Suture Market

Suture Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701950 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Suture Market Size

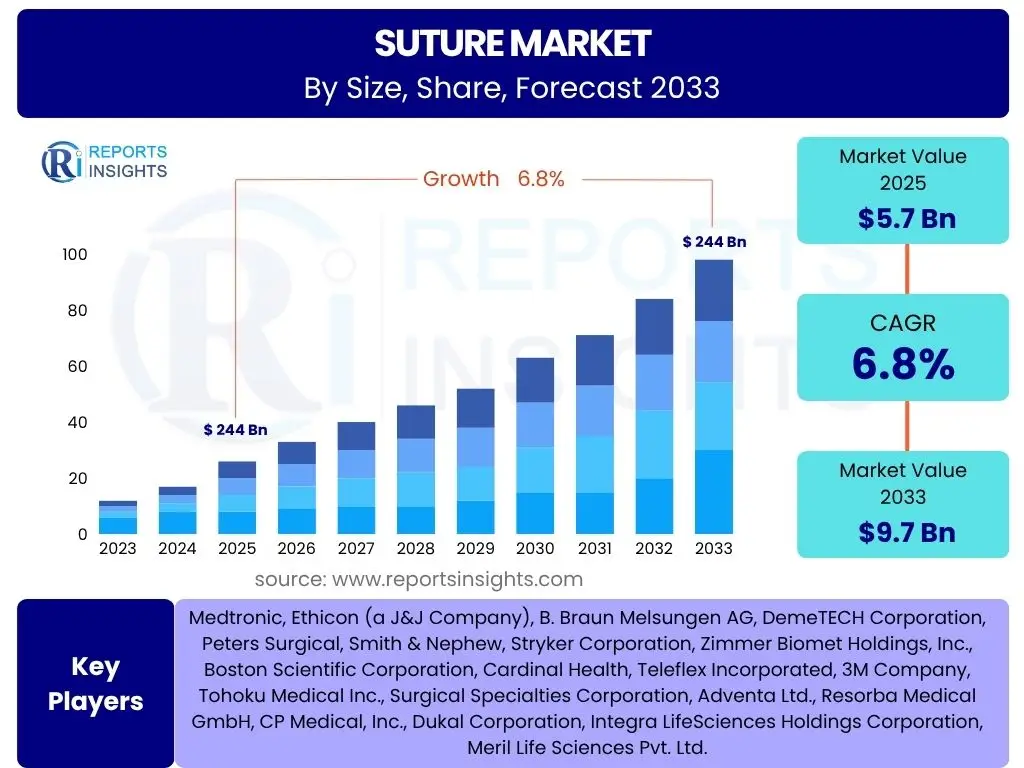

According to Reports Insights Consulting Pvt Ltd, The Suture Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. This robust growth trajectory is primarily driven by an increasing number of surgical procedures globally, advancements in surgical techniques, and a rising prevalence of chronic diseases requiring surgical intervention. The expanding healthcare infrastructure in emerging economies also contributes significantly to this positive outlook.

The market is estimated at USD 5.7 Billion in 2025 and is projected to reach USD 9.7 Billion by the end of the forecast period in 2033. This substantial increase reflects continuous innovation in suture materials and designs, including the development of absorbable, antimicrobial, and specialized sutures for various surgical applications. The demand for minimally invasive surgeries further propels the need for high-precision and technologically advanced wound closure devices, positioning sutures as a critical component of modern healthcare.

Key Suture Market Trends & Insights

Common user inquiries about suture market trends often revolve around material innovations, surgical technique evolution, and patient outcome improvements. Analysis reveals a significant shift towards advanced synthetic materials that offer enhanced strength, biodegradability, and reduced tissue reaction, alongside a growing interest in specialty sutures designed for specific surgical fields. The emphasis on faster patient recovery and reduced post-operative complications is paramount, influencing product development towards more biocompatible and effective solutions.

Furthermore, the integration of smart technologies, such as antimicrobial coatings and sensors, into suture design is gaining traction, addressing concerns about surgical site infections and enabling real-time monitoring of wound healing. The rise of robotic-assisted surgeries necessitates sutures that are easily manipulated by robotic arms, driving demand for specialized and pre-loaded suture kits. This confluence of material science, digital integration, and surgical methodology is shaping the future landscape of the suture market, prioritizing both efficacy and patient safety.

- Increased adoption of absorbable and synthetic sutures due to superior performance and reduced complications.

- Growing demand for antimicrobial sutures to mitigate surgical site infections (SSIs).

- Technological advancements in suture materials, including barbed, knotless, and smart sutures.

- Rising prevalence of minimally invasive surgical procedures driving demand for specialized sutures.

- Integration of robotics in surgery influencing suture design for enhanced precision and handling.

- Focus on improved wound healing outcomes and reduced scarring.

AI Impact Analysis on Suture

User questions regarding AI's impact on sutures frequently probe its role in surgical training, precision, and post-operative care. AI is poised to revolutionize the application and development of sutures by enhancing surgical planning and execution. Machine learning algorithms can analyze vast datasets of patient outcomes to recommend optimal suture types and techniques based on tissue characteristics, patient history, and surgical complexity, thereby improving surgical success rates and reducing variability.

In surgical training, AI-powered simulations and virtual reality platforms can provide realistic environments for surgeons to practice suturing techniques with immediate feedback, accelerating skill acquisition and refinement. Furthermore, AI could play a role in the design and development of next-generation sutures, optimizing material properties and geometric configurations for specific clinical needs through computational modeling. Post-operatively, AI-driven analytics could monitor wound healing through imaging, detecting early signs of complications like infection or dehiscence, potentially even with smart sutures embedded with sensors, leading to more timely interventions and better patient management.

- AI-driven optimization of suture selection based on patient-specific tissue properties and surgical requirements.

- Enhanced surgical training through AI-powered simulations for precise suturing practice.

- Development of intelligent sutures with integrated sensors for real-time wound healing monitoring and complication detection.

- Predictive analytics to forecast wound healing trajectories and identify patients at risk of surgical site infections.

- Robotic-assisted suturing enhanced by AI for greater precision, consistency, and reduced surgeon fatigue.

Key Takeaways Suture Market Size & Forecast

Analysis of common user questions about the suture market's size and forecast highlights a strong interest in understanding the primary drivers of growth, the resilience of the market against potential challenges, and key investment areas. The market demonstrates significant upward momentum, largely propelled by an aging global population, the increasing incidence of chronic diseases requiring surgical intervention, and continuous innovation in medical technology. This ensures a stable demand for sutures as an indispensable component of surgical procedures worldwide.

The forecast indicates a sustained expansion, underscoring opportunities for stakeholders in areas such as advanced biomaterials, antimicrobial applications, and specialty sutures for niche surgical fields. Despite potential restraints like pricing pressures and the emergence of alternative wound closure methods, the fundamental necessity of sutures in a vast array of surgical specialties ensures continued market vitality. Key strategic takeaways include prioritizing research and development in smart and bio-integrative sutures and expanding presence in high-growth emerging economies to capitalize on increasing healthcare expenditure and surgical volumes.

- The suture market exhibits robust growth, driven by increasing surgical volumes and an aging population.

- Technological advancements, particularly in absorbable and antimicrobial sutures, are key growth catalysts.

- Significant opportunities exist in emerging economies due to improving healthcare access and infrastructure.

- Minimally invasive surgical techniques are a major force shaping product development and market demand.

- Investment in research and development of innovative materials and smart sutures is crucial for competitive advantage.

Suture Market Drivers Analysis

The suture market's expansion is fundamentally propelled by a confluence of demographic shifts, disease prevalence, and ongoing advancements in medical science. An aging global population naturally leads to a higher incidence of age-related conditions, many of which necessitate surgical intervention, thereby driving a consistent demand for sutures. Simultaneously, the rising global burden of chronic diseases such as cardiovascular disorders, diabetes, and various forms of cancer contributes significantly to an increase in the total volume of surgical procedures performed annually.

Furthermore, continuous technological innovation in surgical techniques, including the widespread adoption of minimally invasive procedures, and the development of sophisticated suture materials with enhanced properties like absorbability, strength, and antimicrobial capabilities, are pivotal in expanding market opportunities. Improvements in healthcare infrastructure, particularly in developing regions, coupled with greater access to surgical care, also serve as significant accelerators for market growth. These factors collectively create a robust environment for sustained market progression.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Surgical Procedures | +1.2% | Global | Long-term (2025-2033) |

| Aging Population and Chronic Disease Prevalence | +0.8% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Technological Advancements in Suture Materials | +0.9% | North America, Europe, Asia Pacific | Mid-to-Long-term (2025-2033) |

| Growing Adoption of Minimally Invasive Surgeries | +0.7% | Global | Mid-term (2025-2030) |

| Improvements in Healthcare Infrastructure and Access | +0.6% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

Suture Market Restraints Analysis

Despite significant growth drivers, the suture market faces several challenges that could impede its expansion. One prominent restraint is the relatively high cost associated with advanced and specialized sutures, particularly those incorporating novel materials or antimicrobial properties. This can limit their adoption in cost-sensitive healthcare environments, especially in developing economies where budgetary constraints are more pronounced, potentially favoring traditional, less expensive alternatives.

Furthermore, the increasing preference for alternative wound closure methods, such as surgical staplers, tissue adhesives, sealants, and wound closure strips, poses a competitive threat. While sutures remain the gold standard for many procedures, these alternatives offer advantages like faster application times and reduced patient discomfort in certain contexts, potentially eroding the market share for traditional sutures. Lastly, stringent regulatory approval processes, particularly in highly regulated markets, can delay the introduction of innovative products, thereby impacting market dynamism and manufacturers' return on investment.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Sutures | -0.6% | Developing Economies, Public Healthcare Systems | Long-term (2025-2033) |

| Availability of Alternative Wound Closure Methods | -0.5% | Global | Mid-to-Long-term (2025-2033) |

| Stringent Regulatory Approval Processes | -0.4% | North America, Europe | Short-to-Mid-term (2025-2028) |

| Risk of Surgical Site Infections (SSIs) with Conventional Sutures | -0.3% | Global | Ongoing |

Suture Market Opportunities Analysis

The suture market presents several compelling opportunities for growth and innovation. Expansion into emerging economies offers a significant avenue, as these regions are experiencing rapid development in healthcare infrastructure, increasing disposable incomes, and a growing demand for advanced medical treatments. Markets in Asia Pacific, Latin America, and the Middle East and Africa are particularly poised for growth due to their large populations and improving access to surgical services, providing untapped potential for suture manufacturers.

Moreover, the continuous research and development of novel materials and smart sutures represent a substantial opportunity. This includes biodegradable materials that offer optimal wound support before safely dissolving, and intelligent sutures with integrated sensors for monitoring wound healing, detecting infections, or even releasing therapeutic agents. Such innovations not only address existing clinical needs but also open entirely new therapeutic possibilities, driving future market demand. The ongoing trend towards personalized medicine and patient-specific surgical solutions also creates a niche for highly specialized and customized suture products.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Economies | +1.0% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

| Development of Antimicrobial and Smart Sutures | +0.9% | North America, Europe | Mid-to-Long-term (2025-2033) |

| Increased Adoption of Robotic and Minimally Invasive Surgeries | +0.8% | Global | Mid-term (2025-2030) |

| Focus on Biodegradable and Bio-integrative Materials | +0.7% | North America, Europe | Long-term (2025-2033) |

Suture Market Challenges Impact Analysis

The suture market encounters several formidable challenges that necessitate strategic responses from manufacturers and healthcare providers. A persistent concern is the risk of post-operative complications, particularly surgical site infections (SSIs), which despite advances in surgical hygiene, remain a significant challenge. These complications not only impact patient outcomes and recovery times but also incur substantial additional healthcare costs, potentially leading to increased scrutiny of wound closure methods and a drive towards more expensive, specialized solutions.

Furthermore, the global supply chain for medical devices, including sutures, remains vulnerable to disruptions stemming from geopolitical tensions, natural disasters, or pandemics, which can lead to material shortages, production delays, and increased costs. Intense price competition, especially for commoditized suture products, pressures manufacturers to optimize production efficiencies and innovate continually to maintain profitability. These challenges underscore the need for resilient supply chain management, continuous product improvement, and strategic pricing models to sustain market competitiveness.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Post-operative Complications and Infections (SSIs) | -0.5% | Global | Ongoing |

| Supply Chain Volatility and Raw Material Costs | -0.4% | Global | Short-to-Mid-term (2025-2027) |

| Intense Price Competition and Commoditization | -0.3% | Global | Ongoing |

| Lack of Skilled Healthcare Professionals for Advanced Techniques | -0.2% | Developing Economies | Long-term (2025-2033) |

Suture Market - Updated Report Scope

This updated report provides an in-depth, data-driven analysis of the global suture market, encompassing a comprehensive evaluation of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key geographical regions. It offers crucial insights into the competitive landscape, profiling leading market players and their strategic initiatives. The report aims to equip stakeholders with actionable intelligence for informed decision-making, strategic planning, and identifying lucrative investment avenues within the evolving healthcare sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.7 Billion |

| Market Forecast in 2033 | USD 9.7 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic, Ethicon (a J&J Company), B. Braun Melsungen AG, DemeTECH Corporation, Peters Surgical, Smith & Nephew, Stryker Corporation, Zimmer Biomet Holdings, Inc., Boston Scientific Corporation, Cardinal Health, Teleflex Incorporated, 3M Company, Tohoku Medical Inc., Surgical Specialties Corporation, Adventa Ltd., Resorba Medical GmbH, CP Medical, Inc., Dukal Corporation, Integra LifeSciences Holdings Corporation, Meril Life Sciences Pvt. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global suture market is meticulously segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for a detailed analysis of market dynamics across different product types, materials, surgical applications, and end-user settings. By dissecting the market into these core categories, stakeholders can identify specific growth niches, evaluate competitive landscapes, and tailor their strategies to target particular segments with high growth potential, ensuring a comprehensive market outlook.

Understanding these segments is crucial for strategic planning, product development, and market entry decisions. The variations in demand, technological requirements, and regulatory considerations across each segment necessitate a tailored approach. This granular analysis facilitates the identification of high-growth areas, such as synthetic absorbable sutures for minimally invasive procedures or specialized sutures for cardiovascular applications, enabling companies to focus their resources effectively and capitalize on emerging trends.

- By Type:

- Absorbable Sutures (Natural Absorbable, Synthetic Absorbable)

- Non-Absorbable Sutures (Natural Non-Absorbable, Synthetic Non-Absorbable)

- By Raw Material:

- Natural (Catgut, Silk)

- Synthetic (Polyglycolic Acid (PGA), Polyglactin 910 (PGLA), Polydioxanone (PDO), Polypropylene, Nylon, Polyester, PVDF, Others)

- By Application:

- Cardiovascular Surgery

- General Surgery

- Gynecological Surgery

- Orthopedic Surgery

- Ophthalmic Surgery

- Neurological Surgery

- Plastic Surgery

- Other Surgical Applications

- By End-Use:

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

Regional Highlights

Geographically, the suture market is analyzed across key regions: North America, Europe, Asia Pacific, Latin America, and Middle East and Africa (MEA). Each region presents unique market dynamics influenced by healthcare expenditure, prevalence of chronic diseases, technological adoption, and regulatory frameworks. North America and Europe typically represent mature markets characterized by advanced healthcare infrastructure, high adoption rates of innovative products, and significant research and development investments. These regions are early adopters of new surgical techniques and premium suture products.

The Asia Pacific region is anticipated to exhibit the fastest growth over the forecast period. This acceleration is driven by improving economic conditions, increasing healthcare spending, a large patient pool, and the development of robust medical tourism sectors. Countries like China, India, and Japan are investing heavily in upgrading their healthcare facilities and expanding access to surgical care, leading to a surge in demand for various types of sutures. Latin America and MEA are emerging markets that offer substantial growth opportunities, fueled by increasing awareness of advanced medical treatments, improving healthcare access, and a growing number of surgical procedures performed annually.

- North America: Dominates the market due to advanced healthcare infrastructure, high prevalence of chronic diseases, and early adoption of innovative products.

- Europe: Exhibits significant growth driven by an aging population, increasing surgical procedures, and strong emphasis on patient safety and quality.

- Asia Pacific (APAC): Fastest-growing region, propelled by rising healthcare expenditure, improving medical facilities, and a large patient base in countries like China and India.

- Latin America: Shows promising growth with increasing investments in healthcare, expanding access to surgical care, and a rising prevalence of lifestyle diseases.

- Middle East and Africa (MEA): Emerging market with growth attributed to developing healthcare infrastructure, increasing medical tourism, and a growing burden of chronic conditions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Suture Market.- Medtronic

- Ethicon (a J&J Company)

- B. Braun Melsungen AG

- DemeTECH Corporation

- Peters Surgical

- Smith & Nephew

- Stryker Corporation

- Zimmer Biomet Holdings, Inc.

- Boston Scientific Corporation

- Cardinal Health

- Teleflex Incorporated

- 3M Company

- Tohoku Medical Inc.

- Surgical Specialties Corporation

- Adventa Ltd.

- Resorba Medical GmbH

- CP Medical, Inc.

- Dukal Corporation

- Integra LifeSciences Holdings Corporation

- Meril Life Sciences Pvt. Ltd.

Frequently Asked Questions

Analyze common user questions about the Suture market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are sutures and how are they used in surgery?

Sutures are sterile threads used by surgeons to close wounds, approximate tissues, and ligate blood vessels during surgical procedures. They play a critical role in promoting wound healing, maintaining tissue integrity, and preventing infection by securely holding incised edges together until the body's natural healing process takes over. They are applied using surgical needles, and chosen based on tissue type, strength requirements, and desired healing outcomes.

What are the main types of sutures available in the market?

The main types of sutures are categorized primarily by their absorbability and material. Absorbable sutures, such as catgut, polyglactin (Vicryl), and polydioxanone (PDS), are designed to break down and be absorbed by the body over time. Non-absorbable sutures, including silk, nylon, polypropylene, and polyester, retain their tensile strength indefinitely and are either left permanently in the body or removed after wound healing.

How is technology impacting the suture market?

Technological advancements are significantly transforming the suture market through the development of innovative materials like antimicrobial-coated sutures to prevent infection, barbed and knotless sutures for faster closure, and smart sutures embedded with sensors for real-time wound monitoring. Robotic-assisted surgery is also driving demand for specialized sutures that are easier to manipulate with robotic instruments, enhancing precision and efficiency in complex procedures.

What factors are driving the growth of the suture market?

Key drivers include an increase in the global volume of surgical procedures due to the aging population and rising prevalence of chronic diseases. Advancements in surgical techniques, such as the increasing adoption of minimally invasive surgeries, and continuous innovation in suture materials (e.g., absorbable and antimicrobial options) also significantly contribute to market expansion. Improved healthcare infrastructure and access in emerging economies further bolster demand.

What are the key challenges faced by the suture market?

The suture market faces challenges such as the high cost of advanced and specialized sutures, which can limit adoption in budget-constrained settings. Competition from alternative wound closure methods (e.g., staplers, adhesives) and stringent regulatory approval processes for new products also pose hurdles. Additionally, the persistent risk of surgical site infections and potential supply chain disruptions are ongoing concerns for manufacturers and healthcare providers.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted