Takaful Market

Takaful Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702580 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Takaful Market Size

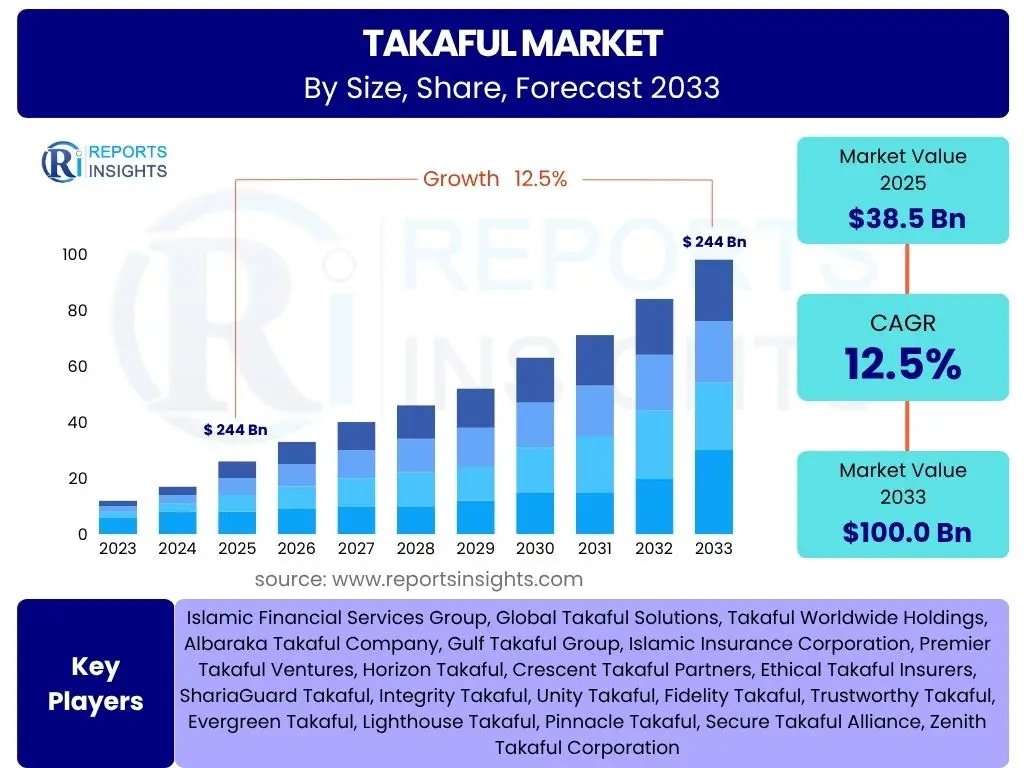

According to Reports Insights Consulting Pvt Ltd, The Takaful Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2033. The market is estimated at USD 38.5 Billion in 2025 and is projected to reach USD 100.0 Billion by the end of the forecast period in 2033.

Key Takaful Market Trends & Insights

The Takaful market is experiencing significant transformation, driven by evolving consumer demands for ethical financial products and technological advancements. Key user inquiries often revolve around the market's trajectory, the integration of digital solutions, and the diversification of Takaful product offerings. Analysis indicates a strong inclination towards digital distribution channels, heightened awareness among Muslim populations, and a growing interest from non-Muslim consumers seeking ethical investment and insurance options. This evolution is fostering greater product innovation, moving beyond traditional family and general Takaful to encompass specialized and niche segments.

The market is further shaped by increasing regulatory support and standardization efforts across various jurisdictions, particularly in the Middle East and Southeast Asia, which are pivotal hubs for Islamic finance. This regulatory clarity is enhancing operational efficiency and market confidence. Furthermore, there's a discernible shift towards incorporating Environmental, Social, and Governance (ESG) principles within Takaful operations, aligning with broader global ethical investment trends. These factors collectively contribute to a dynamic market landscape characterized by sustained growth and expanding reach.

- Digitalization of Takaful operations and distribution channels.

- Growing demand for Sharia-compliant wealth management and investment products.

- Increased focus on Microtakaful to cater to underserved populations.

- Expansion into new geographical markets beyond traditional Islamic finance hubs.

- Product diversification, including specialized health, travel, and corporate Takaful.

- Harmonization of regulatory frameworks across different regions.

- Integration of Environmental, Social, and Governance (ESG) principles.

AI Impact Analysis on Takaful

User queries frequently explore how artificial intelligence (AI) is set to revolutionize the Takaful sector, questioning its potential benefits in operational efficiency, customer engagement, and risk assessment, as well as considering any Sharia compliance implications. AI is poised to significantly enhance various facets of Takaful operations, from streamlining underwriting processes and claims management to developing highly personalized product offerings. By leveraging advanced data analytics, AI algorithms can identify patterns, predict risks with greater accuracy, and automate routine tasks, thereby reducing operational costs and improving service delivery speeds. This technological integration is expected to lead to more efficient resource allocation within Takaful funds and improve the overall participant experience.

However, the adoption of AI in Takaful also presents unique considerations, particularly regarding data privacy, algorithmic transparency, and ensuring adherence to Sharia principles in automated decision-making. Stakeholders are keen to understand how AI can be implemented while maintaining the ethical foundations of Takaful, such as fairness, transparency, and mutuality. The balance between technological advancement and foundational Islamic finance values is crucial. Despite these challenges, the overwhelming consensus points towards AI as a transformative force, enabling Takaful providers to offer more competitive, accessible, and participant-centric solutions, ultimately fostering market growth and innovation.

- Enhanced data analytics for improved risk assessment and underwriting.

- Automation of claims processing, leading to faster settlements.

- Personalized Takaful product development based on individual participant behavior.

- Advanced fraud detection and prevention mechanisms.

- Improved customer service through AI-powered chatbots and virtual assistants.

- Optimization of operational efficiency and reduction of administrative costs.

- Predictive modeling for better capital management and investment strategies.

Key Takeaways Takaful Market Size & Forecast

Analysis of common user questions regarding the Takaful market's size and forecast reveals a strong interest in understanding the primary growth catalysts and the sustainability of its expansion. A key takeaway is the robust and consistent double-digit growth projected for the Takaful market, underscoring its resilience and increasing acceptance globally. This growth is fundamentally driven by the expanding global Muslim population, rising awareness of Sharia-compliant financial products, and significant governmental support in key Islamic finance hubs. The market's potential for expansion is not solely confined to traditional Muslim-majority regions but is increasingly drawing interest from diverse demographic segments seeking ethical and transparent financial solutions, positioning Takaful as a viable alternative to conventional insurance.

Furthermore, the forecast highlights the pivotal role of digital transformation and product innovation in accelerating market penetration and accessibility. The shift towards online distribution and the introduction of specialized Takaful products catering to specific needs are expanding the market's reach to underserved populations and niche segments. The steady increase in Takaful assets and contributions, coupled with continuous investment in technology and human capital, reinforces the optimistic outlook. This trajectory suggests that the Takaful market is poised for significant future growth, driven by a combination of demographic trends, ethical considerations, and technological advancements, solidifying its position within the broader financial services landscape.

- The Takaful market is set for substantial growth, projecting to nearly triple in size by 2033.

- Growth is primarily fueled by increasing awareness, favorable demographics, and supportive regulatory environments.

- Digitalization and FinTech integration are critical enablers for market expansion and efficiency.

- Emerging markets, particularly in Southeast Asia and the Middle East, will continue to be growth epicenters.

- Product innovation, including specialized and micro-Takaful offerings, is broadening market appeal.

Takaful Market Drivers Analysis

The Takaful market's consistent growth is propelled by several fundamental drivers that reinforce its appeal and expand its operational scope. A primary catalyst is the burgeoning global Muslim population, coupled with increasing disposable incomes and a heightened demand for financial products that align with Islamic principles. This demographic shift naturally leads to a larger addressable market for Sharia-compliant insurance solutions. Simultaneously, governments and regulatory bodies in key Islamic finance jurisdictions are actively implementing supportive frameworks and policies, which foster a stable and conducive environment for Takaful operators, encouraging both domestic and international players to enter and expand within these markets.

Beyond demographics and regulatory support, the market is significantly benefiting from rising consumer awareness regarding the ethical and mutual benefits of Takaful over conventional insurance. This growing understanding is driven by educational initiatives and the inherent transparency and fairness embedded in Takaful models. Furthermore, technological advancements, particularly in digitalization and mobile connectivity, are enabling Takaful providers to reach wider audiences through online platforms, streamlining processes from policy issuance to claims settlement, thereby enhancing accessibility and convenience for participants.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Global Muslim Population and Disposable Income | +1.8% | Global, particularly MEA & Southeast Asia | Long-term (2025-2033) |

| Increasing Awareness of Sharia-Compliant Financial Products | +1.5% | MEA, Southeast Asia, South Asia | Mid to Long-term (2025-2033) |

| Favorable Regulatory Support and Government Initiatives | +1.2% | Malaysia, UAE, Saudi Arabia, Indonesia | Mid-term (2025-2029) |

| Digital Transformation and FinTech Integration | +1.0% | Global, especially urban centers | Mid to Long-term (2025-2033) |

| Product Innovation and Diversification | +0.8% | Global | Mid-term (2025-2029) |

Takaful Market Restraints Analysis

Despite its promising growth trajectory, the Takaful market faces several restraints that could impede its full potential. A significant challenge lies in the lack of standardized regulatory frameworks across different jurisdictions. While some regions have well-established Takaful regulations, others are still developing, leading to inconsistencies that can complicate cross-border operations and hinder the scalability of Takaful models globally. This regulatory disparity often results in increased compliance costs and operational complexities for Takaful providers aiming for international expansion, creating a fragmented market landscape.

Another major restraint is the relatively low level of public awareness and understanding of Takaful principles, particularly in non-traditional Islamic finance markets. Many potential participants, both Muslim and non-Muslim, remain unfamiliar with how Takaful operates, its ethical underpinnings, and its distinctions from conventional insurance. This knowledge gap necessitates significant investment in public education and outreach, which can be resource-intensive. Furthermore, intense competition from well-established conventional insurance providers, who often possess larger capital bases, extensive distribution networks, and a longer market presence, poses a continuous challenge for Takaful operators to capture and retain market share, especially in saturated insurance markets.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lack of Standardized Regulatory Frameworks | -1.3% | Global, particularly emerging markets | Long-term (2025-2033) |

| Low Awareness and Education among Potential Participants | -1.0% | Non-OIC countries, rural areas in OIC countries | Long-term (2025-2033) |

| Intense Competition from Conventional Insurance Providers | -0.8% | Global | Long-term (2025-2033) |

| Limited Distribution Channels and Infrastructure in Some Regions | -0.7% | Africa, Latin America, parts of Asia | Mid-term (2025-2029) |

Takaful Market Opportunities Analysis

The Takaful market is ripe with opportunities that can significantly accelerate its growth and expand its global footprint. A prominent opportunity lies in tapping into underserved and untapped markets, not only within Muslim-majority nations where Takaful penetration is still low but also among non-Muslim populations globally who are increasingly seeking ethical, socially responsible, and transparent financial products. This broader appeal, driven by shared values of fairness and communal support, presents a substantial avenue for market expansion beyond traditional demographics. Furthermore, the burgeoning demand for Microtakaful, aimed at low-income segments and small businesses, represents a vast, largely unaddressed market. This segment often lacks access to conventional insurance and could greatly benefit from affordable, Sharia-compliant protection solutions.

Another significant opportunity stems from the rapid advancements in digital technologies and FinTech. The integration of mobile applications, blockchain, and artificial intelligence can revolutionize Takaful distribution, underwriting, and claims processing, making products more accessible, efficient, and cost-effective. These technological innovations can reduce operational overheads, enhance customer experience, and enable Takaful providers to scale their operations quickly. Moreover, diversification into new product lines, such as specialized corporate Takaful, health Takaful, and Sharia-compliant investment-linked Takaful products, allows operators to cater to evolving participant needs and capture higher-value segments, further strengthening the market's overall resilience and growth potential.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Untapped Markets (including non-Muslims seeking ethical products) | +1.5% | Global, particularly Western countries | Long-term (2025-2033) |

| Growth in Microtakaful and Digital Takaful Offerings | +1.2% | Emerging markets (Africa, Southeast Asia, South Asia) | Mid to Long-term (2025-2033) |

| Leveraging FinTech and InsurTech for Enhanced Operations | +1.0% | Global | Mid to Long-term (2025-2033) |

| Diversification into New Product Lines (e.g., corporate, health, investment-linked) | +0.9% | Global | Mid-term (2025-2029) |

| Strategic Partnerships and Collaborations | +0.7% | Global | Mid-term (2025-2029) |

Takaful Market Challenges Impact Analysis

Despite the positive outlook, the Takaful market faces several inherent challenges that demand strategic navigation. One significant challenge is the ongoing talent shortage, particularly for professionals with dual expertise in both actuarial science/insurance and Islamic finance principles. This scarcity of qualified personnel, especially Sharia scholars with practical industry experience, can hinder product innovation, risk management, and overall operational efficiency, making it difficult for Takaful operators to scale effectively and maintain robust governance structures in line with Sharia requirements.

Furthermore, maintaining strict Sharia compliance in an increasingly complex and technologically driven financial landscape presents an evolving challenge. As Takaful products become more sophisticated and digital platforms integrate advanced analytics, ensuring that all operations, investments, and profit-sharing mechanisms strictly adhere to Islamic ethical guidelines requires continuous oversight and adaptation. This compliance complexity can slow down product development and market entry. Additionally, data privacy and cybersecurity concerns are growing, particularly with the widespread adoption of digital platforms. Takaful operators must invest heavily in robust security infrastructure to protect sensitive participant data, build trust, and mitigate the risks of cyber threats, which adds to operational costs and complexity.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Talent Shortage in Sharia and Takaful Expertise | -1.0% | Global | Long-term (2025-2033) |

| Maintaining Sharia Compliance in a Rapidly Evolving Digital Landscape | -0.8% | Global | Long-term (2025-2033) |

| Data Privacy and Cybersecurity Concerns | -0.7% | Global | Mid to Long-term (2025-2033) |

| Economic Volatility and Geopolitical Instability in Key Markets | -0.5% | Regional (e.g., Middle East, North Africa) | Short to Mid-term (2025-2027) |

| Capital Adequacy and Profitability Pressures | -0.4% | Global | Mid-term (2025-2029) |

Takaful Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Takaful market, offering detailed insights into its current size, historical performance, and future growth projections from 2025 to 2033. The report meticulously examines the key trends shaping the industry, identifies the primary drivers and restraints influencing market dynamics, and highlights emerging opportunities and persistent challenges. It offers a granular segmentation analysis across various dimensions, including product types, distribution channels, and applications, providing a holistic view of the market's structure and operational landscape. Furthermore, the report presents a thorough regional analysis, pinpointing high-growth areas and their specific market characteristics. A detailed profiling of leading market players, including their strategies and market positioning, is also incorporated to provide a competitive overview.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 38.5 Billion |

| Market Forecast in 2033 | USD 100.0 Billion |

| Growth Rate | 12.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Islamic Financial Services Group, Global Takaful Solutions, Takaful Worldwide Holdings, Albaraka Takaful Company, Gulf Takaful Group, Islamic Insurance Corporation, Premier Takaful Ventures, Horizon Takaful, Crescent Takaful Partners, Ethical Takaful Insurers, ShariaGuard Takaful, Integrity Takaful, Unity Takaful, Fidelity Takaful, Trustworthy Takaful, Evergreen Takaful, Lighthouse Takaful, Pinnacle Takaful, Secure Takaful Alliance, Zenith Takaful Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Takaful market is comprehensively segmented to provide a detailed understanding of its diverse components and their respective contributions to overall market dynamics. This segmentation facilitates targeted strategies for market players and offers granular insights into consumer preferences and industry trends. The primary segmentation is by type, distinguishing between Family Takaful, which covers aspects similar to life insurance, and General Takaful, encompassing non-life insurance categories such as motor, property, and health. A separate segment for Retakaful, which is the Sharia-compliant equivalent of reinsurance, is also crucial for understanding the market's risk-sharing capacity and stability.

Further segmentation explores distribution channels, including traditional methods like agents and brokers, bancassurance partnerships, and direct sales, alongside rapidly growing online channels that leverage digital platforms for broader reach and efficiency. Application-based segmentation differentiates between personal Takaful products, which cater to individual needs such as health, motor, and life protection, and commercial Takaful products, designed for businesses covering property, marine, engineering, and liability risks. This multi-faceted approach to segmentation provides a granular view of market opportunities and competitive landscapes across various product and distribution avenues, supporting informed strategic decisions for market participants.

- By Type:

- Family Takaful

- General Takaful

- Retakaful

- By Distribution Channel:

- Agents & Brokers

- Bancassurance

- Direct Sales

- Online Channels

- By Application:

- Personal (Health, Motor, Property, Life)

- Commercial (Property, Marine, Engineering, Liability, Aviation)

Regional Highlights

- Middle East & Africa (MEA): This region stands as the epicenter of the Takaful market, driven by a large Muslim population, strong governmental support for Islamic finance, and a well-developed regulatory framework. Countries like Saudi Arabia, UAE, and Malaysia are significant contributors, with increasing penetration rates and product diversification.

- Asia Pacific (APAC): Emerging as a high-growth region, APAC is witnessing rapid adoption of Takaful, particularly in Indonesia, Malaysia, Pakistan, and Bangladesh. The substantial Muslim population, combined with economic growth and digital literacy, fuels demand for both Family and General Takaful products, with significant potential for Microtakaful.

- Europe: While a smaller market, Europe shows promising growth due to expanding Muslim communities and a rising interest from non-Muslims in ethical financial products. The UK, France, and Germany are seeing increasing Takaful offerings, often focused on niche segments and community-based models.

- North America: The Takaful market in North America remains nascent but is gradually expanding, primarily catering to the Muslim diaspora. Growth is observed in urban centers with significant Muslim populations, focusing on niche Family and General Takaful products and ethical investment opportunities.

- Latin America: This region represents an emerging frontier for Takaful, with nascent interest in Islamic finance. Although currently a small market, the growing awareness of ethical finance and potential for strategic partnerships could unlock future growth opportunities, particularly in countries with increasing trade ties with Islamic nations.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Takaful Market.- Islamic Financial Services Group

- Global Takaful Solutions

- Takaful Worldwide Holdings

- Albaraka Takaful Company

- Gulf Takaful Group

- Islamic Insurance Corporation

- Premier Takaful Ventures

- Horizon Takaful

- Crescent Takaful Partners

- Ethical Takaful Insurers

- ShariaGuard Takaful

- Integrity Takaful

- Unity Takaful

- Fidelity Takaful

- Trustworthy Takaful

- Evergreen Takaful

- Lighthouse Takaful

- Pinnacle Takaful

- Secure Takaful Alliance

- Zenith Takaful Corporation

Frequently Asked Questions

Analyze common user questions about the Takaful market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Takaful?

Takaful is an Islamic insurance concept based on mutual cooperation, where participants contribute to a common pool to help each other in times of need. It operates on principles of mutual assistance, solidarity, and shared responsibility, adhering strictly to Sharia (Islamic law) by avoiding Riba (interest), Maysir (gambling), and Gharar (excessive uncertainty).

How does Takaful differ from conventional insurance?

Takaful differs fundamentally from conventional insurance in its underlying principles and operational model. While conventional insurance involves the transfer of risk for a premium, Takaful focuses on risk sharing and mutual assistance. Participants donate to a fund from which claims are paid, and any surplus is typically distributed among participants or retained for future use, unlike conventional models where profit often accrues solely to shareholders.

What are the benefits of Takaful?

Takaful offers several key benefits, including Sharia compliance, ensuring financial protection aligns with Islamic ethical values. It promotes fairness and transparency through its cooperative model, where surpluses can be shared with participants. Additionally, Takaful encourages community solidarity and responsible risk management, providing an ethical alternative for those seeking financial security.

What are the major types of Takaful products?

The Takaful market primarily offers two major types of products: Family Takaful, which provides long-term savings and protection analogous to life insurance, and General Takaful, which covers non-life risks such as motor, property, health, and marine insurance. There is also Retakaful, which serves as the Sharia-compliant equivalent of reinsurance, providing coverage for Takaful operators.

What is the future outlook for the Takaful market?

The future outlook for the Takaful market is highly positive, projected for robust growth driven by increasing global awareness of Islamic finance, supportive regulatory environments, and demographic shifts in Muslim-majority regions. Digitalization, product innovation, and expanding reach into underserved and ethical-conscious markets are expected to further accelerate its expansion and enhance its competitiveness against conventional insurance.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted