3D NAND Memory Market

3D NAND Memory Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708567 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

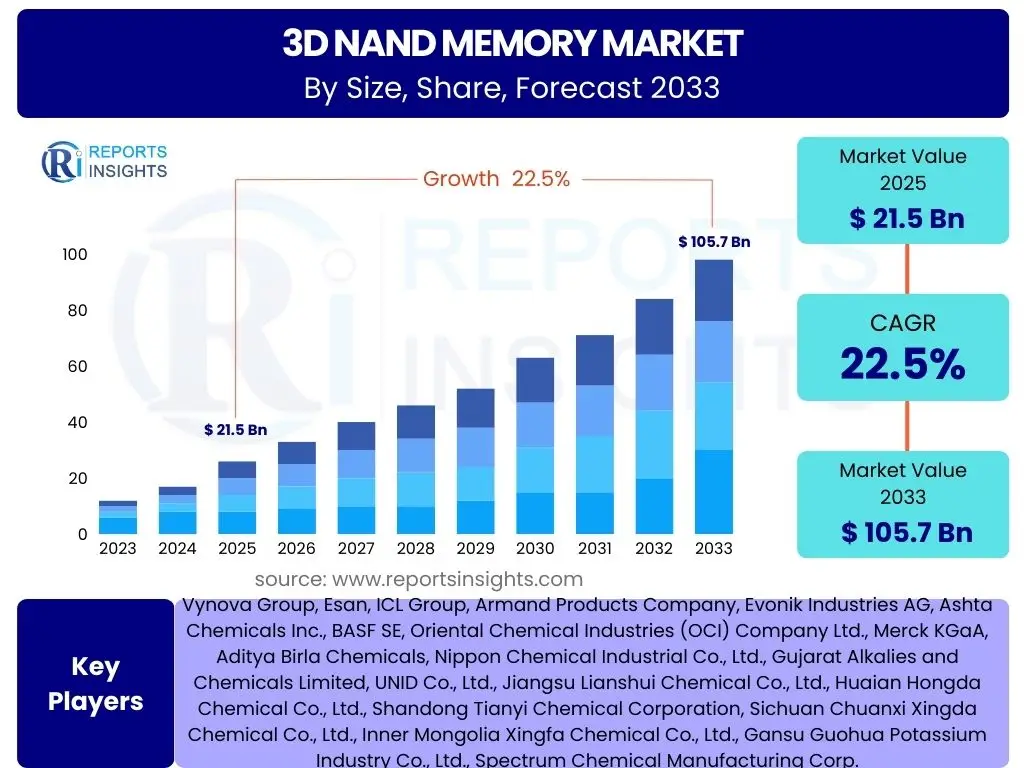

3D NAND Memory Market Size

According to Reports Insights Consulting Pvt Ltd, The 3D NAND Memory Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 22.5% between 2025 and 2033. The market is estimated at USD 21.5 Billion in 2025 and is projected to reach USD 105.7 Billion by the end of the forecast period in 2033.

Key 3D NAND Memory Market Trends & Insights

The 3D NAND memory market is currently experiencing dynamic evolution driven by a confluence of technological advancements and burgeoning data consumption. Key user inquiries often revolve around the continuous pursuit of higher bit density, which translates into increased storage capacity within smaller footprints, and the resulting impact on cost per gigabyte. This intense focus on density is a primary factor fueling the adoption of multi-level cell technologies such as Quad-Level Cell (QLC) and Penta-Level Cell (PLC), which allow more bits to be stored per memory cell, fundamentally altering the economics of data storage solutions.

Another significant area of interest concerns the expansion of 3D NAND into diverse application domains beyond traditional consumer electronics. Users frequently seek to understand how this technology is being leveraged in demanding environments such as enterprise data centers, automotive systems, and advanced industrial IoT applications. The inherent performance characteristics, including improved read/write speeds and enhanced endurance over earlier generations, make 3D NAND increasingly indispensable for high-performance computing and real-time data processing requirements. The transition towards higher layer counts, exceeding hundreds of layers, is a prominent trend that consistently garners attention, as it directly addresses the escalating global demand for efficient and scalable storage.

- Continuous increase in 3D NAND layer count and stack density.

- Rising adoption of QLC (Quad-Level Cell) and emerging PLC (Penta-Level Cell) technologies.

- Growing demand for high-capacity SSDs in data centers and enterprise storage.

- Expansion of 3D NAND into automotive and industrial applications for robust data storage.

- Integration of 3D NAND in edge computing devices to support localized data processing.

- Focus on reducing cost per bit through technological advancements and manufacturing efficiencies.

AI Impact Analysis on 3D NAND Memory

The burgeoning field of Artificial Intelligence (AI) is profoundly influencing the landscape of 3D NAND memory, with user questions frequently centering on the symbiotic relationship between these two technologies. AI workloads, particularly in training large language models, computer vision, and advanced analytics, necessitate massive datasets that require high-density, high-speed storage solutions. 3D NAND's ability to offer increased capacity per unit area at competitive costs makes it an ideal choice for supporting the data-intensive nature of AI, driving demand for more advanced and efficient memory architectures within data centers and AI accelerators.

Moreover, the performance demands of AI applications are pushing the boundaries of what 3D NAND can offer. Users are keen to understand how 3D NAND facilitates faster data access, which is crucial for reducing latency in AI inference and training processes. The parallel processing capabilities of AI systems benefit significantly from storage that can deliver data quickly and reliably. This has led to innovations in controller technology and interface standards specifically designed to optimize data flow between 3D NAND storage arrays and AI processing units, ensuring that memory does not become a bottleneck in the performance of AI systems. The demand for robust and scalable storage solutions for AI data lakes and model repositories is a primary driver for 3D NAND market expansion.

- Significant increase in data storage demand driven by AI model training and inference.

- Requirement for high-performance storage solutions to accelerate AI workloads.

- Development of specialized enterprise SSDs leveraging 3D NAND for AI data centers.

- Enhanced data throughput and reduced latency for AI applications due to advanced 3D NAND architectures.

- Growth in edge AI applications requiring compact, high-capacity 3D NAND storage.

Key Takeaways 3D NAND Memory Market Size & Forecast

The 3D NAND memory market is poised for robust expansion, reflecting a fundamental shift in data storage paradigms that consistently emerges as a central theme in user inquiries. The significant projected CAGR underscores the technology's critical role in meeting the escalating global demand for efficient, high-density, and cost-effective data storage solutions. This growth is not merely incremental but represents a foundational evolution, driven by the pervasive digitalization across industries and the exponential growth of data generated from diverse sources, from consumer devices to enterprise-scale applications. Understanding the scale of this projected market expansion is vital for strategic planning across the entire semiconductor ecosystem.

Furthermore, the forecast highlights the indispensable nature of 3D NAND in supporting next-generation technologies and infrastructure. Users often seek clarity on the long-term viability and growth trajectory of this technology in the face of evolving market dynamics. The consistent upward trend in market valuation signals sustained innovation in memory architecture, manufacturing processes, and application integration. These key takeaways collectively paint a picture of a resilient and expanding market, where 3D NAND is not just a component but a foundational element enabling advancements in cloud computing, artificial intelligence, automotive electronics, and a myriad of other data-centric fields, making it a critical area for investment and development.

- The 3D NAND market is projected for substantial growth, indicating a high demand for advanced storage solutions.

- Technological advancements, particularly in layer stacking and bit density, are key growth catalysts.

- Enterprise and data center segments will remain primary drivers for high-capacity 3D NAND deployments.

- The increasing adoption of AI and ML technologies is a significant factor in accelerating market expansion.

- Continued efforts to reduce the cost per bit will sustain market competitiveness and widespread adoption.

3D NAND Memory Market Drivers Analysis

The 3D NAND memory market is experiencing significant impetus from several critical factors that collectively fuel its expansion and adoption across diverse industries. A primary driver is the relentless growth in data generation, driven by the proliferation of smart devices, cloud computing services, and the increasing reliance on digital information across all sectors. As data volumes surge, there is an inherent demand for storage solutions that can offer higher capacities, improved performance, and greater efficiency, which 3D NAND technology is uniquely positioned to provide, distinguishing itself from planar NAND limitations. This pervasive need for enhanced storage underpins the foundational growth of the market.

Another powerful catalyst is the widespread adoption of Solid-State Drives (SSDs) in both consumer and enterprise segments. SSDs, largely powered by 3D NAND, offer superior speed, durability, and energy efficiency compared to traditional Hard Disk Drives (HDDs). The continuous decline in the cost per gigabyte for 3D NAND has made SSDs more accessible and attractive, leading to their integration into an ever-broader range of devices, from personal computers to high-performance servers. Furthermore, the burgeoning demand for specialized storage in emerging applications such as Artificial Intelligence (AI), autonomous vehicles, and the Internet of Things (IoT) explicitly requires the high-density and robust performance characteristics of 3D NAND, positioning it as an indispensable technology for future innovation.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for High-Density Storage | +5.8% | Global, particularly APAC (Smartphones, Data Centers) | Short-term to Long-term (2025-2033) |

| Proliferation of Solid-State Drives (SSDs) | +4.2% | North America, Europe, APAC (Enterprise, Consumer) | Mid-term to Long-term (2026-2033) |

| Growth in Cloud Computing and Data Centers | +3.5% | North America, Europe, Asia (Hyperscale operators) | Short-term to Long-term (2025-2033) |

| Rising Adoption of AI, ML, and IoT Technologies | +4.0% | Global, particularly developed economies | Mid-term to Long-term (2027-2033) |

| Advancements in Automotive Electronics (Autonomous Driving) | +2.0% | Europe, North America, East Asia (Germany, USA, Japan) | Long-term (2028-2033) |

3D NAND Memory Market Restraints Analysis

Despite its robust growth, the 3D NAND memory market faces several significant restraints that could potentially temper its expansion trajectory. One primary concern revolves around the complex and capital-intensive manufacturing processes required for producing high-layer-count 3D NAND chips. The intricate lithography, etching, and deposition techniques involved demand substantial research and development investments and sophisticated fabrication facilities. These high entry barriers and ongoing operational costs can impact profitability and slow down the pace of innovation, especially for smaller market players, thereby concentrating market power among a few large manufacturers capable of sustaining such investments.

Another notable restraint is the inherent volatility of NAND flash memory prices, which are subject to supply-demand dynamics and macroeconomic fluctuations. Overcapacity or sudden shifts in consumer demand can lead to price drops, affecting manufacturers' revenues and profit margins. Furthermore, the physical limitations and reliability challenges associated with scaling to even higher layer counts and adopting more aggressive multi-level cell technologies (e.g., QLC, PLC) present technical hurdles. As more bits are squeezed into a single cell, issues such as cell-to-cell interference, reduced endurance, and data retention degradation become more pronounced, necessitating advanced error correction and management techniques, which can increase complexity and cost, potentially limiting widespread adoption in highly sensitive applications.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Complexity and Capital Expenditure | -1.5% | Global (Impacts all manufacturers) | Short-term to Long-term (2025-2033) |

| Volatility in NAND Flash Pricing and Market Oversupply | -1.8% | Global (Market-wide impact) | Short-term to Mid-term (2025-2028) |

| Scaling Challenges (Endurance, Reliability with higher layers/QLC) | -1.2% | Global (Technical limitation) | Mid-term to Long-term (2027-2033) |

| Intense Competition and Intellectual Property Disputes | -0.8% | Global (Major manufacturing regions) | Short-term to Long-term (2025-2033) |

3D NAND Memory Market Opportunities Analysis

The 3D NAND memory market is replete with significant opportunities that promise to drive its continued expansion and technological innovation. One of the most compelling avenues for growth lies in the relentless pursuit of higher layer counts and more advanced multi-level cell (MLC) technologies. The development of 500-layer and even 1000-layer 3D NAND stacks, coupled with the mainstream adoption of Penta-Level Cell (PLC) technology, presents an unparalleled opportunity to dramatically increase bit density and further reduce the cost per gigabyte. This technological frontier promises to unlock new application possibilities that were previously constrained by cost or capacity, offering unprecedented storage capabilities for future generations of data-intensive systems.

Furthermore, the expansion into new and underserved application areas represents another substantial opportunity. While consumer electronics and enterprise SSDs remain strongholds, emerging sectors such as advanced industrial automation, medical imaging, and next-generation networking equipment are increasingly demanding robust, high-capacity, and low-latency storage solutions. The automotive industry, in particular, with the rise of autonomous vehicles and sophisticated in-car infotainment systems, offers a burgeoning market for specialized 3D NAND. Strategic collaborations between memory manufacturers and end-user industries can also foster tailored solutions, opening up niche markets and ensuring that 3D NAND technology is optimized for specific, high-value applications, thereby diversifying revenue streams and strengthening market resilience against volatility in traditional segments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Ultra-High Layer Count (e.g., >300L, >500L) NAND | +3.0% | Global (Technological Leaders: East Asia, North America) | Mid-term to Long-term (2027-2033) |

| Emergence of Penta-Level Cell (PLC) Technology | +2.5% | Global (Research & Development hubs) | Long-term (2029-2033) |

| Expansion into New Verticals (e.g., Quantum Computing support, Advanced Medical) | +2.0% | Developed Economies (North America, Europe, Japan) | Mid-term to Long-term (2028-2033) |

| Strategic Partnerships and Ecosystem Development | +1.5% | Global (Cross-industry collaboration) | Short-term to Long-term (2025-2033) |

| Untapped Markets in Developing Regions | +1.0% | Southeast Asia, Latin America, Africa | Mid-term to Long-term (2027-2033) |

3D NAND Memory Market Challenges Impact Analysis

The 3D NAND memory market, while experiencing significant growth, is not immune to substantial challenges that could impact its future trajectory and profitability. One major hurdle is the increasing complexity of manufacturing processes as layer counts continue to rise. Scaling beyond 200 or 300 layers introduces unprecedented engineering difficulties in etching, deposition, and alignment, leading to potential yield degradation and higher production costs. Maintaining product quality, reliability, and performance consistency across these increasingly intricate architectures becomes a critical challenge, demanding advanced metrology and process control techniques that add to manufacturing overheads and extend development cycles.

Furthermore, sustaining performance and endurance while simultaneously increasing bit density (e.g., moving from TLC to QLC and PLC) presents a fundamental technical conundrum. As more bits are stored per cell, the voltage differences between states become smaller, making cells more susceptible to noise, wear, and data corruption. This necessitates more sophisticated error correction codes (ECC) and wear-leveling algorithms, which can consume more controller resources and potentially reduce overall performance or endurance for demanding applications. Geopolitical tensions and supply chain vulnerabilities, particularly concerning critical raw materials and specialized manufacturing equipment, also pose a persistent challenge, threatening production stability and market predictability across major manufacturing regions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Performance and Reliability at Higher Bit Densities (QLC/PLC) | -1.0% | Global (Technological barrier) | Short-term to Long-term (2025-2033) |

| Yield Management and Cost Optimization for Ultra-High Layer Stacks | -1.3% | Major Manufacturing Hubs (East Asia) | Short-term to Mid-term (2025-2029) |

| Geopolitical Tensions and Supply Chain Disruptions | -1.7% | Global (Trade-dependent regions) | Short-term to Mid-term (2025-2028) |

| Environmental Sustainability in Manufacturing and E-waste Management | -0.5% | Developed Economies (Regulatory pressure) | Mid-term to Long-term (2027-2033) |

| Shortage of Skilled Talent in Advanced Semiconductor Manufacturing | -0.8% | North America, Europe, East Asia | Short-term to Long-term (2025-2033) |

3D NAND Memory Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global 3D NAND Memory Market, offering a detailed understanding of market dynamics, growth drivers, restraints, opportunities, and challenges. The scope encompasses a thorough examination of market sizing, historical performance, and future projections, segmented by type, wafer size, application, and end-user. It also includes an extensive regional analysis, competitive landscape assessment, and the impact of emerging technologies like AI. The report aims to deliver actionable insights for stakeholders seeking to navigate and capitalize on the evolving memory industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 21.5 Billion |

| Market Forecast in 2033 | USD 105.7 Billion |

| Growth Rate | 22.5% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Leading Memory Solutions Provider A, Global Storage Corporation B, Advanced Semiconductor Company C, Flash Technology Innovator D, Integrated Device Manufacturer E, High-Performance Memory Solutions F, Data Storage Systems G, Digital Storage Leader H, Memory Products Pioneer I, Semiconductor Foundry J, Component Supplier K, Storage Technology Provider L, Embedded Solutions M, Cloud Storage Innovator N, Next-Gen Memory Developer O |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The 3D NAND memory market is extensively segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for precise analysis of market dynamics across different technological tiers, application areas, and end-user industries, reflecting the varied requirements and adoption patterns within the global digital ecosystem. Each segment plays a crucial role in the overall market landscape, driven by specific demands for capacity, performance, and cost efficiency. The detailed breakdown provides insights into where growth is most concentrated and identifies emerging areas of opportunity for manufacturers and solution providers.

- By Type: This segment categorizes 3D NAND based on the number of bits stored per cell, influencing cost, capacity, and endurance.

- TLC (Triple-Level Cell)

- QLC (Quad-Level Cell)

- PLC (Penta-Level Cell)

- By Wafer Size: Segmentation by layer count reflects the technological advancement and density achieved in the manufacturing process.

- 128-layer

- 176-layer

- 232-layer

- >232-layer

- By Application: This segment examines the primary uses of 3D NAND memory across various devices and systems.

- Smartphones

- SSDs (Client SSD, Enterprise SSD)

- Enterprise Storage

- Automotive

- Industrial

- IoT Devices

- Others (Gaming, AI Accelerators)

- By End-User: Categorization by the industry or sector that utilizes 3D NAND products.

- Consumer Electronics

- Enterprise

- Automotive

- Healthcare

- Industrial

- Telecommunications

Regional Highlights

- North America: This region is a significant market for 3D NAND memory, largely driven by the presence of major cloud service providers, large data centers, and advanced technology research. High adoption rates of enterprise SSDs and burgeoning investments in AI and machine learning infrastructure contribute substantially to market demand. The region also benefits from a strong ecosystem of semiconductor manufacturers and research institutions pushing innovation in memory technologies.

- Europe: Characterized by a robust automotive industry and a growing focus on industrial IoT and automation, Europe presents a strong market for specialized 3D NAND solutions. Stringent data privacy regulations also drive demand for secure and reliable local storage within data centers. Technological advancements in autonomous driving and smart factories necessitate high-performance and resilient memory components.

- Asia Pacific (APAC): APAC is the largest and fastest-growing market for 3D NAND, primarily due to its dominant position in consumer electronics manufacturing and the rapid expansion of digital infrastructure. Countries like China, South Korea, Japan, and Taiwan are not only major producers of 3D NAND but also immense consumers, driven by smartphone adoption, vast data center construction, and a rapidly expanding e-commerce landscape. The region's increasing investment in AI and 5G technologies further propels demand for advanced storage solutions.

- Latin America & Middle East and Africa (MEA): These emerging markets are experiencing accelerated digitalization, leading to increasing demand for mobile devices, cloud services, and localized data storage. While smaller in market share compared to mature regions, they offer significant growth potential as internet penetration increases and digital transformation initiatives gain momentum. Investments in telecommunications infrastructure and localized data centers are key drivers for 3D NAND adoption in these regions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the 3D NAND Memory Market.- Leading Memory Solutions Provider A

- Global Storage Corporation B

- Advanced Semiconductor Company C

- Flash Technology Innovator D

- Integrated Device Manufacturer E

- High-Performance Memory Solutions F

- Data Storage Systems G

- Digital Storage Leader H

- Memory Products Pioneer I

- Semiconductor Foundry J

- Component Supplier K

- Storage Technology Provider L

- Embedded Solutions M

- Cloud Storage Innovator N

- Next-Gen Memory Developer O

Frequently Asked Questions

Analyze common user questions about the 3D NAND Memory market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is 3D NAND memory?

3D NAND memory is a type of non-volatile flash memory that stacks memory cells vertically in multiple layers, enabling significantly higher storage capacity and improved performance compared to traditional 2D (planar) NAND, which arranges cells horizontally on a single plane.

How does 3D NAND differ from 2D NAND?

The primary difference lies in their architecture: 2D NAND cells are arranged side-by-side on a flat surface, facing limitations in scaling beyond a certain point. 3D NAND overcomes this by stacking cells vertically, akin to a skyscraper, allowing for greater density, lower power consumption, and better endurance, making it more cost-effective per bit at higher capacities.

What are the primary applications of 3D NAND?

3D NAND is predominantly used in Solid-State Drives (SSDs) for consumer, enterprise, and data center applications, offering faster boot times and data access. It is also crucial for smartphones, tablets, automotive electronics, industrial storage, and supporting high-performance computing needs for AI and cloud infrastructure.

What are the benefits of 3D NAND over traditional memory technologies?

3D NAND offers several advantages, including much higher storage density and capacity, leading to a lower cost per gigabyte. It also provides improved performance (faster read/write speeds), better power efficiency, and enhanced endurance, making it ideal for demanding applications that require reliable and scalable data storage.

What is the future outlook for 3D NAND technology?

The future of 3D NAND is very promising, with ongoing advancements in increasing layer counts (e.g., beyond 300L, 500L), and the adoption of more advanced multi-level cell technologies like PLC. This evolution will further reduce costs and boost capacities, driving its integration into emerging applications such as advanced AI systems, autonomous vehicles, edge computing, and next-generation data centers, ensuring sustained market growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted