Wind Turbine Gearbox Repair and Refurbishment Market

Wind Turbine Gearbox Repair and Refurbishment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701180 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Wind Turbine Gearbox Repair and Refurbishment Market Size

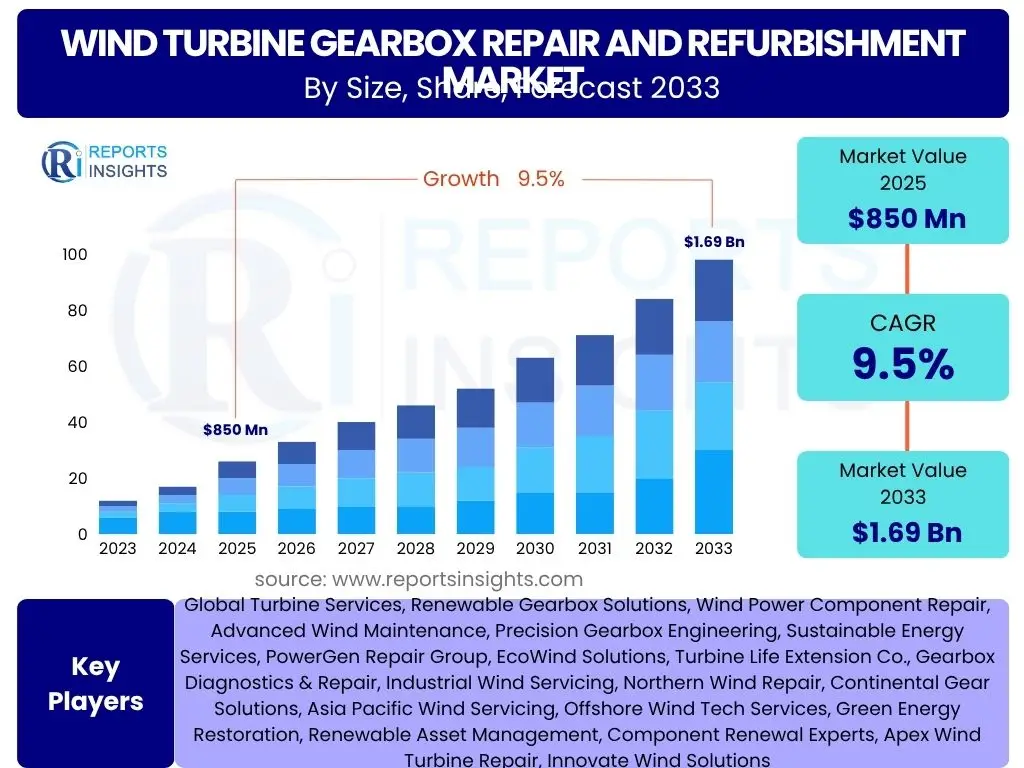

According to Reports Insights Consulting Pvt Ltd, The Wind Turbine Gearbox Repair and Refurbishment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. This robust growth is primarily driven by the expanding global installed base of wind turbines, the increasing average age of operational assets, and a heightened focus on extending the operational lifespan of existing infrastructure. The market is estimated at USD 850 Million in 2025 and is projected to reach USD 1.69 Billion by the end of the forecast period in 2033. This significant expansion underscores the critical role of maintenance and repair services in the sustainable growth of the renewable energy sector, moving beyond new installations to optimize asset performance and longevity.

The market's valuation reflects a growing recognition among asset owners and operators of the economic benefits associated with repairing and refurbishing high-value components like gearboxes, rather than opting for full replacement. Gearboxes are among the most critical and failure-prone components in a wind turbine, making their efficient repair and refurbishment essential for minimizing downtime and maximizing energy production. The increasing demand for specialized repair techniques, advanced diagnostics, and on-site servicing solutions contributes significantly to this market expansion. Furthermore, the rising adoption of predictive maintenance strategies, enabled by IoT and advanced analytics, is improving the efficiency and effectiveness of repair operations, further bolstering market growth.

Key Wind Turbine Gearbox Repair and Refurbishment Market Trends & Insights

Users frequently inquire about the evolving landscape of wind turbine gearbox maintenance, seeking to understand the significant shifts and innovations shaping the industry. Key trends revolve around leveraging advanced technologies for efficiency, extending asset life, and adapting to the growing scale of wind energy projects. Insights indicate a move towards more proactive and data-driven maintenance approaches, driven by the increasing maturity of the global wind fleet and the imperative to optimize operational expenditures.

The market is experiencing a paradigm shift from reactive repair to predictive and preventive maintenance, fueled by digitalization and the integration of sophisticated monitoring systems. This transition is not only enhancing the reliability of wind turbines but also significantly reducing unexpected downtimes and associated costs. Furthermore, there is a rising emphasis on modular repair solutions and component-level refurbishment, which offer more cost-effective and environmentally friendly alternatives to full gearbox replacement. The development of specialized repair facilities equipped with advanced machinery and skilled personnel is also a notable trend, reflecting the increasing complexity and scale of modern wind turbine gearboxes.

- Shift from reactive to predictive maintenance using advanced diagnostics and IoT.

- Increased demand for on-site repair and mobile service units to minimize downtime.

- Growing adoption of modular repair and component-level refurbishment strategies.

- Emphasis on extending the operational life of existing wind assets.

- Development of specialized high-capacity repair facilities for larger gearboxes.

- Integration of advanced materials and coatings for enhanced durability and repair.

- Focus on circular economy principles, promoting reusability and sustainability in repairs.

AI Impact Analysis on Wind Turbine Gearbox Repair and Refurbishment

Common user questions regarding AI's influence in the wind turbine gearbox repair and refurbishment domain often center on how artificial intelligence can enhance predictive capabilities, optimize maintenance schedules, and improve the overall efficiency and cost-effectiveness of operations. Users are keen to understand the practical applications of AI, its limitations, and its potential to revolutionize traditional maintenance practices. The analysis indicates that AI is poised to significantly transform this sector by enabling smarter, more proactive, and data-driven decision-making processes.

AI's primary impact lies in its ability to analyze vast amounts of operational data from sensors, SCADA systems, and historical failure records to identify patterns and anomalies indicative of impending gearbox failures. This capability allows for highly accurate predictive maintenance, shifting from time-based or reactive repairs to condition-based interventions, thereby reducing unplanned downtime and optimizing repair windows. Furthermore, AI algorithms can optimize spare parts inventory management, forecast future repair needs, and even assist in quality control during refurbishment processes. While challenges such as data quality, integration complexity, and the need for specialized AI expertise exist, the long-term benefits in terms of efficiency, reliability, and cost savings are substantial, positioning AI as a critical enabler for the future of wind turbine maintenance.

- Enhanced predictive maintenance through advanced anomaly detection and failure prediction.

- Optimized maintenance scheduling and resource allocation using AI-driven insights.

- Improved fault diagnosis accuracy, reducing the need for costly manual inspections.

- Automated analysis of operational data for early detection of gearbox component wear.

- Streamlined inventory management for spare parts, reducing holding costs and lead times.

- Potential for AI-guided robotic repair or automated inspection within confined spaces.

- Development of AI-powered digital twins for comprehensive gearbox health monitoring.

Key Takeaways Wind Turbine Gearbox Repair and Refurbishment Market Size & Forecast

Users frequently seek concise summaries of the most critical insights from the wind turbine gearbox repair and refurbishment market size and forecast. The primary inquiries revolve around the overall investment attractiveness, major growth catalysts, and the most promising future avenues within the sector. The key takeaways underscore a market poised for significant expansion, driven by foundational shifts in renewable energy infrastructure management and technological advancements in maintenance.

The market's projected growth indicates a strong and sustained demand for specialized repair and refurbishment services throughout the forecast period. This growth is intrinsically linked to the global push for renewable energy, which results in a continuous increase in the installed base of wind turbines, many of which are approaching or have exceeded their initial operational lifespans. Furthermore, the economic advantages of extending asset life through repair over costly replacement, coupled with the rising sophistication of repair technologies, are fundamental drivers. Stakeholders looking to enter or expand within this market should focus on developing advanced diagnostic capabilities, efficient logistics for large components, and expertise in diverse gearbox types to capitalize on the robust opportunities presented.

- The market is set for substantial growth, driven by an aging global wind turbine fleet.

- Cost-effectiveness of repair and refurbishment over replacement is a primary market driver.

- Technological advancements in diagnostics and repair techniques are crucial for market evolution.

- Opportunities exist in specialized services for offshore wind and high-capacity turbines.

- Increased focus on predictive maintenance will lead to more efficient repair cycles.

Wind Turbine Gearbox Repair and Refurbishment Market Drivers Analysis

The wind turbine gearbox repair and refurbishment market is propelled by a confluence of factors, primarily stemming from the global expansion of wind energy and the inherent operational challenges associated with large-scale machinery. As wind energy capacity continues to grow worldwide, so does the population of operational turbines, many of which are reaching a critical age where component wear and tear become significant. This demographic shift within the wind fleet naturally drives demand for robust and reliable repair solutions to extend asset lifespan and maintain energy production efficiency.

Furthermore, the economic imperative to reduce operational and maintenance (O&M) costs plays a crucial role. Repairing and refurbishing existing gearboxes often presents a significantly more cost-effective alternative to purchasing and installing entirely new units, especially for older turbine models where spare parts availability might be limited. Technological advancements in repair methodologies, including advanced welding, machining, and material science, also contribute by making complex repairs more feasible and durable. The increasing focus on sustainability and circular economy principles within the energy sector further supports the repair and reuse model, minimizing waste and resource consumption associated with manufacturing new components.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Aging Wind Turbine Fleet & Component Wear | +1.5% | Global, particularly Europe & North America | Short-to-Medium Term |

| Cost-Effectiveness of Repair vs. Replacement | +1.2% | Global | Short-to-Medium Term |

| Growth in Global Wind Energy Installations | +1.0% | Asia Pacific, Europe, North America | Medium-to-Long Term |

| Advancements in Repair & Diagnostics Technologies | +0.8% | Global | Medium Term |

Wind Turbine Gearbox Repair and Refurbishment Market Restraints Analysis

Despite the strong growth drivers, the wind turbine gearbox repair and refurbishment market faces several significant restraints that can impede its full potential. One of the primary challenges is the high upfront cost and logistical complexity associated with transporting large, heavy gearbox components to specialized repair facilities. This often requires heavy-lift cranes and specialized transport, adding substantial expense and planning to the repair process. Furthermore, the extended downtime required for comprehensive repair or refurbishment operations can result in significant revenue losses for turbine operators, impacting their willingness to opt for lengthy repair cycles.

Another major restraint is the shortage of highly skilled technicians and engineers specializing in complex wind turbine gearbox mechanics. The intricate nature of these components demands a specialized skill set that is not widely available, leading to labor shortages and increased service costs. Additionally, the rapid evolution of wind turbine technology, including the increasing size and complexity of new gearbox designs, can render older repair methodologies less effective or create new challenges for maintaining a standardized repair approach. Competition from new turbine sales, especially during periods of favorable government incentives for new installations, can also divert investment away from maintenance and refurbishment, as operators might prioritize upgrading their fleet.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Repair Costs & Extended Downtime | -0.9% | Global | Short-to-Medium Term |

| Shortage of Skilled Technicians & Expertise | -0.7% | Global | Short-to-Medium Term |

| Logistical Challenges of Large Components | -0.6% | Global | Short-to-Medium Term |

| Competition from New Turbine Sales & Upgrades | -0.5% | Global, especially developing markets | Medium Term |

Wind Turbine Gearbox Repair and Refurbishment Market Opportunities Analysis

The wind turbine gearbox repair and refurbishment market is ripe with opportunities, particularly driven by the accelerating growth of offshore wind energy and the global trend of repowering older wind farms. Offshore wind turbines, with their harsher operating environments and greater capacities, present more frequent and complex gearbox challenges, thereby creating a specialized and high-value niche for repair and refurbishment services. The increasing number of repowering projects, where older turbines are replaced or upgraded with more efficient components, also provides a significant opportunity for refurbishing or repurposing existing gearboxes, extending their useful life in other applications or markets.

Furthermore, the growing adoption of advanced diagnostic and monitoring technologies, such as condition monitoring systems (CMS) and predictive analytics, creates opportunities for service providers to offer value-added solutions beyond basic repairs. This includes proactive maintenance planning, optimized component replacement strategies, and data-driven insights that improve overall asset reliability and performance. The expansion into emerging wind energy markets in Asia Pacific, Latin America, and Africa also presents new geographical opportunities for companies capable of establishing local service infrastructure. Customization of repair solutions for specific gearbox types and turbine models, coupled with long-term service agreements, can also secure steady revenue streams for market players.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Offshore Wind Farms | +1.2% | Europe, Asia Pacific (esp. China), North America | Medium-to-Long Term |

| Growth in Wind Turbine Repowering Projects | +1.0% | Europe, North America | Medium Term |

| Adoption of Advanced Diagnostics & Predictive Maintenance | +0.9% | Global | Short-to-Medium Term |

| Emerging Wind Markets in Asia Pacific, Latin America & Africa | +0.7% | Asia Pacific, Latin America, MEA | Medium-to-Long Term |

Wind Turbine Gearbox Repair and Refurbishment Market Challenges Impact Analysis

The wind turbine gearbox repair and refurbishment market faces a range of challenges that can hinder its operational efficiency and market growth. One significant challenge is the ongoing supply chain volatility, which can lead to delays and increased costs for critical spare parts and raw materials required for repairs. Geopolitical events, trade disputes, and natural disasters can disrupt global supply networks, making it difficult for service providers to procure necessary components in a timely manner. This volatility impacts repair turnaround times and overall project profitability.

Another major challenge is the lack of standardization across different wind turbine gearbox models and manufacturers. Each OEM often uses proprietary designs and components, which complicates repair processes, requires specialized tools, and necessitates a wide inventory of unique spare parts. This fragmentation makes it challenging for independent service providers to achieve economies of scale and often requires significant investment in diverse technical expertise and equipment. Furthermore, stringent environmental regulations and disposal requirements for lubricants and hazardous materials used in gearbox operations and repairs add complexity and cost. Ensuring high-quality, durable repairs that meet original equipment specifications, especially for older or heavily worn gearboxes, also remains a constant technical challenge, requiring continuous innovation in repair methodologies and quality assurance processes.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Volatility & Parts Availability | -0.8% | Global | Short-to-Medium Term |

| Lack of Standardization Across Gearbox Models | -0.7% | Global | Medium Term |

| High Quality Control & Technical Complexity of Repairs | -0.6% | Global | Short-to-Medium Term |

| Environmental Regulations & Waste Management | -0.5% | Europe, North America, key developing markets | Medium-to-Long Term |

Wind Turbine Gearbox Repair and Refurbishment Market - Updated Report Scope

This market research report provides an in-depth analysis of the global wind turbine gearbox repair and refurbishment market, encompassing historical data, current market dynamics, and future projections. The scope includes a detailed examination of market size, growth drivers, restraints, opportunities, and challenges. It further segments the market by various service types, component types, turbine capacities, end-users, and key geographical regions, offering a comprehensive view for strategic decision-making. The report aims to equip stakeholders with actionable insights to navigate the evolving landscape of wind energy asset management.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 850 Million |

| Market Forecast in 2033 | USD 1.69 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Turbine Services, Renewable Gearbox Solutions, Wind Power Component Repair, Advanced Wind Maintenance, Precision Gearbox Engineering, Sustainable Energy Services, PowerGen Repair Group, EcoWind Solutions, Turbine Life Extension Co., Gearbox Diagnostics & Repair, Industrial Wind Servicing, Northern Wind Repair, Continental Gear Solutions, Asia Pacific Wind Servicing, Offshore Wind Tech Services, Green Energy Restoration, Renewable Asset Management, Component Renewal Experts, Apex Wind Turbine Repair, Innovate Wind Solutions |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The wind turbine gearbox repair and refurbishment market is comprehensively segmented to provide a granular understanding of its dynamics across various dimensions. This segmentation allows for a detailed analysis of specific market niches, demand patterns, and competitive landscapes. By breaking down the market based on service type, component, turbine type, capacity, and end-user, stakeholders can identify precise growth opportunities and tailor their strategies to specific market needs. Each segment reflects unique operational demands, technological requirements, and customer preferences, collectively contributing to the overall market complexity and growth trajectory.

The segmentation highlights the diverse range of services demanded in the market, from emergency repairs to long-term predictive maintenance contracts. It also emphasizes the critical role of specific gearbox components in driving repair demand. The distinction between onshore and offshore turbines, and varying capacities, underscores the different operational environments and technical challenges that influence repair needs and solutions. Furthermore, analyzing the end-user segments helps in understanding the procurement patterns and service expectations of different market participants, ranging from original equipment manufacturers to independent power producers.

- By Service Type: Repair, Refurbishment, Component Overhaul, Predictive Maintenance, Corrective Maintenance, Preventive Maintenance

- By Component: Bearings, Gears, Shafts, Housings, Seals, Lubrication Systems

- By Turbine Type: Onshore Wind Turbines, Offshore Wind Turbines

- By Capacity: Less than 2 MW, 2 MW - 5 MW, More than 5 MW

- By End-User: Original Equipment Manufacturers (OEMs), Independent Service Providers (ISPs), Utilities, Private Power Producers

Regional Highlights

The global wind turbine gearbox repair and refurbishment market exhibits significant regional variations, driven by factors such as the maturity of wind energy infrastructure, renewable energy policies, and the pace of new installations. Each region presents unique opportunities and challenges for service providers, necessitating tailored approaches for market penetration and growth. Understanding these regional dynamics is crucial for developing effective business strategies and resource allocation plans.

Europe, a pioneering region in wind energy, possesses a mature and aging fleet of wind turbines, driving a strong and consistent demand for repair and refurbishment services. This region also leads in offshore wind development, which presents higher value and more complex repair opportunities. North America, particularly the United States, is experiencing substantial growth in wind energy, leading to an increasing need for O&M services for its expanding installed base. Supportive government policies and the widespread adoption of renewable energy targets further fuel market demand here. Asia Pacific is emerging as the fastest-growing market, primarily led by China, which has the largest installed wind capacity globally. The sheer volume of turbines, coupled with a focus on extending asset life, creates immense opportunities for repair and refurbishment services in this region. Latin America, the Middle East, and Africa are nascent but rapidly developing markets, with growing interest in wind energy and a rising need for local service capabilities as wind farms come online and mature.

- Europe: Dominates the market due to an extensive and aging installed base of wind turbines, particularly strong demand from pioneering offshore wind projects. Emphasis on life extension and advanced repair techniques.

- North America: Significant market growth driven by increasing wind energy capacity, particularly in the U.S., and a growing focus on optimizing operational efficiency of existing assets.

- Asia Pacific (APAC): Fastest-growing region, primarily fueled by massive installations in China, India, and Australia. High potential for new service partnerships and localized repair solutions.

- Latin America, Middle East, and Africa (MEA): Emerging markets with burgeoning wind energy sectors. While smaller in current market share, they represent long-term growth potential as their wind farms mature and require maintenance.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Wind Turbine Gearbox Repair and Refurbishment Market.- Global Turbine Services

- Renewable Gearbox Solutions

- Wind Power Component Repair

- Advanced Wind Maintenance

- Precision Gearbox Engineering

- Sustainable Energy Services

- PowerGen Repair Group

- EcoWind Solutions

- Turbine Life Extension Co.

- Gearbox Diagnostics & Repair

- Industrial Wind Servicing

- Northern Wind Repair

- Continental Gear Solutions

- Asia Pacific Wind Servicing

- Offshore Wind Tech Services

- Green Energy Restoration

- Renewable Asset Management

- Component Renewal Experts

- Apex Wind Turbine Repair

- Innovate Wind Solutions

Frequently Asked Questions

Analyze common user questions about the Wind Turbine Gearbox Repair and Refurbishment market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Wind Turbine Gearbox Repair and Refurbishment Market?

The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033, reaching an estimated value of USD 1.69 Billion by 2033.

What are the primary drivers for this market's growth?

Key drivers include the aging global wind turbine fleet, the cost-effectiveness of repairing components versus full replacement, the continuous expansion of global wind energy installations, and advancements in repair and diagnostic technologies.

How is AI impacting the wind turbine gearbox repair and refurbishment sector?

AI significantly impacts the sector by enabling enhanced predictive maintenance, optimizing maintenance scheduling, improving fault diagnosis accuracy, and streamlining spare parts management through advanced data analysis.

Which regions are key contributors to the Wind Turbine Gearbox Repair and Refurbishment Market?

Europe and North America are mature markets with substantial demand from aging fleets, while Asia Pacific, particularly China, is the fastest-growing region due to rapid new installations and a focus on asset longevity. Latin America, the Middle East, and Africa are emerging markets.

What are the main challenges faced by the market?

Major challenges include supply chain volatility for spare parts, the lack of standardization across various gearbox models, high quality control requirements and technical complexity of repairs, and the logistical challenges associated with transporting large components.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted