Hydrofluoroolefin Market

Hydrofluoroolefin Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709142 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

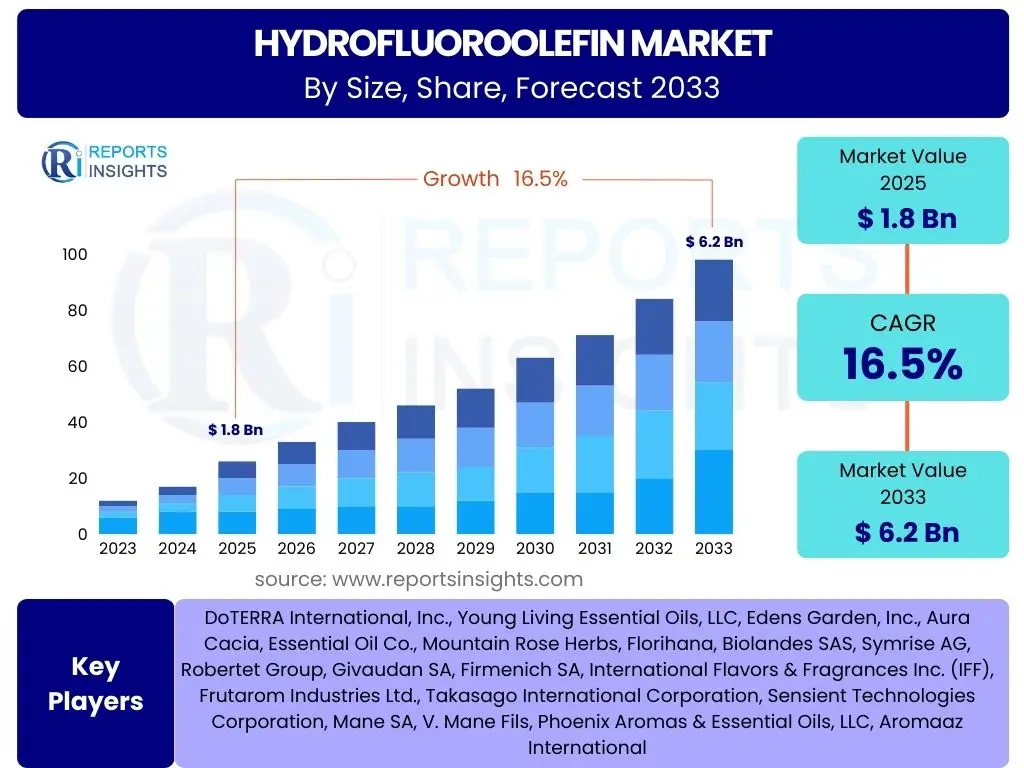

Hydrofluoroolefin Market Size

According to Reports Insights Consulting Pvt Ltd, The Hydrofluoroolefin Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 16.5% between 2025 and 2033. The market is estimated at USD 1.8 Billion in 2025 and is projected to reach USD 6.2 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by the escalating global focus on environmental sustainability and stringent regulatory frameworks mandating the phase-down of high Global Warming Potential (GWP) hydrofluorocarbons (HFCs), positioning HFOs as indispensable next-generation alternatives across a multitude of applications.

Key Hydrofluoroolefin Market Trends & Insights

Common user inquiries regarding Hydrofluoroolefin market trends frequently revolve around the industry's response to environmental mandates, the adoption rates across various applications, and technological advancements. The overarching trend indicates a significant shift towards low GWP solutions, with HFOs at the forefront. Insights suggest that market players are heavily investing in R&D to optimize HFO formulations for specific uses, enhance energy efficiency, and improve overall cost-effectiveness. Furthermore, the integration of HFOs into existing infrastructure, particularly in the automotive and HVACR sectors, represents a critical area of ongoing development and market expansion.

- Accelerated transition from high GWP HFCs to low GWP HFOs driven by global environmental regulations such as the Kigali Amendment and regional policies.

- Increasing adoption of HFO-1234yf in automotive air conditioning systems as a standard refrigerant due to its ultra-low GWP.

- Expansion of HFO applications beyond traditional refrigeration and air conditioning, including foam blowing, aerosol propellants, solvents, and medical devices.

- Growing emphasis on developing HFO blends and mixtures to achieve optimal performance characteristics (e.g., flammability, energy efficiency, capacity) for diverse end-use needs.

- Rising investment in research and development activities to discover novel HFO compounds and optimize production processes, aiming for enhanced sustainability and cost efficiency.

AI Impact Analysis on Hydrofluoroolefin

User questions related to the impact of AI on the Hydrofluoroolefin sector often explore how artificial intelligence can optimize manufacturing, facilitate new product development, and streamline supply chains. AI's influence is anticipated to be transformative, primarily through enhanced predictive analytics for demand forecasting, which can mitigate supply chain volatilities inherent in the chemical industry. Moreover, AI-driven simulations and machine learning algorithms are increasingly being deployed in the R&D phase to accelerate the discovery of novel HFO compounds with improved properties and lower environmental footprints, significantly reducing the time and cost associated with traditional experimentation.

- AI-driven optimization of HFO production processes, leading to increased efficiency, reduced waste, and lower energy consumption in manufacturing plants.

- Enhanced predictive maintenance for HFO production equipment, minimizing downtime and extending asset lifespans through real-time data analysis.

- Accelerated discovery and development of new HFO formulations using AI and machine learning algorithms to screen potential molecules and predict their properties and environmental impact.

- Improved supply chain management and logistics for HFOs through AI-powered demand forecasting, inventory optimization, and route planning, ensuring timely delivery and reducing operational costs.

- Data analytics and AI applications in market trend analysis and competitive intelligence, enabling companies to identify emerging opportunities and challenges within the HFO sector with greater precision.

Key Takeaways Hydrofluoroolefin Market Size & Forecast

Key takeaways from the Hydrofluoroolefin market size and forecast consistently highlight the market's robust growth trajectory, fundamentally driven by regulatory pressures and the imperative for sustainable chemical alternatives. Users frequently seek concise understanding of the market's core growth catalysts and its future trajectory. The forecast underscores HFOs as a critical component in the global effort to combat climate change, with substantial market expansion anticipated across various industrial applications. Strategic investments in innovation and expanding production capacities are crucial for stakeholders aiming to capitalize on this evolving market landscape.

- The Hydrofluoroolefin market is poised for significant expansion, projecting a CAGR of 16.5% from 2025 to 2033, driven predominantly by environmental regulations.

- Global demand for low GWP refrigerants, foam blowing agents, and propellants is the primary catalyst for market growth, establishing HFOs as indispensable replacements for HFCs.

- Automotive air conditioning and stationary refrigeration are expected to remain key application segments, with increasing penetration of HFOs in new equipment and retrofits.

- Asia Pacific is anticipated to emerge as a leading growth region, fueled by rapid industrialization, increasing disposable income, and the gradual adoption of environmental standards.

- Strategic collaborations, technological advancements, and expansion of production capacities will be critical success factors for market participants to meet the escalating demand for HFOs.

Hydrofluoroolefin Market Drivers Analysis

The Hydrofluoroolefin market is primarily propelled by a confluence of environmental regulations and increasing global awareness regarding climate change. Governments and international bodies worldwide are enacting stricter mandates to phase down high Global Warming Potential (GWP) substances like hydrofluorocarbons (HFCs), compelling industries to adopt more environmentally benign alternatives. This regulatory pressure, coupled with a growing corporate commitment to sustainability and energy efficiency, creates a strong impetus for the adoption of HFOs across diverse applications, from refrigeration and air conditioning to foam blowing and aerosols. The superior environmental profile of HFOs, characterized by ultra-low GWP and zero ozone depletion potential (ODP), positions them as the preferred choice for future-proof solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations (e.g., Kigali Amendment, F-Gas Regulation) | +5.0% - +6.5% | Global, particularly Europe, North America, Japan, China | Short to Long-Term (2025-2033) |

| Growing Demand for Low GWP Refrigerants and Blowing Agents | +4.5% - +5.5% | Global, all major economies | Short to Mid-Term (2025-2029) |

| Increasing Adoption in Automotive Air Conditioning Systems | +3.0% - +4.0% | North America, Europe, Asia Pacific (China, India) | Mid-Term (2027-2031) |

| Focus on Energy Efficiency in HVACR Systems | +2.0% - +3.0% | Global, developed and emerging economies | Mid to Long-Term (2028-2033) |

| Innovation and Development of New HFO Applications | +1.5% - +2.5% | Global, R&D intensive regions (US, EU, Japan) | Long-Term (2030-2033) |

Hydrofluoroolefin Market Restraints Analysis

Despite significant growth prospects, the Hydrofluoroolefin market faces several notable restraints that could temper its expansion. One primary concern is the relatively higher cost of HFOs compared to the HFCs they are designed to replace. This cost disparity can hinder widespread adoption, particularly in price-sensitive emerging markets where budget constraints often dictate purchasing decisions. Furthermore, the limited availability of certain raw materials and the complex manufacturing processes for HFOs can lead to supply chain vulnerabilities and impact production scalability. Patent protections surrounding key HFO technologies also contribute to higher costs and limit market entry for new players, potentially stifling competition and innovation in specific segments. Addressing these economic and logistical challenges is crucial for sustained market penetration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Production Costs and Pricing of HFOs compared to HFCs | -3.0% - -4.5% | Global, particularly emerging economies | Short to Mid-Term (2025-2029) |

| Complex Manufacturing Processes and Limited Raw Material Availability | -2.0% - -3.5% | Global, concentrated supply chains | Short to Mid-Term (2025-2028) |

| Existing Infrastructure and Equipment Compatibility Issues | -1.5% - -2.5% | Global, especially developed markets with established systems | Mid-Term (2027-2031) |

| Patent Landscape and Intellectual Property Barriers | -1.0% - -2.0% | Global, particularly for key patented compounds | Long-Term (2029-2033) |

Hydrofluoroolefin Market Opportunities Analysis

The Hydrofluoroolefin market presents significant opportunities for innovation and expansion, particularly driven by the continuous global shift towards sustainable solutions. The development of next-generation HFO formulations with enhanced performance characteristics, such as improved energy efficiency and broader application compatibility, represents a key growth avenue. Furthermore, the increasing demand for eco-friendly solutions in developing economies, coupled with growing industrialization and urbanization, offers vast untapped markets. Collaborations between chemical manufacturers, equipment providers, and end-use industries can accelerate the adoption of HFO technology and streamline market penetration. Opportunities also lie in the recycling and reclamation of HFOs, supporting circular economy principles and extending the lifecycle of these valuable chemicals, thereby reducing overall environmental impact and potentially creating new revenue streams.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of New HFO Blends and Next-Generation Formulations | +4.0% - +5.5% | Global, especially in R&D hubs | Mid to Long-Term (2027-2033) |

| Expansion into Emerging Economies (e.g., India, Southeast Asia, Latin America) | +3.5% - +4.5% | Asia Pacific, Latin America, Middle East & Africa | Short to Long-Term (2025-2033) |

| Growing Demand for HFOs in Niche and Specialized Applications (e.g., Medical, Electronics) | +2.5% - +3.5% | Global, particularly developed markets | Mid-Term (2028-2032) |

| Advancements in HFO Recycling and Reclamation Technologies | +1.5% - +2.5% | Global, developed economies with strong recycling infrastructure | Long-Term (2030-2033) |

Hydrofluoroolefin Market Challenges Impact Analysis

The Hydrofluoroolefin market, while promising, is not without its challenges. One significant hurdle is the ongoing regulatory uncertainty and the evolving nature of environmental policies, which can create unpredictability for manufacturers and end-users alike. This dynamic landscape requires continuous adaptation and substantial investment in compliance. Additionally, the market faces competition from alternative technologies, including natural refrigerants (such as CO2, ammonia, and hydrocarbons) and other non-fluorinated solutions, which may offer different cost-benefit profiles in specific applications. Managing the high initial investment required for HFO production facilities and navigating complex global supply chains for specialized raw materials also present formidable challenges. Addressing these complexities effectively is crucial for maintaining market momentum and ensuring long-term viability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Regulatory Uncertainty and Evolving Environmental Policies | -2.5% - -4.0% | Global, high impact in Europe and North America | Short to Mid-Term (2025-2029) |

| Competition from Natural Refrigerants and Other Alternatives | -2.0% - -3.0% | Global, particularly for specific application niches | Mid-Term (2027-2031) |

| High Capital Investment for HFO Production Facilities | -1.5% - -2.5% | Global, primarily for new market entrants or capacity expansions | Short-Term (2025-2027) |

| Supply Chain Volatility and Raw Material Price Fluctuations | -1.0% - -2.0% | Global, impacting manufacturing regions | Short to Mid-Term (2025-2028) |

Hydrofluoroolefin Market - Updated Report Scope

This report provides an in-depth analysis of the global Hydrofluoroolefin market, offering comprehensive insights into market dynamics, segmentation, regional trends, and competitive landscape. It covers historical data from 2019 to 2023, along with a detailed forecast for the period 2025-2033, enabling stakeholders to make informed strategic decisions. The scope includes a thorough examination of market drivers, restraints, opportunities, and challenges, alongside an assessment of key market players and their strategies to navigate the evolving industry. Special attention is given to the impact of regulatory changes and technological advancements shaping the market's future.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.8 Billion |

| Market Forecast in 2033 | USD 6.2 Billion |

| Growth Rate | 16.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Chemours, Honeywell International Inc., Arkema S.A., Daikin Industries, Ltd., Orbia (Mexichem, Koura Global), AGC Inc., Linde plc, Sanofi, Shandong Dongyue Chemical Co., Ltd., Haltermann Carless, Merck KGaA, Sinochem Group, Gujarat Fluorochemicals Limited (GFL), Fuburg Industrial Co., Ltd., Zhejiang Sanmei Chemical Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Hydrofluoroolefin market is extensively segmented to provide a granular view of its diverse landscape, enabling a deeper understanding of specific market dynamics and growth opportunities. These segmentations are critical for stakeholders to identify key areas of investment, target markets, and competitive positioning. The categorization by product type differentiates the various HFO compounds, each with unique properties and applications, while segmentation by application highlights their utility across a broad spectrum of industries. Furthermore, an end-use industry breakdown offers insights into how different sectors are integrating HFO technology into their operations, providing a comprehensive framework for market analysis and strategic planning.

- By Product Type:

- HFO-1234yf

- HFO-1234ze

- HFO-1336mzz

- Others (e.g., HFO-1430e)

- By Application:

- Refrigeration (Commercial Refrigeration, Industrial Refrigeration)

- Air Conditioning (Mobile Air Conditioning, Stationary Air Conditioning)

- Foam Blowing Agents (Polyurethane Foams, Polystyrene Foams)

- Aerosols (Medical Aerosols, Technical Aerosols)

- Solvents

- Medical Propellants

- Fire Suppression

- By End-Use Industry:

- Automotive

- HVACR (Heating, Ventilation, Air Conditioning, and Refrigeration)

- Building & Construction

- Healthcare

- Electronics

- Industrial

Regional Highlights

- North America: A significant early adopter of HFOs, particularly in the automotive sector due to stringent environmental regulations and the presence of major HFO manufacturers and technology innovators. The region continues to drive demand through ongoing HFC phase-down initiatives.

- Europe: Leads the world in HFO adoption, primarily propelled by the ambitious F-Gas Regulation which mandates a substantial reduction in fluorinated gas emissions. This has accelerated the transition to low GWP refrigerants and blowing agents across industrial, commercial, and automotive applications.

- Asia Pacific (APAC): Emerging as the fastest-growing region for HFOs, driven by rapid industrialization, urbanization, increasing demand for air conditioning and refrigeration, and the gradual implementation of environmental policies in countries like China, India, and Japan. Significant manufacturing capacities are also being established here.

- Latin America: Expected to witness steady growth as environmental awareness increases and regional regulations align with global standards. Brazil and Mexico are key markets due to their expanding automotive and HVACR industries.

- Middle East & Africa (MEA): Represents a nascent but growing market for HFOs, particularly in urban centers and for large-scale infrastructure projects requiring efficient cooling solutions. Adoption is influenced by economic development and the increasing focus on sustainable technologies.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Hydrofluoroolefin Market.- Chemours

- Honeywell International Inc.

- Arkema S.A.

- Daikin Industries, Ltd.

- Orbia

- AGC Inc.

- Linde plc

- Sanofi

- Shandong Dongyue Chemical Co., Ltd.

- Haltermann Carless

- Merck KGaA

- Sinochem Group

- Gujarat Fluorochemicals Limited (GFL)

- Fuburg Industrial Co., Ltd.

- Zhejiang Sanmei Chemical Co., Ltd.

Frequently Asked Questions

What are Hydrofluoroolefins (HFOs)?

Hydrofluoroolefins (HFOs) are a class of unsaturated organic compounds composed of hydrogen, fluorine, and carbon. They are characterized by their ultra-low Global Warming Potential (GWP) and zero Ozone Depletion Potential (ODP), making them environmentally superior alternatives to traditional hydrofluorocarbons (HFCs) and chlorofluorocarbons (CFCs) in various applications such as refrigerants, blowing agents, and propellants.

Why are HFOs replacing HFCs in many applications?

HFOs are replacing HFCs primarily due to stringent environmental regulations and international agreements like the Kigali Amendment, which mandate the phase-down of high GWP substances. HFCs, while not ozone-depleting, contribute significantly to global warming. HFOs offer similar performance characteristics to HFCs but with GWP values often less than 1, making them a sustainable and compliant choice for industries seeking to reduce their carbon footprint.

What are the primary applications of HFOs?

The primary applications of HFOs include refrigerants in automotive air conditioning (e.g., HFO-1234yf) and stationary refrigeration/air conditioning systems (e.g., HFO-1234ze). They are also widely used as foam blowing agents in the insulation industry, aerosol propellants, solvents, and increasingly in specialized applications such as medical propellants and fire suppression systems, due to their favorable environmental and safety profiles.

What are the key drivers for the growth of the HFO market?

The key drivers for the HFO market's growth are stringent global environmental regulations aimed at phasing down high GWP substances, increasing demand for energy-efficient cooling solutions, growing adoption in the automotive sector, and rising consumer and corporate awareness of sustainability. These factors collectively push industries towards adopting low GWP alternatives like HFOs across various end-use segments.

What are the main challenges facing the Hydrofluoroolefin market?

The main challenges facing the Hydrofluoroolefin market include the higher initial cost of HFOs compared to older alternatives, the complexity of manufacturing processes, and potential raw material supply chain volatilities. Additionally, competition from natural refrigerants and other emerging low GWP technologies, alongside the need for significant capital investment in new production facilities, also pose considerable challenges for market expansion.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted