Rubidium Standard Market

Rubidium Standard Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702136 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Rubidium Standard Market Size

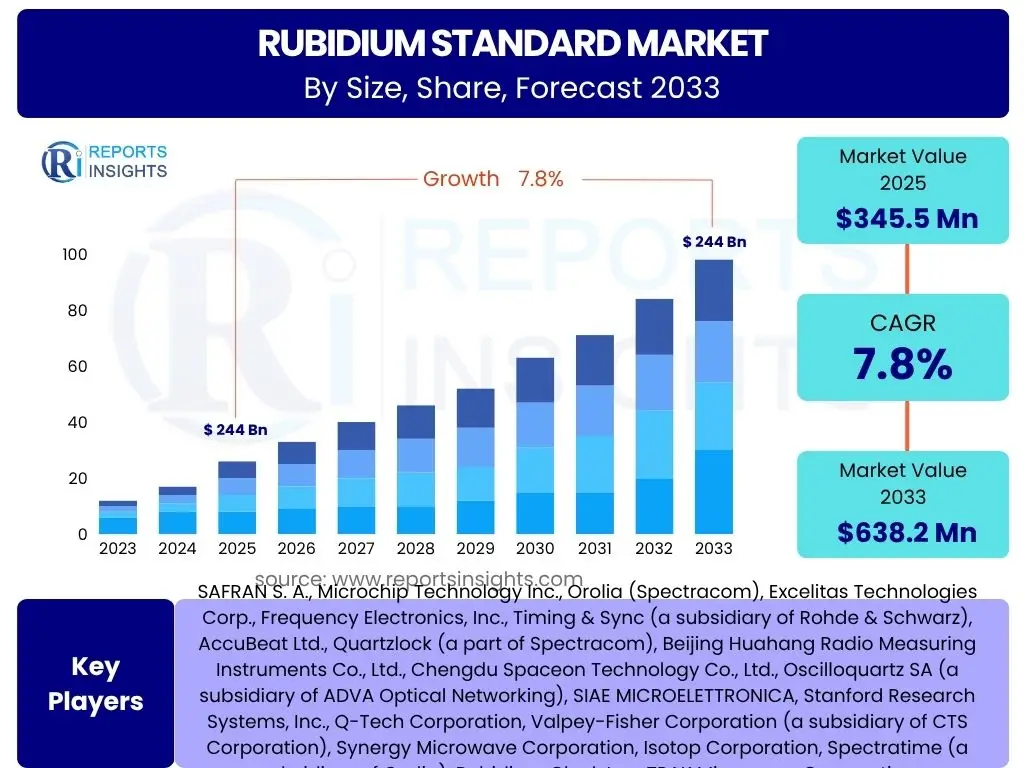

According to Reports Insights Consulting Pvt Ltd, The Rubidium Standard Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 345.5 million in 2025 and is projected to reach USD 638.2 million by the end of the forecast period in 2033.

Key Rubidium Standard Market Trends & Insights

The Rubidium Standard Market is currently experiencing a transformative phase driven by advancements in timing technology and the escalating demand for highly accurate synchronization across diverse industries. Key trends highlight a shift towards miniaturized and more robust rubidium oscillators, enabling their integration into a wider array of portable and space-constrained applications. Furthermore, there is an increasing emphasis on enhanced long-term stability and reduced power consumption, critical factors for deploying these precision devices in remote or energy-sensitive environments. The convergence of high-precision timing with emerging technologies like 5G, satellite navigation, and quantum computing is also a dominant trend, underscoring the indispensable role of rubidium standards in next-generation infrastructure.

Another significant insight into the market involves the growing adoption of chip-scale atomic clocks (CSACs), which leverage rubidium technology to offer unprecedented levels of precision in compact form factors. This trend is democratizing access to atomic clock accuracy for applications previously unable to accommodate larger, more power-intensive solutions. Concurrently, the market is witnessing increased investment in research and development aimed at improving manufacturing processes and reducing the overall cost of rubidium standards, making them more accessible for broader commercial and industrial deployment. The demand for resilient positioning, navigation, and timing (PNT) solutions, especially in scenarios where GNSS signals might be compromised, further solidifies the market's trajectory towards robust and independent timing sources.

- Miniaturization and form factor reduction for broader application integration.

- Enhanced long-term stability and reduced power consumption for extended deployment.

- Growing adoption of Chip-Scale Atomic Clocks (CSACs) for compact precision.

- Increasing integration into 5G telecommunications infrastructure for network synchronization.

- Rising demand from aerospace, defense, and space sectors for robust PNT solutions.

- Advancements in manufacturing processes leading to cost efficiency and improved reliability.

- Development of hybrid timing solutions combining rubidium with other technologies.

- Focus on cybersecurity and resilience in timing systems for critical infrastructure.

AI Impact Analysis on Rubidium Standard

Artificial intelligence is poised to significantly influence the Rubidium Standard Market, primarily through optimization, predictive maintenance, and the enablement of new applications requiring ultra-precise synchronized timing. Users are keenly interested in how AI can enhance the performance and reliability of rubidium standards, for instance, by leveraging machine learning algorithms to analyze environmental data and predict potential drift or failure, thereby enabling proactive calibration or maintenance. This predictive capability is crucial for mission-critical applications where uninterrupted, accurate timing is paramount, reducing operational downtime and increasing system longevity. Furthermore, AI can optimize the integration and synchronization of rubidium standards within complex networks, ensuring seamless operation and efficient resource utilization.

Beyond operational enhancements, AI's role in driving demand for rubidium standards is also a key area of interest. Emerging AI-driven technologies, such as advanced autonomous systems, quantum computing, and high-frequency trading platforms, necessitate extremely precise and stable timing references for optimal performance. AI applications often rely on vast amounts of time-stamped data and require synchronized operations across distributed systems, making rubidium standards an indispensable component. The ability of AI to process and derive insights from sensor data also extends to monitoring the performance of timing devices, feeding back into their design and operational parameters. Consequently, AI acts as both an enabler for more sophisticated rubidium standard applications and a consumer of the high-accuracy timing data these devices provide, fostering a symbiotic relationship.

- Predictive maintenance and anomaly detection using AI for rubidium oscillator performance.

- Optimization of synchronization protocols in complex networks through AI algorithms.

- Enabling high-precision timing for AI-driven autonomous vehicles and robotics.

- Supporting advanced AI research in quantum computing requiring atomic-level precision.

- Facilitating ultra-low-latency communication in AI-powered financial trading systems.

- Data analysis by AI to refine and improve the long-term stability of rubidium standards.

- AI-driven smart grid applications requiring synchronized power distribution enabled by rubidium.

Key Takeaways Rubidium Standard Market Size & Forecast

The Rubidium Standard Market is on a robust growth trajectory, driven by the escalating global demand for highly precise and stable timing solutions across an expanding range of industries. A critical takeaway is the projected substantial growth from USD 345.5 million in 2025 to USD 638.2 million by 2033, reflecting a compound annual growth rate of 7.8%. This growth is not merely incremental but indicative of fundamental shifts in technological infrastructure worldwide, where traditional timing methods are proving insufficient. The market's resilience is underpinned by its indispensable role in critical applications such as 5G network deployment, satellite navigation systems, and national defense, which demand extreme accuracy and reliability that only rubidium standards can consistently provide.

Another significant takeaway is the increasing penetration of rubidium standards into new and emerging sectors, including industrial IoT, smart energy grids, and quantum technologies. This diversification of applications, coupled with ongoing advancements in miniaturization and power efficiency, suggests a broadening market base beyond traditional high-end uses. The emphasis on independent and resilient timing sources, particularly in light of vulnerabilities in satellite-based timing, further solidifies the market's long-term outlook. Investors and industry stakeholders should recognize the enduring strategic importance of rubidium standards as foundational components for future technological evolution, making it a compelling market for sustained investment and innovation.

- Significant market expansion projected from USD 345.5 million (2025) to USD 638.2 million (2033).

- CAGR of 7.8% highlights strong, consistent growth driven by foundational technological needs.

- Indispensable role in critical infrastructure: 5G, GNSS, defense, and data centers.

- Diversification into emerging sectors such as IoT, smart grids, and quantum computing.

- Increasing focus on miniaturization and power efficiency for broader market adoption.

- Growing demand for resilient, independent timing solutions due to PNT vulnerabilities.

- Continued innovation in performance, cost-effectiveness, and integration capabilities.

Rubidium Standard Market Drivers Analysis

The Rubidium Standard Market is propelled by several potent drivers, with the global rollout of 5G networks standing as a paramount factor. 5G infrastructure demands extremely precise and stable timing synchronization to facilitate high-speed data transmission, manage complex massive MIMO arrays, and enable seamless network slicing and edge computing. Rubidium standards offer the superior frequency stability and low phase noise that are essential for these demanding applications, significantly outperforming conventional timing solutions. As telecommunication operators continue to expand 5G coverage and capabilities worldwide, particularly in densely populated urban areas and for industrial automation, the fundamental need for high-accuracy timing sources at base stations, data centers, and backhaul links escalates, directly increasing the demand for rubidium standards.

Another significant driver is the modernization of defense and aerospace systems. Military operations, secure communications, radar systems, and satellite navigation rely heavily on extremely accurate and robust timing for precision targeting, data encryption, and resilient positioning, navigation, and timing (PNT). Rubidium standards provide the necessary stability and reliability in harsh environments where GPS/GNSS signals may be denied or spoofed. Furthermore, the expansion of the satellite industry, including the proliferation of low Earth orbit (LEO) constellations for global connectivity and Earth observation, necessitates highly precise onboard timing for satellite synchronization and data integrity. This sustained demand from defense and space agencies worldwide continues to fuel innovation and adoption in the rubidium standard market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| 5G Network Deployment & Expansion | +2.1% | Global, particularly North America, Asia Pacific, Europe | 2025-2033 |

| Modernization of Defense & Aerospace Systems | +1.8% | North America, Europe, Asia Pacific (China, India) | 2025-2033 |

| Growth in Data Centers & Cloud Computing | +1.5% | Global, high concentration in North America, Europe, Asia Pacific | 2025-2033 |

| Expansion of Satellite Navigation (GNSS/GPS) Systems | +1.2% | Global, key regions: US, Europe, China, Russia, India | 2025-2033 |

| Increasing Demand for Resilient PNT Solutions | +1.0% | Global, emphasis on critical infrastructure regions | 2025-2033 |

Rubidium Standard Market Restraints Analysis

Despite the robust growth drivers, the Rubidium Standard Market faces several significant restraints that could temper its expansion. One of the primary barriers to wider adoption is the relatively high initial cost associated with rubidium standards compared to other timing solutions like Oven Controlled Crystal Oscillators (OCXOs) or GPS-disciplined oscillators. While rubidium standards offer superior performance, the upfront investment can be prohibitive for budget-sensitive applications or smaller-scale deployments. This cost factor extends not only to the purchase of the units but also to the integration, calibration, and maintenance complexities, which can add to the total cost of ownership. Overcoming this economic barrier requires continuous innovation in manufacturing processes and material science to drive down production costs and increase market accessibility.

Another notable restraint is the inherent complexity in the design, manufacturing, and integration of rubidium standards. These devices require specialized expertise and precision engineering, limiting the number of manufacturers capable of producing them at scale. Furthermore, the sensitivity of rubidium standards to environmental factors such as temperature fluctuations, vibrations, and magnetic fields can pose integration challenges in certain applications. While modern designs have made significant strides in ruggedization, these sensitivities can still add complexity and cost to system design. Additionally, the increasing reliance on global supply chains for specialized components and raw materials introduces vulnerabilities, as geopolitical instability or unforeseen events can disrupt production and increase lead times, impacting market supply and pricing stability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost & Total Cost of Ownership | -1.5% | Global, particularly emerging economies | 2025-2033 |

| Technical Complexity & Integration Challenges | -1.2% | Global, impact on small and medium enterprises (SMEs) | 2025-2033 |

| Competition from Alternative Timing Solutions | -0.8% | Global, especially in less critical applications | 2025-2030 |

| Supply Chain Vulnerabilities for Raw Materials | -0.7% | Global, specific impact on manufacturers and end-users | 2025-2033 |

Rubidium Standard Market Opportunities Analysis

Significant opportunities exist within the Rubidium Standard Market, primarily driven by the ongoing technological paradigm shift towards highly precise timing in various emerging applications. The burgeoning field of quantum technologies, including quantum computing, quantum sensing, and quantum communications, presents a substantial opportunity. These advanced applications often require atomic-level precision and stability in timing, making rubidium standards, particularly chip-scale atomic clocks (CSACs), indispensable. As research and development in quantum technologies accelerate globally, the demand for highly stable and compact atomic timing references is expected to grow exponentially, opening new, high-value market segments for rubidium standard manufacturers.

Furthermore, the increasing focus on industrial Internet of Things (IIoT) and smart grid infrastructure offers another compelling growth avenue. IIoT applications, ranging from precision robotics to predictive maintenance in manufacturing, demand synchronized timing for data acquisition, control, and network efficiency. Smart grids require precise timing for fault detection, energy distribution optimization, and grid resilience. Rubidium standards can provide the foundational timing accuracy needed for these distributed, interconnected systems, enhancing operational efficiency and reliability. The development of more miniaturized, ruggedized, and power-efficient rubidium oscillators will be key to unlocking these opportunities, enabling their deployment in diverse and often harsh industrial environments. Moreover, the demand for resilient and independent PNT solutions, particularly in light of vulnerabilities in satellite navigation, creates opportunities for rubidium standards to serve as primary or backup timing references in critical national infrastructure.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Quantum Technologies | +2.0% | North America, Europe, Asia Pacific (China, Japan) | 2027-2033 |

| Expansion in Industrial IoT & Smart Grids | +1.7% | Global, focus on industrialized nations | 2025-2033 |

| Demand for Resilient & Independent PNT | +1.5% | Global, particularly defense and critical infrastructure | 2025-2033 |

| Development of Miniaturized & Low-Power Solutions | +1.3% | Global, enabling wider commercial applications | 2025-2033 |

| Growth in Financial Sector (High-Frequency Trading) | +0.8% | Major financial hubs: North America, Europe, Asia | 2025-2030 |

Rubidium Standard Market Challenges Impact Analysis

The Rubidium Standard Market faces several critical challenges that stakeholders must address to sustain robust growth. One significant hurdle is the continuous requirement for miniaturization without compromising performance. As applications like portable military devices, unmanned aerial vehicles (UAVs), and compact communication systems increasingly demand atomic clock precision, manufacturers are pressured to reduce the size and weight of rubidium standards significantly. Achieving this while maintaining or enhancing frequency stability, power efficiency, and environmental robustness presents considerable engineering and material science challenges. Balancing these often conflicting design parameters requires substantial R&D investment and innovative manufacturing techniques, which can be resource-intensive for market players.

Another key challenge is reducing the manufacturing cost of rubidium standards to enable their wider commercial adoption beyond high-end, niche applications. While the performance benefits are clear, the high cost of production remains a barrier for many potential industrial and consumer-grade uses. This involves optimizing component sourcing, streamlining assembly processes, and potentially exploring new materials or fabrication methods that can scale efficiently. Furthermore, market education and awareness are crucial. Despite their superior accuracy, many potential end-users in emerging sectors may not fully understand the distinct advantages of rubidium standards over less precise alternatives, necessitating targeted outreach and demonstration of value proposition. Finally, geopolitical risks and supply chain disruptions, particularly concerning specialized components and rare earth elements used in rubidium standards, pose a persistent challenge, threatening production continuity and pricing stability for manufacturers globally.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization vs. Performance Trade-offs | -1.0% | Global, affects R&D and product development | 2025-2033 |

| High Manufacturing Costs & Accessibility | -0.9% | Global, impacts market penetration | 2025-2033 |

| Market Education & Awareness for New Applications | -0.6% | Emerging markets & non-traditional sectors | 2025-2030 |

| Managing Supply Chain & Geopolitical Risks | -0.5% | Global, especially for key component sourcing | 2025-2033 |

Rubidium Standard Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Rubidium Standard Market, encompassing historical data from 2019 to 2023, a base year of 2024, and a forecast period extending from 2025 to 2033. The report meticulously details market size estimations, growth projections, and key trends influencing market dynamics. It offers a thorough segmentation analysis across various product types, applications, and end-use industries, alongside a detailed regional outlook. Furthermore, the study includes an exhaustive competitive landscape analysis, profiling leading companies and their strategic initiatives, and provides an impact assessment of key market drivers, restraints, opportunities, and challenges, including the transformative influence of AI.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 345.5 Million |

| Market Forecast in 2033 | USD 638.2 Million |

| Growth Rate | 7.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | SAFRAN S. A., Microchip Technology Inc., Orolia (Spectracom), Excelitas Technologies Corp., Frequency Electronics, Inc., Timing & Sync (a subsidiary of Rohde & Schwarz), AccuBeat Ltd., Quartzlock (a part of Spectracom), Beijing Huahang Radio Measuring Instruments Co., Ltd., Chengdu Spaceon Technology Co., Ltd., Oscilloquartz SA (a subsidiary of ADVA Optical Networking), SIAE MICROELETTRONICA, Stanford Research Systems, Inc., Q-Tech Corporation, Valpey-Fisher Corporation (a subsidiary of CTS Corporation), Synergy Microwave Corporation, Isotop Corporation, Spectratime (a subsidiary of Orolia), Rubidium Clock Inc., TRAK Microwave Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Rubidium Standard Market is comprehensively segmented to provide a granular view of its dynamics and growth prospects across various dimensions. This segmentation allows for a detailed understanding of where demand is originating and how different product types and applications are contributing to overall market growth. The market is primarily segmented by type, application, and end-use industry, each category revealing distinct trends and market opportunities. Analyzing these segments helps stakeholders identify high-growth areas and tailor their strategies to specific market needs and technological requirements, ensuring that products and services are aligned with the precise demands of each niche.

The segmentation by type typically includes distinct product categories such as standalone frequency standards, integrated clock modules, and dedicated atomic frequency standards, each designed for varying levels of precision and integration complexity. Application-based segmentation provides insights into the primary industries leveraging rubidium standards, ranging from established sectors like telecommunications and aerospace & defense to emerging areas such as financial services and smart grids. Furthermore, the end-use industry segmentation categorizes adoption across government, commercial, industrial, and research institutions, reflecting the diverse operational environments and regulatory frameworks that influence market penetration. This multi-faceted segmentation ensures a holistic understanding of the market landscape and future growth areas.

- By Type:

- Frequency Standard: Standalone rubidium oscillators offering high precision timing output.

- Clock Module: Integrated modules combining rubidium oscillator with control electronics for easier system integration.

- Atomic Frequency Standard: High-precision devices designed for primary reference or metrology applications.

- By Application:

- Telecommunications: Critical for 5G network synchronization, base stations, and data centers.

- Aerospace & Defense: Used in satellite navigation, secure communications, radar, and PNT systems.

- Metrology: For calibration, precision measurement, and laboratory reference.

- Test & Measurement: Employed in electronic testing, frequency counting, and signal analysis.

- Research & Scientific: Essential for quantum computing, fundamental physics research, and precise experiments.

- Financial Services: For high-frequency trading platforms and synchronized transaction logging.

- Data Centers: For precise timing of distributed computing, storage, and networking.

- Power & Energy: In smart grids for synchronized power distribution and fault detection.

- Others: Including industrial automation, broadcasting, and critical infrastructure.

- By End-Use Industry:

- Government: Defense, space agencies, national laboratories.

- Commercial: Telecommunications, financial services, data centers.

- Industrial: Manufacturing, energy, oil & gas.

- Research Institutions: Universities, public and private research facilities.

Regional Highlights

- North America: This region is a dominant force in the Rubidium Standard Market, driven by robust investment in defense and aerospace, extensive 5G network rollouts, and the presence of leading technology companies. The United States, in particular, leads in research and development, contributing significantly to advancements in chip-scale atomic clocks (CSACs) and their integration into portable military and commercial applications. The strong emphasis on resilient positioning, navigation, and timing (PNT) solutions for critical infrastructure further stimulates demand.

- Europe: Europe represents a mature market with significant contributions from telecommunications infrastructure modernization, ongoing space programs (e.g., Galileo), and strong industrial automation sectors. Countries like Germany, France, and the UK are key players, investing in precision timing for smart grids, secure communications, and metrology applications. Regulatory frameworks promoting network synchronization and resilience also contribute to market growth.

- Asia Pacific (APAC): The APAC region is projected to exhibit the fastest growth, primarily due to rapid 5G deployment in countries like China, India, Japan, and South Korea. Massive infrastructure projects, increasing defense spending, and burgeoning demand from data centers and high-frequency trading platforms are key drivers. Government initiatives to develop indigenous technologies and strengthen critical infrastructure further fuel the adoption of rubidium standards.

- Latin America: This region is an emerging market for rubidium standards, with growth driven by expanding telecommunications networks, including 5G rollouts in major economies like Brazil and Mexico. Investment in critical infrastructure and natural resource management also contributes to the gradual adoption of precise timing solutions. The market here is expected to grow steadily as technological adoption progresses.

- Middle East and Africa (MEA): The MEA region is witnessing increasing adoption dueated to strategic investments in telecommunications infrastructure, defense modernization, and smart city initiatives. Countries in the Gulf Cooperation Council (GCC) are particularly active in diversifying their economies and enhancing technological capabilities, leading to greater demand for advanced timing solutions. Challenges remain in terms of infrastructure development and market awareness, but growth is anticipated as regional economies mature.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Rubidium Standard Market.- SAFRAN S. A.

- Microchip Technology Inc.

- Orolia (Spectracom)

- Excelitas Technologies Corp.

- Frequency Electronics, Inc.

- Timing & Sync (a subsidiary of Rohde & Schwarz)

- AccuBeat Ltd.

- Quartzlock (a part of Spectracom)

- Beijing Huahang Radio Measuring Instruments Co., Ltd.

- Chengdu Spaceon Technology Co., Ltd.

- Oscilloquartz SA (a subsidiary of ADVA Optical Networking)

- SIAE MICROELETTRONICA

- Stanford Research Systems, Inc.

- Q-Tech Corporation

- Valpey-Fisher Corporation (a subsidiary of CTS Corporation)

- Synergy Microwave Corporation

- Isotop Corporation

- Spectratime (a subsidiary of Orolia)

- Rubidium Clock Inc.

- TRAK Microwave Corporation

Frequently Asked Questions

What is a Rubidium Standard and its primary function?

A rubidium standard is a highly stable atomic clock that generates precise frequency and timing signals by locking to a specific atomic transition of rubidium atoms. Its primary function is to serve as an ultra-accurate and stable time and frequency reference, essential for applications requiring highly synchronized operations and precise measurements.

Why are Rubidium Standards important for 5G networks?

Rubidium standards are crucial for 5G networks because 5G technology demands extremely precise timing synchronization to enable high data rates, low latency, and efficient resource allocation. Their superior frequency stability ensures reliable operation of base stations, massive MIMO systems, and edge computing nodes, preventing data loss and optimizing network performance.

What are the key advantages of Rubidium Standards over other timing solutions?

Rubidium standards offer significantly higher frequency stability and accuracy over longer periods compared to crystal oscillators (like OCXOs), and they provide independence from external signals, unlike GPS-disciplined oscillators. Their compact size and relatively low power consumption, especially for chip-scale atomic clocks (CSACs), make them ideal for many critical applications.

Which industries are the major consumers of Rubidium Standards?

Major industries consuming rubidium standards include telecommunications (for 5G and network synchronization), aerospace and defense (for PNT, secure communications, radar), metrology and test & measurement, research and scientific fields (quantum computing), and the financial sector (high-frequency trading).

What is the future outlook for the Rubidium Standard Market?

The future outlook for the Rubidium Standard Market is strong, driven by increasing global demand for precise timing in 5G, satellite navigation, and emerging quantum technologies. Miniaturization, improved power efficiency, and ongoing cost reductions are expected to broaden market adoption into new industrial and commercial applications, ensuring continued growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted