3D Print Service Bureau Market

3D Print Service Bureau Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710199 | Last Updated : December 30, 2025 |

Format : ![]()

![]()

![]()

![]()

3D Print Service Bureau Market Size

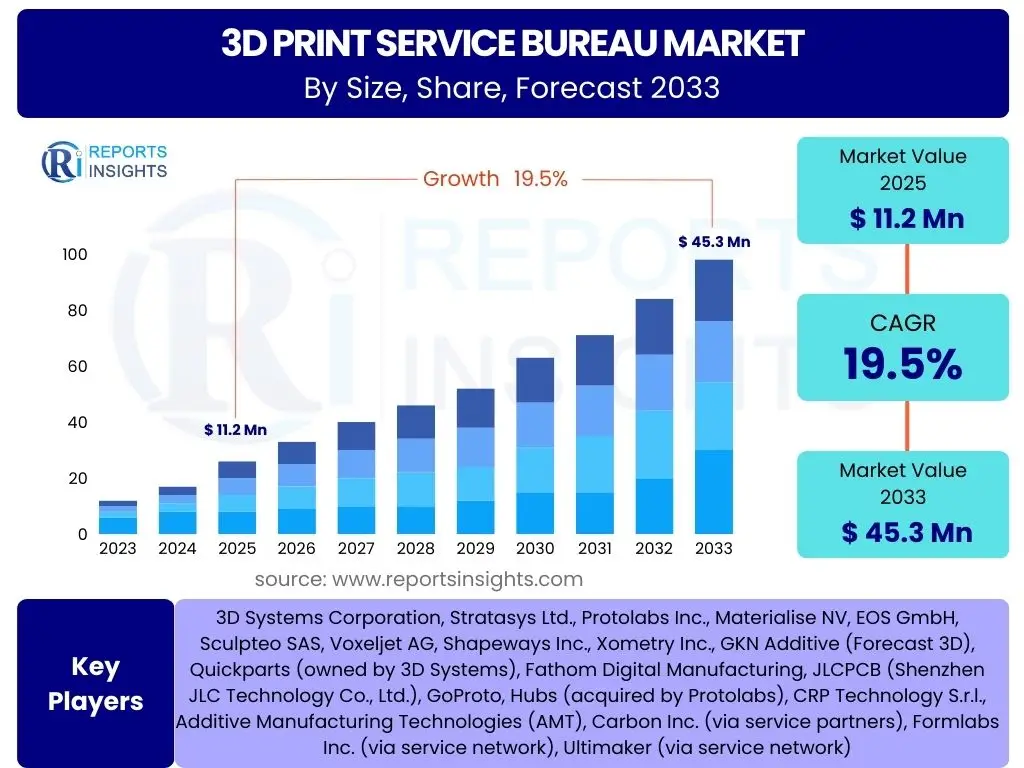

According to Reports Insights Consulting Pvt Ltd, The 3D Print Service Bureau Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 19.5% between 2025 and 2033. The market is estimated at USD 11.2 Billion in 2025 and is projected to reach USD 45.3 Billion by the end of the forecast period in 2033.

Key 3D Print Service Bureau Market Trends & Insights

User inquiries frequently focus on the evolving landscape of additive manufacturing services, seeking to understand the innovations and shifts that are shaping the industry's future. There is significant interest in how technological advancements, material science, and economic factors are influencing the demand for outsourced 3D printing capabilities. Specific questions often revolve around the adoption of advanced printing technologies, the expansion into new application areas, and the increasing focus on sustainable practices within the service bureau model. The market is increasingly characterized by a move towards specialized offerings and value-added services beyond mere part production.

The primary trends indicate a maturation of the 3D print service bureau market, moving beyond rapid prototyping to encompass full-scale production, mass customization, and highly specialized, on-demand manufacturing. Companies are actively exploring how to leverage these bureaus for more complex geometries, faster iteration cycles, and localized production, thereby reducing supply chain vulnerabilities. The growing integration of digital manufacturing workflows, from design to post-processing, is also a prominent theme, suggesting a future where service bureaus act as critical nodes in a more agile and responsive manufacturing ecosystem. Furthermore, the push for eco-friendly materials and processes is becoming a significant differentiator for service providers.

- Shift towards production-grade applications and mass customization.

- Increasing demand for advanced materials, including high-performance polymers and metals.

- Expansion of localized and on-demand manufacturing models.

- Integration of advanced software solutions for design optimization and workflow management.

- Growing adoption of post-processing automation for improved efficiency.

- Focus on sustainability and circular economy principles in material usage.

- Emergence of specialized bureaus catering to specific industries (e.g., medical, aerospace).

- Hybrid manufacturing solutions combining additive and subtractive processes.

AI Impact Analysis on 3D Print Service Bureau

Common user questions regarding AI's impact on 3D print service bureaus often center on how artificial intelligence can optimize processes, enhance design capabilities, and improve overall operational efficiency. There is a strong interest in understanding AI's role in predictive maintenance for 3D printers, material selection, quality control, and the automation of complex workflows. Users are also keen to explore how AI can personalize manufacturing services, leading to greater customer satisfaction and the ability to handle highly customized requests with increased precision and speed. The discussion also includes the potential for AI to manage vast datasets generated by printing operations to uncover insights for process improvement.

The integration of AI is poised to revolutionize several aspects of the 3D print service bureau market, transforming traditional service models into highly intelligent and automated systems. AI algorithms can significantly accelerate the design iteration process through generative design, where optimal geometries are created based on specified constraints and performance requirements. Furthermore, AI-powered predictive analytics can anticipate equipment failures, optimize printing parameters for different materials, and ensure consistent quality across batches, thereby reducing waste and operational costs. This leads to a more efficient, reliable, and cost-effective service offering, enabling bureaus to take on more complex and high-volume projects.

Beyond operational enhancements, AI is expected to play a crucial role in customer engagement and service delivery. Chatbots and intelligent recommendation systems can streamline the quoting and ordering process, providing instant feedback and personalized options to clients. AI also facilitates the management of complex order pipelines, scheduling, and resource allocation, ensuring timely delivery and optimal utilization of printing capacity. This technological evolution will empower service bureaus to offer more competitive pricing, faster turnaround times, and superior product quality, solidifying their position as essential partners in advanced manufacturing.

- Generative design for optimized part geometries and reduced material usage.

- Predictive maintenance for 3D printers, minimizing downtime and increasing throughput.

- AI-driven quality control and defect detection during printing processes.

- Intelligent material selection and parameter optimization for diverse applications.

- Automated workflow management, from order intake to post-processing.

- Enhanced simulation capabilities for predicting part performance and printability.

- Personalized manufacturing and mass customization enabled by AI algorithms.

- Improved supply chain efficiency and inventory management through data insights.

Key Takeaways 3D Print Service Bureau Market Size & Forecast

Users frequently inquire about the overarching implications of the market forecast, specifically seeking concise insights into where the most significant growth opportunities lie and what factors will most profoundly impact the industry's trajectory. There is a desire to understand the strategic imperatives for service bureaus and their clients, encompassing investment areas, technological priorities, and emerging market segments. The focus is often on identifying the critical drivers and inhibitors that will shape market expansion and profitability over the coming decade, alongside the potential for disruptive innovations to reshape competitive landscapes.

The 3D Print Service Bureau Market is set for robust expansion, driven by increasing industrial adoption of additive manufacturing for both prototyping and end-use part production. The market's substantial projected CAGR reflects a fundamental shift in manufacturing paradigms, where flexibility, customization, and on-demand production are gaining precedence. This growth is not merely about more service bureaus entering the market, but also about the existing players expanding their capabilities, investing in advanced technologies, and diversifying their material offerings to cater to a broader spectrum of industry needs. The forecast underscores the critical role service bureaus play in democratizing access to cutting-edge manufacturing technologies for businesses of all sizes.

A significant takeaway is the market's evolving demand profile, moving from singular requests to strategic partnerships where bureaus offer comprehensive design, engineering, and post-processing solutions. This shift necessitates bureaus to invest in skilled talent and integrated digital platforms. Furthermore, the geographic distribution of growth will likely see emerging economies playing a more prominent role, propelled by increased industrialization and government initiatives supporting advanced manufacturing. The forecast also signals the increasing importance of scalability and efficiency in service bureau operations, as competition intensifies and customer expectations for speed and quality rise.

- Robust market expansion, with a nearly four-fold increase in value by 2033, indicating high growth potential.

- Industrial adoption for end-use parts and mass customization is the primary growth engine.

- Significant investment in advanced printing technologies and materials by service providers is anticipated.

- Increasing strategic partnerships between businesses and service bureaus for comprehensive solutions.

- Demand for value-added services, including design optimization, engineering, and post-processing.

- Geographic diversification of market growth, with strong potential in APAC and emerging markets.

- Operational efficiency and scalability are becoming critical competitive advantages.

- The market is shifting towards specialized, industry-specific service offerings.

3D Print Service Bureau Market Drivers Analysis

The accelerated adoption of additive manufacturing across diverse industries is a primary catalyst for the 3D Print Service Bureau Market. As companies seek to reduce time-to-market, minimize tooling costs, and produce complex geometries that are impossible with traditional manufacturing methods, they increasingly rely on specialized service bureaus. These bureaus provide access to expensive, high-performance 3D printing equipment and expertise without requiring significant capital investment from the client. This democratization of advanced manufacturing capabilities fuels demand, allowing businesses of all sizes to leverage the benefits of 3D printing for prototypes, functional parts, and even low-volume production.

Furthermore, the continuous innovation in 3D printing materials, including high-performance polymers, metal alloys, and ceramics, significantly broadens the application scope for service bureaus. These new materials enable the production of parts with enhanced mechanical properties, heat resistance, and biocompatibility, opening doors to highly demanding sectors such as aerospace, medical, and automotive. Concurrently, advancements in printing technologies themselves, such as faster print speeds, larger build volumes, and multi-material printing capabilities, enhance the efficiency and versatility of service bureaus, allowing them to offer more competitive and diverse services. The ability to quickly iterate and produce customized components is a critical advantage, especially for industries driven by rapid innovation and personalization.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Industrial Adoption of Additive Manufacturing | +4.2% | Global, particularly North America, Europe, APAC | Short to Mid-term (2025-2030) |

| Technological Advancements in 3D Printing Materials & Processes | +3.8% | Global | Mid to Long-term (2027-2033) |

| Demand for Mass Customization and On-Demand Production | +3.5% | North America, Europe, China, India | Short to Mid-term (2025-2030) |

| Cost-Effectiveness for Low-Volume Production and Prototyping | +2.9% | Global, particularly SMEs | Short to Mid-term (2025-2028) |

| Supply Chain Resilience and Localization Initiatives | +2.1% | Global, post-pandemic implications | Mid-term (2026-2031) |

3D Print Service Bureau Market Restraints Analysis

One significant restraint on the 3D Print Service Bureau Market is the high initial capital investment required for advanced 3D printing equipment and specialized software. While service bureaus offer an alternative to companies making these investments themselves, the bureaus still bear this substantial cost, which can limit their expansion, technological upgrades, and competitive pricing strategies. The ongoing maintenance, material costs, and need for highly skilled labor further add to operational overheads, potentially hindering market accessibility for smaller service providers and impacting overall market growth rates.

Furthermore, concerns regarding intellectual property (IP) security and data confidentiality present a considerable barrier to widespread adoption, particularly for sensitive industrial applications. Clients may be hesitant to share proprietary designs and critical manufacturing data with third-party service bureaus due to fears of unauthorized replication or misuse. This concern necessitates robust data security protocols and trusted relationships, which can slow down adoption rates for new clients. Additionally, the lack of standardized certification and quality control processes across the diverse range of additive manufacturing technologies can lead to inconsistencies in part quality, eroding client confidence and hindering market maturation.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment & Operational Costs | -3.1% | Global | Short to Mid-term (2025-2030) |

| Intellectual Property Concerns & Data Security Risks | -2.8% | Global, particularly industries with sensitive designs | Short to Mid-term (2025-2030) |

| Lack of Standardized Quality Control and Certification | -2.5% | Global | Mid-term (2026-2031) |

| Limited Material Availability for Certain Niche Applications | -1.9% | Specific industries like aerospace, medical | Short to Mid-term (2025-2028) |

| Competition from In-house Additive Manufacturing Capabilities | -1.5% | Large enterprises, high-volume production sectors | Long-term (2028-2033) |

3D Print Service Bureau Market Opportunities Analysis

The expanding array of materials compatible with 3D printing technologies presents a significant growth opportunity for service bureaus. As new polymers, metals, ceramics, and composites become available, each offering unique properties, bureaus can diversify their service offerings to cater to an even broader range of specialized industrial applications. This includes high-performance materials for demanding sectors like aerospace, automotive, and medical, as well as sustainable and biodegradable options for environmentally conscious industries. Adapting to and integrating these new materials allows service bureaus to capture niche markets and offer more comprehensive solutions to their clients, distinguishing themselves in a competitive landscape.

Furthermore, the growing trend towards distributed manufacturing and localized production offers substantial opportunities. With geopolitical shifts and supply chain vulnerabilities highlighted in recent years, companies are increasingly looking to reduce reliance on distant manufacturing hubs and establish more resilient, regional production capabilities. 3D print service bureaus are perfectly positioned to act as agile, on-demand local manufacturing partners, providing quick turnaround times and customized solutions without the need for extensive capital investment in local infrastructure by client companies. This model not only enhances supply chain robustness but also reduces transportation costs and environmental impact, appealing to a wider range of clients.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New Verticals with Advanced Materials | +3.9% | Global, particularly medical, aerospace, energy | Mid to Long-term (2027-2033) |

| Growth of Distributed Manufacturing & Localization | +3.5% | North America, Europe, Asia Pacific | Mid-term (2026-2031) |

| Increasing Demand for End-Use Parts & Functional Prototypes | +3.1% | Global | Short to Mid-term (2025-2030) |

| Integration of AI and Automation for Workflow Optimization | +2.7% | Global | Mid to Long-term (2027-2033) |

| Strategic Partnerships with Design Firms & OEMs | +2.2% | Global | Short to Mid-term (2025-2028) |

3D Print Service Bureau Market Challenges Impact Analysis

One of the primary challenges confronting the 3D Print Service Bureau Market is managing the complexity and cost associated with post-processing and finishing operations. While 3D printing technology enables intricate geometries, the resulting parts often require significant manual or automated post-processing steps such as support removal, surface finishing, curing, and heat treatment to achieve the desired functional and aesthetic qualities. These steps can be time-consuming, labor-intensive, and costly, often representing a significant portion of the total production cost and lead time. Effectively streamlining these processes without compromising quality remains a critical hurdle for service bureaus aiming for scalability and competitive pricing.

Another significant challenge revolves around the inherent limitations of 3D printing technologies concerning speed, scalability, and part size for large-volume production. While additive manufacturing excels in customization and complex geometries, traditional manufacturing methods often retain an advantage in producing large quantities of identical parts at a lower cost per unit. Service bureaus must navigate this competitive landscape by focusing on their strengths, such as rapid prototyping, highly customized components, and small-batch production. However, overcoming the perception of 3D printing as only suitable for low-volume or niche applications and demonstrating its viability for broader industrial use cases remains a considerable challenge in expanding the market's reach.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Post-Processing & Finishing Requirements | -3.4% | Global | Short to Mid-term (2025-2030) |

| Scalability Limitations for Mass Production | -3.0% | Global | Mid to Long-term (2027-2033) |

| Shortage of Skilled Workforce and Technical Expertise | -2.6% | North America, Europe, China | Short to Mid-term (2025-2030) |

| Achieving Consistent Quality Across Diverse Technologies | -2.3% | Global | Short to Mid-term (2025-2028) |

| High Cost of Certain Advanced Materials | -1.8% | Global | Short to Mid-term (2025-2028) |

3D Print Service Bureau Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global 3D Print Service Bureau Market, covering market size estimations, growth forecasts, key trends, and a detailed examination of market drivers, restraints, opportunities, and challenges. It includes an AI impact analysis, regional breakdowns, and a competitive landscape assessment, offering strategic insights for stakeholders to navigate the evolving market dynamics and identify lucrative growth avenues. The report's scope extends across various segments including technology, material, application, and end-use industry, providing a holistic view of the market's structure and potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 11.2 Billion |

| Market Forecast in 2033 | USD 45.3 Billion |

| Growth Rate | 19.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | 3D Systems Corporation, Stratasys Ltd., Protolabs Inc., Materialise NV, EOS GmbH, Sculpteo SAS, Voxeljet AG, Shapeways Inc., Xometry Inc., GKN Additive (Forecast 3D), Quickparts (owned by 3D Systems), Fathom Digital Manufacturing, JLCPCB (Shenzhen JLC Technology Co., Ltd.), GoProto, Hubs (acquired by Protolabs), CRP Technology S.r.l., Additive Manufacturing Technologies (AMT), Carbon Inc. (via service partners), Formlabs Inc. (via service network), Ultimaker (via service network) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The 3D Print Service Bureau Market is extensively segmented to reflect the diverse range of technologies, materials, applications, and end-use industries that leverage additive manufacturing. This granular segmentation allows for a detailed understanding of market dynamics within specific niches, identifying areas of high growth and emerging opportunities. The varying requirements across different segments, from the precision needed in medical applications to the strength required in aerospace components, drive distinct demands for specific printing technologies and materials, shaping the competitive landscape of service bureaus.

- By Technology: This segment includes key additive manufacturing processes such as Stereolithography (SLA), Fused Deposition Modeling (FDM), Selective Laser Sintering (SLS), Multi Jet Fusion (MJF), Direct Metal Laser Sintering (DMLS)/Selective Laser Melting (SLM), Binder Jetting, PolyJet/Material Jetting, and Digital Light Processing (DLP). Each technology offers unique advantages in terms of material compatibility, part accuracy, surface finish, and cost-effectiveness, catering to different application requirements. For instance, SLA and DLP are favored for high-resolution prototypes and intricate designs, while FDM is popular for robust functional prototypes and certain end-use parts. Metal additive manufacturing technologies like DMLS/SLM are crucial for aerospace and medical applications requiring high strength and complex geometries.

- By Material: The market is broadly segmented into Polymers, Metals, and Ceramics, with further sub-segmentation based on specific material types. Polymers include various plastics (e.g., ABS, PLA, Nylon, PETG, Polycarbonate), resins (standard, engineering, dental, castable), elastomers (TPU), and composites. Metals encompass aluminum alloys, titanium alloys, stainless steel, nickel alloys, cobalt-chrome alloys, and precious metals. Ceramics include materials like alumina and zirconia. The continuous development of new, high-performance, and application-specific materials is a key driver, enabling service bureaus to address a broader range of industrial needs, from lightweight components to biocompatible implants.

- By Application: Applications range from Prototyping & Concept Modeling to Tooling & Manufacturing Aids, Functional Parts & End-Use Production, and Mass Customization. Prototyping remains a foundational application, allowing rapid design iteration. However, the market is seeing a significant shift towards the production of functional parts and end-use components, which leverages the strengths of additive manufacturing for complex, optimized designs. Tooling and manufacturing aids, such as jigs, fixtures, and molds, also represent a strong segment due to the cost and time savings compared to traditional fabrication methods. Mass customization further expands market opportunities, particularly in consumer goods and healthcare.

- By End-Use Industry: Key industries utilizing 3D print service bureaus include Automotive, Aerospace & Defense, Healthcare & Medical, Consumer Goods & Electronics, and Industrial & Manufacturing. The Automotive sector employs 3D printing for rapid prototyping of components, lightweight parts, and customized interior elements. Aerospace & Defense relies on it for intricate, high-performance parts with demanding material properties. Healthcare benefits from custom prosthetics, dental implants, surgical guides, and anatomical models. The Industrial & Manufacturing sector utilizes bureaus for jigs, fixtures, and on-demand spare parts, enhancing operational flexibility and reducing downtime.

Regional Highlights

- North America: This region is a leading market for 3D print service bureaus, driven by robust industrial adoption, significant R&D investments in additive manufacturing technologies, and the presence of numerous key market players. The United States, in particular, showcases high demand from the aerospace, automotive, and healthcare sectors, which are early and consistent adopters of advanced manufacturing solutions. The region's strong innovation ecosystem, coupled with a focus on reshoring manufacturing and supply chain resilience, further propels the growth of service bureaus, especially for specialized and high-value applications.

- Europe: Europe represents another significant market, characterized by strong governmental support for industrial digitalization, advanced manufacturing initiatives, and a mature industrial base. Countries such as Germany, the UK, and France are at the forefront of adopting 3D printing for industrial applications, particularly in the automotive, medical, and machinery industries. The region's emphasis on sustainability and circular economy principles also drives demand for service bureaus capable of utilizing advanced, environmentally friendly materials and processes, fostering a strong market for both prototyping and end-use part production.

- Asia Pacific (APAC): The APAC region is projected to exhibit the highest growth rate, fueled by rapid industrialization, expanding manufacturing sectors, and increasing investments in advanced technologies, especially in China, India, Japan, and South Korea. Emerging economies in the region are leveraging 3D print service bureaus to enhance their manufacturing capabilities, reduce production costs, and accelerate product development cycles. The burgeoning electronics, automotive, and consumer goods industries are key contributors to the demand for outsourced 3D printing services, making APAC a dynamic and critically important market.

- Latin America: While a smaller market compared to North America and Europe, Latin America is experiencing steady growth in the 3D Print Service Bureau Market. This growth is primarily driven by increasing industrialization, a rising awareness of additive manufacturing benefits, and investments in infrastructure across countries like Brazil and Mexico. The automotive and consumer goods sectors are key areas of adoption, with businesses seeking cost-effective prototyping and small-batch production solutions to enhance local manufacturing capabilities and competitiveness.

- Middle East & Africa (MEA): The MEA region is an emerging market for 3D print service bureaus, with growth stimulated by diversification efforts away from oil-dependent economies and strategic investments in smart manufacturing and technological innovation, particularly in the UAE and Saudi Arabia. The healthcare, construction, and oil & gas sectors are beginning to explore the advantages of additive manufacturing for specialized components, rapid prototyping, and on-demand spare parts, signaling future growth potential, albeit from a lower base.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the 3D Print Service Bureau Market.- 3D Systems Corporation

- Stratasys Ltd.

- Protolabs Inc.

- Materialise NV

- EOS GmbH

- Sculpteo SAS

- Voxeljet AG

- Shapeways Inc.

- Xometry Inc.

- GKN Additive

- Quickparts

- Fathom Digital Manufacturing

- JLCPCB (Shenzhen JLC Technology Co., Ltd.)

- GoProto

- Hubs

- CRP Technology S.r.l.

- Additive Manufacturing Technologies (AMT)

- Carbon Inc. (via service partners)

- Formlabs Inc. (via service network)

- Ultimaker (via service network)

Frequently Asked Questions

What is a 3D Print Service Bureau?

A 3D Print Service Bureau is a company that offers additive manufacturing services to clients, providing access to various 3D printing technologies, materials, and expertise for producing prototypes, functional parts, and customized components on demand, without the client needing to invest in their own equipment.

What are the primary benefits of using a 3D Print Service Bureau?

The main benefits include access to advanced technologies and diverse materials, reduced capital expenditure for clients, faster turnaround times for prototypes and low-volume production, expert design and engineering support, and the ability to scale production flexibly without significant in-house investment.

Which industries benefit most from 3D Print Service Bureaus?

Industries such as Automotive, Aerospace & Defense, Healthcare & Medical, Consumer Goods & Electronics, and Industrial Manufacturing benefit significantly due to their need for rapid prototyping, complex part geometries, custom tooling, and on-demand production of specialized components.

What types of materials can 3D Print Service Bureaus work with?

Service bureaus typically work with a wide range of materials, including various polymers (e.g., plastics, resins, elastomers), metals (e.g., aluminum, titanium, stainless steel), and ceramics, often including high-performance and specialty composites tailored for specific applications.

How is AI impacting the 3D Print Service Bureau Market?

AI is transforming the market by enabling generative design for optimized parts, enhancing predictive maintenance for printers, improving quality control, automating complex workflows, and facilitating personalized manufacturing, leading to increased efficiency, reduced costs, and faster innovation.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted