Reciprocating Hydrogen Compressor Market

Reciprocating Hydrogen Compressor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701986 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

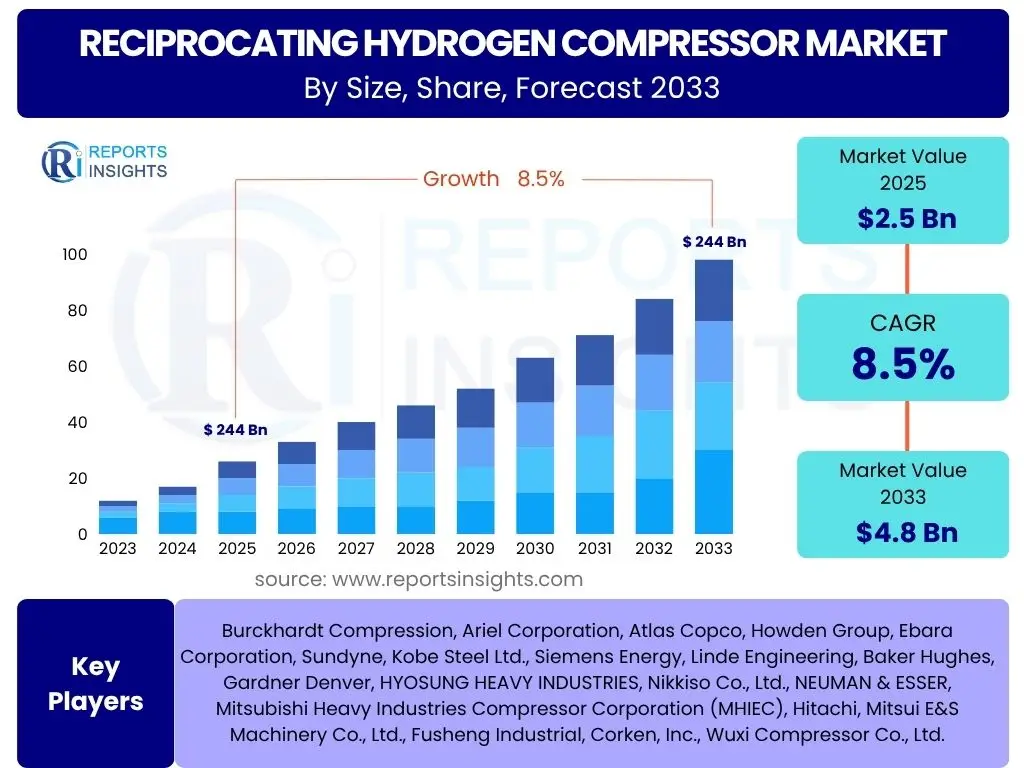

Reciprocating Hydrogen Compressor Market Size

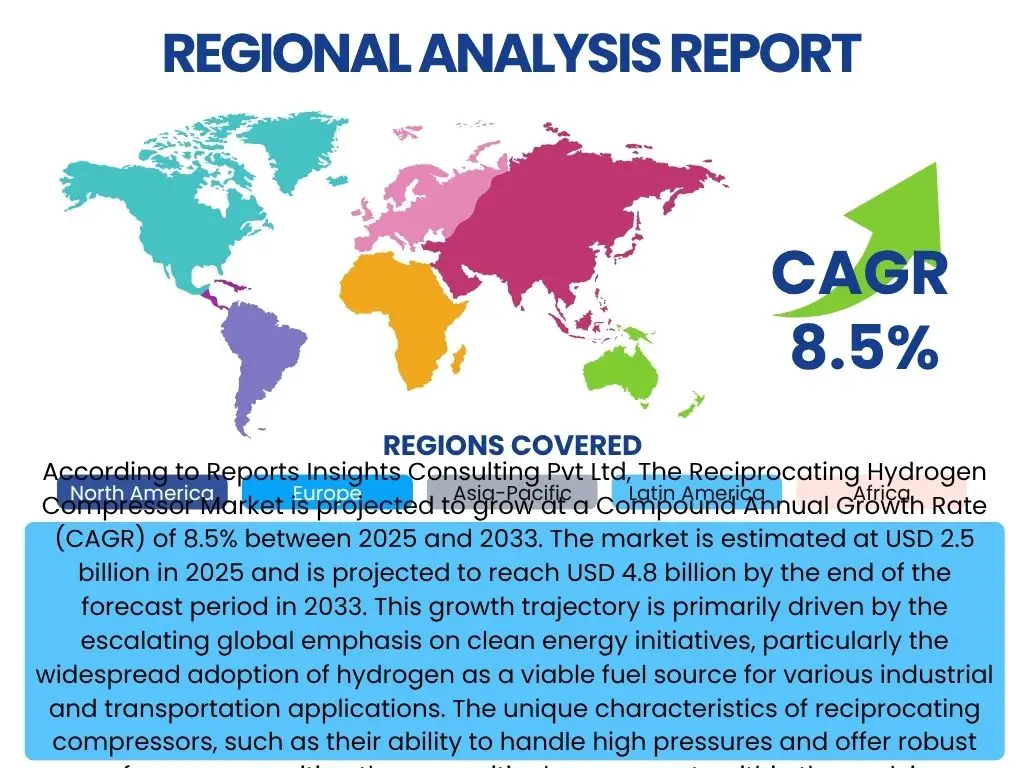

According to Reports Insights Consulting Pvt Ltd, The Reciprocating Hydrogen Compressor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 2.5 billion in 2025 and is projected to reach USD 4.8 billion by the end of the forecast period in 2033. This growth trajectory is primarily driven by the escalating global emphasis on clean energy initiatives, particularly the widespread adoption of hydrogen as a viable fuel source for various industrial and transportation applications. The unique characteristics of reciprocating compressors, such as their ability to handle high pressures and offer robust performance, position them as critical components within the evolving hydrogen economy.

The market's expansion is intrinsically linked to significant investments in hydrogen infrastructure, including the development of large-scale hydrogen production facilities, distribution networks, and refueling stations. Government incentives and supportive policies aimed at decarbonization across sectors such as automotive, power generation, and heavy industry are further bolstering demand for efficient and reliable hydrogen compression solutions. As technological advancements lead to more cost-effective and energy-efficient compressors, their integration into diverse hydrogen value chains is expected to accelerate, driving market size upwards over the forecast period.

Key Reciprocating Hydrogen Compressor Market Trends & Insights

The reciprocating hydrogen compressor market is undergoing transformative shifts driven by global energy transitions and technological innovation. Common user inquiries often revolve around the most significant developments shaping the industry, including advancements in compression efficiency, integration with renewable hydrogen production, and the evolving regulatory landscape. Stakeholders are keen to understand how these trends impact investment opportunities, operational costs, and the overall feasibility of large-scale hydrogen deployment. The market is witnessing a convergence of efforts towards enhancing the durability and reliability of compressors under extreme operating conditions, alongside a push for modular and scalable solutions to meet diverse application requirements.

Furthermore, there is a pronounced trend towards optimizing the total cost of ownership (TCO) for hydrogen compression systems, which includes considerations for energy consumption, maintenance intervals, and capital expenditure. This involves exploring new materials, improved sealing technologies, and advanced control systems that can reduce operational downtime and extend equipment lifespan. The increasing focus on green hydrogen production, generated from renewable energy sources, is also a pivotal trend, as it necessitates compressors capable of handling higher purity hydrogen and integrating seamlessly with electrolyzer facilities. These market dynamics highlight a strategic imperative for manufacturers to innovate and adapt their product offerings to align with the future demands of a rapidly expanding hydrogen ecosystem.

- Growing demand for green hydrogen and associated infrastructure development.

- Increased focus on high-pressure compression for hydrogen refueling stations and industrial applications.

- Technological advancements in sealing solutions and material science for enhanced durability.

- Emphasis on energy efficiency and reduced operational costs through improved compressor designs.

- Integration of smart monitoring and predictive maintenance systems.

- Development of modular and scalable compression solutions for diverse applications.

- Rising adoption of hydrogen in new sectors like maritime and aviation.

AI Impact Analysis on Reciprocating Hydrogen Compressor

Common user questions related to the impact of AI on reciprocating hydrogen compressors frequently center on how artificial intelligence can enhance operational efficiency, predictive maintenance capabilities, and overall system reliability. Stakeholders are particularly interested in AI's potential to optimize compressor performance by analyzing real-time operational data, identifying anomalies, and predicting component failures before they occur. This proactive approach to maintenance, driven by AI algorithms, promises to significantly reduce downtime, lower maintenance costs, and extend the lifespan of critical compression equipment, thereby improving the economic viability of hydrogen infrastructure projects.

AI's influence extends beyond maintenance to include optimized energy management and improved process control. Through machine learning models, compressors can adapt their operations based on fluctuating demand, energy prices, or hydrogen production rates, leading to more efficient energy utilization and reduced operational expenses. Furthermore, AI-driven simulations and design optimization tools are accelerating the development of next-generation compressor technologies, allowing manufacturers to quickly prototype and test new designs for enhanced performance, safety, and scalability. This transformative impact positions AI as a crucial enabler for the future growth and sustainability of the reciprocating hydrogen compressor market.

- Enhanced predictive maintenance and fault diagnosis through machine learning algorithms.

- Optimized compressor performance and energy consumption via AI-driven control systems.

- Improved operational efficiency and reduced downtime through real-time data analysis.

- Accelerated design and development of new compressor models using AI simulation tools.

- Automated monitoring and anomaly detection for increased safety and reliability.

- Better integration with smart grid systems and renewable energy sources for demand-side management.

Key Takeaways Reciprocating Hydrogen Compressor Market Size & Forecast

An analysis of common user questions about key takeaways from the Reciprocating Hydrogen Compressor market size and forecast reveals a strong interest in understanding the core growth drivers, the longevity of the market's expansion, and the critical factors that will influence its trajectory. Users frequently inquire about the primary applications propelling demand, the regions expected to exhibit the most significant growth, and the overarching macroeconomic and policy environments supporting the market. The insights indicate that the sustained momentum of the market is deeply intertwined with global decarbonization efforts and the strategic energy diversification initiatives being pursued by nations worldwide.

Furthermore, stakeholders are keen on identifying the key technological advancements that will shape the market's future, particularly those that address efficiency, reliability, and cost-effectiveness. The market's growth is not merely volumetric but also qualitative, driven by the increasing sophistication of hydrogen production, storage, and distribution technologies. The forecast underscores the critical role of robust and high-performance reciprocating compressors in enabling the widespread adoption of hydrogen across various end-use sectors, solidifying their position as an indispensable technology for the clean energy transition.

- The market is poised for significant growth, projected to nearly double in value by 2033.

- Primary growth is fueled by expanding hydrogen infrastructure and clean energy mandates.

- Technological advancements are crucial for enhancing efficiency and reducing TCO.

- High-pressure applications, particularly hydrogen refueling, will be a major demand driver.

- Government policies and incentives play a pivotal role in accelerating market adoption.

- Emerging markets and regions investing heavily in hydrogen will present substantial opportunities.

Reciprocating Hydrogen Compressor Market Drivers Analysis

The Reciprocating Hydrogen Compressor Market is primarily propelled by the global shift towards a hydrogen-based economy, driven by urgent climate action goals and energy security concerns. The increasing investment in green hydrogen production, fueled by renewable energy sources, necessitates robust compression solutions for storage, transportation, and end-use applications. Governments worldwide are implementing supportive policies, subsidies, and regulatory frameworks to incentivize hydrogen infrastructure development, creating a favorable environment for market expansion. This policy push, coupled with corporate commitments to decarbonization, is significantly accelerating the demand for efficient and reliable hydrogen compressors across various industrial and commercial sectors.

Furthermore, the escalating demand for hydrogen in new and expanding applications, such as fuel cell electric vehicles (FCEVs), industrial feedstock, power generation, and steel production, is a major driver. Reciprocating compressors, known for their ability to achieve high pressures and handle varying flow rates, are well-suited for these diverse applications, especially high-pressure hydrogen refueling stations and large-scale industrial processes. The continuous technological advancements focused on improving compressor efficiency, reliability, and reducing operational costs are also key contributors, making hydrogen compression more economically viable and attractive for large-scale deployment.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Global Hydrogen Economy & Decarbonization Goals | +2.5% | Global, particularly Europe, North America, APAC | Short to Long-term (2025-2033) |

| Increasing Investment in Hydrogen Infrastructure (e.g., refueling stations) | +2.0% | China, Japan, South Korea, Germany, USA | Medium to Long-term (2026-2033) |

| Technological Advancements in Compressor Efficiency & Durability | +1.5% | Global, driven by innovation hubs in Europe & North America | Short to Medium-term (2025-2030) |

| Supportive Government Policies, Incentives & Regulations | +1.0% | EU member states, USA, Canada, Australia | Short to Long-term (2025-2033) |

| Rising Demand for Green Hydrogen Production | +1.5% | Middle East, Australia, Chile, North Africa, Europe | Medium to Long-term (2027-2033) |

Reciprocating Hydrogen Compressor Market Restraints Analysis

Despite the optimistic growth projections, the Reciprocating Hydrogen Compressor Market faces several significant restraints that could impede its full potential. A primary challenge is the high initial capital expenditure associated with hydrogen infrastructure development, including the cost of high-pressure compressors, storage tanks, and distribution networks. This substantial upfront investment can deter potential adopters, particularly small and medium-sized enterprises, from transitioning to hydrogen solutions. Furthermore, the existing energy infrastructure is largely geared towards fossil fuels, requiring significant modifications and new construction to accommodate widespread hydrogen deployment, adding to the cost burden and extending project timelines.

Another key restraint is the current relatively high cost of hydrogen production, especially green hydrogen, which impacts the overall economic viability of hydrogen projects. While costs are declining, they remain a barrier for widespread commercial adoption compared to established energy sources. Additionally, safety concerns related to hydrogen handling, storage, and transportation, particularly at high pressures, necessitate stringent safety protocols and advanced materials, which can increase the complexity and cost of compressor design and operation. Technical challenges such as hydrogen embrittlement of materials and the need for highly reliable sealing solutions under extreme conditions also present ongoing research and development hurdles that can slow market penetration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for Hydrogen Infrastructure | -1.8% | Global, particularly developing economies | Short to Medium-term (2025-2030) |

| High Cost of Green Hydrogen Production | -1.5% | Global | Short to Medium-term (2025-2030) |

| Technical Challenges (e.g., hydrogen embrittlement, sealing) | -1.2% | Global, impacting R&D and product cycles | Short to Medium-term (2025-2029) |

| Limited Existing Hydrogen Infrastructure & Supply Chains | -1.0% | Global, more pronounced in emerging markets | Short to Medium-term (2025-2030) |

| Public Perception & Safety Concerns | -0.8% | Global | Long-term (2025-2033) |

Reciprocating Hydrogen Compressor Market Opportunities Analysis

Significant opportunities are emerging for the Reciprocating Hydrogen Compressor Market, driven by the accelerating global transition towards sustainable energy systems. The increasing focus on diversifying energy sources and achieving net-zero emissions targets presents a vast addressable market for hydrogen technologies across various sectors. The rapid development of large-scale green hydrogen projects, particularly in regions with abundant renewable energy resources, creates a direct demand for high-capacity and efficient compression solutions for storage and distribution. These projects, often supported by significant government funding and private investments, offer substantial avenues for market penetration and growth for compressor manufacturers.

Moreover, the expansion of hydrogen refueling station networks globally, necessitated by the growing adoption of fuel cell electric vehicles (FCEVs) and heavy-duty transport, represents a lucrative opportunity. Reciprocating compressors are critical components in these stations, providing the high pressures required for fast and efficient vehicle refueling. Beyond transportation, the decarbonization of hard-to-abate sectors such as steel production, chemicals, and cement manufacturing, through the utilization of hydrogen as a clean feedstock or fuel, opens up new industrial applications for high-pressure hydrogen compression. The development of advanced materials, smart monitoring systems, and modular compressor designs further enhances the appeal and applicability of these technologies, fostering innovation and creating competitive advantages.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Green Hydrogen Production Capacity | +2.0% | Europe, Australia, Middle East, North America | Medium to Long-term (2026-2033) |

| Growth of Hydrogen Refueling Station Networks | +1.8% | Japan, South Korea, China, Germany, California (USA) | Short to Medium-term (2025-2030) |

| Decarbonization of Heavy Industry (Steel, Chemicals, Cement) | +1.5% | Global, particularly industrial hubs in APAC & Europe | Medium to Long-term (2027-2033) |

| Advancements in Hydrogen Storage & Transportation Technologies | +1.0% | Global, cross-industry collaboration | Short to Medium-term (2025-2030) |

| Emergence of Hydrogen for Power Generation (e.g., gas turbines) | +0.8% | Europe, North America, Japan | Long-term (2028-2033) |

Reciprocating Hydrogen Compressor Market Challenges Impact Analysis

The Reciprocating Hydrogen Compressor Market faces various challenges that require innovative solutions and strategic approaches to overcome. One significant hurdle is the inherent technical complexity associated with compressing hydrogen, particularly at very high pressures, which demands specialized materials and advanced sealing technologies to prevent leakage and ensure safety. Hydrogen's unique properties, such as its small molecular size and tendency to cause embrittlement in certain metals, necessitate continuous research and development to enhance compressor durability and reliability, adding to manufacturing costs and potentially slowing down market adoption if not effectively addressed.

Furthermore, fierce competition from alternative hydrogen compression technologies, such as diaphragm compressors for extremely high pressures or centrifugal compressors for very large volumes, presents a market challenge. While reciprocating compressors offer distinct advantages in certain applications, continuous innovation is required to maintain their competitive edge. The lack of standardized codes and regulations across different regions for hydrogen infrastructure can also create complexities for manufacturers and project developers, leading to increased costs and slower deployment. Addressing these challenges through collaborative industry efforts, robust R&D investments, and supportive policy frameworks will be crucial for the sustained growth of the reciprocating hydrogen compressor market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technical Complexities of High-Pressure Hydrogen Compression | -1.5% | Global, impacting R&D and manufacturing | Short to Medium-term (2025-2029) |

| Hydrogen Embrittlement & Material Compatibility Issues | -1.2% | Global, impacting design and longevity | Short to Medium-term (2025-2030) |

| Competition from Alternative Compression Technologies | -1.0% | Global, impacting market share | Short to Long-term (2025-2033) |

| Lack of Standardized Codes & Regulations | -0.8% | Global, particularly cross-border projects | Medium-term (2025-2030) |

| Supply Chain Vulnerabilities & Raw Material Costs | -0.7% | Global, influenced by geopolitical factors | Short-term (2025-2027) |

Reciprocating Hydrogen Compressor Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Reciprocating Hydrogen Compressor Market, offering a detailed overview of its current size, historical performance, and future growth projections. The scope encompasses key market drivers, restraints, opportunities, and challenges influencing the industry landscape, along with a thorough examination of market trends, technological advancements, and the impact of artificial intelligence. The report meticulously segments the market by type, pressure range, application, and end-use industry, providing granular insights into demand patterns across various sectors. It also includes a robust regional analysis, highlighting market dynamics and growth prospects across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Additionally, a comprehensive competitive landscape section profiles leading companies, offering insights into their strategic initiatives and market positioning, enabling stakeholders to make informed business decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.5 Billion |

| Market Forecast in 2033 | USD 4.8 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Burckhardt Compression, Ariel Corporation, Atlas Copco, Howden Group, Ebara Corporation, Sundyne, Kobe Steel Ltd., Siemens Energy, Linde Engineering, Baker Hughes, Gardner Denver, HYOSUNG HEAVY INDUSTRIES, Nikkiso Co., Ltd., NEUMAN & ESSER, Mitsubishi Heavy Industries Compressor Corporation (MHIEC), Hitachi, Mitsui E&S Machinery Co., Ltd., Fusheng Industrial, Corken, Inc., Wuxi Compressor Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Reciprocating Hydrogen Compressor Market is meticulously segmented to provide a detailed understanding of its diverse landscape and the specific dynamics influencing different product categories, pressure requirements, and end-use applications. This granular segmentation allows for a precise evaluation of demand drivers and growth opportunities across various market niches. Analyzing the market by type helps in understanding the preferences for oil-free versus lubricated compressors, reflecting industry needs for purity and maintenance considerations. The pressure range segmentation is crucial as hydrogen applications vary widely in their pressure requirements, from industrial supply to high-pressure vehicle refueling.

Further segmentation by application and end-use industry highlights the critical role of reciprocating compressors in specific sectors. Hydrogen refueling stations represent a significant and growing application due to the expansion of fuel cell electric vehicles. Industrial gas supply, chemical processing, and power generation also constitute major demand centers, each with unique technical specifications and regulatory requirements. This comprehensive segmentation provides a robust framework for market participants to identify lucrative segments, tailor their product offerings, and devise effective market entry and growth strategies, ultimately contributing to the overall market's expansion and diversification.

- By Type:

- Oil-free Reciprocating Compressors

- Lubricated Reciprocating Compressors

- Multi-stage Reciprocating Compressors

- By Pressure Range:

- Low Pressure (< 200 bar)

- Medium Pressure (200-500 bar)

- High Pressure (> 500 bar)

- By Application:

- Hydrogen Refueling Stations (HRS)

- Industrial Gas Supply

- Chemical & Petrochemical Processing

- Energy & Power Generation

- Metallurgy

- Research & Development

- Others

- By End-Use Industry:

- Automotive

- Chemical & Pharma

- Oil & Gas

- Power Generation

- General Manufacturing

- Aerospace & Defense

- Metal & Mining

Regional Highlights

The global reciprocating hydrogen compressor market exhibits varied dynamics across key geographical regions, each contributing uniquely to the overall market growth based on their energy policies, industrial landscapes, and hydrogen infrastructure development. Asia Pacific, particularly countries like China, Japan, and South Korea, is projected to be a dominant and rapidly growing market. This is primarily attributed to robust government initiatives supporting hydrogen adoption, significant investments in fuel cell electric vehicle manufacturing, and the establishment of extensive hydrogen refueling networks. Japan's long-standing commitment to a hydrogen society and China's ambitious decarbonization targets drive substantial demand for high-pressure compression solutions, establishing the region as a global leader in hydrogen technology deployment.

Europe is another key region, demonstrating strong growth fueled by the European Union's ambitious hydrogen strategy aimed at achieving climate neutrality. Countries such as Germany, the Netherlands, and France are heavily investing in green hydrogen production via electrolysis and developing cross-border hydrogen pipelines, which necessitates high-performance compressors for various applications, including industrial use and energy storage. North America, especially the United States and Canada, is also witnessing increasing traction due to policy support through initiatives like the Bipartisan Infrastructure Law, focusing on hydrogen hubs and clean energy projects. This regional diversity underscores the global commitment to hydrogen as a cornerstone of future energy systems, driving demand for advanced compression technologies.

- North America: Driven by government funding for hydrogen hubs and decarbonization efforts in industrial sectors, particularly in the United States and Canada.

- Europe: Strong growth propelled by the European Hydrogen Strategy, significant investments in green hydrogen production, and cross-border infrastructure development, notably in Germany, France, and the Netherlands.

- Asia Pacific (APAC): Expected to be the largest and fastest-growing market due to aggressive hydrogen strategies in China, Japan, and South Korea, coupled with expanding FCEV markets and industrial applications.

- Latin America: Emerging market with potential due to renewable energy resources for green hydrogen production, though infrastructure development is in nascent stages.

- Middle East and Africa (MEA): Significant long-term potential for green hydrogen exports and domestic use, leveraging abundant solar and wind resources, leading to future demand for large-scale compression.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Reciprocating Hydrogen Compressor Market.- Burckhardt Compression

- Ariel Corporation

- Atlas Copco

- Howden Group

- Ebara Corporation

- Sundyne

- Kobe Steel Ltd.

- Siemens Energy

- Linde Engineering

- Baker Hughes

- Gardner Denver

- HYOSUNG HEAVY INDUSTRIES

- Nikkiso Co., Ltd.

- NEUMAN & ESSER

- Mitsubishi Heavy Industries Compressor Corporation (MHIEC)

- Hitachi

- Mitsui E&S Machinery Co., Ltd.

- Fusheng Industrial

- Corken, Inc.

- Wuxi Compressor Co., Ltd.

Frequently Asked Questions

What is the projected growth rate for the Reciprocating Hydrogen Compressor Market?

The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033, driven by expanding hydrogen infrastructure and global decarbonization efforts.

What are the primary drivers of the Reciprocating Hydrogen Compressor Market?

Key drivers include the global shift towards a hydrogen economy, increasing investments in green hydrogen production and infrastructure, technological advancements in compressor efficiency, and supportive government policies worldwide.

How does AI impact the Reciprocating Hydrogen Compressor industry?

AI significantly enhances operational efficiency through predictive maintenance, optimizes energy consumption via smart control systems, and accelerates compressor design and development using advanced simulation tools.

Which regions are expected to show the most significant growth in this market?

Asia Pacific, particularly China, Japan, and South Korea, is projected to be the largest and fastest-growing market due to aggressive hydrogen strategies and infrastructure development. Europe and North America also show strong growth.

What are the main applications for reciprocating hydrogen compressors?

Primary applications include hydrogen refueling stations, industrial gas supply, chemical and petrochemical processing, energy and power generation, and metallurgy, driven by the need for high-pressure hydrogen handling.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted