Offshore Wind Cable Market

Offshore Wind Cable Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700346 | Last Updated : July 24, 2025 |

Format : ![]()

![]()

![]()

![]()

Offshore Wind Cable Market Size

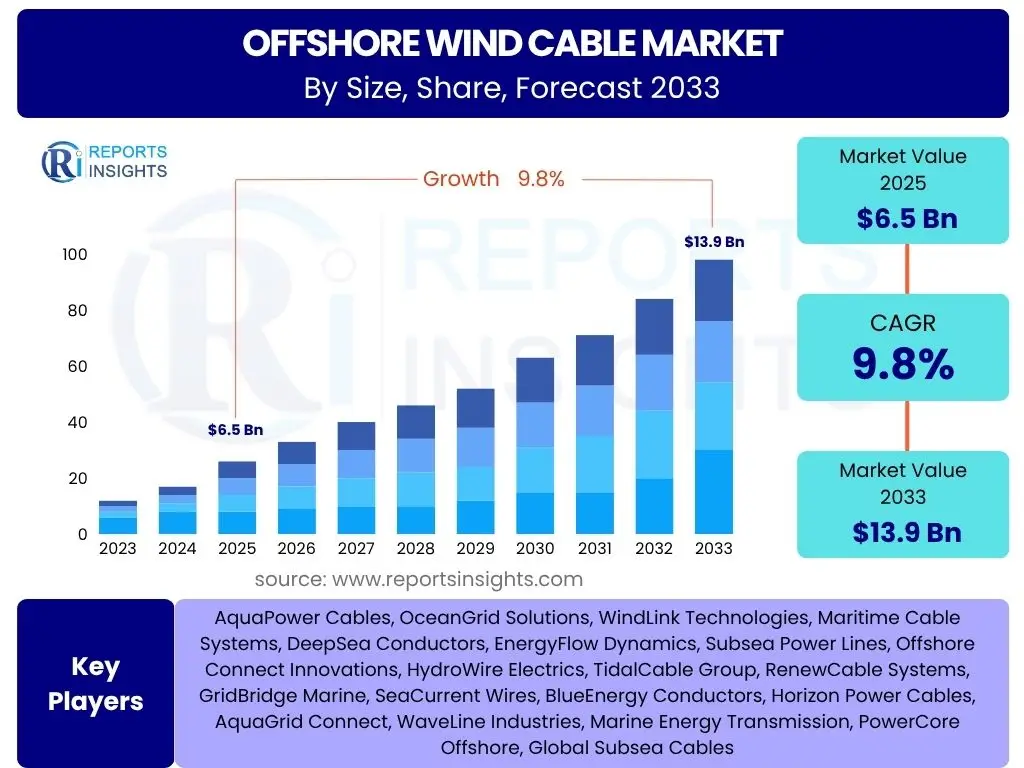

The Offshore Wind Cable Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033, valued at USD 6.5 billion in 2025, and is projected to reach USD 13.9 billion by 2033, at the end of the forecast period. This significant growth is driven by the escalating global demand for renewable energy sources and the continuous expansion of offshore wind farm installations. The increasing investments in offshore wind infrastructure across various regions, coupled with advancements in cable technology, are further bolstering market expansion and solidifying its pivotal role in the global energy transition.

Key Offshore Wind Cable Market Trends & Insights

The offshore wind cable market is experiencing dynamic shifts, influenced by technological innovation, policy frameworks, and evolving energy demands. Key trends shaping this sector include:

- Increasing adoption of High Voltage Direct Current (HVDC) cables for long-distance power transmission from large-scale offshore wind farms due to lower losses and higher efficiency.

- Growing focus on developing and deploying floating offshore wind technologies, which necessitate specialized dynamic cable solutions capable of withstanding constant movement and harsh marine conditions.

- Development of smart cable monitoring systems incorporating fiber optics and sensors for real-time performance tracking, fault detection, and predictive maintenance, enhancing operational efficiency and reliability.

- Rising demand for superconducting cables as a potential future solution to minimize transmission losses and enable even higher power capacities, although currently in research and development phases.

- Emphasis on sustainable and environmentally friendly cable materials and installation methods to reduce ecological impact and adhere to stricter environmental regulations.

- Strategic partnerships and collaborations among cable manufacturers, wind farm developers, and grid operators to optimize project execution, share expertise, and accelerate innovation in cable technology and deployment.

- Standardization efforts in cable design and manufacturing processes aimed at reducing costs, improving interoperability, and streamlining procurement for large-scale offshore wind projects.

- Geographical expansion beyond traditional European markets, with significant growth projected in Asia Pacific, particularly China, Taiwan, and South Korea, and emerging opportunities in North America.

- Integration of digital twin technologies for lifecycle management of offshore wind cables, enabling virtual simulations for design optimization, installation planning, and ongoing operational monitoring.

AI Impact Analysis on Offshore Wind Cable

Artificial Intelligence (AI) is set to significantly transform the offshore wind cable market by enhancing various operational aspects, from design and manufacturing to installation and maintenance. AI-driven predictive analytics can forecast cable degradation, identify potential failure points, and optimize maintenance schedules, thereby reducing downtime and extending cable lifespan. Furthermore, AI algorithms can analyze vast datasets from subsea surveys and environmental conditions to optimize cable routing, minimizing installation risks and costs while improving overall project efficiency.

- AI-powered predictive maintenance for proactive fault detection and lifespan extension of subsea cables.

- Optimization of cable laying routes using AI to minimize environmental impact and installation costs.

- Enhanced real-time monitoring of cable performance and integrity through AI-driven sensor data analysis.

- AI integration in automated inspection and repair vehicles for efficient subsea operations.

- Advanced material development for cables using AI for novel material discovery and performance simulation.

Key Takeaways Offshore Wind Cable Market Size & Forecast

- The Offshore Wind Cable Market is poised for substantial growth, projecting a near doubling in market size from 2025 to 2033.

- The market is underpinned by aggressive global renewable energy targets and the expansion of offshore wind capacities.

- Technological advancements, especially in HVDC and dynamic cable systems, are crucial enablers of market growth.

- AI integration is expected to revolutionize cable lifecycle management, from design to predictive maintenance.

- Key growth drivers include governmental support, decreasing Levelized Cost of Energy (LCOE) for offshore wind, and increasing energy demand.

- Challenges such as high capital expenditure and complex installation logistics require continuous innovation and strategic solutions.

- Opportunities are emerging in floating offshore wind, grid modernization, and market expansion into new geographical regions.

- Sustainability and environmental considerations are increasingly influencing cable material selection and installation methodologies.

Offshore Wind Cable Market Drivers Analysis

The expansion of the offshore wind cable market is primarily propelled by a confluence of robust drivers, reflecting the global commitment to sustainable energy and the inherent advantages of offshore wind power. These drivers span from supportive governmental policies and ambitious renewable energy targets to significant technological advancements that enhance efficiency and reduce costs. The increasing global energy demand, coupled with the depleting fossil fuel reserves, further solidifies the long-term growth trajectory of offshore wind, thereby stimulating demand for advanced cable infrastructure. Moreover, the falling Levelized Cost of Energy (LCOE) for offshore wind projects makes them increasingly competitive against traditional power sources, attracting greater investment and accelerating project development worldwide.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Renewable Energy Targets: Governments worldwide are setting ambitious renewable energy targets to combat climate change and reduce carbon emissions, driving significant investment in offshore wind projects, which directly increases the demand for high-capacity subsea cables. | +3.5% | Europe, Asia Pacific (China, South Korea, Taiwan), North America (US, UK) | Long-term (2025-2033) |

| Technological Advancements in Cable Manufacturing: Innovations in materials, design, and manufacturing processes for offshore wind cables, including the development of High Voltage Direct Current (HVDC) systems and dynamic cables for floating wind, are improving efficiency, reducing losses, and enabling longer transmission distances, thus making offshore wind more viable. | +2.8% | Global, especially Europe (Germany, Norway), Japan, US | Mid-term (2025-2030) |

| Supportive Government Policies & Regulations: Favorable policies, subsidies, tax incentives, and regulatory frameworks, such as feed-in tariffs, auctions, and offshore wind development zones, are instrumental in de-risking investments and attracting project developers, directly stimulating the construction of new offshore wind farms and associated cable infrastructure. | +2.3% | Europe (UK, Denmark, Germany), US (East Coast), Asia (China, Vietnam) | Short to Mid-term (2025-2028) |

| Decreasing Levelized Cost of Energy (LCOE) for Offshore Wind: Continuous reductions in the LCOE of offshore wind power, driven by economies of scale, improved technology, and optimized project execution, are making it increasingly competitive with conventional energy sources, leading to accelerated adoption and expansion of offshore wind projects globally. | +1.2% | Global, particularly competitive markets like Europe and US | Mid to Long-term (2027-2033) |

| Grid Modernization and Interconnectivity Needs: As more renewable energy sources are integrated into national grids, there is a growing need for robust and efficient transmission infrastructure to handle intermittent power generation and ensure grid stability. Offshore wind cables are critical components in these grid modernization efforts, facilitating cross-border energy transfer. | +1.0% | Europe (Nordic Grid, North Sea Grid), North America, East Asia | Long-term (2028-2033) |

Offshore Wind Cable Market Restraints Analysis

Despite its significant growth potential, the offshore wind cable market faces several substantial restraints that could impede its rapid expansion. These challenges primarily revolve around the immense capital expenditure required for project development, the complex and high-risk nature of offshore installation and maintenance operations, and the intricate regulatory and environmental hurdles. Furthermore, supply chain bottlenecks for specialized components and skilled labor shortages can also create delays and increase project costs. Addressing these restraints effectively requires sustained innovation in technology, strategic investment frameworks, and harmonized international cooperation to streamline development processes and mitigate risks across the value chain.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure (CAPEX): The initial investment required for manufacturing, purchasing, and installing high-voltage subsea cables, especially for large-scale offshore wind farms, is exceptionally high, posing a significant financial barrier for new market entrants and smaller developers. | -1.8% | Global, especially emerging markets | Short to Mid-term (2025-2029) |

| Complex Installation and Maintenance Challenges: Deploying and maintaining offshore wind cables in harsh marine environments involves significant technical complexities, specialized vessels, and skilled personnel. Adverse weather conditions, seabed topography, and unforeseen geological challenges can lead to delays and increased operational costs. | -1.5% | Global, particularly deep-water projects | Ongoing |

| Regulatory and Environmental Permitting Delays: Obtaining the necessary permits and approvals for offshore cable routes can be a lengthy and intricate process due to environmental impact assessments, stakeholder consultations, and conflicting interests with other marine activities (e.g., fishing, shipping, defense), causing project delays. | -1.0% | Europe (North Sea), US (East and West Coast), Asia (Japan, South Korea) | Short to Mid-term (2025-2028) |

| Supply Chain Constraints and Geopolitical Risks: The specialized nature of offshore cables means a limited number of global manufacturers, leading to potential supply chain bottlenecks, long lead times, and vulnerability to geopolitical disruptions, which can affect project schedules and costs. | -0.7% | Global, impacting key manufacturing regions | Short-term (2025-2026) |

Offshore Wind Cable Market Opportunities Analysis

The offshore wind cable market is ripe with opportunities that could significantly accelerate its growth trajectory. The most prominent among these is the burgeoning field of floating offshore wind technology, which opens up vast new areas for development in deeper waters, beyond the traditional fixed-bottom installations. Additionally, the increasing focus on developing supergrids and interconnections between national grids creates demand for advanced, long-distance subsea cables. Furthermore, the adoption of smart grid technologies and digitalization in offshore wind farms presents opportunities for integrating intelligent cable monitoring and management systems, enhancing operational efficiency and reliability. The growing demand for green hydrogen production offshore could also lead to new applications for power export cables, connecting electrolysers directly to wind farms.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Floating Offshore Wind Farms: Floating offshore wind technology unlocks vast deep-water areas previously inaccessible to fixed-bottom turbines, creating new markets for dynamic cables capable of handling movement and extreme conditions, significantly expanding the addressable market for cable manufacturers. | +2.0% | Europe (Norway, UK), Japan, US (West Coast), South Korea | Mid to Long-term (2028-2033) |

| Emergence of Offshore Energy Hubs & Grids: The concept of integrated offshore energy hubs and multi-country supergrids, aimed at efficiently transmitting large volumes of renewable energy across borders, presents a substantial opportunity for high-capacity, long-distance HVDC interconnector cables and related infrastructure. | +1.5% | Europe (North Sea, Baltic Sea), Asia (East Asia grids) | Long-term (2030-2033) |

| Retrofitting and Upgrading Existing Grid Infrastructure: As older offshore wind farms mature, there will be opportunities for replacing or upgrading existing inter-array and export cables with newer, more efficient, and higher-capacity solutions to extend asset life and improve power transmission. | +0.9% | Europe (mature markets like UK, Denmark, Germany) | Mid to Long-term (2027-2033) |

| Integration with Green Hydrogen Production Offshore: The potential for co-locating offshore wind farms with green hydrogen electrolysers presents a new application area for power cables, facilitating the direct supply of renewable electricity for hydrogen production, which can then be transported via pipeline or vessel. | +0.7% | Europe (Netherlands, Germany), Australia | Long-term (2030-2033) |

Offshore Wind Cable Market Challenges Impact Analysis

The offshore wind cable market confronts distinct challenges that necessitate innovative solutions and strategic foresight. Beyond the aforementioned high capital costs and installation complexities, ensuring the long-term reliability and resilience of cables in corrosive marine environments remains a significant technical hurdle. The sheer scale and remoteness of many offshore projects exacerbate logistics and maintenance issues, making swift repairs challenging. Furthermore, the global competition for seabed usage, coupled with evolving environmental protection mandates, adds layers of complexity to project planning and execution. Overcoming these challenges will require continuous investment in research and development, robust risk management strategies, and collaborative efforts across the industry to develop more durable, cost-effective, and environmentally compliant cable solutions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring Long-term Reliability and Durability: Offshore cables are exposed to harsh marine conditions, including saltwater corrosion, strong currents, and potential damage from marine life or anchors. Ensuring their long-term reliability and durability over a 20-30 year lifespan without frequent failures is a significant technical challenge. | -1.2% | Global, especially challenging environments | Ongoing |

| Logistical Complexities in Remote Offshore Locations: The increasing distance of offshore wind farms from shore means greater logistical complexities for cable transport, laying, and maintenance operations. This necessitates larger and more specialized vessels, increasing costs and extending project timelines. | -0.8% | Global, particularly far-shore projects | Ongoing |

| Grid Congestion and Connection Delays: In some regions, the existing onshore grid infrastructure may not be adequately prepared to handle the large influx of power from new offshore wind farms. This can lead to grid congestion issues and delays in connecting offshore projects to the national grid, impacting project viability. | -0.6% | Europe (North Sea), US (Northeast), UK | Mid-term (2026-2030) |

| Shortage of Skilled Workforce and Specialized Vessels: The rapid expansion of the offshore wind sector creates a high demand for a specialized workforce (e.g., cable engineers, installation technicians) and dedicated offshore vessels. A global shortage in these areas can lead to project delays and increased labor costs. | -0.5% | Global, particularly in emerging markets | Ongoing |

Offshore Wind Cable Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the global Offshore Wind Cable Market, providing critical insights into its current landscape, historical performance, and future growth trajectory. It covers market size estimations, growth drivers, restraints, opportunities, and challenges, along with detailed segmentation analysis and regional breakdowns. The report also includes a competitive landscape assessment, profiling key industry players and their strategic initiatives, enabling stakeholders to make informed business decisions and capitalize on emerging market trends.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.5 billion |

| Market Forecast in 2033 | USD 13.9 billion |

| Growth Rate | 9.8% CAGR from 2025 to 2033 |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | AquaPower Cables, OceanGrid Solutions, WindLink Technologies, Maritime Cable Systems, DeepSea Conductors, EnergyFlow Dynamics, Subsea Power Lines, Offshore Connect Innovations, HydroWire Electrics, TidalCable Group, RenewCable Systems, GridBridge Marine, SeaCurrent Wires, BlueEnergy Conductors, Horizon Power Cables, AquaGrid Connect, WaveLine Industries, Marine Energy Transmission, PowerCore Offshore, Global Subsea Cables |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Offshore Wind Cable Market is meticulously segmented to provide a granular understanding of its diverse components and dynamics. This segmentation facilitates a detailed analysis of market performance across various parameters, offering actionable insights for stakeholders. The key segments include cable type, voltage level, application, and installation depth, each playing a crucial role in the overall market landscape and future development trajectories of offshore wind energy.

- By Type:

- Inter-array Cables: These cables connect individual wind turbines within an offshore wind farm to a common offshore substation. They typically operate at lower to medium voltages and are designed for robustness to withstand turbine movements and seabed conditions.

- Export Cables: These are critical for transmitting the aggregated power from the offshore substation to the onshore grid.

- HVAC (High Voltage Alternating Current): Used for shorter distances, typically up to 80-100 km, due to reactive power losses over longer runs. They are cost-effective for near-shore projects.

- HVDC (High Voltage Direct Current): Preferred for longer distances and larger power capacities, HVDC cables minimize transmission losses and are increasingly vital for far-shore and multi-gigawatt projects, offering superior efficiency and stability.

- By Voltage: This segmentation reflects the power transmission capacity and application of the cables.

- Low Voltage (LV): Primarily used for auxiliary systems and internal connections within turbine components.

- Medium Voltage (MV): Common for inter-array cables connecting turbines within a wind farm.

- High Voltage (HV): Used for some inter-array systems and shorter export cables.

- Extra-High Voltage (EHV): Predominantly used for long-distance export cables, especially HVDC systems, to transmit large amounts of power with minimal losses.

- By Application: This category differentiates cable usage based on the foundation type of the wind farm.

- Fixed-Bottom Offshore Wind Farms: Cables designed for traditional wind farms where turbines are fixed to the seabed, requiring static cable solutions.

- Floating Offshore Wind Farms: A rapidly emerging segment requiring specialized dynamic cables that can flex and move with the floating structures, adapting to continuous motion and environmental forces.

- By Depth: This segmentation considers the installation environment and the specific demands placed on the cables.

- Shallow Water Installations: Cables designed for relatively shallower depths, often closer to shore, with simpler installation requirements.

- Deep Water Installations: Cables engineered for greater depths, demanding higher mechanical strength, specialized laying techniques, and advanced protection against extreme pressures and currents.

Regional Highlights

The global Offshore Wind Cable Market exhibits significant regional variations in terms of maturity, growth drivers, and market opportunities. Europe remains the pioneering and leading market, while Asia Pacific is emerging as the fastest-growing region, and North America is positioned for substantial future expansion. Each region presents a unique landscape shaped by governmental policies, resource availability, and technological adoption.

- Europe: Europe stands as the undisputed leader in the offshore wind cable market, largely due to its early adoption of offshore wind technology, ambitious renewable energy targets, and extensive installed capacity. Countries like the United Kingdom, Germany, Denmark, and the Netherlands have well-established offshore wind industries, driving continuous demand for inter-array and export cables. The region is also at the forefront of developing interconnected offshore grids and exploring floating wind solutions, necessitating advanced HVDC and dynamic cables. Supportive policies, mature supply chains, and significant investment in R&D contribute to its dominant position and sustained growth.

- Asia Pacific (APAC): The APAC region is experiencing the most rapid growth in the offshore wind cable market, primarily driven by China, Taiwan, South Korea, and emerging markets like Vietnam and Japan. China leads global installations, propelled by massive domestic energy demand and strong governmental support for renewable energy. Taiwan and South Korea are rapidly expanding their offshore wind capacities, attracting significant foreign investment and technological expertise. This region's growth is characterized by large-scale projects, increasing adoption of HVDC for longer transmission distances, and a burgeoning domestic manufacturing base for cables and components.

- North America: The North American market, particularly the United States, is poised for significant expansion in offshore wind, albeit from a smaller base. The U.S. East Coast is a key focus area, with states like New York, New Jersey, and Massachusetts setting ambitious offshore wind targets and investing heavily in port infrastructure and supply chain development. The market here is driven by federal and state-level renewable energy mandates, the availability of strong wind resources, and the need for reliable power in coastal urban centers. As projects move forward, the demand for both inter-array and export cables, including HVDC systems, is expected to surge, with particular attention to environmental permitting and stakeholder engagement.

- Latin America, Middle East, and Africa (LAMEA): While still in nascent stages, the LAMEA region presents long-term potential for the offshore wind cable market. Countries with suitable coastlines and significant wind resources, such as Brazil in Latin America and South Africa in Africa, are exploring initial offshore wind projects. The Middle East is also showing nascent interest in renewable energy diversification. Market development in these regions will be contingent on the establishment of clear regulatory frameworks, infrastructure development, and attracting international investment, creating future opportunities for cable suppliers as these markets mature.

Top Key Players:

The market research report covers the analysis of key stakeholders of the Offshore Wind Cable Market. Some of the leading players profiled in the report include -- AquaPower Cables

- OceanGrid Solutions

- WindLink Technologies

- Maritime Cable Systems

- DeepSea Conductors

- EnergyFlow Dynamics

- Subsea Power Lines

- Offshore Connect Innovations

- HydroWire Electrics

- TidalCable Group

- RenewCable Systems

- GridBridge Marine

- SeaCurrent Wires

- BlueEnergy Conductors

- Horizon Power Cables

- AquaGrid Connect

- WaveLine Industries

- Marine Energy Transmission

- PowerCore Offshore

- Global Subsea Cables

Frequently Asked Questions:

1. What is the projected growth of the Offshore Wind Cable Market?

The Offshore Wind Cable Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. It is valued at USD 6.5 billion in 2025 and is forecasted to reach USD 13.9 billion by 2033, driven by increasing global investments in offshore wind energy and advancements in cable technology.2. What are the primary drivers accelerating the Offshore Wind Cable Market?

Key drivers include increasing global renewable energy targets, significant technological advancements in cable manufacturing (especially HVDC and dynamic cables), supportive government policies and regulations for offshore wind development, and the decreasing Levelized Cost of Energy (LCOE) for offshore wind power, making it more competitive.3. How does AI influence the Offshore Wind Cable Market?

Artificial Intelligence (AI) impacts the Offshore Wind Cable Market by enabling advanced predictive maintenance for proactive fault detection, optimizing cable laying routes to reduce costs and environmental impact, and enhancing real-time monitoring of cable performance. AI also supports the development of new materials and automated inspection processes.4. What are the key challenges facing the Offshore Wind Cable Market?

Major challenges include the exceptionally high capital expenditure required for projects, the complex and risky nature of offshore installation and maintenance, potential delays from stringent regulatory and environmental permitting processes, and supply chain constraints coupled with a shortage of skilled labor and specialized vessels.5. Which regions are leading the growth in the Offshore Wind Cable Market?

Europe currently leads the Offshore Wind Cable Market due to its mature industry and ambitious renewable goals. However, the Asia Pacific region, particularly China, Taiwan, and South Korea, is experiencing the fastest growth. North America, especially the United States, is also poised for significant future expansion driven by new offshore wind projects and supportive policies.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted