Telecom Equipment Market

Telecom Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705562 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

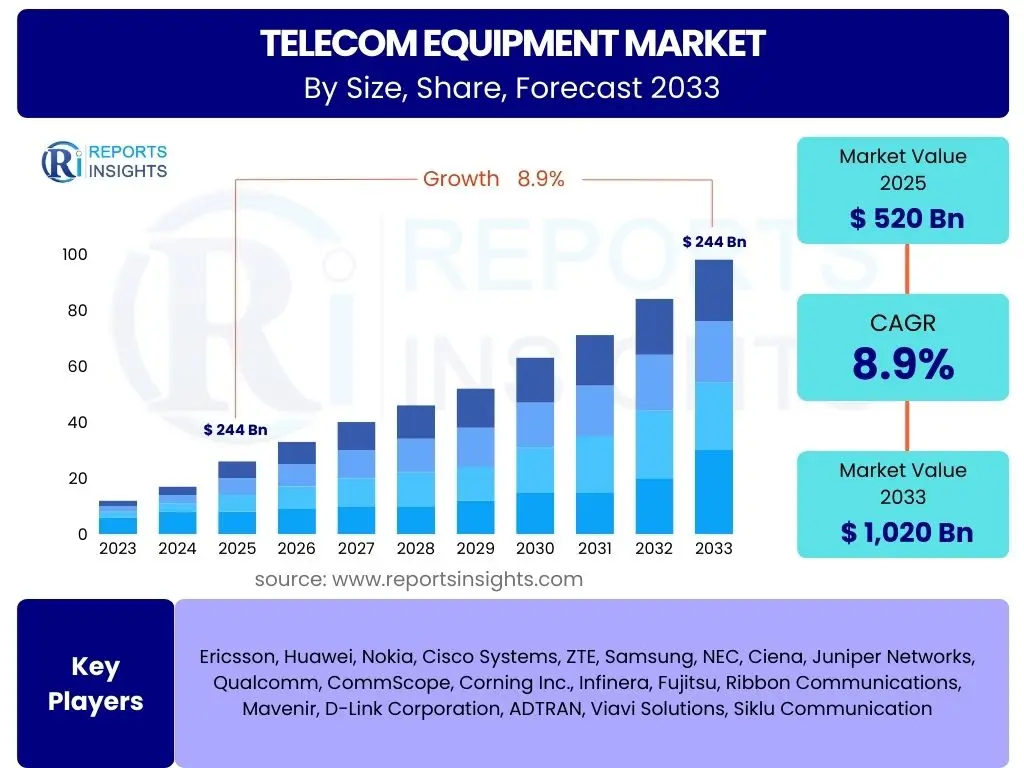

Telecom Equipment Market Size

According to Reports Insights Consulting Pvt Ltd, The Telecom Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 520 billion in 2025 and is projected to reach USD 1,020 billion by the end of the forecast period in 2033.

Key Telecom Equipment Market Trends & Insights

User queries regarding the telecom equipment market trends frequently highlight the rapid evolution of network technologies and the increasing demand for high-speed, reliable connectivity. A primary theme revolves around the global rollout of 5G infrastructure, which is not only expanding mobile broadband capabilities but also enabling new applications like IoT and enterprise private networks. Furthermore, there is significant interest in how network architectures are transforming, with a shift towards virtualization, cloud-native solutions, and open interfaces to enhance flexibility and reduce operational costs.

Another area of focus for users is the emergence of non-traditional communication methods, such as Low Earth Orbit (LEO) satellites, and their potential to extend connectivity to underserved areas, thereby expanding the addressable market for telecom equipment. The push for energy efficiency and sustainable network operations, often termed "green networking," also resonates with user concerns about environmental impact and operational expenditure. These trends collectively underscore a market in flux, driven by technological innovation and a persistent need for ubiquitous and efficient communication infrastructure.

- Accelerated 5G Network Rollouts and Monetization Strategies

- Proliferation of Internet of Things (IoT) and Machine-to-Machine (M2M) Communications

- Increased Adoption of Cloud-Native Network Functions and Virtualization (NFV/SDN)

- Emergence of Open RAN (Radio Access Network) Architectures for Vendor Diversity

- Expansion of Edge Computing Capabilities for Low Latency Applications

- Growing Investment in Fiber Optic Infrastructure and Fixed Wireless Access (FWA)

- Development of Non-Terrestrial Networks (NTN) including LEO Satellite Constellations

- Focus on Network Automation and AI-driven Operations (AIOps)

- Emphasis on Green Networking and Energy Efficiency in Network Design

- Rising Demand for Private 5G Networks in Enterprise and Industrial Sectors

AI Impact Analysis on Telecom Equipment

User inquiries concerning Artificial Intelligence's impact on telecom equipment consistently point to expectations of enhanced network performance, efficiency, and security. A significant theme is AI's role in automating complex network operations, enabling predictive maintenance, and optimizing resource allocation, which can drastically reduce human intervention and operational expenditures. Users are keen to understand how AI facilitates intelligent network slicing, dynamic traffic management, and proactive fault detection, transforming reactive network management into a highly predictive and adaptive system.

Furthermore, there is a strong interest in AI's contribution to cybersecurity within telecom networks, where it can identify anomalous behaviors and respond to threats in real-time. The integration of AI capabilities directly into network equipment, such as base stations and core network components, is also a focal point, as it allows for distributed intelligence and faster decision-making at the edge. Ultimately, the market anticipates AI as a critical enabler for scaling 5G networks, supporting the massive influx of IoT devices, and delivering highly personalized services with guaranteed quality of experience.

- Network Optimization and Performance Enhancement: AI algorithms predict traffic patterns, optimize routing, and manage network resources dynamically, leading to improved bandwidth utilization and reduced latency.

- Automated Network Operations (AIOps): AI automates routine tasks, performs root cause analysis for network issues, and enables self-healing networks, significantly reducing operational costs and human error.

- Enhanced Cybersecurity and Threat Detection: AI analyzes vast amounts of network data to detect anomalies, identify sophisticated cyber threats, and provide real-time responses, bolstering network security.

- Predictive Maintenance: AI models analyze equipment performance data to predict potential failures, allowing for proactive maintenance and minimizing network downtime.

- Intelligent Network Slicing: AI enables dynamic creation and management of network slices for diverse applications, ensuring Quality of Service (QoS) for various use cases in 5G networks.

- Edge AI Integration: AI capabilities are increasingly embedded into edge devices and equipment, enabling faster processing and decision-making closer to the data source.

- Service Personalization and Customer Experience Management: AI assists in analyzing user behavior and network conditions to deliver personalized services and optimize customer experience.

- Energy Efficiency: AI-driven systems can optimize power consumption of network equipment by intelligently managing device states and resource allocation based on demand.

Key Takeaways Telecom Equipment Market Size & Forecast

User queries regarding key takeaways from the telecom equipment market size and forecast consistently emphasize the robust growth trajectory, primarily fueled by the global rollout of advanced network technologies. A central insight is the significant investment in 5G infrastructure, which is acting as a primary catalyst for market expansion, alongside the burgeoning ecosystem of IoT devices that demand higher network capacity and lower latency. The market's future is intrinsically linked to digital transformation initiatives across various industries, creating demand for sophisticated and reliable communication solutions.

Another crucial takeaway is the increasing complexity of network architectures, pushing for innovative solutions like virtualization, open RAN, and edge computing to manage growth and improve efficiency. While growth is strong, the market also faces challenges such as high capital expenditure, geopolitical influences on supply chains, and the need for skilled talent. However, the overarching theme is one of transformative potential, where telecom equipment providers are foundational to realizing a globally connected and digitally empowered future, marked by continuous innovation and strategic investments.

- The Telecom Equipment Market is poised for substantial growth, driven primarily by ongoing global 5G deployments and rising demand for ubiquitous connectivity.

- Significant investments in advanced network infrastructure, including fiber optic and fixed wireless access, are key growth contributors.

- Digital transformation across industries is fueling demand for specialized telecom solutions, including private networks and edge computing equipment.

- Technological advancements such as Open RAN, network virtualization, and AI integration are reshaping equipment design and deployment strategies.

- Emerging markets in Asia Pacific and Africa represent significant opportunities for infrastructure expansion and new subscriber growth.

- Supply chain resilience and geopolitical considerations remain critical factors influencing market dynamics and vendor strategies.

- The market is shifting towards more intelligent, automated, and energy-efficient network solutions to reduce operational costs and environmental impact.

- Security concerns and the need for robust network resilience are increasingly influencing equipment procurement decisions.

Telecom Equipment Market Drivers Analysis

The global telecom equipment market is primarily propelled by the insatiable demand for high-speed internet and the expansive rollout of 5G networks. This fundamental shift towards faster and more reliable connectivity for both consumers and enterprises necessitates substantial investments in new infrastructure and upgrades to existing networks. The proliferation of connected devices, ranging from smartphones to IoT sensors, further stresses current network capacities, driving the need for more sophisticated and efficient telecom equipment to handle the massive data traffic and diverse application requirements.

Additionally, the ongoing digital transformation across various industries, including manufacturing, healthcare, and transportation, is creating a strong impetus for advanced telecom solutions. Enterprises are adopting private 5G networks, edge computing, and cloud-native architectures to enhance operational efficiency, enable real-time analytics, and support mission-critical applications. This enterprise-driven demand, coupled with government initiatives to bridge the digital divide and foster smart city development, collectively acts as a powerful catalyst for the sustained growth of the telecom equipment market, pushing innovation in network capacity, latency, and reliability.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global 5G Rollout and Expansion | +2.5% | Global, particularly North America, Asia Pacific, Europe | 2025-2033 (Long-term) |

| Proliferation of IoT Devices and Applications | +1.8% | Global, strong in developed economies and smart cities | 2025-2033 (Long-term) |

| Increasing Demand for High-Speed Connectivity | +1.5% | Global, especially emerging markets and densely populated areas | 2025-2030 (Mid-term) |

| Cloud Computing and Network Virtualization Adoption | +1.2% | Global, high relevance in enterprise and hyperscale deployments | 2025-2033 (Long-term) |

| Government Initiatives for Digital Infrastructure | +1.0% | Asia Pacific (India, China), Europe (EU Digital Agenda), Africa | 2025-2030 (Mid-term) |

| Growth of Enterprise Private Networks | +0.9% | North America, Europe, Asia Pacific (Industrial sectors) | 2025-2033 (Long-term) |

Telecom Equipment Market Restraints Analysis

Despite robust growth drivers, the telecom equipment market faces several significant restraints that could temper its expansion. One primary concern is the substantial capital expenditure required for network upgrades and new infrastructure deployments, particularly for 5G, which often strains the financial resources of telecom operators. This high upfront cost can lead to slower adoption rates in certain regions or deferment of investments, directly impacting equipment sales. Additionally, the complex and often fragmented regulatory landscape across different countries, coupled with evolving spectrum allocation policies, can introduce delays and uncertainties in network planning and deployment, hindering market fluidity.

Geopolitical tensions and trade disputes also pose a notable restraint, leading to supply chain disruptions, increased component costs, and restrictions on technology transfer. This environment can force operators to diversify their vendor base, potentially leading to less optimized solutions or higher integration complexities. Furthermore, the inherent cybersecurity risks associated with increasingly interconnected and software-defined networks demand continuous investment in security features and compliance, adding to the overall cost burden. These multifaceted restraints necessitate careful strategic planning by market participants to navigate potential slowdowns and maintain growth momentum.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure Requirements | -1.5% | Global, particularly developing markets | 2025-2030 (Mid-term) |

| Supply Chain Disruptions and Component Shortages | -1.2% | Global, especially affecting hardware manufacturers | 2025-2027 (Short-term) |

| Geopolitical Tensions and Trade Barriers | -1.0% | Global, significant in US-China relations, Europe | 2025-2033 (Long-term) |

| Stringent Regulatory Frameworks and Spectrum Costs | -0.8% | Europe, India, certain Latin American countries | 2025-2033 (Long-term) |

| Cybersecurity Concerns and Data Privacy Regulations | -0.7% | Global, strong in North America, Europe | 2025-2033 (Long-term) |

Telecom Equipment Market Opportunities Analysis

The telecom equipment market is ripe with opportunities driven by technological advancements and evolving connectivity needs. The push towards Open RAN architectures presents a significant opportunity for new vendors to enter the market and for operators to diversify their supply chains, fostering innovation and reducing vendor lock-in. This shift also encourages the development of more specialized and interoperable equipment components. Furthermore, the burgeoning demand for private 5G networks in industrial, enterprise, and public safety sectors creates a distinct niche for tailor-made equipment and solutions, moving beyond traditional consumer-centric deployments.

Another area of immense potential lies in the expansion of connectivity to underserved and remote areas through satellite-based broadband and fixed wireless access technologies, which require specific equipment designed for challenging environments. The increasing focus on edge computing also opens new avenues for equipment manufacturers to develop compact, high-performance network infrastructure closer to the data sources, supporting low-latency applications like autonomous vehicles and augmented reality. Lastly, the industry's drive towards sustainable and energy-efficient network solutions offers a unique opportunity for innovation in green telecom equipment, aligning with global environmental objectives and reducing operational costs for operators.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Adoption of Open RAN and Disaggregated Networks | +1.5% | Global, particularly North America, Europe, Japan | 2026-2033 (Mid- to Long-term) |

| Growth of Private 5G Networks for Enterprises | +1.3% | North America, Europe, Asia Pacific (Industrial, Logistics) | 2025-2033 (Long-term) |

| Expansion of Broadband to Underserved Areas (FWA, Satellite) | +1.0% | Emerging markets, rural North America, Africa, Latin America | 2025-2033 (Long-term) |

| Development of Edge Computing Infrastructure | +0.9% | Global, driven by IoT and real-time application needs | 2026-2033 (Mid- to Long-term) |

| Increasing Focus on Green Telecom and Energy Efficiency | +0.7% | Global, strong in Europe, North America | 2025-2033 (Long-term) |

Telecom Equipment Market Challenges Impact Analysis

The telecom equipment market faces a complex array of challenges that can significantly impact its growth trajectory and operational efficiency. One prominent challenge is the rapid pace of technological obsolescence, where continuous innovation demands substantial research and development investments to stay competitive. This also creates pressure on operators to frequently upgrade equipment, leading to high capital expenditure and potential issues with integrating new technologies with legacy systems. Another critical challenge is the inherent interoperability issues between diverse vendor equipment, particularly with the rise of multi-vendor strategies and Open RAN, which necessitates complex integration and testing efforts.

Furthermore, the industry grapples with a global shortage of skilled professionals, especially those proficient in emerging technologies like 5G, AI, and cloud-native networking. This talent gap can slow down deployment, maintenance, and optimization of advanced networks. Energy consumption of network equipment is also a growing concern, as operators strive to reduce their carbon footprint and operational costs, pushing for more energy-efficient designs. Navigating these challenges requires strategic foresight, collaborative industry efforts, and a continuous focus on innovation to ensure the sustainable evolution of the telecom equipment market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence | -1.3% | Global, impacting all technology segments | 2025-2033 (Long-term) |

| Interoperability and Integration Complexities | -1.0% | Global, especially with multi-vendor deployments | 2025-2030 (Mid-term) |

| Shortage of Skilled Workforce | -0.9% | Global, significant in developed markets | 2025-2033 (Long-term) |

| High Energy Consumption of Network Infrastructure | -0.7% | Global, increasing scrutiny in Europe, North America | 2025-2033 (Long-term) |

| Intense Competition and Price Pressure | -0.6% | Global, particularly in mature markets | 2025-2030 (Mid-term) |

Telecom Equipment Market - Updated Report Scope

This report provides an in-depth analysis of the global Telecom Equipment Market, segmenting it by product type, technology, application, and component. It offers a comprehensive overview of market dynamics, including key drivers, restraints, opportunities, and challenges influencing market growth from 2025 to 2033. The scope extends to a detailed competitive landscape, profiling key players and their strategic initiatives, while also analyzing regional market performance across major geographical areas to provide a holistic market view.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 520 billion |

| Market Forecast in 2033 | USD 1,020 billion |

| Growth Rate | 8.9% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Ericsson, Huawei, Nokia, Cisco Systems, ZTE, Samsung, NEC, Ciena, Juniper Networks, Qualcomm, CommScope, Corning Inc., Infinera, Fujitsu, Ribbon Communications, Mavenir, D-Link Corporation, ADTRAN, Viavi Solutions, Siklu Communication |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Telecom Equipment Market is broadly segmented based on product type, technology, application, and component, reflecting the diverse landscape of network infrastructure and services. Product type segmentation encompasses the essential hardware and systems that form the backbone of telecommunications, from Radio Access Networks (RAN) that connect end-user devices to the core network that manages traffic and services, as well as transmission equipment for data transport. This granular view allows for a detailed understanding of demand for specific network elements.

Technology segmentation highlights the evolution of network standards and capabilities, with a significant focus on 5G and LTE, which are driving current market investments, alongside emerging satellite and fiber optic technologies that are expanding connectivity options. Application segmentation addresses the varying needs of different end-user sectors, from individual residential consumers requiring basic internet access to complex industrial and public sector applications demanding high reliability and specialized network features. Finally, component segmentation distinguishes between the physical hardware, the software that enables network intelligence and management, and the services essential for deployment, maintenance, and optimization, providing a holistic view of the market's value chain.

- By Product Type:

- Radio Access Network (RAN)

- Core Network

- Transmission Equipment (Optical, Microwave)

- Mobile Backhaul

- Fixed-Line Access Equipment

- Routers and Switches

- Base Stations

- Antennas

- Customer Premises Equipment (CPE)

- By Technology:

- 5G

- LTE

- 4G/3G

- Fiber Optic

- Satellite

- IoT Connectivity

- By Application:

- Residential

- Commercial (Enterprise, Industrial)

- Public Sector

- Others (Defense, Research)

- By Component:

- Hardware

- Software

- Services

Regional Highlights

- North America: This region is characterized by early and aggressive 5G deployments, significant investments in fiber optic networks, and a strong focus on private networks for enterprises. The presence of major technology innovators and a high adoption rate of advanced digital services contribute to its leading position in telecom equipment expenditure. The United States and Canada are key drivers, with continuous upgrades to support cloud computing, IoT, and high-bandwidth applications.

- Europe: Driven by digitalization initiatives, smart city projects, and the need for universal broadband access, Europe is a robust market for telecom equipment. While 5G rollout is progressive, the region also emphasizes Open RAN adoption and the development of energy-efficient network infrastructure. Regulatory frameworks play a significant role in shaping market dynamics, promoting competition and sustainable growth.

- Asia Pacific (APAC): This region is poised for the highest growth, fueled by rapid urbanization, massive subscriber bases in countries like China and India, and increasing disposable incomes. Extensive 5G deployments, particularly in China, South Korea, and Japan, coupled with government-backed digital infrastructure projects in emerging economies, make APAC a dominant force in the global telecom equipment market. The region also sees substantial investment in fiber and IoT.

- Latin America: This market is undergoing significant infrastructure development, with increasing efforts to expand broadband access and upgrade existing networks to 4G and 5G. Governments and telecom operators are investing to bridge the digital divide and support economic growth, creating demand for base stations, fiber optic cables, and mobile backhaul solutions. Brazil and Mexico are leading the regional investments.

- Middle East and Africa (MEA): Characterized by increasing mobile penetration, government-led smart nation initiatives, and diverse connectivity needs, MEA represents a burgeoning market. Investments in 5G and fiber are accelerating, particularly in Gulf Cooperation Council (GCC) countries and parts of Africa, driven by the demand for improved digital services, enterprise connectivity, and mobile-first strategies.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Telecom Equipment Market.- Ericsson

- Huawei

- Nokia

- Cisco Systems

- ZTE

- Samsung

- NEC

- Ciena

- Juniper Networks

- Qualcomm

- CommScope

- Corning Inc.

- Infinera

- Fujitsu

- Ribbon Communications

- Mavenir

- D-Link Corporation

- ADTRAN

- Viavi Solutions

- Siklu Communication

Frequently Asked Questions

What is the projected growth rate of the Telecom Equipment Market?

The Telecom Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033, reaching an estimated USD 1,020 billion by 2033.

What are the primary drivers for the Telecom Equipment Market's growth?

The primary drivers include the global rollout of 5G networks, the rapid proliferation of IoT devices, increasing demand for high-speed connectivity, and the widespread adoption of cloud computing and network virtualization technologies across various industries.

How is Artificial Intelligence (AI) impacting the Telecom Equipment Market?

AI is significantly impacting the market by enabling advanced network optimization, automating operations (AIOps), enhancing cybersecurity, facilitating predictive maintenance, and supporting intelligent network slicing for improved efficiency and service delivery.

What are the key challenges faced by the Telecom Equipment Market?

Key challenges include the rapid pace of technological obsolescence, complex interoperability issues between diverse vendor equipment, a shortage of skilled professionals, high energy consumption of network infrastructure, and intense market competition with associated price pressures.

Which regions are leading in the adoption and investment in telecom equipment?

North America and Asia Pacific are leading regions in telecom equipment adoption and investment, driven by extensive 5G deployments, strong digital transformation initiatives, and growing subscriber bases. Europe is also a significant market, with Latin America and MEA showing substantial growth potential.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted