3D Printing Metal Market

3D Printing Metal Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701312 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

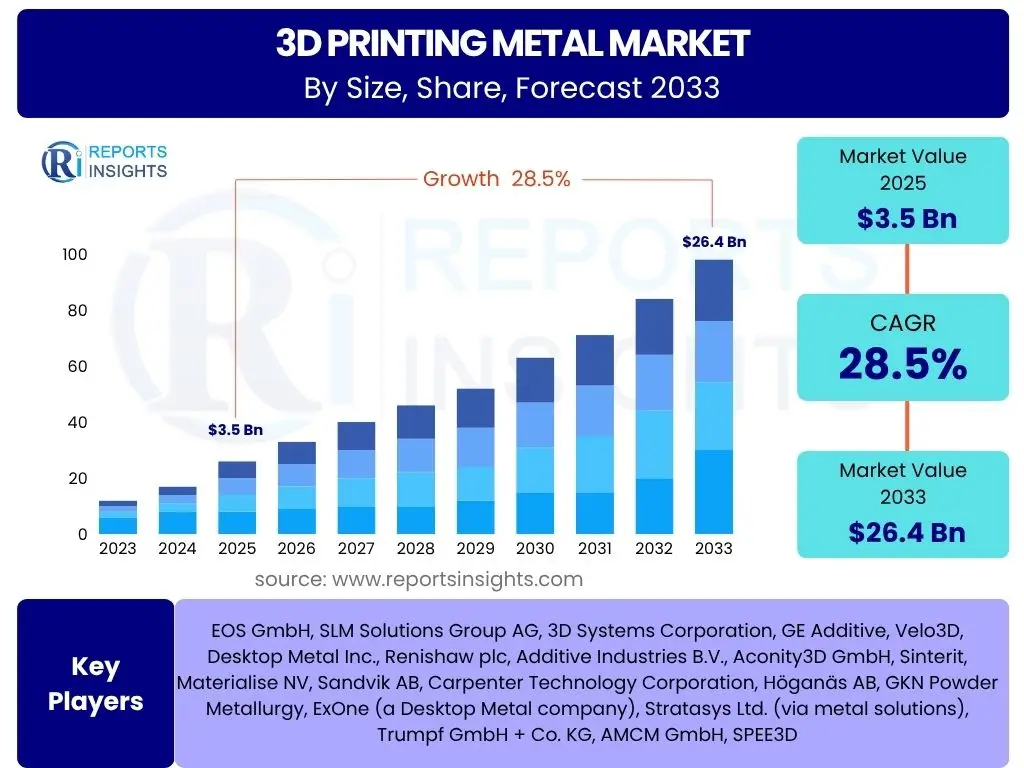

3D Printing Metal Market Size

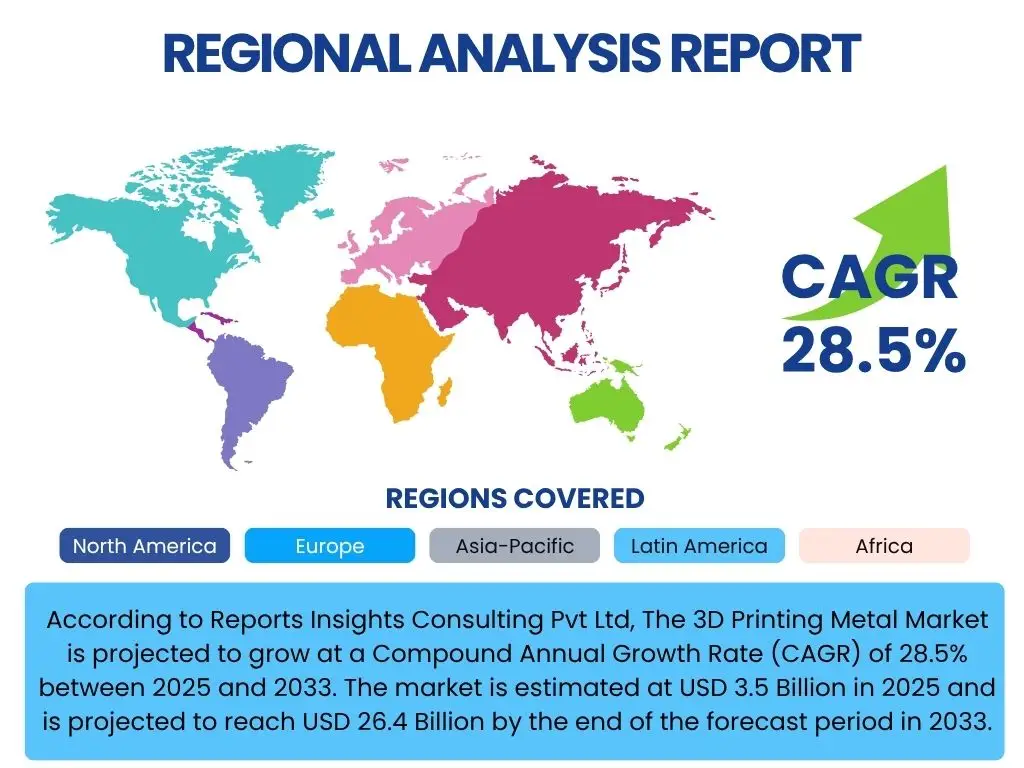

According to Reports Insights Consulting Pvt Ltd, The 3D Printing Metal Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 28.5% between 2025 and 2033. The market is estimated at USD 3.5 Billion in 2025 and is projected to reach USD 26.4 Billion by the end of the forecast period in 2033.

Key 3D Printing Metal Market Trends & Insights

The 3D Printing Metal market is undergoing significant transformation, driven by advancements in material science and machine capabilities. Current trends indicate a strong focus on developing new metal alloys that offer enhanced performance characteristics, such as improved strength-to-weight ratios and better resistance to extreme temperatures and corrosive environments. This material innovation is broadening the applicability of metal additive manufacturing across various high-value industries, from aerospace to healthcare.

Another prominent trend involves the increasing industrialization and automation of metal 3D printing processes. Manufacturers are seeking solutions that enable higher production volumes, greater repeatability, and reduced manual intervention. This includes the integration of in-situ monitoring systems, automated post-processing, and artificial intelligence-driven process optimization, all aimed at achieving production-grade quality and efficiency comparable to traditional manufacturing methods.

Furthermore, the market is witnessing a notable shift towards distributed manufacturing models and localized production. The ability of 3D printing to produce complex parts on demand, without the need for extensive tooling, makes it ideal for supply chain resilience and customization. This trend is particularly relevant in sectors requiring rapid prototyping, low-volume production of intricate components, and the localized repair or replacement of parts, minimizing logistical complexities and lead times.

- Development of high-performance metal alloys with superior mechanical properties.

- Increased adoption of industrial-scale metal 3D printers for higher volume production.

- Integration of automation, in-situ monitoring, and AI for process optimization and quality control.

- Growing demand for customized and complex geometries in various end-use applications.

- Shift towards distributed manufacturing models and localized production capabilities.

- Expansion of metal binder jetting technology for cost-effective mass production.

- Focus on sustainability through reduced material waste and optimized designs.

- Emergence of hybrid manufacturing systems combining additive and subtractive processes.

AI Impact Analysis on 3D Printing Metal

Artificial Intelligence (AI) is set to profoundly transform the 3D Printing Metal market by optimizing various stages of the additive manufacturing workflow, from design to post-processing. Users frequently inquire about how AI can enhance efficiency, reduce costs, and improve part quality. AI algorithms can analyze vast datasets of material properties, print parameters, and structural integrity, enabling predictive modeling that significantly minimizes trial-and-error, a common bottleneck in traditional additive manufacturing.

Specifically, AI is instrumental in generative design, where algorithms autonomously create optimized geometries based on specified performance criteria, often leading to lighter yet stronger parts that are impossible to achieve with conventional design methods. Beyond design, AI-powered systems can monitor the printing process in real-time, detecting anomalies, predicting defects, and dynamically adjusting parameters to ensure consistent part quality. This capability addresses critical concerns about process variability and reliability, which are crucial for industrial adoption.

Looking ahead, the integration of AI will extend to intelligent material selection, predictive maintenance for 3D printers, and automated quality assurance using computer vision and machine learning. This comprehensive application of AI promises to unlock higher levels of efficiency, reduce material waste, accelerate product development cycles, and ultimately drive down the overall cost of metal additive manufacturing, making it more competitive against traditional production techniques. The expectation is that AI will be a key enabler for fully automated and optimized additive manufacturing factories.

- Design Optimization: AI-driven generative design creates complex, lightweight, and high-performance part geometries.

- Process Monitoring & Control: Real-time AI analysis of sensor data detects anomalies, predicts defects, and enables dynamic parameter adjustments during printing.

- Material Selection: Machine learning algorithms identify optimal material compositions for specific application requirements.

- Predictive Maintenance: AI analyzes machine performance data to forecast equipment failures, minimizing downtime and maintenance costs.

- Quality Assurance: AI-powered computer vision systems automate post-print inspection, identifying defects with high accuracy and speed.

- Parameter Optimization: AI reduces trial-and-error by predicting optimal printing parameters for new materials and designs.

- Supply Chain Optimization: AI enhances inventory management and logistics for metal powders and printed parts.

Key Takeaways 3D Printing Metal Market Size & Forecast

The 3D Printing Metal market is poised for exceptional growth, driven by its unique ability to produce complex, high-performance components across critical industries. A key takeaway is the escalating demand from sectors like aerospace, automotive, and healthcare, where the benefits of lightweighting, intricate design, and rapid prototyping are paramount. The market's significant Compound Annual Growth Rate (CAGR) reflects a strong and sustained investment in additive manufacturing technologies and materials, signaling a profound shift in global manufacturing paradigms.

Another crucial insight is the continuous evolution of metal additive manufacturing technologies, including advancements in powder bed fusion, directed energy deposition, and binder jetting. These technological improvements are addressing previous limitations related to build speed, material variety, and part size, making the technology more viable for production-scale applications. The increasing maturity of these processes is expanding the addressable market beyond niche applications into mainstream industrial production.

Furthermore, the forecast indicates a growing emphasis on cost-effectiveness and process scalability, as manufacturers seek to integrate 3D printing into their existing production lines. This involves not only advancements in printer hardware and software but also the development of more affordable metal powders and streamlined post-processing solutions. The market is moving towards a future where metal 3D printing is not just for prototyping or specialized parts, but a competitive alternative for mass production of complex components, fundamentally reshaping supply chains and design possibilities.

- High Growth Trajectory: The market exhibits robust growth, driven by increasing adoption in industrial applications.

- Technological Maturity: Advancements in printing technologies and materials are enabling production-grade quality and scalability.

- Industry Diversification: Adoption is expanding beyond aerospace to automotive, medical, and industrial sectors for mainstream use.

- Cost Reduction Focus: Ongoing efforts to lower material and equipment costs are enhancing market accessibility and competitiveness.

- Supply Chain Resilience: 3D printing offers benefits in localizing production and mitigating supply chain disruptions.

- Sustainability Imperative: The technology supports sustainable manufacturing through reduced waste and optimized material use.

- Digital Transformation: Integration with Industry 4.0 concepts, including AI and IoT, is central to future growth.

3D Printing Metal Market Drivers Analysis

The widespread adoption of 3D printing metal technologies is significantly propelled by the increasing demand for lightweight, high-performance components across various industries. Industries such as aerospace and automotive are continuously seeking innovative methods to reduce weight without compromising structural integrity, directly contributing to improved fuel efficiency and enhanced performance. Metal additive manufacturing offers the unique ability to produce complex geometries and optimized designs that are unachievable with traditional methods, thereby meeting these stringent requirements effectively.

Furthermore, the growing emphasis on product customization and rapid prototyping serves as a substantial market driver. In sectors like healthcare, particularly in dental and orthopedic implants, personalized medical devices tailored to individual patient needs are becoming standard. 3D printing metal allows for on-demand manufacturing of highly customized parts with intricate designs, significantly reducing lead times and facilitating quicker iteration cycles in product development. This agility is crucial for industries with dynamic design requirements and a strong focus on bespoke solutions.

Technological advancements in metal powders and printing processes also play a critical role in driving market expansion. Continuous innovation in materials, including new alloys and improved powder characteristics, alongside enhancements in printer capabilities (e.g., faster build speeds, larger build volumes, multi-material printing), are making the technology more efficient, reliable, and cost-effective. These improvements broaden the range of applications and lower the barrier to entry for potential adopters, encouraging wider industrial integration.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Demand for Lightweight, High-Performance Components | +5.2% | Global (Aerospace: North America, Europe; Automotive: Europe, Asia Pacific) | Short to Medium Term (2025-2029) |

| Increased Adoption in Healthcare & Medical Devices | +4.8% | North America, Europe, Asia Pacific | Medium Term (2026-2030) |

| Advancements in Metal Powder & Printing Technologies | +4.5% | Global (Key R&D hubs: Germany, USA, Japan) | Long Term (2028-2033) |

| Growing Focus on Rapid Prototyping and Customization | +4.1% | Global (Diverse industries) | Short Term (2025-2027) |

| Government Initiatives and Funding for Additive Manufacturing | +3.9% | USA, China, Germany, Japan | Medium to Long Term (2027-2033) |

3D Printing Metal Market Restraints Analysis

Despite its significant growth potential, the 3D Printing Metal market faces notable restraints, primarily the high initial investment costs associated with metal 3D printers and related infrastructure. These machines, along with the necessary post-processing equipment, specialized software, and facility upgrades, represent a substantial capital outlay that can deter small and medium-sized enterprises (SMEs) from adopting the technology. This high entry barrier limits the wider proliferation of metal additive manufacturing, particularly in regions with less robust industrial funding.

Another key restraint is the relatively high cost of metal powders, which are significantly more expensive than traditional manufacturing materials or even plastic filaments used in other 3D printing methods. The complex production processes for these specialized metal powders, coupled with limited economies of scale, contribute to their premium pricing. This material cost impacts the overall economic viability for large-scale production runs, making it challenging for 3D printed metal parts to compete on price with conventionally manufactured components for many applications.

Furthermore, the limited availability of skilled labor and the complexity of the design and printing process present significant challenges. Operating and maintaining sophisticated metal 3D printing systems requires specialized expertise in areas like metallurgy, CAD/CAM, and process optimization. The scarcity of such skilled professionals, combined with the intricate nature of designing for additive manufacturing and ensuring consistent part quality, can slow down adoption rates and increase operational overheads for companies venturing into this technology.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment Costs | -4.5% | Global (More pronounced in developing economies) | Short to Medium Term (2025-2029) |

| High Cost of Metal Powders | -3.8% | Global (Impacts all adopters) | Short to Medium Term (2025-2029) |

| Complexity of Design and Process & Lack of Skilled Labor | -3.2% | Global (All regions) | Short to Medium Term (2025-2029) |

3D Printing Metal Market Opportunities Analysis

Significant opportunities in the 3D Printing Metal market arise from the expanding adoption of the technology in industrial end-use sectors, particularly within the automotive, industrial machinery, and energy industries. While aerospace and healthcare have been early adopters, the ongoing advancements in scalability, material variety, and cost-effectiveness are making metal 3D printing increasingly viable for producing components in these high-volume sectors. This expansion represents a substantial untapped market, offering opportunities for widespread integration into mainstream manufacturing processes beyond specialized or low-volume applications.

The development of new alloys and composite materials specifically engineered for additive manufacturing also presents a crucial opportunity. Research and development efforts are continuously yielding materials with enhanced properties, such as improved strength, ductility, corrosion resistance, and thermal performance, which broaden the scope of applications for metal 3D printing. Furthermore, the ability to combine different materials within a single print, or create gradient materials, opens new avenues for innovative product design and functionality, addressing niche market demands and creating entirely new product categories.

Moreover, the increasing demand for custom tooling, jigs, and fixtures, particularly in the manufacturing industry, offers a lucrative opportunity. Metal 3D printing allows for rapid production of highly customized and complex tooling, reducing lead times and costs associated with traditional manufacturing methods. This capability enables manufacturers to quickly adapt to new production requirements, optimize their assembly lines, and enhance overall operational efficiency, presenting a clear value proposition that drives adoption and market growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expanding Applications in Industrial and Automotive Sectors | +4.9% | Asia Pacific, Europe, North America | Medium to Long Term (2026-2033) |

| Development of New Metal Alloys and Composite Materials | +4.6% | Global (R&D focused regions) | Long Term (2028-2033) |

| Increased Demand for Custom Tooling, Jigs, and Fixtures | +4.3% | Global (Manufacturing hubs) | Short to Medium Term (2025-2030) |

| Growth in Service Bureau Model for Outsourced Production | +3.7% | North America, Europe, Asia Pacific | Short to Medium Term (2025-2029) |

3D Printing Metal Market Challenges Impact Analysis

One significant challenge facing the 3D Printing Metal market is the issue of process repeatability and quality control, particularly for critical industrial applications. Achieving consistent mechanical properties and surface finishes across multiple builds and machines remains a hurdle. Slight variations in powder quality, machine calibration, or environmental conditions can lead to inconsistencies in the final part, making it difficult to meet stringent industry certifications, especially in aerospace and medical sectors where part failure can have severe consequences. Ensuring robust and reliable production processes is crucial for wider industrial adoption.

Another major challenge revolves around post-processing requirements, which can be time-consuming, labor-intensive, and add significantly to the overall cost and complexity of metal 3D printed parts. Components often require extensive support removal, heat treatment, surface finishing, and machining to achieve final specifications. These steps can negate some of the advantages of rapid prototyping or complex geometry creation, increasing turnaround times and reducing the cost-effectiveness, particularly for high-volume production. Automation of post-processing is an ongoing area of development but currently remains a bottleneck.

The limitations in build volume and speed for many metal 3D printing technologies also pose a challenge for manufacturers aiming for large-scale production. While advancements are being made, many current systems are better suited for smaller, complex parts rather than large industrial components. This restriction limits the application of metal additive manufacturing in sectors requiring large-format parts or very high throughput. Overcoming these scaling limitations while maintaining precision and cost-efficiency is essential for the market to fully penetrate industries traditionally reliant on conventional large-scale manufacturing methods.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Process Repeatability and Quality Control Issues | -4.0% | Global (High-precision industries) | Short to Medium Term (2025-2029) |

| Extensive Post-Processing Requirements | -3.5% | Global (All end-users) | Short to Medium Term (2025-2029) |

| Limitations in Build Volume and Speed for Mass Production | -3.0% | Global (Industries requiring large parts/high throughput) | Medium Term (2026-2030) |

3D Printing Metal Market - Updated Report Scope

This report provides a comprehensive analysis of the 3D Printing Metal market, offering in-depth insights into market dynamics, segmentation, regional trends, and competitive landscape. It covers market size estimations, growth forecasts, and a detailed examination of key drivers, restraints, opportunities, and challenges shaping the industry from 2025 to 2033. The scope encompasses various technologies, materials, and end-use industries, presenting a holistic view of the market's current state and future potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 26.4 Billion |

| Growth Rate | 28.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | EOS GmbH, SLM Solutions Group AG, 3D Systems Corporation, GE Additive, Velo3D, Desktop Metal Inc., Renishaw plc, Additive Industries B.V., Aconity3D GmbH, Sinterit, Materialise NV, Sandvik AB, Carpenter Technology Corporation, Höganäs AB, GKN Powder Metallurgy, ExOne (a Desktop Metal company), Stratasys Ltd. (via metal solutions), Trumpf GmbH + Co. KG, AMCM GmbH, SPEE3D |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The 3D Printing Metal market is comprehensively segmented by technology, material, and end-use industry to provide a granular understanding of its diverse landscape. Each segment represents distinct market dynamics, adoption patterns, and growth opportunities. Analyzing these segmentations helps identify key areas of innovation, investment, and market penetration, crucial for stakeholders to strategize effectively within this evolving industry. The technological segmentation highlights the various printing methodologies employed, each offering specific advantages for different applications.

The material segmentation underscores the importance of metallurgy in advancing metal additive manufacturing. The choice of metal powder significantly impacts the final part's properties and is often dictated by the specific requirements of the end-use application, from high-strength aerospace components to biocompatible medical implants. This diversity in material options is crucial for meeting the varied demands of industries adopting 3D printing.

The end-use industry segmentation showcases the primary sectors driving market demand. While aerospace and healthcare have historically led adoption due to their need for complex, lightweight, and customized parts, the technology's increasing maturity and cost-effectiveness are broadening its appeal to high-volume industries like automotive and general industrial manufacturing. This expansion into new industries is a key indicator of the market's growing potential and its transition from niche applications to widespread industrial integration.

- By Technology: Powder Bed Fusion (PBF) (including SLM, EBM, DMLS), Directed Energy Deposition (DED), Binder Jetting (BJ), Material Extrusion (MEX) / Bound Metal Deposition (BMD), Sheet Lamination (SL) / Ultrasonic Additive Manufacturing (UAM), and other emerging technologies.

- By Material: Titanium Alloys, Aluminum Alloys, Nickel Alloys, Stainless Steel, Tool Steel, Cobalt-Chrome Alloys, Precious Metals, Copper Alloys, and other specialized metal compositions.

- By End-Use Industry: Aerospace & Defense, Automotive, Healthcare (Medical & Dental), Industrial (Machinery, Tooling, Robotics), Consumer Products & Electronics, Energy (Oil & Gas, Power Generation), Education & Research, and other diverse applications.

Regional Highlights

- North America: This region holds a significant share of the 3D Printing Metal market, driven by substantial investments in research and development, particularly from the aerospace and defense sectors in the United States. The presence of leading industry players, robust government funding for additive manufacturing initiatives, and a strong ecosystem of material suppliers and service bureaus contribute to its dominance. The region is characterized by early adoption of advanced manufacturing technologies and a high demand for high-performance, complex metal parts. Canada and Mexico are also contributing to regional growth through increasing industrial applications.

- Europe: Europe is a key market, propelled by strong automotive, industrial machinery, and medical device industries, especially in Germany, the UK, and France. These countries are at the forefront of additive manufacturing innovation, with extensive research programs, collaborative industry initiatives, and a focus on industrialization of 3D printing processes. Government support for Industry 4.0 initiatives and a skilled workforce further bolster the market's growth, emphasizing the integration of additive manufacturing into conventional production lines.

- Asia Pacific (APAC): The APAC region is projected to exhibit the highest growth rate, primarily driven by rapid industrialization, increasing manufacturing activities, and growing awareness of additive manufacturing benefits in countries like China, Japan, South Korea, and India. China, in particular, is witnessing massive investments in 3D printing technology for domestic production and export, aiming to become a global manufacturing powerhouse. The expanding automotive and electronics industries, coupled with government support for advanced manufacturing, are key factors contributing to the robust market expansion in this region.

- Latin America: This region is an emerging market for 3D Printing Metal, with increasing adoption in sectors such as automotive, healthcare, and industrial machinery, particularly in Brazil and Mexico. While currently smaller in market share compared to established regions, growing foreign investments, improving economic conditions, and the desire for localized production capabilities are expected to drive gradual but steady growth. The focus here is often on customization and rapid prototyping applications.

- Middle East and Africa (MEA): The MEA region is experiencing nascent but promising growth, primarily influenced by investments in diversification away from oil-dependent economies. Countries like the UAE and Saudi Arabia are investing in smart manufacturing initiatives and building advanced industrial infrastructure, including additive manufacturing hubs. Applications are emerging in energy, aerospace, and defense sectors, driven by strategic government visions to foster technological innovation and local manufacturing capabilities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the 3D Printing Metal Market.- EOS GmbH

- SLM Solutions Group AG

- 3D Systems Corporation

- GE Additive

- Velo3D

- Desktop Metal Inc.

- Renishaw plc

- Additive Industries B.V.

- Aconity3D GmbH

- Sinterit

- Materialise NV

- Sandvik AB

- Carpenter Technology Corporation

- Höganäs AB

- GKN Powder Metallurgy

- ExOne (a Desktop Metal company)

- Stratasys Ltd. (via metal solutions)

- Trumpf GmbH + Co. KG

- AMCM GmbH

- SPEE3D

Frequently Asked Questions

What is 3D printing metal and how does it work?

3D printing metal, also known as metal additive manufacturing, is a process of creating three-dimensional metal objects layer by layer from a digital design. It primarily works by fusing metal powder particles using a heat source like a laser (e.g., in Selective Laser Melting) or an electron beam (e.g., in Electron Beam Melting), or by binding metal powder with a liquid agent and then sintering it (Binder Jetting). This allows for the production of complex geometries and lightweight structures.

Which industries benefit most from 3D printing metal?

Industries that benefit most include Aerospace & Defense, for lightweight and structurally optimized components; Healthcare, for custom medical and dental implants; Automotive, for prototyping, tooling, and specialized parts; and Industrial sectors, for complex machinery, jigs, fixtures, and energy components. These industries leverage metal 3D printing for design freedom, material efficiency, and rapid iteration.

What are the primary advantages of using metal 3D printing over traditional manufacturing?

The primary advantages include the ability to create highly complex and optimized geometries (e.g., lattice structures for weight reduction), rapid prototyping and production of low-volume parts, reduced material waste, consolidation of multiple components into a single part, and customization capabilities. It also allows for on-demand manufacturing, enhancing supply chain flexibility.

What challenges does the 3D printing metal market face?

Key challenges include the high initial investment cost for equipment, the high cost of specialized metal powders, the need for extensive post-processing (e.g., heat treatment, surface finishing), and ensuring consistent process repeatability and quality control for critical applications. There is also a demand for more skilled labor to operate and maintain these advanced systems.

How is artificial intelligence impacting metal 3D printing?

Artificial intelligence significantly impacts metal 3D printing by enabling generative design for optimal part geometries, enhancing real-time process monitoring to predict and correct defects, and optimizing print parameters for improved quality and efficiency. AI also aids in predictive maintenance for machines and automated quality assurance, leading to more reliable and cost-effective production.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted