Rhodium Market

Rhodium Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700136 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

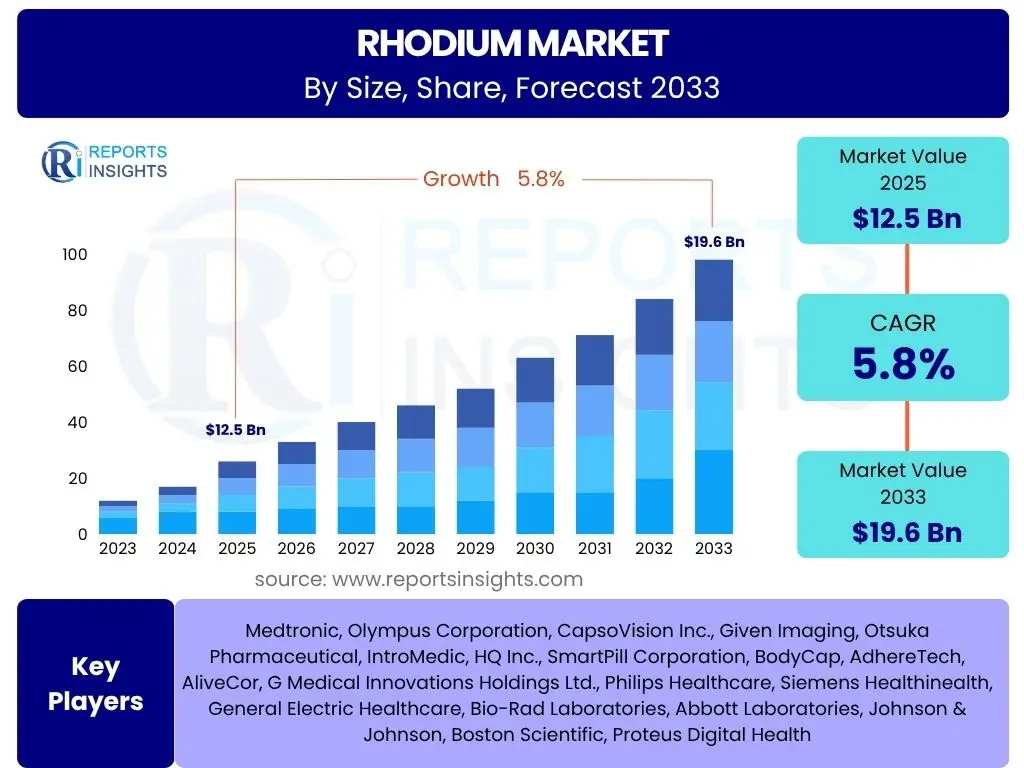

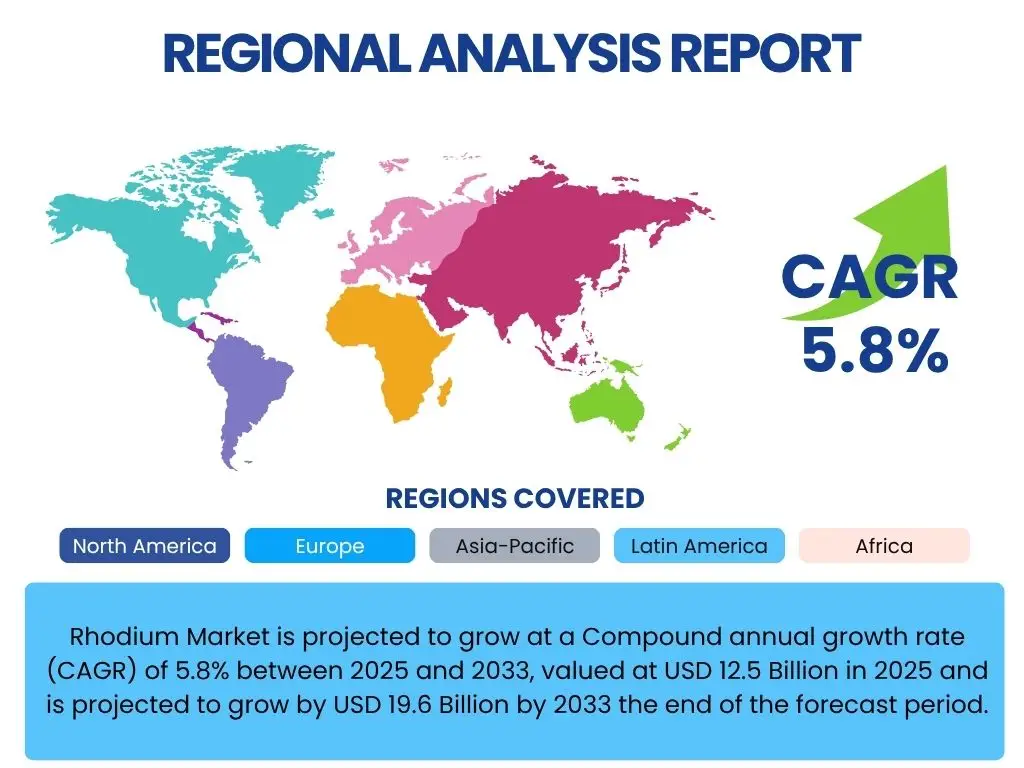

Rhodium Market is projected to grow at a Compound annual growth rate (CAGR) of 5.8% between 2025 and 2033, current valued at USD 12.5 Billion in 2025 and is projected to grow by USD 19.6 Billion by 2033 the end of the forecast period.

Key Rhodium Market Trends & Insights

The Rhodium market is shaped by a confluence of macroeconomic and industry-specific trends that dictate its trajectory. Foremost among these is the enduring demand from the automotive sector, driven by stringent global emission regulations mandating catalytic converters for pollutant reduction. Furthermore, the market observes increasing interest in advanced industrial applications, particularly in chemical processing and glass manufacturing, where rhodium's unique catalytic properties are indispensable. The market also experiences significant volatility due to its concentrated supply base and relatively inelastic demand, making price fluctuations a recurring theme. The growing emphasis on the circular economy and sustainable practices is driving innovations in rhodium recycling and recovery, aimed at mitigating supply risks and environmental impact. Lastly, ongoing geopolitical developments in key producing regions significantly influence supply chain stability and market sentiment, adding another layer of complexity to price dynamics.

- Increasing demand from the automotive catalyst sector due to stricter emission standards.

- Growing applications in the chemical industry for catalytic processes.

- Heightened focus on recycling and recovery of rhodium to ensure sustainable supply.

- Price volatility influenced by supply concentration and geopolitical factors.

- Technological advancements in industrial applications expanding its utility.

AI Impact Analysis on Rhodium

Artificial Intelligence (AI) is poised to exert a transformative influence across various facets of the Rhodium market, from mining and refining to demand forecasting and price prediction. In the upstream segment, AI-driven analytics can optimize mining operations by identifying high-yield ore bodies, improving extraction efficiency, and enhancing safety protocols, thereby potentially increasing supply stability. For refining processes, AI can facilitate the development of more efficient and environmentally friendly recovery methods, reducing operational costs and material waste. Furthermore, AI's predictive capabilities are invaluable for market analysis, offering more accurate forecasts of rhodium demand based on complex economic indicators, automotive production trends, and regulatory changes. This enhanced foresight enables stakeholders to make more informed strategic decisions regarding inventory management, procurement, and investment, contributing to a more resilient and responsive rhodium supply chain.

- Optimized mining and extraction processes through AI-driven geological analysis.

- Enhanced efficiency in rhodium recycling and refining via intelligent process control.

- Improved price prediction and demand forecasting using AI algorithms.

- Supply chain optimization and risk management through predictive analytics.

- Facilitation of new material discovery and catalyst design with AI simulations.

Key Takeaways Rhodium Market Size & Forecast

- The Rhodium market is projected to achieve a market value of USD 19.6 Billion by 2033.

- The market is anticipated to expand at a Compound Annual Growth Rate (CAGR) of 5.8% from 2025 to 2033.

- Automotive catalytic converters remain the dominant application driving market growth.

- Industrial catalytic applications, particularly in chemical and glass industries, contribute significantly to demand.

- Market expansion is notably influenced by evolving global emission regulations and industrial output.

- The inherent volatility of rhodium prices necessitates strategic market monitoring and risk assessment.

- Growth in recycling initiatives is expected to bolster supply security and market stability over the forecast period.

Rhodium Market Drivers Analysis

The Rhodium market's growth trajectory is primarily propelled by a combination of environmental regulations, industrial innovation, and macroeconomic factors. The automotive sector stands as the single largest consumer of rhodium, owing to its indispensable role in catalytic converters. Increasingly stringent global emission standards, particularly in emerging economies and established markets, necessitate higher loadings of platinum group metals (PGMs), including rhodium, in these devices to meet ambitious air quality targets. This regulatory push directly translates into sustained and growing demand for rhodium.

Beyond automotive, rhodium's exceptional catalytic properties make it vital in various industrial processes. Its use in chemical catalysts, for instance, is crucial for the efficient production of nitric acid, acetic acid, and other organic compounds. The expanding global chemical industry, driven by population growth and industrialization, fuels a steady demand for rhodium. Similarly, its application in the glass industry, particularly for fiberglass and flat panel display production, contributes significantly to its market momentum. Furthermore, investor interest in precious metals as a hedge against inflation and economic instability can also indirectly bolster demand and market liquidity for rhodium, given its status as a rare and valuable commodity.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Global Emission Regulations | +1.8% | Global, particularly Asia Pacific (China, India) and Europe | Short to Medium Term (2025-2028) |

| Increasing Automotive Production | +1.5% | Asia Pacific, North America, Europe | Medium Term (2026-2030) |

| Growth in Chemical and Glass Industries | +1.2% | Global, strong in Asia Pacific and Europe | Medium to Long Term (2027-2033) |

| Rising Investment Demand for Precious Metals | +0.8% | Global, particularly North America and Europe | Short to Medium Term (2025-2029) |

| Technological Advancements in Catalyst Design | +0.5% | Global, with R&D centers in North America, Europe, Japan | Long Term (2028-2033) |

Rhodium Market Restraints Analysis

Despite its critical applications, the Rhodium market faces several significant restraints that could temper its growth. Foremost among these is the extreme price volatility that has characterized the market in recent years. Rhodium is a notoriously illiquid market with a highly concentrated supply base, predominantly from South Africa, making it susceptible to sudden and dramatic price swings based on supply disruptions, shifts in demand, or speculative trading. Such volatility poses considerable challenges for industrial consumers in terms of budgeting and consistent procurement, potentially leading them to seek out alternative materials or optimize their usage.

Another key restraint is the potential for substitution, particularly in applications where rhodium's high cost becomes prohibitive. While rhodium possesses unique catalytic properties that are difficult to replicate entirely, ongoing research into palladium-only catalysts or other PGM combinations for automotive applications could reduce the reliance on rhodium. Similarly, technological shifts, such as the accelerating adoption of electric vehicles (EVs), represent a long-term threat to rhodium demand in catalytic converters, although this impact is expected to materialize more significantly towards the latter half of the forecast period as EV penetration increases. Furthermore, the high initial capital investment required for rhodium mining and refining operations, coupled with the environmental and social concerns associated with mining, can deter new market entrants and limit supply expansion, indirectly contributing to market tightness and price instability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Price Volatility | -1.5% | Global, affecting all end-use sectors | Short to Medium Term (2025-2029) |

| Supply Concentration Risk (South Africa) | -1.2% | Global, with direct impact on all consuming regions | Medium to Long Term (2026-2033) |

| Potential for Substitution in Catalytic Applications | -0.9% | North America, Europe, Japan (R&D focus) | Long Term (2029-2033) |

| Accelerated Electric Vehicle (EV) Adoption | -0.7% | Global, particularly China, Europe, North America | Long Term (2030-2033) |

| Environmental & Regulatory Hurdles for Mining | -0.5% | South Africa, Zimbabwe, Russia | Medium to Long Term (2027-2033) |

Rhodium Market Opportunities Analysis

Despite the inherent volatility and supply constraints, the Rhodium market presents several compelling opportunities for growth and innovation. One significant avenue lies in the burgeoning hydrogen economy, particularly the development and scaling of fuel cell technologies. Rhodium, or alloys containing rhodium, show promise in certain types of fuel cell catalysts, and as the world transitions towards cleaner energy sources, demand from this sector could emerge as a substantial new growth driver. Furthermore, advancements in chemical synthesis and industrial catalysis continually uncover new applications where rhodium's unique properties offer superior efficiency or performance over other materials. This ongoing innovation widens the scope of its utility beyond traditional automotive and chemical sectors.

Another crucial opportunity stems from the increasing global focus on sustainability and resource circularity. Enhancing rhodium recycling and recovery rates from end-of-life products, particularly catalytic converters, represents a significant opportunity to secure supply, reduce reliance on primary mining, and mitigate environmental impact. Innovations in recycling technologies, coupled with favorable policies for material recovery, can unlock substantial secondary supply. Additionally, the growing industrialization and rising environmental awareness in emerging economies present dual opportunities: on one hand, increased industrial output drives demand for chemical and glass applications; on the other, stricter environmental regulations in these regions will mandate greater use of automotive catalysts, boosting rhodium consumption. Strategic investments in these regions, coupled with R&D in advanced applications, can capitalize on these evolving market dynamics.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Hydrogen Economy & Fuel Cells | +1.0% | North America, Europe, Japan, China | Long Term (2030-2033) |

| Advancements in Recycling & Urban Mining | +0.9% | Europe, North America, Japan | Medium to Long Term (2027-2033) |

| New Applications in Advanced Materials & Electronics | +0.7% | Global, R&D in developed economies | Long Term (2028-2033) |

| Increasing Industrialization in Emerging Economies | +0.6% | Asia Pacific (Southeast Asia, India), Latin America | Medium Term (2026-2030) |

| Development of More Efficient Chemical Processes | +0.5% | Global, with significant chemical industry presence | Medium to Long Term (2027-2033) |

Rhodium Market Challenges Impact Analysis

The Rhodium market is confronted with a distinct set of challenges that demand strategic foresight and adaptive responses from industry participants. A primary concern is the extreme concentration of its primary supply, with South Africa accounting for a substantial majority of global production. This high dependency on a single geographical region makes the market highly vulnerable to geopolitical instability, labor disputes, energy crises, or mining policy changes within that country. Any significant disruption to South African mining operations can send immediate shockwaves through the global supply chain, leading to severe shortages and exacerbating price volatility, which in turn impacts downstream industries reliant on rhodium.

Another significant challenge is the ongoing pressure from the transition to electric vehicles (EVs). While the full impact is a long-term prospect, the accelerating pace of EV adoption, driven by global climate goals and technological advancements, implies a gradual but eventual decline in demand for internal combustion engine (ICE) vehicles and, consequently, for catalytic converters. This structural shift necessitates that rhodium producers and refiners explore diversification strategies and invest in research for alternative applications. Furthermore, the high capital intensity and complex metallurgical processes involved in rhodium extraction and refining create high barriers to entry, limiting the number of new producers and maintaining the oligopolistic nature of the market. Navigating the delicate balance between ensuring a stable supply for current demands and adapting to future market paradigms will be critical for the sustainable growth of the rhodium market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Concentrated Primary Supply (South Africa) | -1.3% | Global, impacting all major consuming regions | Short to Medium Term (2025-2029) |

| Impact of Electric Vehicle (EV) Transition | -1.0% | Global, with early impact in developed economies | Long Term (2030-2033) |

| Market Illiquidity and Speculative Trading | -0.8% | Global financial markets | Short to Medium Term (2025-2028) |

| High Production Costs and Capital Intensity | -0.6% | Primary producing regions (South Africa, Russia) | Medium to Long Term (2026-2033) |

| Compliance with Evolving Environmental Regulations | -0.4% | Global, affecting mining and refining operations | Ongoing, Medium Term (2025-2029) |

Rhodium Market - Updated Report Scope

This comprehensive market research report on the Rhodium market provides a detailed analysis of its current state and future growth trajectory. It offers in-depth insights into market size, segmentation, regional dynamics, key trends, drivers, restraints, opportunities, and challenges. The report aims to equip stakeholders with critical intelligence for strategic decision-making in this highly specialized and volatile market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 19.6 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Sibanye-Stillwater, Anglo American Platinum (Amplats), Impala Platinum Holdings (Implats), Northam Platinum, Glencore, Johnson Matthey, BASF, Heraeus Precious Metals, Umicore, Tanaka Kikinzoku Kogyo, Platinum Group Metals Ltd., Royal Bafokeng Platinum, Norilsk Nickel, Rio Tinto, Vale, African Rainbow Minerals (ARM), Eastern Platinum Limited, Sedibelo Platinum Mines, Aurubis AG, Evonik Industries AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Rhodium market is comprehensively segmented to provide a granular view of its diverse applications and forms, alongside a detailed regional breakdown. This segmentation allows for precise analysis of demand drivers and market dynamics across various end-use industries and geographical landscapes. Understanding these distinct segments is crucial for stakeholders seeking to identify niche opportunities, assess competitive landscapes, and formulate targeted growth strategies within this specialized commodity market.

- By Application: This segment categorizes rhodium consumption based on its end-use industries.

- Automotive Catalysts: The dominant application, driven by global emission regulations for internal combustion engine vehicles.

- Chemical Catalysts: Essential for industrial processes producing nitric acid, acetic acid, and in hydroformylation reactions.

- Glass Manufacturing: Utilized in the production of high-quality glass, including fiberglass and flat panel displays.

- Electrical & Electronics: Employed in electrical contacts and specialized components due to its corrosion resistance.

- Jewelry: A minor but stable application, often used for plating to enhance durability and luster.

- Other Industrial Applications: Includes thermocouples, medical instruments, and laboratory equipment.

- By Form: This segmentation differentiates rhodium based on its physical and chemical states in the market.

- Metal: Refers to rhodium in its pure metallic form, typically as sponge or ingot.

- Powder: Fine particulate rhodium, commonly used in catalyst preparations.

- Solution: Rhodium in dissolved forms, often used in plating baths or as precursors for catalysts.

- Compound: Various chemical compounds of rhodium used in specialized chemical processes.

- By Region: This geographical segmentation highlights regional market sizes, growth rates, and key demand-supply dynamics.

- North America: Key market driven by stringent automotive emission standards and industrial applications.

- Europe: High demand from the automotive and chemical industries, coupled with advanced recycling infrastructure.

- Asia Pacific (APAC): Rapidly growing market due to increasing automotive production, industrialization, and tightening emission norms in countries like China and India.

- Latin America: Emerging market with growing industrial activities and developing automotive sector.

- Middle East & Africa (MEA): Significant due to primary rhodium production and developing industrial base.

Regional Highlights

The global Rhodium market exhibits distinct regional dynamics, influenced by varying industrial activity, regulatory frameworks, and economic conditions. Understanding these regional contributions is vital for strategic market engagement.

- Asia Pacific (APAC): This region is projected to be the fastest-growing market for rhodium, primarily driven by robust automotive production, particularly in China and India. Increasingly stringent vehicle emission standards across APAC countries are mandating the greater adoption of catalytic converters, directly boosting rhodium demand. Furthermore, the expansion of the chemical and glass manufacturing industries in key economies like China, Japan, and South Korea significantly contributes to industrial rhodium consumption.

- Europe: Europe represents a mature but substantial market for rhodium, characterized by a strong automotive sector and a well-developed chemical industry. Strict Euro emission standards have historically ensured high demand for rhodium in catalytic converters. The region also leads in rhodium recycling and recovery technologies, contributing significantly to secondary supply and promoting circular economy principles within the PGM market.

- North America: The North American market is a significant consumer of rhodium, driven by a large automotive industry and diversified industrial applications. Environmental regulations, though already mature, continue to support demand for catalytic converters. Additionally, ongoing research and development in new catalytic applications and advanced materials contribute to sustained market relevance.

- Middle East & Africa (MEA): This region is crucial not for its demand, but for its role as the dominant primary producer of rhodium, primarily from South Africa. Geopolitical stability and mining policy in this region directly impact global rhodium supply and price stability. The developing industrial base in certain MEA countries also contributes to modest, but growing, local demand.

Top Key Players:

The market research report covers the analysis of key stake holders of the Rhodium Market. Some of the leading players profiled in the report include -:- Sibanye-Stillwater

- Anglo American Platinum (Amplats)

- Impala Platinum Holdings (Implats)

- Northam Platinum

- Glencore

- Johnson Matthey

- BASF

- Heraeus Precious Metals

- Umicore

- Tanaka Kikinzoku Kogyo

- Platinum Group Metals Ltd.

- Royal Bafokeng Platinum

- Norilsk Nickel

- Rio Tinto

- Vale

- African Rainbow Minerals (ARM)

- Eastern Platinum Limited

- Sedibelo Platinum Mines

- Aurubis AG

- Evonik Industries AG

Frequently Asked Questions:

Below are some of the most commonly asked questions regarding the Rhodium market, providing concise and informative answers for quick reference.

What is the current market size of Rhodium?

The global Rhodium market was valued at USD 12.5 Billion in 2025 and is projected to reach USD 19.6 Billion by 2033, growing at a CAGR of 5.8% during the forecast period.What are the primary applications of Rhodium?

Rhodium's primary applications are in automotive catalytic converters, which account for the largest share of demand. It is also extensively used in chemical catalysts, glass manufacturing, electrical and electronics components, and to a lesser extent, in jewelry.How do emission regulations impact the Rhodium market?

Stringent global emission regulations, particularly for vehicles, directly drive the demand for rhodium. As governments worldwide implement stricter standards for reducing pollutant emissions, more efficient catalytic converters are required, which often necessitate higher loadings of rhodium, thereby boosting market growth.What factors influence Rhodium prices?

Rhodium prices are primarily influenced by its highly concentrated supply (mainly from South Africa), limited global production, and inelastic demand from critical industries like automotive. Geopolitical stability in producing regions, industrial output, and speculative investment also contribute to its notorious price volatility.What is the future outlook for the Rhodium market?

The future outlook for the Rhodium market is characterized by continued strong demand from the automotive and chemical sectors, driven by evolving regulations and industrial growth. Opportunities exist in advanced recycling and new applications like the hydrogen economy, though challenges such as supply concentration and the long-term impact of electric vehicle adoption will necessitate careful navigation.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted