5G Equipment Market

5G Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710069 | Last Updated : December 29, 2025 |

Format : ![]()

![]()

![]()

![]()

5G Equipment Market Size

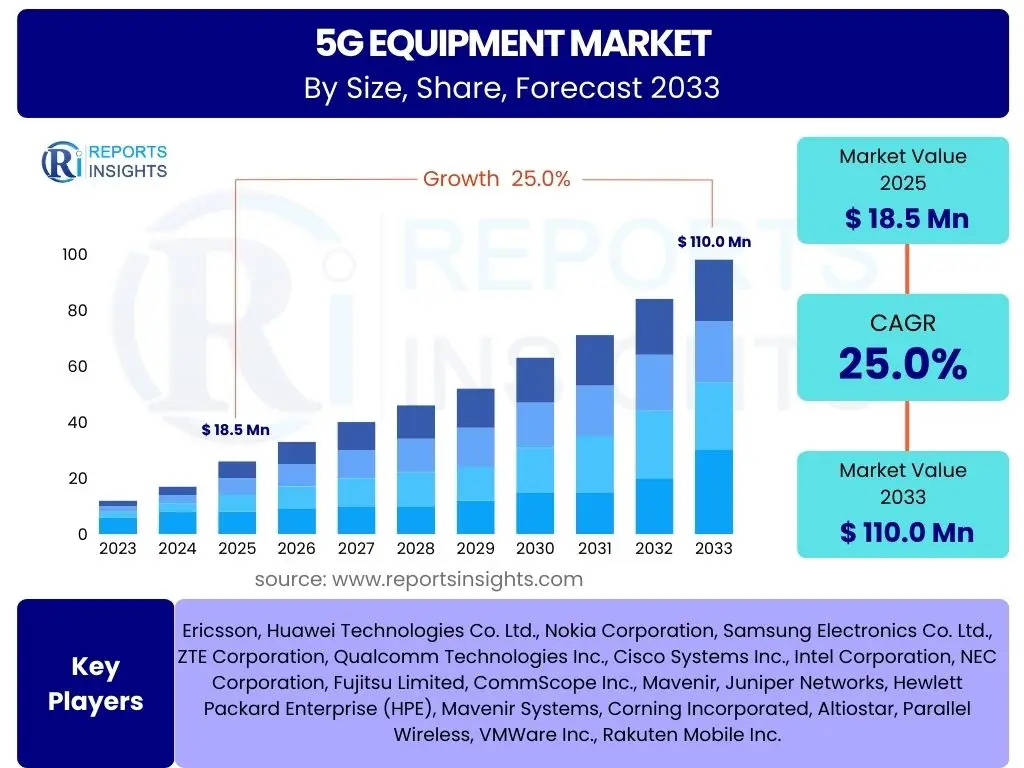

According to Reports Insights Consulting Pvt Ltd, The 5G Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 25.0% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 110.0 Billion by the end of the forecast period in 2033.

The substantial growth of the 5G equipment market is driven by the global imperative for enhanced connectivity, higher data speeds, and ultra-low latency, essential for advanced applications across various sectors. The initial phase of 5G deployment focused on enhanced Mobile Broadband (eMBB), serving consumer needs for faster streaming and mobile internet. However, the market's trajectory is increasingly shaped by the enterprise segment, where 5G's capabilities enable transformative applications like industrial automation, smart cities, and advanced telemedicine. This shift necessitates robust and scalable infrastructure, ranging from radio access networks (RAN) to core network components, fueling significant investment from communication service providers and private enterprises alike.

The market expansion is further propelled by the proliferation of IoT devices and the demand for real-time data processing at the edge. 5G equipment forms the backbone for these interconnected ecosystems, providing the necessary bandwidth and reliability for massive machine-type communications (mMTC) and ultra-reliable low-latency communications (URLLC). Developing economies are rapidly investing in 5G infrastructure to bridge digital divides and foster economic growth, while developed nations continue to expand coverage and densify networks to support next-generation services. This global push for digital transformation ensures a sustained demand for innovative 5G equipment, ranging from base stations and antennas to software-defined networking (SDN) and network function virtualization (NFV) solutions, underpinning the projected robust market growth through 2033.

Key 5G Equipment Market Trends & Insights

The 5G equipment market is undergoing rapid evolution, influenced by technological advancements, changing deployment strategies, and evolving user demands. Users frequently inquire about the leading trends shaping the market's future, particularly concerning network architecture, spectrum utilization, and the integration of new technologies. A significant theme is the move towards more open, disaggregated, and software-defined networks, aiming for greater flexibility, cost-efficiency, and innovation. This shift promises to democratize the vendor landscape and accelerate the deployment of specialized 5G services.

Another prominent trend involves the expansion of 5G into new verticals, driven by the unique capabilities of ultra-reliable low-latency communication (URLLC) and massive machine-type communication (mMTC). This includes the rise of private 5G networks tailored for industrial automation, logistics, and enterprise campus environments, moving beyond traditional public mobile networks. Additionally, sustainability and energy efficiency are emerging as critical considerations, with new equipment designs and operational strategies focusing on reducing the carbon footprint of extensive 5G infrastructure. These trends collectively point towards a more versatile, intelligent, and environmentally conscious 5G ecosystem.

- Open Radio Access Network (Open RAN) architecture adoption

- Increasing deployment of private 5G networks for enterprises

- Expansion of millimeter-wave (mmWave) spectrum for high-capacity areas

- Integration of AI and Machine Learning for network optimization and automation

- Focus on energy-efficient 5G equipment and sustainable network operations

- Growth in network slicing for differentiated service offerings

- Proliferation of Fixed Wireless Access (FWA) solutions in underserved areas

AI Impact Analysis on 5G Equipment

The impact of Artificial Intelligence (AI) on 5G equipment is a frequent subject of user inquiry, highlighting a keen interest in how intelligent systems are enhancing network capabilities and operational efficiency. AI is fundamentally transforming 5G equipment by enabling smarter, more autonomous networks that can self-optimize, predict issues, and adapt to changing conditions in real-time. This includes using AI algorithms for intelligent resource allocation, optimizing signal processing, and managing complex network slicing configurations. The integration of AI moves 5G networks beyond mere connectivity providers to intelligent, self-managing platforms, addressing the intricate demands of next-generation applications and services.

Furthermore, AI plays a crucial role in enhancing the security and reliability of 5G infrastructure. By leveraging machine learning for anomaly detection, AI can identify and mitigate potential security threats faster than traditional methods, protecting critical network assets and user data. Predictive maintenance, powered by AI, allows operators to anticipate equipment failures before they occur, minimizing downtime and reducing operational costs. This leads to more robust and resilient 5G networks. The synergy between AI and 5G equipment is creating a paradigm shift towards highly automated and efficient network operations, capable of supporting the most demanding use cases of Industry 4.0, smart cities, and autonomous systems.

- Enhanced network orchestration and management through AIOps

- Predictive analytics for proactive fault detection and maintenance

- Intelligent resource allocation and spectrum management optimization

- Improved cybersecurity with AI-driven threat detection and response

- Automated network slice provisioning and dynamic adaptation

- Optimized energy consumption of 5G infrastructure

- Real-time traffic management and quality of service (QoS) assurance

Key Takeaways 5G Equipment Market Size & Forecast

Stakeholders frequently seek concise summaries of the most critical insights derived from the 5G Equipment market's current state and future projections. A primary takeaway is the significant and sustained growth trajectory, indicating that 5G is not merely an incremental upgrade but a foundational technology enabling widespread digital transformation across industries. The projected market expansion underscores the ongoing need for substantial investments in network infrastructure, capacity upgrades, and the development of innovative hardware and software solutions to meet the escalating demands of connectivity and advanced applications. This growth is pervasive, impacting both mature and emerging markets globally.

Another crucial insight is the evolving nature of 5G deployments, moving beyond traditional mobile broadband to support specialized enterprise use cases and private networks. This shift opens up new revenue streams and necessitates more flexible, customizable, and software-centric equipment. The forecast highlights the increasing importance of technologies like Open RAN, network slicing, and edge computing, which are instrumental in unlocking the full potential of 5G. Furthermore, the market's future will be heavily influenced by advancements in AI and automation, critical for managing the complexity and ensuring the efficiency of next-generation 5G networks, positioning them as intelligent platforms for innovation.

- Robust and sustained market growth driven by global digital transformation.

- Shift towards enterprise-focused 5G deployments and private networks.

- Increasing adoption of open and disaggregated network architectures (Open RAN).

- Critical role of AI and automation in optimizing 5G network performance and operations.

- Significant investment in both hardware and software components of the 5G ecosystem.

- Expansion of 5G into new spectrum bands, including millimeter-wave (mmWave).

- Emphasis on energy efficiency and sustainable practices in network design and operation.

5G Equipment Market Drivers Analysis

The 5G equipment market is propelled by a confluence of powerful drivers, each contributing significantly to its accelerated growth and widespread adoption. These drivers stem from both consumer demand for enhanced mobile experiences and enterprise requirements for advanced digital capabilities. The overarching need for faster, more reliable, and lower-latency connectivity forms the bedrock of this market expansion, enabling a new era of applications and services previously unattainable with prior generations of wireless technology.

Key drivers include the explosive growth in data traffic, the proliferation of Internet of Things (IoT) devices, and governmental initiatives aimed at fostering digital economies. These factors create an urgent demand for resilient and high-capacity network infrastructure. Furthermore, the ongoing digital transformation across various industries, from manufacturing to healthcare, relies heavily on 5G's unique capabilities, driving enterprises to invest in private 5G networks and specialized equipment. The strategic importance of 5G for national competitiveness and technological leadership also fuels significant public and private sector investment globally.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for High-Speed Data and Bandwidth | +4.5% | Global | Immediate to Long-term |

| Proliferation of IoT and Connected Devices | +3.8% | Global | Mid to Long-term |

| Government Initiatives and Investments in Digital Infrastructure | +3.2% | Asia Pacific, North America, Europe | Ongoing |

| Enterprise Digital Transformation and Industry 4.0 Adoption | +4.0% | Global | Immediate to Mid-term |

| Expansion of Edge Computing Capabilities | +2.7% | Global | Mid-term |

| Increased Demand for Fixed Wireless Access (FWA) | +2.5% | North America, Europe, Latin America | Immediate to Mid-term |

| Development of New 5G-Enabled Applications and Services | +3.0% | Global | Mid to Long-term |

5G Equipment Market Restraints Analysis

Despite its significant growth potential, the 5G equipment market faces several notable restraints that could temper its expansion. These challenges often involve the substantial investment required, regulatory complexities, and the technical hurdles associated with deploying and maintaining advanced wireless infrastructure. Addressing these restraints is crucial for ensuring the smooth and efficient rollout of 5G networks globally, allowing the market to realize its full potential.

High initial deployment costs, particularly for dense urban environments and specialized industrial use cases, represent a significant barrier for communication service providers and enterprises. Coupled with issues such as limited availability of suitable spectrum in certain regions and ongoing cybersecurity concerns, these factors pose considerable challenges. Furthermore, the complexity of integrating new 5G equipment with existing legacy systems, alongside evolving regulatory frameworks and potential public health concerns regarding electromagnetic fields, adds layers of intricacy that can slow down deployment and adoption rates across various markets.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure (CAPEX) for Deployment | -3.5% | Global | Immediate to Mid-term |

| Spectrum Availability and Licensing Costs | -2.8% | Regional (Europe, Asia Pacific) | Ongoing |

| Cybersecurity Concerns and Network Vulnerabilities | -2.0% | Global | Ongoing |

| Interoperability Challenges with Existing Infrastructure | -1.5% | Global | Immediate to Mid-term |

| Regulatory Hurdles and Standardization Delays | -1.8% | Regional (Europe, North America) | Ongoing |

| Public Health Concerns Regarding EMF Exposure | -1.0% | Global | Mid to Long-term |

| Geopolitical Tensions Affecting Supply Chains | -2.2% | Global | Immediate |

5G Equipment Market Opportunities Analysis

The 5G equipment market is rich with significant opportunities that promise to drive innovation, create new revenue streams, and expand the technology's reach into previously untapped sectors. These opportunities often arise from the unique capabilities of 5G technology, which enable specialized services and solutions tailored to specific industry needs, extending far beyond traditional mobile communication.

A prime opportunity lies in the burgeoning market for private 5G networks, where enterprises across various sectors, including manufacturing, logistics, and healthcare, can deploy bespoke networks for enhanced security, control, and performance. This niche allows equipment providers to offer highly customized solutions, moving beyond a one-size-fits-all approach. Furthermore, the advent of network slicing opens up new business models for operators to deliver differentiated services with guaranteed quality of service. The expansion of 5G into rural and underserved areas through Fixed Wireless Access (FWA) also presents a considerable growth avenue, addressing the digital divide and creating new markets for connectivity equipment. These opportunities, coupled with the ongoing development of new 5G-enabled applications and services, position the market for continuous evolution and value creation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Private 5G Networks for Enterprises | +4.0% | Global (Manufacturing, Logistics) | Immediate to Long-term |

| Development of Network Slicing as a Service | +3.5% | Global | Mid to Long-term |

| Industry 4.0 Applications (e.g., Smart Factories, Autonomous Vehicles) | +3.8% | Europe, Asia Pacific, North America | Mid to Long-term |

| Expansion of Fixed Wireless Access (FWA) in Rural Areas | +2.9% | North America, Latin America, MEA | Immediate to Mid-term |

| Emergence of New Revenue Models for Telecom Operators | +2.7% | Global | Mid to Long-term |

| Cloud-Native and Open-Source 5G Implementations | +2.5% | Global | Mid to Long-term |

| Enhanced Focus on Smart City Infrastructure | +2.3% | Global | Long-term |

5G Equipment Market Challenges Impact Analysis

The 5G equipment market, while brimming with potential, is not without its significant challenges that demand innovative solutions and strategic planning. These hurdles can impact the pace of deployment, the cost-effectiveness of operations, and the overall adoption rate of 5G technologies. Overcoming these challenges is critical for realizing the full promise of 5G as a transformative technology.

One primary concern is the substantial energy consumption of 5G infrastructure, particularly with network densification, posing both environmental and operational cost challenges. Supply chain disruptions, exacerbated by geopolitical factors, can lead to delays and increased costs for critical components. Furthermore, the scarcity of skilled professionals capable of designing, deploying, and maintaining complex 5G networks presents a workforce challenge. The fragmented nature of global standardization efforts and the inherent complexity of integrating new 5G systems with diverse legacy networks also create technical and logistical obstacles, requiring significant investment in research, development, and talent acquisition to mitigate their impact on market growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Energy Consumption of 5G Infrastructure | -2.8% | Global | Immediate to Long-term |

| Supply Chain Disruptions and Component Shortages | -2.5% | Global | Immediate to Mid-term |

| Shortage of Skilled Workforce and Expertise | -2.0% | Global | Ongoing |

| Standardization and Interoperability Issues Across Vendors | -1.7% | Global | Mid-term |

| Complex Integration with Legacy Network Systems | -1.5% | Global | Immediate to Mid-term |

| Evolving Regulatory Landscape and Spectrum Harmonization | -1.2% | Regional (Europe, Asia Pacific) | Ongoing |

| Ensuring Quality of Service (QoS) for Diverse Applications | -1.0% | Global | Mid to Long-term |

5G Equipment Market - Updated Report Scope

This market insights report offers a detailed and forward-looking analysis of the 5G Equipment market, providing a comprehensive understanding of its current landscape and projected growth trajectory. The scope encompasses an in-depth examination of market size, trends, drivers, restraints, opportunities, and challenges affecting the industry. It further delves into the impact of Artificial Intelligence on 5G equipment and presents a detailed segmentation analysis, regional highlights, and profiles of key market players to offer a holistic perspective for strategic decision-making and investment planning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 110.0 Billion |

| Growth Rate | 25.0% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Ericsson, Huawei Technologies Co. Ltd., Nokia Corporation, Samsung Electronics Co. Ltd., ZTE Corporation, Qualcomm Technologies Inc., Cisco Systems Inc., Intel Corporation, NEC Corporation, Fujitsu Limited, CommScope Inc., Mavenir, Juniper Networks, Hewlett Packard Enterprise (HPE), Mavenir Systems, Corning Incorporated, Altiostar, Parallel Wireless, VMWare Inc., Rakuten Mobile Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The 5G equipment market is intricately segmented to reflect the diverse technological components, spectrum bands, end-user applications, and industry verticals it serves. This granular segmentation provides a detailed understanding of how different parts of the market contribute to the overall growth and where specific investment and innovation opportunities lie. Analyzing these segments is crucial for identifying targeted market strategies and understanding the evolving demands of various stakeholders, from telecommunication operators to vertical industries adopting private 5G solutions.

The segmentation across components, spectrum, end-user, and application highlights the complex interplay of hardware, software, and services that define the 5G ecosystem. Hardware components form the physical backbone, while software solutions enable the intelligence and flexibility of 5G networks. Spectrum utilization dictates the deployment scenarios and capabilities, with sub-6 GHz offering broad coverage and mmWave providing high capacity. End-user categories differentiate between large-scale public network deployments by service providers and specialized private networks for enterprises. Application segments further distinguish the diverse use cases, ranging from consumer mobile broadband to mission-critical industrial communications, each demanding specific equipment characteristics and functionalities.

- By Component:

- Hardware: Radio Access Network (RAN), Core Network, Backhaul and Transport, Antennas, Base Stations

- Software: Network Orchestration, Network Function Virtualization (NFV), Software-Defined Networking (SDN), Security Software, Analytics and AI Platforms

- Services: Deployment and Integration, Managed Services, Consulting Services, Maintenance and Support

- By Spectrum:

- Sub-6 GHz

- mmWave (Millimeter Wave)

- By End-User:

- Communication Service Providers (CSPs)

- Enterprises

- Government and Public Safety

- By Application:

- Enhanced Mobile Broadband (eMBB)

- Ultra-Reliable Low-Latency Communication (URLLC)

- Massive Machine-Type Communication (mMTC)

- Fixed Wireless Access (FWA)

- Automotive

- Healthcare

- Smart Manufacturing

- Smart Cities

Regional Highlights

Regional analysis reveals significant disparities and unique characteristics in the adoption and growth of the 5G equipment market across different geographical areas. Each region presents a distinct mix of regulatory environments, economic conditions, technological maturity, and strategic priorities, influencing the pace and nature of 5G deployments. Understanding these regional nuances is essential for market players to tailor their strategies, allocate resources effectively, and capitalize on localized opportunities.

For instance, while North America and parts of Asia Pacific lead in early 5G adoption and enterprise investment, Europe is often characterized by complex regulatory frameworks and a strong emphasis on private 5G networks for industrial applications. Emerging markets in Latin America and the Middle East & Africa are rapidly building out their 5G infrastructure, often driven by government initiatives to improve digital connectivity and economic development. These regional differences underscore the need for a granular approach to market entry and expansion, considering local demand, competitive landscapes, and technological readiness to maximize success in the global 5G equipment market.

- North America: Early and aggressive 5G deployments, strong enterprise adoption of private networks, significant investment in mmWave spectrum for dense urban areas, and a focus on advanced applications like autonomous vehicles and industrial IoT.

- Europe: Characterized by diverse regulatory landscapes, a growing emphasis on Open RAN initiatives, increasing adoption of private 5G networks in manufacturing and logistics, and a commitment to energy-efficient network solutions.

- Asia Pacific (APAC): The largest and fastest-growing market, driven by extensive government support, rapid consumer adoption, dense urban deployments, and a strong focus on advanced manufacturing and smart cities applications, particularly in China, South Korea, and Japan.

- Latin America: Emerging market with increasing 5G infrastructure investments, particularly for Fixed Wireless Access (FWA) to bridge the digital divide, and a growing interest in private networks for mining and agricultural sectors.

- Middle East and Africa (MEA): Rapidly expanding 5G coverage, fueled by national digital transformation agendas, significant government-led infrastructure projects, and a focus on smart city development and enhanced public safety communications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the 5G Equipment Market.- Ericsson

- Huawei Technologies Co. Ltd.

- Nokia Corporation

- Samsung Electronics Co. Ltd.

- ZTE Corporation

- Qualcomm Technologies Inc.

- Cisco Systems Inc.

- Intel Corporation

- NEC Corporation

- Fujitsu Limited

- CommScope Inc.

- Mavenir

- Juniper Networks

- Hewlett Packard Enterprise (HPE)

- Corning Incorporated

- Altiostar

- Parallel Wireless

- VMWare Inc.

- Rakuten Mobile Inc.

- Deutsche Telekom AG (as a major operator driving equipment demand and innovation)

Frequently Asked Questions

What is the projected growth rate of the 5G Equipment market?

The 5G Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 25.0% between 2025 and 2033, reaching an estimated USD 110.0 Billion by 2033.

How does AI impact 5G equipment development and operations?

AI significantly impacts 5G equipment by enabling smarter network management, predictive maintenance, enhanced cybersecurity, and optimized resource allocation through AIOps, leading to more efficient and autonomous networks.

What are the primary drivers of 5G equipment market growth?

Key drivers include the surging demand for high-speed data, the proliferation of IoT devices, government investments in digital infrastructure, and the widespread adoption of 5G for enterprise digital transformation and Industry 4.0 applications.

Which regions are leading in 5G equipment deployment and market adoption?

Asia Pacific, particularly countries like China, South Korea, and Japan, along with North America, are leading in 5G equipment deployment due to early adoption, significant investments, and robust enterprise engagement.

What challenges are associated with 5G equipment deployment and market expansion?

Challenges include high capital expenditure, spectrum availability issues, cybersecurity concerns, complex integration with legacy systems, energy consumption of infrastructure, and the shortage of skilled personnel.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted