Organic Wine Market

Organic Wine Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700429 | Last Updated : July 24, 2025 |

Format : ![]()

![]()

![]()

![]()

Organic Wine Market Size

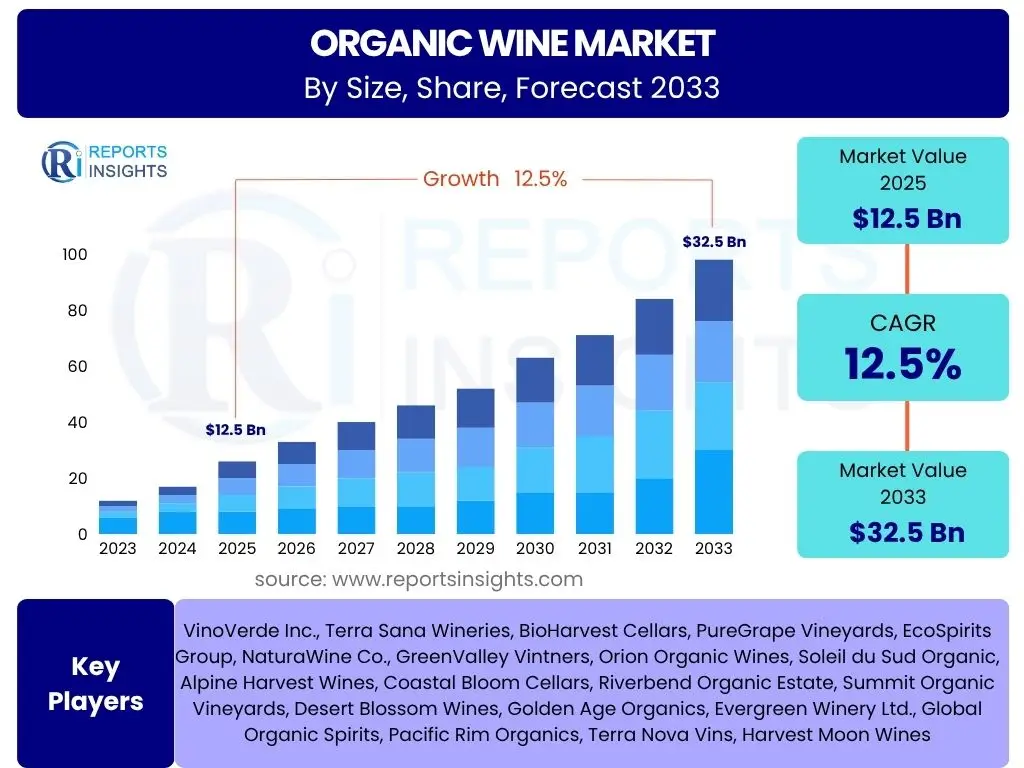

The Organic Wine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2033, valued at USD 12.5 Billion in 2025 and is projected to reach USD 32.5 Billion by 2033, marking the end of the forecast period. This significant expansion is driven by escalating consumer demand for sustainable and health-conscious products, coupled with advancements in organic viticulture and expanding global distribution networks. The market's robust growth trajectory reflects a fundamental shift in consumer preferences towards environmentally friendly and ethically produced goods, positioning organic wine as a premium segment with considerable future potential across diverse geographical regions.

Key Organic Wine Market Trends & Insights

The organic wine market is characterized by several dynamic trends reflecting evolving consumer values and industry innovation. Firstly, there is a pronounced surge in consumer health and wellness consciousness, driving demand for wines free from synthetic pesticides and fertilizers. Secondly, a heightened focus on environmental sustainability and ethical consumption patterns is influencing purchasing decisions, as consumers increasingly seek products that align with their eco-friendly principles. Thirdly, the ongoing premiumization of organic wines, with an emphasis on quality and unique terroir expressions, is attracting a sophisticated consumer base willing to pay more for superior products. Fourthly, the rapid expansion of e-commerce platforms and specialized online wine retailers is significantly improving accessibility and convenience for organic wine consumers worldwide. Lastly, innovation in packaging solutions, including lighter glass bottles and alternative formats like cans and bag-in-box, is gaining traction, driven by sustainability goals and convenience for a broader range of consumption occasions.

AI Impact Analysis on Organic Wine

The integration of Artificial intelligence (AI) is set to revolutionize various facets of the organic wine industry, offering unprecedented opportunities for optimization and innovation. AI-driven precision viticulture applications are enabling vineyards to monitor soil health, predict disease outbreaks, and optimize irrigation and nutrient delivery with remarkable accuracy, thereby improving grape quality and yield while reducing resource consumption, critical for organic certification. Furthermore, AI is enhancing supply chain efficiency through predictive analytics for demand forecasting, inventory management, and logistics optimization, ensuring optimal freshness and reducing waste from vineyard to consumer. In terms of consumer engagement, AI algorithms are facilitating highly personalized marketing campaigns and product recommendations, analyzing individual preferences to connect consumers with organic wines that truly match their tastes. Quality control processes are also being transformed by AI, with intelligent systems capable of analyzing fermentation processes, detecting defects, and ensuring consistent product quality without compromising organic integrity. Lastly, AI is providing invaluable insights into market trends and consumer behavior, allowing organic wine producers to rapidly adapt to shifts in demand and identify emerging opportunities for product development and market expansion.

Key Takeaways Organic Wine Market Size & Forecast

- The organic wine market exhibits robust double-digit growth, driven primarily by increasing consumer health awareness and sustainability concerns.

- Significant market expansion is anticipated in both established European markets and rapidly emerging economies across Asia Pacific and Latin America.

- Technological advancements, particularly in precision viticulture and supply chain optimization, are pivotal in enhancing the efficiency and quality of organic wine production.

- Premiumization trends are fostering higher average selling prices, contributing substantially to overall market value growth.

- Distribution channel diversification, notably through e-commerce and specialized retail, is expanding market reach and consumer accessibility.

- Regulatory support for organic farming and clear certification standards continue to build consumer trust and market credibility.

- Despite higher production costs and supply constraints, the long-term outlook for organic wine remains exceptionally positive due to persistent consumer demand for authentic, eco-friendly products.

Organic Wine Market Drivers Analysis

The organic wine market's upward trajectory is underpinned by a confluence of powerful drivers that collectively amplify demand and foster industry innovation. These drivers span across shifting consumer preferences, technological advancements, and evolving regulatory landscapes, creating a fertile ground for sustained growth. The increasing global awareness regarding health and environmental sustainability is arguably the most significant catalyst, compelling consumers to seek out products that align with their values of purity and ecological responsibility. This fundamental shift is further supported by expanding distribution channels and a growing appreciation for the premium quality associated with organic viticulture.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Consumer Health and Wellness Consciousness: Consumers are increasingly prioritizing natural, chemical-free products, driving demand for organic wines perceived as healthier alternatives to conventional varieties due to the absence of synthetic pesticides, herbicides, and chemical fertilizers. This trend is amplified by a growing understanding of the benefits of organic farming practices on personal health and environmental well-being. | +4.0% | North America, Western Europe, Australia, Japan | Short to Long-term (2025-2033) |

| Growing Environmental Sustainability and Ethical Consumption: A significant segment of the global consumer base is becoming more environmentally conscious, actively seeking out products that contribute positively to ecological preservation. Organic wine, produced through sustainable viticulture that promotes biodiversity and soil health, aligns perfectly with these ethical consumption patterns, enhancing its appeal. | +3.5% | Europe (France, Italy, Germany), Scandinavia, Pacific Northwest (USA), New Zealand | Medium to Long-term (2027-2033) |

| Supportive Government Policies and Organic Certifications: Government bodies and international organizations are increasingly establishing and promoting stringent organic certification standards and offering incentives for organic farming. This regulatory support lends credibility to organic wine, builds consumer trust, and encourages more vineyards to transition to organic practices, standardizing quality and authenticity. | +2.5% | European Union (EU Organic), United States (USDA Organic), Canada, Australia, China | Short to Medium-term (2025-2030) |

| Expansion of Distribution Channels and E-commerce Adoption: The increasing availability of organic wines through diverse retail channels, including major supermarkets, specialty organic stores, and a rapidly expanding online retail presence, is significantly improving market accessibility. E-commerce platforms, in particular, enable producers to reach a wider, geographically dispersed consumer base directly. | +1.5% | Global, particularly North America, Europe, and emerging APAC e-commerce markets | Short-term (2025-2028) |

| Premiumization and Diversification of Organic Offerings: Organic wine is increasingly shedding its niche image and entering the premium segment, with producers focusing on high-quality varietals and sophisticated blends. The diversification into sparkling organic wines, low-alcohol options, and unique terroir expressions broadens consumer appeal and justifies higher price points, attracting connoisseurs. | +1.0% | France, Italy, Spain, California (USA), South Africa, Argentina | Medium to Long-term (2027-2033) |

Organic Wine Market Restraints Analysis

Despite its promising growth trajectory, the organic wine market faces several inherent restraints that can temper its expansion and present challenges to producers and consumers alike. These limitations primarily stem from the complexities of organic farming, market perceptions, and economic factors. The higher costs associated with organic viticulture, coupled with potentially lower yields compared to conventional methods, often result in a higher price point for organic wines. This elevated cost can be a significant barrier for price-sensitive consumers, limiting broader market penetration. Additionally, the time-consuming and rigorous certification processes, along with limited availability of certified organic grapes, pose supply-side constraints. Overcoming these restraints requires innovative strategies, consumer education, and continued investment in sustainable practices to balance growth with market realities.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Production Costs and Lower Yields: Organic farming methods often entail increased manual labor, stricter pest and disease management without synthetic chemicals, and lower permissible yields per hectare to maintain soil health. These factors contribute significantly to higher production costs compared to conventional wine, which translates into a higher retail price for organic wine. | -2.0% | Global, particularly competitive markets like North America and Europe | Short to Medium-term (2025-2030) |

| Limited Availability of Certified Organic Grapes and Conversion Time: The process of converting a conventional vineyard to certified organic status is lengthy and rigorous, typically requiring a transition period of three years. This, combined with the stringent requirements for organic cultivation, limits the immediate supply of organic grapes and therefore organic wine, creating supply-demand imbalances. | -1.5% | Major wine-producing regions (e.g., France, Italy, Spain, California) | Medium-term (2027-2032) |

| Price Sensitivity Among Consumers: Despite growing environmental awareness, a significant portion of consumers remains price-sensitive. The premium price point of organic wine, often 20-50% higher than comparable conventional wines, can deter mass market adoption, particularly in regions with lower disposable incomes or strong competition from affordable conventional options. | -1.0% | Emerging Markets (Asia Pacific, Latin America), parts of Eastern Europe | Short-term (2025-2028) |

| Perception of Inconsistent Quality or Shorter Shelf Life: Historically, some consumers have harbored misconceptions about the quality or longevity of organic wines, believing them to be less stable or more prone to spoilage without conventional additives. While modern organic winemaking techniques have largely dispelled these myths, residual perceptions can still act as a minor deterrent for some buyers. | -0.5% | Global, particularly markets with established wine traditions | Medium-term (2027-2032) |

Organic Wine Market Opportunities Analysis

The organic wine market is ripe with opportunities that, if strategically leveraged, can significantly accelerate its growth and expand its global footprint. These opportunities stem from evolving consumer lifestyles, technological innovation, and unexplored geographical territories. The increasing global awareness of health and environmental issues is opening doors in emerging markets where sustainable consumption is gaining traction. Furthermore, advancements in viticultural technology are making organic farming more efficient and less risky, while product diversification allows brands to tap into new consumer segments and consumption occasions. The burgeoning e-commerce landscape also presents a low-cost, high-reach avenue for market expansion, enabling organic wine producers to connect directly with consumers who prioritize authenticity and sustainability.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets: Growing disposable incomes, increasing health consciousness, and burgeoning environmental awareness in regions like Asia Pacific (e.g., China, India, Southeast Asia) and Latin America present significant untapped potential. These markets are increasingly receptive to premium and sustainable products, offering new growth avenues for organic wine producers. | +2.0% | Asia Pacific, Latin America, Middle East | Medium to Long-term (2027-2033) |

| Product Diversification and Innovation: Development of new organic wine categories such as sparkling organic wines, low-alcohol or alcohol-free organic options, organic fortified wines, and innovative packaging formats like cans and pouches can attract younger demographics and cater to diverse consumption preferences and occasions, expanding the market's reach. | +1.8% | North America, Europe, Australia | Short to Medium-term (2025-2030) |

| Technological Advancements in Organic Viticulture: Ongoing innovations in precision farming, biological pest control, and vineyard management software are making organic viticulture more efficient, resilient, and cost-effective. These technologies can help address historical challenges related to yield stability and disease management, thereby encouraging more vineyards to adopt organic practices. | +1.5% | Major wine-producing nations (e.g., USA, France, Italy, Chile) | Medium to Long-term (2027-2033) |

| Growth of E-commerce and Direct-to-Consumer (DTC) Sales Models: The acceleration of online retail platforms and direct-to-consumer sales provides organic wine producers with a cost-effective way to bypass traditional distribution layers, reach niche markets, and offer a personalized shopping experience. This model also allows for greater transparency and direct communication regarding organic credentials. | +1.2% | Global, particularly North America, Western Europe, and rapidly digitalizing APAC regions | Short-term (2025-2028) |

Organic Wine Market Challenges Impact Analysis

Despite the inherent strengths and opportunities within the organic wine market, several significant challenges persist, requiring strategic navigation by industry players. These challenges are often magnified by the very nature of organic production, which relies heavily on natural processes and is more susceptible to external environmental factors. Climate change, with its unpredictable weather patterns, poses a substantial threat to organic grape cultivation, impacting yield and quality. Moreover, the integrity of organic certification faces ongoing threats from fraud and counterfeiting, which can erode consumer trust and brand value. Intense competition from conventional wines, often at lower price points and with wider market penetration, also demands robust marketing and differentiation strategies. Addressing these challenges effectively will be crucial for the sustained growth and credibility of the organic wine sector.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Climate Change and Weather Volatility: Organic vineyards are particularly vulnerable to the impacts of climate change, including extreme temperatures, unpredictable rainfall patterns, droughts, and increased frequency of severe weather events. These conditions can significantly affect grape yields, quality, and the overall viability of organic farming, leading to production instability and economic losses. | -1.5% | Global wine regions, notably Mediterranean climates (Southern Europe, California, Australia) | Long-term (2028-2033) |

| Maintaining Authenticity and Preventing Fraud/Counterfeiting: As the organic wine market grows, so does the risk of fraudulent labeling and counterfeiting. Ensuring the authenticity of organic certifications and protecting consumers from mislabeled products is a continuous challenge that requires robust regulatory oversight, advanced traceability systems, and consumer education to maintain market integrity and trust. | -1.0% | Global, particularly markets with high demand and complex supply chains | Medium to Long-term (2027-2033) |

| Intense Competition from Conventional Wine Market: The organic wine market, despite its growth, still represents a smaller segment compared to the vast conventional wine market. Organic wines face strong competition from well-established conventional brands that often benefit from economies of scale, lower production costs, broader marketing budgets, and wider consumer recognition, necessitating strong differentiation. | -0.8% | Global, especially in mature wine-consuming markets | Short to Medium-term (2025-2030) |

| Supply Chain Disruptions and Logistics for Niche Products: The global supply chain is susceptible to disruptions from geopolitical events, natural disasters, and trade policy changes. For organic wine, which often originates from specialized vineyards and may involve complex international logistics, these disruptions can severely impact supply, increase costs, and challenge timely delivery to consumers. | -0.7% | Global, particularly for import/export dependent regions | Short-term (2025-2028) |

Organic Wine Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Organic Wine Market, offering critical insights into its current size, historical performance, and future growth projections. It meticulously examines the key trends, growth drivers, inherent restraints, emerging opportunities, and significant challenges that shape the industry landscape. The report also features a detailed segmentation analysis, encompassing various product types, packaging formats, and distribution channels. Furthermore, it delivers a thorough regional assessment, highlighting the performance and unique dynamics of key geographical markets, alongside profiles of leading market players, ensuring a holistic understanding for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 32.5 Billion |

| Growth Rate | 12.5% |

| Number of Pages | 248 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | VinoVerde Inc., Terra Sana Wineries, BioHarvest Cellars, PureGrape Vineyards, EcoSpirits Group, NaturaWine Co., GreenValley Vintners, Orion Organic Wines, Soleil du Sud Organic, Alpine Harvest Wines, Coastal Bloom Cellars, Riverbend Organic Estate, Summit Organic Vineyards, Desert Blossom Wines, Golden Age Organics, Evergreen Winery Ltd., Global Organic Spirits, Pacific Rim Organics, Terra Nova Vins, Harvest Moon Wines |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Organic Wine Market is meticulously segmented to provide a granular understanding of its diverse components and consumer preferences. This detailed analysis allows stakeholders to identify specific growth areas, target consumer groups, and develop tailored strategies. The segmentation primarily considers the type of wine, its packaging, the channels through which it reaches consumers, and the crucial certification standards it adheres to, each playing a vital role in shaping market dynamics and consumer choices across different regions.

- By Type: This segment categorizes organic wines based on their color and style, reflecting diverse consumer palates and traditional preferences.

- Red Organic Wine: Represents a significant share due to its popularity and traditional association with wine consumption, often sought for its rich flavors and health benefits.

- White Organic Wine: Gaining traction, particularly among consumers seeking lighter, more refreshing options, and often perceived as versatile for various culinary pairings.

- Rosé Organic Wine: Experiencing rapid growth, especially in warmer climates and among younger demographics, driven by its vibrant appeal and easy-drinking style.

- Sparkling Organic Wine: A dynamic segment benefiting from increasing demand for celebratory beverages and innovative organic production techniques.

- Others: Includes niche categories such as fortified organic wines (e.g., organic Port, Sherry) and sweet organic wines, catering to specialized tastes.

- By Packaging: This segmentation reflects the evolving consumer demand for convenience, sustainability, and aesthetic appeal in wine packaging.

- Glass Bottles: Remain the dominant packaging format, widely accepted for their traditional appeal, perceived quality preservation, and recyclability.

- Bag-in-Box: Gaining popularity for its convenience, extended shelf life after opening, and reduced environmental footprint due to lighter weight and less material usage.

- Cans: A rapidly emerging segment, particularly appealing to younger consumers and for on-the-go consumption, offering single-serving convenience and environmental benefits.

- Others: Includes alternative formats such as pouches, Tetra Pak cartons, and smaller, single-serve plastic bottles, driven by innovation in sustainability and portability.

- By Distribution Channel: This categorizes how organic wine reaches the end consumer, indicating the most effective routes to market and consumer access points.

- On-Trade: Encompasses sales through hospitality venues like Hotels, Restaurants, Cafes, and Bars, where organic wine is often featured as part of a curated dining experience, reflecting its premium status.

- Off-Trade: Covers retail sales where wine is purchased for consumption elsewhere, including:

- Supermarkets/Hypermarkets: Major sales channels offering wide accessibility and competitive pricing for a broad consumer base.

- Specialty Stores: Retailers focusing on organic, natural, or gourmet products, attracting informed consumers seeking specific organic wine selections.

- Online Retail: A rapidly expanding channel, offering unparalleled convenience, wider selection, and direct-to-consumer options, driving market penetration globally.

- Convenience Stores: Increasingly stocking organic wine, especially smaller formats, catering to immediate consumption needs.

- Others: Includes direct sales from wineries, farmers' markets, and subscription box services, fostering direct consumer relationships and unique offerings.

- By Certification: This critical segmentation highlights the various regulatory standards organic wines adhere to, assuring consumers of authenticity and quality.

- EU Organic: The most widely recognized and stringent certification in Europe, ensuring compliance with strict organic farming and winemaking regulations across the European Union.

- USDA Organic: The primary certification for organic products in the United States, signifying adherence to national organic standards.

- Other National/Regional Certifications: Includes various country-specific or regional organic standards such as Bio Suisse (Switzerland), Demeter (international biodynamic certification), and others unique to different wine-producing nations, reflecting local regulations and consumer trust.

Regional Highlights

- Europe: Europe stands as the undisputed leader in the organic wine market, driven by a deep-rooted tradition of winemaking, stringent organic farming regulations (EU Organic certification), and a highly developed consumer awareness regarding sustainable practices. Countries such as France, Italy, and Spain are not only major producers but also significant consumers of organic wine. France, in particular, has seen a strong conversion to organic viticulture, with a growing number of vineyards adopting ecological practices. Italy's diverse wine regions have also embraced organic methods, leveraging their rich biodiversity. Germany and Scandinavia exhibit strong consumer demand, often leading per capita consumption due to their advanced environmental consciousness. The supportive governmental policies and subsidies for organic agriculture further bolster market growth across the continent.

- North America: This region represents a rapidly expanding market for organic wine, primarily fueled by the increasing health and wellness trend and a growing preference for natural and clean label products among consumers. The United States is the largest market within North America, experiencing significant growth in both domestic organic wine production and imports. Consumers in states like California, Oregon, and Washington are particularly receptive to organic offerings, aligning with broader trends in organic food consumption. Canada also shows strong growth, driven by similar consumer inclinations and increasing product availability. The retail landscape, including major supermarket chains and online platforms, has been instrumental in making organic wines more accessible to the mainstream consumer.

- Asia Pacific (APAC): The APAC region is poised for substantial growth in the organic wine market, albeit from a lower base compared to Europe and North America. This growth is primarily propelled by rising disposable incomes, rapid urbanization, and an emerging health-conscious consumer class. Countries like China, Japan, and Australia are at the forefront of this expansion. While Japan has a mature market for premium imports, China's burgeoning middle class is increasingly seeking out healthier and environmentally friendly options, creating significant opportunities for both domestic organic wine production and imports. Australia and New Zealand, with their strong focus on sustainable agriculture, are also becoming important players in organic wine production and consumption, influencing regional trends.

- Latin America: This region is emerging as a noteworthy contributor to the global organic wine market, with countries like Chile and Argentina leading the charge. Blessed with diverse terroirs and favorable climatic conditions, these nations are increasingly adopting organic and biodynamic viticulture practices. The emphasis here is often on producing high-quality, export-oriented organic wines that leverage the pristine natural environments. While domestic consumption is growing, a significant portion of the organic wine produced in Latin America is targeted towards export markets, particularly North America and Europe, capitalizing on the global demand for sustainably produced wines.

- Middle East and Africa (MEA): The MEA region currently represents a nascent but growing segment of the organic wine market. Growth is predominantly driven by increasing tourism, exposure to global trends, and a gradual shift in consumer preferences towards premium and healthy beverage options in certain urban centers. Imports constitute the majority of organic wine consumption in this region, with a limited local production base. However, as awareness of organic products expands and disposable incomes rise, there is potential for gradual market development, particularly in countries with established tourism industries and a growing expatriate population.

Top Key Players:

The market research report covers the analysis of key stakeholders of the Organic Wine Market. Some of the leading players profiled in the report include -

- VinoVerde Inc.

- Terra Sana Wineries

- BioHarvest Cellars

- PureGrape Vineyards

- EcoSpirits Group

- NaturaWine Co.

- GreenValley Vintners

- Orion Organic Wines

- Soleil du Sud Organic

- Alpine Harvest Wines

- Coastal Bloom Cellars

- Riverbend Organic Estate

- Summit Organic Vineyards

- Desert Blossom Wines

- Golden Age Organics

- Evergreen Winery Ltd.

- Global Organic Spirits

- Pacific Rim Organics

- Terra Nova Vins

- Harvest Moon Wines

Frequently Asked Questions:

Q1: What is organic wine and how does it differ from conventional wine?

Organic wine is produced from grapes grown without synthetic pesticides, herbicides, fungicides, or chemical fertilizers. The winemaking process also adheres to strict organic standards, which typically involve minimal use of sulfites, no genetically modified organisms (GMOs), and adherence to sustainable practices that promote biodiversity and ecological balance in the vineyard. In contrast, conventional wine production often utilizes synthetic chemicals in viticulture and may employ a broader range of additives and processing aids during winemaking. The core difference lies in the cultivation methods and the absence of synthetic inputs throughout the entire production chain, emphasizing environmental stewardship and the purity of the final product.

Q2: What factors are driving the growth of the organic wine market?

The growth of the organic wine market is primarily driven by escalating consumer health consciousness, leading to a preference for natural and chemical-free products. A heightened global awareness of environmental sustainability also plays a crucial role, as consumers increasingly seek out eco-friendly and ethically produced goods. Furthermore, supportive government policies and the establishment of robust organic certification standards lend credibility and promote widespread adoption. The expansion of e-commerce platforms and diverse distribution channels, coupled with the premiumization and diversification of organic wine offerings, are also significant contributors to the market's robust growth.

Q3: Which regions are dominant in the organic wine market?

Europe currently dominates the organic wine market, with countries like France, Italy, and Spain being major producers and consumers, supported by strong organic farming traditions and stringent EU organic regulations. North America, particularly the United States, is also a significant and rapidly growing market, driven by increasing consumer health awareness and strong demand for sustainable products. Asia Pacific, though starting from a smaller base, is emerging as a key growth region due to rising disposable incomes and a burgeoning interest in organic and healthy lifestyles, with China and Japan leading the way in adoption and imports.

Q4: What are the main challenges faced by organic wine producers?

Organic wine producers face several key challenges, including higher production costs due to increased manual labor and strict input restrictions, often resulting in higher retail prices. The limited availability of certified organic grapes and the lengthy, rigorous conversion period for vineyards also pose significant supply constraints. Furthermore, the organic wine market experiences strong competition from the larger, more established conventional wine sector, necessitating effective differentiation and marketing. Finally, the unpredictability of climate change, with its impact on grape yields and quality, presents an ongoing environmental challenge for organic viticulture.

Q5: How is technology impacting the organic wine industry?

Technology is profoundly impacting the organic wine industry by enhancing efficiency, sustainability, and quality. AI-driven precision viticulture enables optimized resource management, disease prediction, and improved grape quality through data analysis, reducing the need for synthetic interventions crucial for organic certification. Blockchain technology is being explored to enhance supply chain transparency and combat fraud, ensuring the authenticity of organic claims. Furthermore, advancements in sustainable winemaking equipment and alternative energy solutions are helping producers reduce their environmental footprint, aligning with organic principles. Digital platforms and e-commerce innovations are also expanding market reach and facilitating direct consumer engagement for organic wine brands.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted