods. This capability is paramount in reducing research and development cycles and bringing innovative materials to market faster.

Beyond material discovery, AI's influence extends deeply into optimizing manufacturing workflows. Predictive analytics, machine learning for process control, and robotic automation powered by AI are enhancing precision in fabrication, minimizing waste, and ensuring consistency in material properties—critical for aerospace applications where safety and reliability are paramount. Furthermore, AI-driven inspection systems are revolutionizing quality assurance by identifying microscopic defects with unprecedented accuracy, thereby improving overall product integrity and reducing the likelihood of failures. The ability of AI to model complex material behaviors and predict potential points of failure under various operational stresses is also a significant area of focus, offering proactive insights for maintenance and material longevity, ultimately contributing to safer and more efficient aerospace operations.

- Accelerated discovery and development of novel aerospace materials through AI-driven simulations and data analysis.

- Optimization of advanced manufacturing processes, including additive manufacturing, for reduced defects and improved efficiency.

- Enhanced quality control and non-destructive testing through AI-powered anomaly detection and predictive maintenance.

- Predictive modeling of material performance and degradation under extreme aerospace conditions.

- Streamlined supply chain management for raw materials and finished components using AI logistics.

- AI-assisted design for complex structural components, optimizing material usage and performance.

Key Takeaways Advanced Aerospace Material Market Size & Forecast

Stakeholders frequently seek concise summaries of the Advanced Aerospace Material market's trajectory and the core factors shaping its future. The primary takeaway centers on robust growth, fueled by relentless innovation in material science and engineering, directly addressing the aerospace industry's twin objectives of enhanced performance and reduced environmental impact. The market's expansion is not merely incremental but represents a significant pivot towards highly specialized, application-specific materials designed for extreme operating conditions and longer service lives. Furthermore, the forecast underscores a persistent investment in research and development, particularly in areas like smart materials and advanced composites, reflecting a strategic imperative to maintain technological superiority and competitive advantage.

Another crucial insight is the increasing complexity of the advanced aerospace material landscape, necessitating closer collaboration across the value chain, from raw material suppliers to aircraft manufacturers. The market's growth is also significantly influenced by geopolitical factors, defense spending, and the expansion of global air travel, all of which drive demand for both new aircraft and the modernization of existing fleets. The forecast period anticipates continued emphasis on materials that contribute to fuel efficiency, lighter structures, and reduced emissions, aligning with global sustainability goals. This indicates that material innovation will remain at the forefront of aerospace development, influencing aircraft design, operational economics, and long-term industry trends.

- The Advanced Aerospace Material market is poised for significant expansion, driven by continuous innovation and increasing demand for high-performance, lightweight solutions.

- Growth will be substantially propelled by new aircraft programs, defense modernization efforts, and the burgeoning space exploration sector.

- Advanced composites and high-performance alloys are expected to maintain market dominance, with increasing adoption in critical structural and engine components.

- Sustainability and fuel efficiency mandates will increasingly dictate material selection, favoring eco-friendly and lightweight options.

- Digitalization, including AI and advanced simulation, will play a pivotal role in accelerating material development and optimizing manufacturing processes.

Advanced Aerospace Material Market Drivers Analysis

The Advanced Aerospace Material market is propelled by a confluence of powerful drivers, each contributing significantly to its upward trajectory. The relentless pursuit of fuel efficiency in commercial aviation, driven by environmental regulations and economic pressures, necessitates the adoption of lighter, yet stronger, materials. This demand directly fuels innovation in advanced composites and lightweight alloys. Concurrently, increasing global defense expenditures and the modernization of military aircraft fleets create a consistent demand for materials offering superior ballistic protection, extreme temperature resistance, and stealth capabilities. These factors combine to create a robust environment for material science advancements, pushing the boundaries of what is technologically possible in aerospace engineering.

Moreover, the expansion of commercial air travel, particularly in emerging economies, drives the need for new aircraft production, indirectly boosting the market for advanced materials. As aircraft production rates climb, manufacturers seek reliable, scalable, and cost-effective solutions in material supply. The burgeoning space exploration sector, encompassing both governmental and private ventures, also acts as a critical driver, demanding materials capable of withstanding the harsh conditions of space, including radiation, extreme temperatures, and vacuum environments. These diverse yet interconnected demands highlight a market underpinned by both commercial viability and strategic imperatives, ensuring sustained innovation and growth across various material categories.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Fuel-Efficient Aircraft | +2.1% | Global, particularly North America, Europe, Asia Pacific | Mid-term to Long-term (2025-2033) |

| Rising Defense Budgets and Military Aircraft Modernization | +1.8% | North America, Europe, Middle East, Asia Pacific | Mid-term (2025-2029) |

| Growing Air Passenger Traffic and Aircraft Production | +1.5% | Asia Pacific, North America, Europe | Short-term to Mid-term (2025-2030) |

| Advancements in Space Exploration and Satellite Deployment | +1.2% | North America, Europe, China, India | Long-term (2028-2033) |

| Technological Innovations in Material Science and Manufacturing | +1.6% | Global, particularly developed economies | Ongoing (2025-2033) |

Advanced Aerospace Material Market Restraints Analysis

Despite robust growth prospects, the Advanced Aerospace Material market faces several significant restraints that could temper its expansion. High material and manufacturing costs represent a primary barrier, particularly for exotic alloys and advanced composites, which often require specialized processing techniques and expensive raw inputs. These elevated costs can deter adoption, especially in price-sensitive segments or for smaller-scale projects. Furthermore, the stringent regulatory environment and the extremely long material qualification and certification processes in the aerospace industry pose considerable challenges. New materials must undergo rigorous testing and validation, which can take many years and incur substantial financial investment, slowing down market entry and innovation cycles.

Another major restraint is the complexity of supply chains for advanced aerospace materials. These chains are often global, intricate, and susceptible to disruptions from geopolitical events, trade disputes, or raw material scarcity. The reliance on a limited number of specialized suppliers for certain high-performance materials can create bottlenecks and increase lead times, impacting production schedules for aircraft manufacturers. Moreover, the challenges associated with the reparability and recyclability of some advanced composites, particularly thermoset resins, present environmental and logistical hurdles, driving up end-of-life management costs and complicating the transition towards a more circular economy in aerospace. Addressing these restraints effectively will be crucial for sustained market growth and broader adoption.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Material and Manufacturing Costs | -1.5% | Global | Ongoing (2025-2033) |

| Stringent Regulatory and Certification Processes | -1.3% | North America, Europe (FAA, EASA) | Long-term (2025-2033) |

| Supply Chain Volatility and Geopolitical Tensions | -0.9% | Global, particularly reliant on specific raw material sources | Short-term to Mid-term (2025-2028) |

| Technical Complexity in Processing and Repair | -0.8% | Global | Mid-term (2025-2030) |

| Challenges in Recyclability and Waste Management | -0.6% | Europe (environmental regulations) | Long-term (2028-2033) |

Advanced Aerospace Material Market Opportunities Analysis

The Advanced Aerospace Material market is replete with significant opportunities driven by evolving technological landscapes and emerging market needs. One prominent area is the burgeoning Urban Air Mobility (UAM) sector, including eVTOL (electric Vertical Take-Off and Landing) aircraft, which necessitates ultralight, robust, and cost-effective materials for mass production. This new segment offers a fertile ground for novel material solutions that combine structural integrity with efficient manufacturing processes. Furthermore, the relentless pursuit of sustainability in aviation presents a vast opportunity for the development and adoption of bio-based composites, recyclable polymers, and advanced manufacturing techniques that reduce waste and energy consumption. These sustainable material innovations are becoming increasingly critical for aerospace companies striving to meet ambitious net-zero emission targets and appeal to environmentally conscious consumers and regulators.

Another key opportunity lies in the continued expansion of space exploration, including reusable launch vehicles, satellite constellations, and lunar/Martian missions. These applications demand materials with exceptional performance under extreme conditions, such as high radiation shielding, ultra-high temperature resistance, and cryogenic stability. The advancements in additive manufacturing (3D printing) also open up new avenues for complex component geometries, on-demand part production, and reduced lead times, enabling the use of advanced materials in previously unachievable designs. Moreover, the modernization of existing aircraft fleets, particularly in regions with aging inventories, offers opportunities for material upgrades that enhance performance, extend service life, and improve fuel efficiency. These diverse growth areas underscore a dynamic market landscape with considerable potential for innovative material solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Urban Air Mobility (UAM) and eVTOL Aircraft | +1.9% | North America, Europe, Asia Pacific | Mid-term to Long-term (2027-2033) |

| Development of Sustainable and Bio-based Materials | +1.7% | Europe (strong regulatory push), North America | Long-term (2028-2033) |

| Increasing Adoption of Additive Manufacturing (3D Printing) | +1.5% | Global, particularly developed industrial bases | Mid-term (2025-2030) |

| Expanded Investment in Deep Space Exploration and Satellite Technology | +1.3% | North America, China, Europe | Long-term (2028-2033) |

| Retrofit and Modernization of Existing Aircraft Fleets | +1.0% | Global, especially regions with aging fleets | Short-term to Mid-term (2025-2029) |

Advanced Aerospace Material Market Challenges Impact Analysis

The Advanced Aerospace Material market faces several significant challenges that demand innovative solutions and strategic foresight. One primary challenge is the inherent difficulty in achieving a balance between high performance requirements, cost-effectiveness, and ease of manufacturability. Developing materials that offer exceptional strength-to-weight ratios, temperature resistance, and durability without incurring prohibitive costs or requiring overly complex fabrication processes remains a constant battle. This delicate equilibrium is particularly critical as aerospace programs increasingly seek to reduce overall production costs while simultaneously enhancing aircraft capabilities. Furthermore, the shortage of skilled labor proficient in advanced material science, composite manufacturing, and specialized processing techniques poses a significant constraint, impacting both research and development efforts and large-scale production capacities across the globe.

Another formidable challenge involves the long and capital-intensive qualification and certification cycles for new aerospace materials. The rigorous safety standards and performance benchmarks necessitate extensive testing, analysis, and regulatory approval, which can span several years and cost millions of dollars. This protracted process significantly delays the market entry of innovative materials, slowing down the pace of technological adoption. Moreover, the industry grapples with managing supply chain resilience amidst increasing global volatility, including geopolitical tensions, trade restrictions, and disruptions in the availability of critical raw materials. Ensuring a consistent and secure supply of specialized inputs while navigating complex international trade dynamics is an ongoing challenge for manufacturers of advanced aerospace materials. Addressing these multifaceted challenges will require sustained investment in R&D, workforce development, and robust supply chain strategies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Balancing Performance, Cost, and Manufacturability | -1.2% | Global | Ongoing (2025-2033) |

| Long and Costly Qualification and Certification Processes | -1.0% | North America, Europe | Long-term (2025-2033) |

| Scarcity of Skilled Workforce and Specialized Expertise | -0.7% | Developed economies with advanced aerospace industries | Mid-term (2025-2030) |

| Raw Material Availability and Supply Chain Resilience | -0.8% | Global, especially for rare earth and strategic metals | Short-term to Mid-term (2025-2028) |

| Integration of New Materials into Legacy Aircraft Designs | -0.5% | Global, for MRO and fleet upgrades | Mid-term (2025-2030) |

Advanced Aerospace Material Market - Updated Report Scope

This comprehensive market report delves into the intricate dynamics of the Advanced Aerospace Material sector, providing an exhaustive analysis of market size, growth drivers, restraints, opportunities, and challenges influencing its trajectory from 2025 to 2033. The scope includes detailed segmentation by material type, application, and end-user, offering granular insights into various sub-segments. It also presents a thorough regional analysis, highlighting key market trends and competitive landscapes across major geographical areas. The report aims to equip stakeholders with critical data and strategic intelligence necessary for informed decision-making and navigating the evolving demands of the aerospace industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 19.2 Billion |

| Market Forecast in 2033 | USD 36.5 Billion |

| Growth Rate | 8.2% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | AeroMat Innovations, Global Aero Composites, Titan Aerospace Materials, Advanced Polymer Solutions, Skyline Alloys Group, Prime Aerospace Metals, Future Flight Materials, Aerotech Composites, Precision Aero Alloys, NextGen Aerospace Solutions, Stratosphere Materials Inc., Apex Aero Components, Flight Dynamics Materials, Endurance Composites, Vector Aero Structures, High-Performance Material Systems, Quantum Aerospace Composites, Zenith Aero Materials, Integrated Flight Solutions, Alpha Aerospace Innovations |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Advanced Aerospace Material market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to overall market growth. This segmentation allows for a detailed analysis of specific material preferences, application-specific demands, and end-user requirements, which are crucial for strategic planning. The market is primarily divided by material type, which includes various classes such as composites, alloys, ceramics, and polymers, each with unique properties catering to different aerospace needs. Further divisions by application cover a broad spectrum of aerospace vehicles, from commercial aircraft to advanced spacecraft, while end-user segmentation differentiates between original equipment manufacturers and maintenance, repair, and overhaul service providers.

- By Material Type:

- Composites: Representing the largest segment due to their superior strength-to-weight ratio, extensively used in fuselage, wings, and empennage.

- Carbon Fiber Composites: Dominant within composites, offering high stiffness and strength.

- Glass Fiber Composites: Valued for cost-effectiveness and good insulation properties.

- Aramid Fiber Composites: Known for high impact resistance and energy absorption.

- Alloys: Critical for high-stress and high-temperature applications.

- Aluminum Alloys: Widely used for their lightweight and corrosion resistance.

- Titanium Alloys: Essential for components requiring high strength, low weight, and excellent corrosion resistance at elevated temperatures.

- Superalloys: Indispensable for engine components and hot sections due to exceptional high-temperature strength and creep resistance.

- Ceramics: Used for extreme temperature and abrasive environments, particularly in engine components and thermal protection systems.

- Polymers: Applied in interiors, non-structural components, and specialized seals.

- Others: Including smart materials, nanomaterials, and other emerging material classes.

- Composites: Representing the largest segment due to their superior strength-to-weight ratio, extensively used in fuselage, wings, and empennage.

- By Application:

- Commercial Aircraft: Largest application segment, driven by new aircraft orders and fleet modernization.

- Military Aircraft: Includes fighter jets, transport aircraft, and surveillance planes, demanding robust and specialized materials.

- Spacecraft: Covers satellites, launch vehicles, and deep-space probes, requiring materials for extreme environments.

- Helicopters: Utilizes advanced materials for rotor blades, fuselage, and critical structural components.

- Drones/UAVs (Unmanned Aerial Vehicles): A rapidly growing segment, benefiting from lightweight and durable materials for enhanced range and payload capacity.

- By End-User:

- OEM (Original Equipment Manufacturer): Focuses on the production of new aircraft and components.

- MRO (Maintenance, Repair, and Overhaul): Deals with the upkeep, repair, and upgrade of existing fleets, requiring replacement and specialized repair materials.

Regional Highlights

- North America: This region holds a significant share of the Advanced Aerospace Material market, primarily driven by a robust defense industry, extensive research and development activities, and the presence of major aircraft manufacturers. The United States, in particular, leads in technological innovation and investment in advanced material science, with strong demand from both commercial and military aviation sectors. Emphasis on next-generation aircraft programs and space exploration initiatives further solidifies its market position.

- Europe: Europe represents another key market, characterized by a well-established aerospace industry, stringent environmental regulations, and a strong focus on sustainable aviation. Countries like France, Germany, and the UK are at the forefront of advanced material development, particularly in composites and lightweight alloys for commercial aircraft. Investments in Urban Air Mobility (UAM) and clean aviation technologies are also contributing to market expansion.

- Asia Pacific (APAC): The APAC region is projected to exhibit the highest growth rate, fueled by rapid economic development, increasing air passenger traffic, and significant investments in aerospace manufacturing capabilities, especially in China and India. The expanding middle class in these countries drives demand for commercial aircraft, while growing defense budgets support military modernization efforts. Local governments are also promoting indigenous aerospace material development.

- Latin America: While smaller in market size compared to North America and Europe, Latin America shows steady growth, particularly in the MRO segment and regional aircraft manufacturing. Brazil stands out as a key player with its established aerospace industry, focusing on both commercial and military applications. The demand for advanced materials is gradually increasing as the region modernizes its fleets.

- Middle East and Africa (MEA): The MEA region demonstrates growth driven by significant investments in commercial aviation infrastructure, strategic defense spending, and burgeoning space programs in countries like the UAE and Saudi Arabia. The region's airlines are rapidly expanding and modernizing their fleets, creating demand for advanced materials, particularly those offering fuel efficiency and performance in hot climates.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Advanced Aerospace Material Market.- AeroMat Innovations

- Global Aero Composites

- Titan Aerospace Materials

- Advanced Polymer Solutions

- Skyline Alloys Group

- Prime Aerospace Metals

- Future Flight Materials

- Aerotech Composites

- Precision Aero Alloys

- NextGen Aerospace Solutions

- Stratosphere Materials Inc.

- Apex Aero Components

- Flight Dynamics Materials

- Endurance Composites

- Vector Aero Structures

- High-Performance Material Systems

- Quantum Aerospace Composites

- Zenith Aero Materials

- Integrated Flight Solutions

- Alpha Aerospace Innovations

Frequently Asked Questions

What is the projected growth rate for the Advanced Aerospace Material Market?

The Advanced Aerospace Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2025 and 2033. This robust growth is primarily driven by the escalating demand for lightweight, high-performance materials in both commercial and military aviation, alongside the expanding space exploration sector.

Which material types are driving the Advanced Aerospace Material Market?

Advanced composites, particularly carbon fiber composites, and high-performance alloys such as titanium alloys and superalloys, are the primary drivers. These materials are critical for enhancing fuel efficiency, structural integrity, and performance under extreme operational conditions in modern aircraft and spacecraft designs.

How is AI impacting the development and manufacturing of advanced aerospace materials?

AI is profoundly impacting the sector by accelerating material discovery, optimizing complex manufacturing processes (like additive manufacturing), and enhancing quality control through predictive analytics. AI-driven simulations and data analysis significantly reduce research and development cycles, allowing for faster deployment of innovative materials with improved performance characteristics.

What are the key opportunities in the Advanced Aerospace Material Market?

Key opportunities include the rapid emergence of the Urban Air Mobility (UAM) sector, the increasing demand for sustainable and bio-based materials, the widespread adoption of additive manufacturing, and the continuous expansion of global space exploration initiatives. These areas require novel material solutions that are lighter, stronger, and more cost-effective to produce.

What challenges does the Advanced Aerospace Material Market face?

The market faces challenges such as high material and manufacturing costs, stringent and lengthy qualification and certification processes, and the complexities of ensuring supply chain resilience for specialized raw materials. Additionally, the shortage of a skilled workforce and the inherent technical complexity of processing advanced materials represent significant hurdles to widespread adoption and market expansion.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted