1 10 MW Geothermal Power Market

1 10 MW Geothermal Power Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708617 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

1 10 MW Geothermal Power Market Size

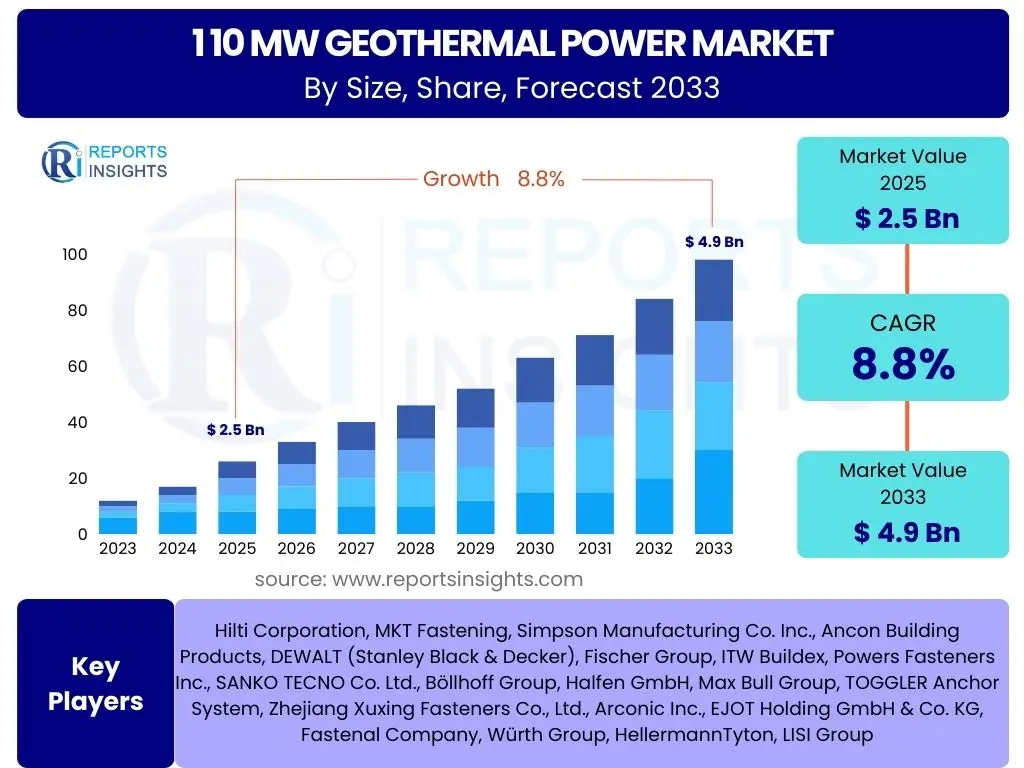

According to Reports Insights Consulting Pvt Ltd, The 1 10 MW Geothermal Power Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.8% between 2025 and 2033. The market is estimated at USD 2.5 Billion in 2025 and is projected to reach USD 4.9 Billion by the end of the forecast period in 2033.

Key 1 10 MW Geothermal Power Market Trends & Insights

User inquiries frequently center on the evolving landscape of renewable energy, specifically how geothermal power within the 1-10 MW range is adapting to global energy demands and technological advancements. Key questions often relate to the adoption rate of binary cycle power plants, the increasing focus on enhanced geothermal systems (EGS) for resource expansion, and the impact of decentralized energy models. Stakeholders are keen to understand which regions are leading in deployment and how policy frameworks are shaping the market trajectory, alongside the integration of digital technologies for improved operational efficiency.

A significant trend observed is the growing interest in small-scale geothermal projects, driven by their potential to provide stable, baseload power in remote or off-grid locations, thus reducing reliance on fossil fuels. This segment also benefits from a renewed focus on energy independence and resilience, particularly in regions prone to grid instability or with abundant, albeit moderate, geothermal resources. Furthermore, innovations in drilling techniques and reservoir management are making previously uneconomical sites viable, opening new avenues for market expansion.

The market is also witnessing a trend towards modular and standardized plant designs, which can significantly reduce installation times and capital expenditures. This modularity allows for greater flexibility in project scaling and can accelerate deployment in diverse geological settings. Additionally, increasing environmental consciousness and the global push for decarbonization are amplifying the appeal of geothermal power as a clean, sustainable energy source, leading to greater investment and research into its untapped potential, especially in the sub-10 MW capacity range which is ideal for community-scale projects.

- Growing adoption of binary cycle technology for lower-temperature resources.

- Increased investment and research into Enhanced Geothermal Systems (EGS).

- Decentralization of energy generation, favoring smaller, distributed power plants.

- Development of modular and standardized plant designs to reduce costs and deployment time.

- Integration of advanced sensor technology and data analytics for reservoir management.

- Expanding direct use applications, such as district heating and industrial processes, alongside power generation.

- Heightened focus on energy security and baseload renewable energy provision.

AI Impact Analysis on 1 10 MW Geothermal Power

User questions regarding artificial intelligence often explore its transformative potential across the entire geothermal project lifecycle, from initial exploration and resource assessment to plant operations and maintenance. Stakeholders are particularly interested in how AI can mitigate geological uncertainties, optimize drilling efficiency, predict equipment failures, and improve energy output, thereby addressing some of the historical challenges associated with geothermal development. There's a strong expectation that AI will lead to more cost-effective and reliable geothermal energy solutions, making the 1-10 MW segment more competitive.

The application of AI in the 1-10 MW geothermal power market is poised to bring significant advancements in resource characterization. Machine learning algorithms can process vast datasets from seismic surveys, well logs, and geological models to identify optimal drilling locations with higher precision, reducing exploration risks and costs. This capability is crucial for smaller-scale projects where upfront investment efficiency is paramount. Predictive analytics powered by AI can also forecast reservoir performance more accurately, enabling better long-term planning and energy output guarantees for investors and off-takers.

Furthermore, AI-driven solutions are enhancing the operational efficiency of existing geothermal plants within this capacity range. Predictive maintenance systems, for instance, utilize real-time sensor data to monitor equipment health, identify anomalies, and anticipate potential failures before they occur. This minimizes downtime, extends asset lifespan, and optimizes maintenance schedules, leading to significant reductions in operational expenditure. AI can also fine-tune plant controls to maximize energy generation based on reservoir conditions and grid demand, ensuring the power plant operates at peak efficiency, which is vital for the economic viability of smaller geothermal installations.

- Enhanced geothermal resource exploration and characterization through machine learning.

- Predictive maintenance for critical plant components, minimizing downtime and operational costs.

- Optimization of drilling operations and well placement to increase efficiency and reduce risks.

- Real-time plant performance optimization and automated control systems for maximum energy output.

- Improved reservoir modeling and simulation for more accurate long-term yield forecasts.

- AI-driven data analysis for better decision-making in project development and risk management.

- Automated fault detection and diagnostics, ensuring higher reliability and safety standards.

Key Takeaways 1 10 MW Geothermal Power Market Size & Forecast

Key takeaways from the 1-10 MW Geothermal Power market size and forecast consistently highlight the segment's robust growth trajectory, driven by increasing demand for reliable, decentralized renewable energy. Users are keenly interested in understanding the underlying factors contributing to this expansion, particularly the role of technological advancements in making smaller-scale geothermal projects more feasible and economically attractive. The forecast suggests a sustained momentum, positioning this segment as a crucial component of future diversified energy portfolios, especially for communities and industries seeking energy independence and reduced carbon footprints.

The market's resilience is underscored by its ability to tap into a broader range of geothermal resources, including lower-temperature reservoirs, which are more common globally. This expanded resource base, combined with modular plant designs and improved drilling techniques, lowers entry barriers and accelerates project development. The growing awareness of geothermal energy's baseload capabilities—providing continuous power irrespective of weather conditions—further solidifies its appeal, making it a preferred choice for grid stabilization and reliable power supply in various regions.

Ultimately, the market forecast reflects a convergence of technological maturity, policy support, and environmental imperatives. Stakeholders should recognize the substantial opportunities for investment and innovation, particularly in regions with significant untapped geothermal potential. The increasing competitiveness of geothermal power in the 1-10 MW range, alongside its environmental benefits and long-term operational stability, positions it as a vital contributor to the global energy transition, promising consistent returns for early adopters and continued expansion throughout the forecast period.

- The 1-10 MW geothermal market is poised for significant and consistent growth through 2033.

- Technological advancements, particularly in binary cycle and EGS, are key enablers of this growth.

- Decentralized energy needs and the demand for baseload renewables are primary market drivers.

- Investment opportunities are expanding in regions with abundant, often lower-temperature, geothermal resources.

- Cost reductions through modular design and improved drilling techniques enhance market attractiveness.

- The market contributes substantially to energy independence and carbon reduction goals globally.

- Enhanced reliability and operational stability make it an attractive long-term energy solution.

1 10 MW Geothermal Power Market Drivers Analysis

The growth of the 1-10 MW Geothermal Power Market is fundamentally propelled by the global imperative to transition towards sustainable and reliable energy sources. This capacity segment, often ideal for localized power generation, directly addresses the increasing demand for energy security and independence, especially in regions with a high reliance on imported fossil fuels or prone to grid instabilities. Government policies, including renewable energy mandates, feed-in tariffs, and carbon pricing mechanisms, play a critical role in incentivizing the development and deployment of geothermal projects, making them more financially viable for investors and developers.

Technological advancements are another significant driver. Innovations in drilling technologies, such as advanced directional drilling and slimhole drilling, reduce exploration and development costs, making smaller geothermal projects more economically attractive. The proliferation of binary cycle power plants, capable of utilizing lower-temperature geothermal fluids (down to 70°C), has expanded the accessible resource base considerably. These advancements mean that geothermal power is no longer limited to areas with high-enthalpy resources, opening up new geographies for deployment of 1-10 MW systems.

Furthermore, the inherent baseload characteristic of geothermal power – its ability to provide continuous, dispatchable energy 24/7 – positions it as a crucial component in stabilizing electricity grids that are increasingly incorporating intermittent renewable sources like solar and wind. This reliability makes 1-10 MW geothermal plants particularly appealing for industrial applications, remote communities, and island nations seeking stable, independent power supply. The growing recognition of geothermal's unique advantages in energy diversification and grid resilience continues to drive its adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Baseload Renewable Energy | +1.8% | Global, particularly Southeast Asia, North America, Europe | Mid-term to Long-term |

| Government Incentives and Policy Support | +1.5% | Europe (e.g., Turkey, Iceland), APAC (e.g., Indonesia, Philippines), Latin America (e.g., Mexico) | Short-term to Mid-term |

| Technological Advancements in Binary Cycle and EGS | +1.6% | North America, Europe, Asia Pacific | Mid-term to Long-term |

| Rising Global Electricity Consumption | +1.3% | Emerging Economies (e.g., India, China), Africa | Mid-term to Long-term |

1 10 MW Geothermal Power Market Restraints Analysis

Despite its significant potential, the 1-10 MW Geothermal Power Market faces several notable restraints that can impede its growth. One of the primary barriers is the high upfront capital cost associated with exploration, drilling, and plant construction. Geothermal projects require substantial initial investment, often involving deep drilling into unknown geological formations, which carries inherent risks and can deter potential investors. This is particularly challenging for smaller-scale projects where the return on investment might take longer compared to other renewable energy sources with lower initial costs.

Another significant restraint is the geological risk and resource uncertainty inherent in geothermal development. Unlike solar or wind, the availability and quality of geothermal resources beneath the Earth's surface are not always precisely known until extensive and costly exploration drilling is undertaken. Unsuccessful drilling or lower-than-expected reservoir temperatures and flow rates can significantly impact project feasibility and lead to substantial financial losses, increasing the perceived risk for developers and financial institutions hesitant to fund such ventures without guaranteed resource assessment.

Furthermore, the long development timelines and complex permitting processes can also act as restraints. Geothermal projects typically require several years from initial exploration to commercial operation, involving numerous environmental impact assessments, land use permits, and regulatory approvals. These bureaucratic hurdles, coupled with potential opposition from local communities regarding land disturbance or perceived environmental impacts, can cause delays and escalate project costs, making the overall development process challenging and less attractive compared to quicker-to-deploy energy alternatives.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Capital Costs | -1.2% | Global, especially developing countries | Short-term to Mid-term |

| Geological Exploration Risks and Resource Uncertainty | -1.0% | Global, new resource areas | Short-term to Mid-term |

| Long Development Timelines and Permitting Challenges | -0.8% | North America, Europe, Asia Pacific | Mid-term |

| Competition from Other Renewable Energy Sources | -0.7% | Global, particularly competitive electricity markets | Mid-term to Long-term |

1 10 MW Geothermal Power Market Opportunities Analysis

The 1-10 MW Geothermal Power Market is ripe with opportunities, particularly in the realm of technological innovation and resource expansion. The development of Enhanced Geothermal Systems (EGS) represents a significant breakthrough, enabling power generation from hot dry rock formations that lack natural permeability or sufficient fluid, thereby expanding the potential geothermal resource base dramatically. This technology allows for the creation of artificial reservoirs, unlocking vast amounts of previously inaccessible heat energy and offering new avenues for development in regions not traditionally considered geothermal hotspots. Investing in EGS research and deployment offers long-term growth prospects for the market.

Another compelling opportunity lies in the integration of geothermal power with direct use applications, such as district heating, greenhouse heating, aquaculture, and industrial processes. For 1-10 MW plants, particularly those with lower-temperature resources, co-production of electricity and heat can significantly improve project economics by monetizing both energy outputs. This combined heat and power (CHP) approach maximizes resource utilization, enhances energy efficiency, and provides diverse revenue streams, making smaller geothermal projects more attractive and sustainable in local communities and industrial clusters.

Furthermore, the growing demand for decentralized and resilient power systems, especially in remote areas or island nations, presents a strong market opportunity for 1-10 MW geothermal solutions. These smaller-scale plants can provide stable, baseload power, reducing reliance on expensive and polluting diesel generators, and contribute to energy independence. The modular nature of many 1-10 MW systems also facilitates quicker deployment and scalability, making them suitable for meeting specific local energy needs and supporting grid stability in isolated or developing regions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Enhanced Geothermal Systems (EGS) | +1.9% | North America, Europe, Australia, Japan | Long-term |

| Integration with Direct Use and Combined Heat and Power (CHP) | +1.4% | Europe, North America, parts of Asia Pacific | Mid-term to Long-term |

| Demand for Decentralized and Resilient Power Systems | +1.7% | Island Nations, Remote Communities, Developing Countries (e.g., Africa, Southeast Asia) | Short-term to Mid-term |

| Co-production with Oil & Gas Wells | +1.2% | North America, Middle East, Russia | Mid-term |

1 10 MW Geothermal Power Market Challenges Impact Analysis

The 1-10 MW Geothermal Power Market faces several distinct challenges that require strategic mitigation to sustain growth. One significant hurdle is the public perception and potential opposition from local communities. Projects can face resistance due to concerns about land use, seismic activity (particularly with EGS), water consumption, or visual impact. Addressing these concerns often requires extensive public engagement, transparent communication about environmental safeguards, and demonstrating tangible local benefits, which can add complexity and delays to project development, particularly for smaller, localized installations.

Another critical challenge is the highly specialized workforce and technical expertise required for geothermal development. The industry demands deep knowledge in geology, geophysics, drilling engineering, reservoir management, and power plant operations. A shortage of skilled professionals can hinder project execution, increase labor costs, and limit the scalability of development efforts, especially in emerging geothermal markets where local expertise may be scarce. Investing in training and capacity building programs is essential to overcome this bottleneck.

Furthermore, the relatively smaller scale of 1-10 MW projects can sometimes struggle to achieve economies of scale compared to larger utility-scale power plants. While modularity helps, the per-unit cost of development for smaller projects might remain higher without further standardization and innovation in supply chains. Additionally, securing financing for these mid-size projects can be challenging, as they may fall between the scope of micro-financing and large-scale infrastructure funds, requiring tailored financial instruments and risk-sharing mechanisms to attract sufficient investment capital.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Community Acceptance and Environmental Concerns | -0.9% | Global, particularly densely populated areas | Short-term to Mid-term |

| Lack of Specialized Workforce and Technical Expertise | -0.7% | Emerging Geothermal Markets (e.g., Africa, Latin America) | Mid-term to Long-term |

| Securing Project Financing for Mid-Scale Projects | -0.6% | Global, particularly private developers | Short-term to Mid-term |

| Seismic Risk Management, especially for EGS Projects | -0.5% | Regions with seismic activity, areas deploying EGS | Mid-term |

1 10 MW Geothermal Power Market - Updated Report Scope

This report provides a comprehensive analysis of the 1-10 MW Geothermal Power Market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. It covers market sizing and forecasts from 2025 to 2033, highlighting key drivers, restraints, opportunities, and challenges. The report aims to equip stakeholders with critical information for strategic decision-making and investment planning within this crucial renewable energy segment.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.5 Billion |

| Market Forecast in 2033 | USD 4.9 Billion |

| Growth Rate | 8.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Geothermal Power Solutions Inc., Earth Heat Renewables, Terra Geothermal Energy, Volcanic Power Systems, Global Heat Resources, Summit Geopower, Green Earth Energy Solutions, GeoThermal Innovations Group, Core Energy Systems, Blue Planet Geothermal, Prime Geopower, Ocean Thermal Energy, Deep Earth Energy Partners, Alpine Geothermal, Horizon Renewable Energy. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The 1-10 MW Geothermal Power Market is comprehensively segmented to provide granular insights into its diverse components and drivers. This segmentation allows for a detailed understanding of how different technologies, applications, and capacity ranges contribute to the overall market growth and where the most significant opportunities lie. Analyzing these segments helps stakeholders identify niche markets, tailor strategies, and optimize investments to align with specific market demands and resource characteristics. Understanding the interplay between these segments is crucial for navigating the evolving landscape of geothermal energy and for developing targeted solutions that cater to various user requirements.

The segmentation by type, specifically focusing on Dry Steam, Flash Steam, and Binary Cycle technologies, highlights the technological preferences and efficiencies associated with different geothermal resource temperatures. Binary cycle plants, for instance, are increasingly dominant due to their ability to exploit lower-temperature resources, significantly expanding the addressable market for 1-10 MW installations. This technological diversity underscores the adaptability of geothermal power to a wide range of geological conditions and project scales, making it a versatile renewable energy solution.

Furthermore, the segmentation by application—On-grid, Off-grid Power Generation, and Direct Use—reveals the broad utility of geothermal energy beyond electricity production. While grid-connected projects contribute to national power grids, off-grid solutions address energy poverty and remote access challenges. Direct use applications, which often utilize residual heat, offer an additional layer of economic viability and sustainability, particularly for smaller plants. This multi-faceted utility demonstrates geothermal's potential to serve diverse energy needs, from large-scale industrial heating to localized community power, reinforcing its role as a flexible and comprehensive energy source.

- By Type:

- Dry Steam

- Flash Steam

- Binary Cycle

- By Application:

- On-grid Power Generation

- Off-grid Power Generation

- Direct Use (District Heating, Agricultural, Industrial)

- By Output Capacity:

- 1 MW - 5 MW

- 5 MW - 10 MW

Regional Highlights

- North America: Driven by technological advancements, favorable government incentives, and a robust pipeline of EGS projects, particularly in the Western U.S. and Canada. The region focuses on both on-grid and direct use applications.

- Europe: Leading in the deployment of binary cycle plants and district heating networks, with strong government support in countries like Iceland, Turkey, and Italy. Emphasis on decarbonization and energy independence fuels growth.

- Asia Pacific (APAC): Significant untapped potential in countries like Indonesia, Philippines, Japan, and China, where increasing energy demand and rich geothermal resources converge. Growing investment in both utility-scale and decentralized projects.

- Latin America: Emerging market with substantial resources in countries such as Mexico, Chile, and Costa Rica. Focus on developing baseload renewable energy to support growing industrial and residential sectors.

- Middle East and Africa (MEA): Kenya and Ethiopia are key players in East Africa's Rift Valley, possessing vast geothermal potential. The region is increasingly investing in geothermal for energy security and economic development, particularly for rural electrification.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the 1 10 MW Geothermal Power Market.- Geothermal Power Solutions Inc.

- Earth Heat Renewables

- Terra Geothermal Energy

- Volcanic Power Systems

- Global Heat Resources

- Summit Geopower

- Green Earth Energy Solutions

- GeoThermal Innovations Group

- Core Energy Systems

- Blue Planet Geothermal

- Prime Geopower

- Ocean Thermal Energy

- Deep Earth Energy Partners

- Alpine Geothermal

- Horizon Renewable Energy

Frequently Asked Questions

What is the projected growth rate for the 1-10 MW Geothermal Power Market?

The 1-10 MW Geothermal Power Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.8% between 2025 and 2033, driven by increasing demand for reliable renewable energy.

How is AI impacting the development and operation of 1-10 MW geothermal power plants?

AI is significantly impacting the market by enhancing geothermal resource exploration, optimizing drilling operations, implementing predictive maintenance for plant components, and improving overall operational efficiency and energy output.

What are the main technological trends driving the 1-10 MW Geothermal Power Market?

Key technological trends include the widespread adoption of binary cycle technology, advanced research and deployment of Enhanced Geothermal Systems (EGS), and the development of modular and standardized plant designs that reduce costs and accelerate deployment.

What are the primary challenges faced by the 1-10 MW Geothermal Power Market?

The primary challenges include high upfront capital costs, geological exploration risks and resource uncertainty, long development timelines with complex permitting processes, and potential community opposition regarding environmental concerns.

Which regions are leading in the deployment and growth of 1-10 MW geothermal power?

North America and Europe are leading due to technological advancements and strong policy support. Asia Pacific, particularly countries like Indonesia and the Philippines, also shows significant growth due to vast untapped resources and rising energy demand.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted