Industrial Camera Market

Industrial Camera Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708200 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

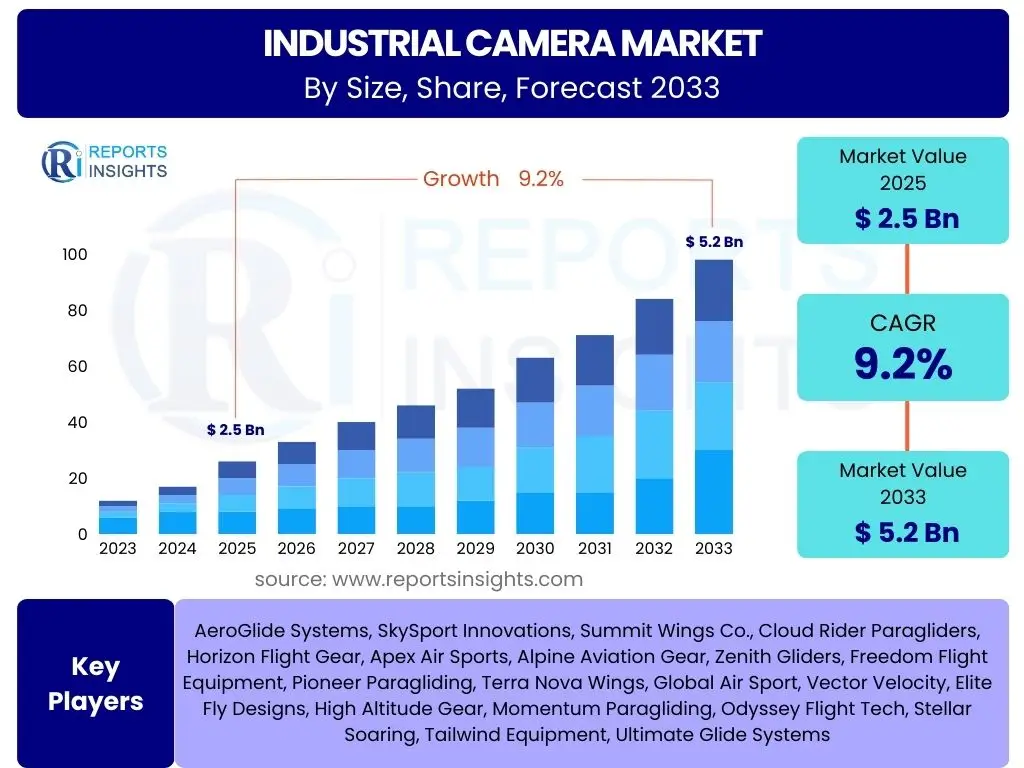

Industrial Camera Market Size

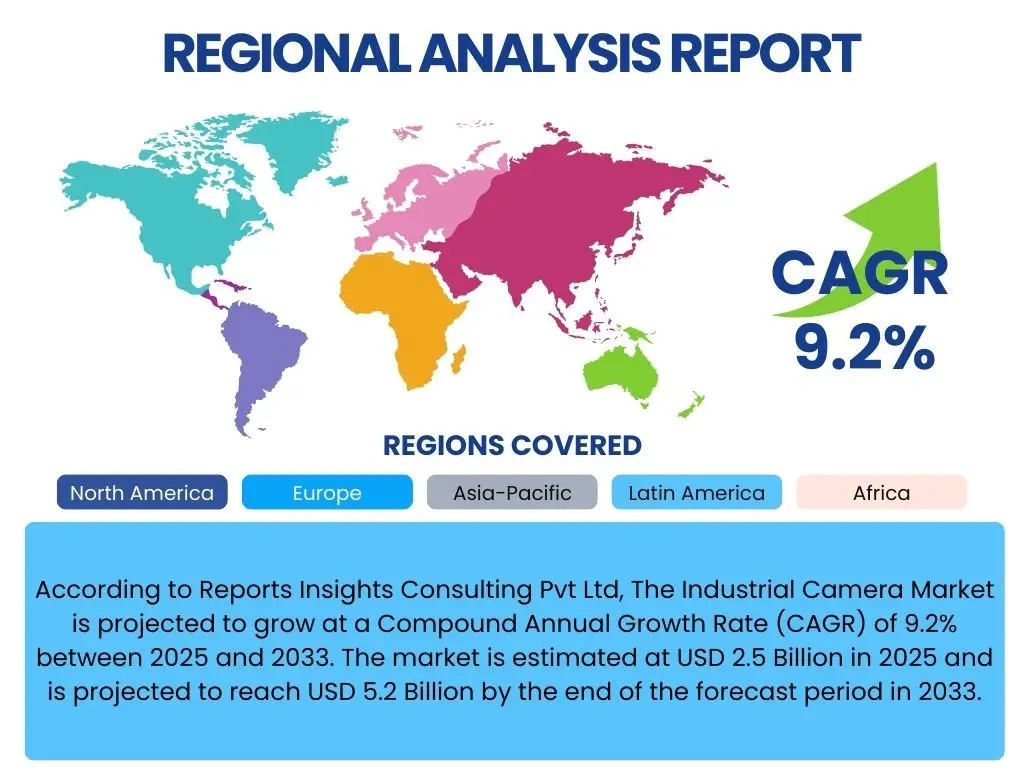

According to Reports Insights Consulting Pvt Ltd, The Industrial Camera Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.2% between 2025 and 2033. The market is estimated at USD 2.5 Billion in 2025 and is projected to reach USD 5.2 Billion by the end of the forecast period in 2033.

Key Industrial Camera Market Trends & Insights

The industrial camera market is currently experiencing a transformative phase, driven by the accelerating pace of automation and the pervasive integration of advanced technologies across diverse sectors. Users frequently inquire about the emerging technological shifts and their implications for manufacturing, quality control, and logistics. A significant trend involves the development of cameras with higher resolution, increased frame rates, and enhanced spectral capabilities, moving beyond traditional visible light to infrared, UV, and even hyperspectral imaging to provide more comprehensive data for complex industrial applications. The demand for smart cameras with embedded processing capabilities is also rising, enabling on-device analytics and reducing the need for extensive external computing infrastructure, thereby streamlining operational workflows and improving real-time decision-making. These advancements are crucial for addressing the stringent requirements of modern industrial processes, where precision and speed are paramount.

Furthermore, the market is profoundly influenced by the principles of Industry 4.0 and the Internet of Things (IoT), fostering greater connectivity and data exchange between industrial cameras and other factory systems. This interconnected ecosystem facilitates predictive maintenance, optimized resource allocation, and a more adaptive manufacturing environment. The increasing adoption of 3D vision systems, capable of providing detailed spatial data, is another pivotal trend, particularly in robotics, automated assembly, and quality inspection where depth perception is critical. Miniaturization, robust design for harsh environments, and the development of more user-friendly software interfaces are also shaping the market, making advanced vision systems more accessible and deployable across a wider range of industrial settings, from automotive manufacturing to food processing and pharmaceutical production.

- Integration of AI and Machine Learning for enhanced image analysis and decision-making.

- Rising adoption of 3D vision systems for accurate depth perception in automation.

- Development of smart cameras with embedded processing and edge computing capabilities.

- Expansion of hyperspectral and multispectral imaging for advanced material analysis.

- Increased demand for high-resolution and high-speed cameras in precision manufacturing.

- Emphasis on compact, robust, and environmentally resilient camera designs.

- Growing connectivity and interoperability within Industry 4.0 and IoT frameworks.

- Customization of camera solutions for niche industrial applications and specific tasks.

AI Impact Analysis on Industrial Camera

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is fundamentally reshaping the capabilities and applications of industrial cameras, addressing common user questions regarding automation efficiency, accuracy, and operational intelligence. AI-powered industrial cameras transcend traditional image capture and processing, offering advanced functionalities such as complex pattern recognition, anomaly detection, predictive analytics, and autonomous decision-making. This shift allows for more sophisticated quality control systems that can identify minute defects with greater accuracy and speed than human inspectors, significantly reducing production errors and waste. Furthermore, AI enables industrial cameras to learn from vast datasets, continuously improving their performance in tasks like object classification, robot guidance, and process optimization, thereby elevating the overall intelligence of manufacturing and logistics operations.

The impact of AI extends to facilitating the development of truly autonomous systems, where industrial cameras serve as the "eyes" that perceive, understand, and react to their environment in real-time. This is particularly evident in robotics, where AI-driven vision systems enable robots to perform intricate assembly tasks, navigate complex environments, and handle variable objects with unprecedented flexibility. Concerns often raised by users pertain to the computational requirements and data security challenges associated with AI. However, the emergence of edge AI, where AI algorithms are processed directly on the camera, is mitigating these concerns by reducing latency, bandwidth needs, and enhancing data privacy. This technological evolution not only boosts efficiency and productivity but also unlocks new possibilities for personalized manufacturing, advanced diagnostics, and enhanced safety protocols across various industrial domains, making AI a pivotal factor in the future trajectory of industrial camera technology.

- Enhanced precision in quality inspection and defect detection.

- Facilitation of advanced robotic guidance and autonomous navigation.

- Predictive maintenance capabilities through visual data analysis.

- Improved object recognition, classification, and tracking.

- Real-time decision-making and adaptive process control.

- Reduction of human intervention in repetitive or hazardous tasks.

- Development of self-learning vision systems for continuous improvement.

- Optimization of manufacturing workflows and resource utilization.

Key Takeaways Industrial Camera Market Size & Forecast

Analyzing common user questions regarding the core insights from the Industrial Camera market size and forecast reveals a keen interest in understanding the primary growth drivers, regions exhibiting the highest potential, and the strategic implications for businesses operating within or looking to enter this sector. A significant takeaway is the robust and sustained growth trajectory, with the market projected to more than double in value by 2033. This expansion is predominantly fueled by the global imperative for industrial automation, the proliferation of smart factories under Industry 4.0 initiatives, and the increasing demand for high-precision quality control across manufacturing, logistics, and automotive industries. Stakeholders are particularly interested in how these macro trends translate into tangible market opportunities and the critical factors that will dictate success in a rapidly evolving technological landscape.

Another crucial insight is the accelerating pace of technological innovation, particularly the symbiotic relationship between industrial cameras and artificial intelligence. AI is not merely an add-on but a fundamental enabler for advanced functionalities, transforming cameras from passive data capture devices into intelligent analytical tools. This integration is expected to be a key differentiator and a primary catalyst for market expansion. Geographically, Asia Pacific is anticipated to remain a dominant and high-growth region, driven by extensive manufacturing bases and aggressive adoption of automation technologies. For companies, a focus on developing integrated solutions that combine high-performance hardware with sophisticated AI algorithms, along with strategic investments in R&D and market penetration in emerging economies, will be essential to capitalize on the significant growth forecasted for the industrial camera market.

- The market exhibits substantial growth potential, driven by automation and Industry 4.0 adoption.

- Asia Pacific is expected to be a primary growth engine due to robust manufacturing and technological adoption.

- AI and machine learning integration are critical for future differentiation and competitive advantage.

- High-resolution, 3D, and smart camera technologies will lead product innovation.

- Increased demand for precise quality control and inspection solutions across industries.

- Strategic partnerships and mergers will be key for market expansion and technology acquisition.

Industrial Camera Market Drivers Analysis

The industrial camera market is propelled by a confluence of powerful drivers, primarily the global push towards comprehensive industrial automation and the continuous advancements in manufacturing processes. The imperative for higher efficiency, reduced operational costs, and superior product quality across various industries, including automotive, electronics, and food and beverage, necessitates the widespread adoption of automated inspection and guidance systems where industrial cameras play a pivotal role. The principles of Industry 4.0, which advocate for smart factories and interconnected production systems, further amplify this demand by creating an ecosystem where real-time data acquisition and analysis through vision systems are crucial for optimizing complex manufacturing workflows and enabling predictive maintenance strategies. This paradigm shift requires not just cameras, but intelligent vision solutions that can seamlessly integrate into advanced robotic and automated environments.

Moreover, the escalating demand for stringent quality control and metrology in precision manufacturing sectors is a significant catalyst. Industrial cameras, equipped with high resolution and sophisticated image processing capabilities, are indispensable for detecting minuscule defects, ensuring dimensional accuracy, and maintaining product integrity at every stage of production. The expansion of the robotics industry, particularly collaborative robots (cobots), also directly correlates with the growth of industrial cameras, as vision systems provide the essential guidance and perception for robots to perform complex tasks, from pick-and-place operations to intricate assembly. Additionally, the continuous innovation in sensor technology, image processing algorithms, and connectivity standards (like GigE Vision and USB3 Vision) makes industrial cameras more capable, versatile, and easier to integrate, thereby accelerating their market penetration across new and existing applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Industrial Automation and Robotics Adoption | +2.5% | Global, particularly Asia Pacific (China, Japan), Europe (Germany), North America (US) | Short to Long-term |

| Rise of Industry 4.0 and Smart Factory Initiatives | +2.0% | Global, with strong impetus in developed economies | Medium to Long-term |

| Growing Demand for Quality Control and Inspection Systems | +1.8% | Global, especially in high-value manufacturing sectors | Short to Long-term |

| Technological Advancements in Machine Vision and AI | +1.5% | Global, driven by innovation hubs (US, Germany, Japan) | Short to Medium-term |

| Expansion of Logistics and E-commerce Sectors | +1.4% | Global, strong in emerging markets and developed regions | Medium-term |

Industrial Camera Market Restraints Analysis

Despite the robust growth projections, the industrial camera market faces several significant restraints that could temper its expansion. One primary barrier is the substantial initial investment required for sophisticated industrial vision systems, which includes not only the cameras themselves but also specialized lighting, lenses, software, integration services, and training. This high upfront cost can be prohibitive for small and medium-sized enterprises (SMEs) with limited capital budgets, particularly in developing regions, thereby slowing down the broader adoption of advanced automation technologies. The perceived return on investment (ROI) may not always be immediately apparent or quickly realized, leading to hesitation among potential buyers, despite the long-term benefits in efficiency and quality.

Furthermore, the inherent technical complexity associated with integrating, configuring, and maintaining advanced industrial camera systems poses another significant restraint. Companies often lack the in-house expertise in machine vision, AI, and systems integration, necessitating reliance on external specialists or extensive employee training. This complexity can lead to longer deployment times, higher operational costs, and potential system malfunctions if not managed properly. Additionally, the rapid pace of technological obsolescence in the electronics and imaging industries means that newly installed systems can quickly become outdated, requiring frequent upgrades or replacements. This continuous need for investment and adaptation to new standards or software versions can be a financial burden. Economic uncertainties, global supply chain disruptions for critical components, and a shortage of skilled personnel capable of developing and managing these advanced systems also represent ongoing challenges that limit market growth and widespread deployment.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Setup Costs | -1.5% | Global, particularly impacting SMEs in emerging markets | Short to Medium-term |

| Technical Complexity and Integration Challenges | -1.2% | Global, especially in sectors with diverse legacy systems | Short to Medium-term |

| Lack of Skilled Workforce and Expertise | -1.0% | Global, pronounced in regions with lower automation education | Medium to Long-term |

| Rapid Technological Obsolescence | -0.8% | Global, affecting long-term investment planning | Medium-term |

Industrial Camera Market Opportunities Analysis

The industrial camera market is ripe with numerous opportunities for expansion and innovation, primarily driven by the continuous evolution of digital technologies and the broadening scope of industrial applications. A significant opportunity lies in the burgeoning adoption of AI and deep learning within vision systems. As algorithms become more sophisticated and computational power more accessible, industrial cameras can perform increasingly complex analytical tasks, opening doors for advanced predictive maintenance, intricate quality inspections, and highly adaptive robotic guidance systems that were previously unfeasible. This allows for the creation of truly intelligent vision solutions that offer superior performance and efficiency, thereby addressing critical industrial needs and creating higher value propositions for end-users. The ongoing development of embedded AI and edge computing capabilities further enhances this opportunity by enabling faster, more secure, and localized data processing, reducing latency and reliance on cloud infrastructure.

Furthermore, the expansion into new vertical markets and geographical regions presents substantial growth avenues. While traditional manufacturing remains a core segment, emerging applications in healthcare (e.g., medical diagnostics, surgical robotics), agriculture (e.g., crop monitoring, automated harvesting), defense, and smart city infrastructure (e.g., traffic management, public safety) are increasingly leveraging industrial vision technology. These sectors often require specialized camera capabilities, fostering innovation in areas like multispectral and hyperspectral imaging, thermal imaging, and high-dynamic-range imaging. Moreover, emerging economies in Asia Pacific, Latin America, and the Middle East and Africa, with their rapid industrialization and growing investments in automation infrastructure, represent untapped markets with immense potential for growth. Providing customizable, cost-effective, and easy-to-integrate solutions tailored to the specific needs of these diverse applications and regions will be key to unlocking these opportunities and sustaining long-term market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of AI and Deep Learning for Advanced Analytics | +2.0% | Global, particularly in technologically advanced economies | Short to Long-term |

| Expansion into Emerging Markets and New Verticals | +1.8% | Asia Pacific (India, Southeast Asia), Latin America, MEA | Medium to Long-term |

| Development of 3D Vision Systems for Complex Automation | +1.5% | Global, especially in automotive, aerospace, and electronics | Short to Medium-term |

| Increased Demand for Customized and Integrated Solutions | +1.2% | Global, across diverse industrial applications | Short to Long-term |

Industrial Camera Market Challenges Impact Analysis

The industrial camera market, while robust, confronts several significant challenges that could hinder its full potential. One prominent challenge is the relentless pace of technological evolution, which can lead to rapid product obsolescence. Manufacturers must constantly innovate to keep up with demands for higher resolutions, faster frame rates, advanced spectral capabilities, and seamless AI integration. This requires substantial and continuous investment in research and development, which can be a financial strain, particularly for smaller market players. Failure to adapt quickly risks losing competitive edge, as customers seek the most advanced and efficient vision solutions available. This also presents a challenge for end-users, who face pressure to upgrade existing systems frequently to leverage the latest efficiencies and capabilities, impacting their budget planning and operational continuity.

Another critical challenge revolves around data security and privacy concerns, especially as industrial cameras become more networked and integrated into IoT and cloud-based systems. The collection and transmission of vast amounts of visual data, often containing sensitive operational details, raise questions about vulnerability to cyber threats and unauthorized access. Ensuring robust cybersecurity measures and compliance with evolving data protection regulations (such as GDPR or CCPA) is paramount but adds complexity and cost to system design and deployment. Furthermore, interoperability remains a hurdle; while standards like GigE Vision and USB3 Vision exist, integrating cameras from different manufacturers with varied software platforms and existing industrial infrastructure can still be complex and time-consuming. This fragmentation can impede seamless data flow and holistic system optimization, requiring significant engineering effort. Intense competition from a growing number of established players and new entrants, coupled with price pressure, also challenges profitability and market share for industrial camera manufacturers globally.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence and Innovation Pressure | -1.0% | Global, impacts R&D investment and product lifecycles | Short to Medium-term |

| Data Security and Privacy Concerns in Networked Systems | -0.9% | Global, particularly in highly regulated industries (e.g., defense, healthcare) | Medium to Long-term |

| Interoperability and Standardization Issues | -0.8% | Global, affecting integration into diverse industrial ecosystems | Short to Medium-term |

| Intense Competition and Price Pressure | -0.7% | Global, affecting market share and profitability | Short to Long-term |

Industrial Camera Market - Updated Report Scope

This updated report provides a comprehensive and in-depth analysis of the global Industrial Camera Market, offering critical insights into its current status, historical performance from 2019 to 2023, and detailed projections through to 2033. The scope encompasses a thorough examination of market size estimations, growth drivers, restraints, opportunities, and challenges across various segments including camera type, spectrum, application, and end-use industry. Furthermore, the report delves into the geographical dynamics, highlighting key regional contributions and country-level market trends, alongside a competitive landscape analysis profiling leading market participants. It aims to furnish stakeholders with actionable intelligence to inform strategic decisions, identify lucrative growth avenues, and navigate the evolving market landscape effectively.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.5 Billion |

| Market Forecast in 2033 | USD 5.2 Billion |

| Growth Rate | 9.2% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Basler AG, FLIR Systems (Teledyne FLIR), Cognex Corporation, Teledyne DALSA, Stemmer Imaging AG, SICK AG, JAI A/S, Sony Corporation, Canon Inc., Hikvision Digital Technology Co. Ltd., Allied Vision GmbH, Baumer Holding AG, The Imaging Source Europe GmbH, IDS Imaging Development Systems GmbH, National Instruments Corporation, HIKROBOT, ADLINK Technology Inc., ISRA VISION AG (Atlas Copco), Jai A/S, Vision Components GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The industrial camera market is comprehensively segmented to provide a granular view of its diverse components and their respective market dynamics. This detailed segmentation allows for a precise understanding of where growth is most pronounced and which technologies or applications are driving this expansion. Analyzing the market across various dimensions such as camera type, spectral capabilities, specific applications, and distinct end-use industries helps to delineate the intricate web of demand and supply, enabling stakeholders to identify niche opportunities and tailor their strategies effectively. Each segment reflects unique technological requirements, operational challenges, and market maturity levels, contributing differently to the overall market landscape and future growth trajectory. This granular breakdown is crucial for robust market sizing, forecasting, and competitive analysis.

The segmentation also highlights the increasing specialization within the industrial camera domain. For instance, the demand for 3D cameras is escalating in robotics and automotive for precise guidance and inspection, while hyperspectral cameras are gaining traction in food processing and pharmaceuticals for advanced material analysis. Similarly, different end-use industries, from high-volume manufacturing to defense and healthcare, have distinct needs for resolution, speed, ruggedness, and intelligent features. Understanding these specific requirements across segments is essential for product development, market positioning, and strategic resource allocation. The interplay between these segments often creates synergistic growth opportunities, such as the combination of AI-enabled smart cameras with specific application-driven software in a particular end-use industry, driving further innovation and market penetration.

- By Type:

- Area Scan Camera: Dominant in general inspection, robotics, and logistics.

- Line Scan Camera: Essential for continuous web inspection and high-speed applications.

- 3D Camera: Crucial for volumetric measurement, pick-and-place, and advanced metrology.

- Thermal Camera: Utilized for temperature monitoring, process control, and predictive maintenance.

- Other Types: Includes X-ray, UV, and specialized scientific cameras for niche applications.

- By Spectrum:

- Visible Light: Standard imaging for human-interpretable inspection tasks.

- Infrared: Used for thermal imaging, night vision, and penetrating obscurities.

- X-Ray: For internal defect detection and non-destructive testing.

- UV: Applied in fluorescence imaging, surface inspection, and specialized material analysis.

- Hyperspectral: Advanced imaging for detailed material composition analysis and quality assessment.

- By Application:

- Quality Assurance & Inspection: Defect detection, dimensional checks, assembly verification.

- Metrology: Precision measurement and calibration.

- Identification: Barcode reading, OCR, and object recognition.

- Security & Surveillance: Access control, perimeter monitoring in industrial settings.

- Traffic Management: Vehicle detection, toll collection, traffic flow analysis.

- Process Control: Monitoring and optimizing industrial processes.

- Medical Imaging: Diagnostics, surgical guidance, laboratory automation.

- Other Applications: Includes scientific research, defense, and environmental monitoring.

- By End-Use Industry:

- Manufacturing:

- Automotive: Assembly, paint inspection, robotic guidance.

- Electronics & Semiconductors: Component inspection, wafer alignment, PCB verification.

- Food & Beverage: Quality sorting, foreign object detection, packaging inspection.

- Pharmaceutical & Chemical: Pill inspection, chemical analysis, sterile packaging.

- Metal & Machinery: Surface inspection, welding control, robotic machining.

- Logistics & Packaging: Parcel sorting, dimensioning, label inspection.

- Defense & Aerospace: UAV guidance, surveillance, quality control of components.

- Healthcare: Medical devices, diagnostics, surgical robots.

- Intelligent Transportation Systems (ITS): Traffic monitoring, enforcement, smart parking.

- Retail: Automated checkout, inventory management.

- Agriculture: Crop monitoring, automated harvesting, grading.

- Research & Development: Scientific experiments, laboratory automation.

- Manufacturing:

Regional Highlights

- North America: This region is characterized by early adoption of advanced automation technologies and significant investment in research and development, particularly in the automotive, aerospace, and electronics sectors. The United States leads in industrial camera deployment, driven by smart factory initiatives and a strong demand for high-precision manufacturing. Canada and Mexico also contribute through manufacturing and logistics growth, respectively. The region benefits from a robust innovation ecosystem and a high level of technological maturity, leading to the rapid integration of AI and 3D vision systems.

- Europe: Europe represents a mature market with a strong emphasis on Industry 4.0, particularly in countries like Germany (a hub for automation and machine vision), France, and the UK. The automotive, pharmaceutical, and food and beverage industries are key adopters of industrial cameras for quality control and process optimization. Strict regulatory standards for manufacturing and product quality further drive the demand for advanced vision systems. Eastern European countries are also emerging as significant growth areas due to increasing industrialization and investment in automation.

- Asia Pacific (APAC): APAC is the largest and fastest-growing market for industrial cameras, fueled by extensive manufacturing bases, rapid industrialization, and significant government investments in automation and smart factories. China, Japan, South Korea, and India are pivotal countries, demonstrating high adoption rates across electronics, automotive, textiles, and food processing industries. The region benefits from a large labor force increasingly augmented by automation, coupled with a strong emphasis on cost-effective yet high-performance solutions.

- Latin America: This region is experiencing steady growth in the industrial camera market, primarily driven by increasing foreign direct investment in manufacturing sectors, particularly in Brazil and Mexico. The automotive, food and beverage, and packaging industries are key contributors. While the market is less mature than in developed regions, there is a growing recognition of the benefits of automation and vision systems for improving productivity and quality, creating nascent but promising opportunities.

- Middle East and Africa (MEA): The MEA industrial camera market is in its early stages but shows significant potential, particularly in countries with diversifying economies like the UAE, Saudi Arabia, and South Africa. Investments in infrastructure, oil and gas, manufacturing, and security applications are driving demand. Government initiatives to promote industrial diversification and technological advancements are expected to accelerate the adoption of industrial cameras for various applications, including surveillance, process monitoring, and quality control in emerging manufacturing sectors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Camera Market.- Basler AG

- FLIR Systems (Teledyne FLIR)

- Cognex Corporation

- Teledyne DALSA

- Stemmer Imaging AG

- SICK AG

- JAI A/S

- Sony Corporation

- Canon Inc.

- Hikvision Digital Technology Co. Ltd.

- Allied Vision GmbH

- Baumer Holding AG

- The Imaging Source Europe GmbH

- IDS Imaging Development Systems GmbH

- National Instruments Corporation

- HIKROBOT

- ADLINK Technology Inc.

- ISRA VISION AG (Atlas Copco)

- Vision Components GmbH

Frequently Asked Questions

What is an industrial camera and how does it differ from a consumer camera?

An industrial camera is a specialized digital camera designed for use in industrial, scientific, or medical environments, built for durability, precision, and performance in harsh conditions. Unlike consumer cameras, industrial cameras prioritize robust construction, consistent image quality, high frame rates, precise synchronization, and standardized interfaces for seamless integration into machine vision systems for tasks like quality inspection, automation, and robotics.

What are the primary applications of industrial cameras?

Industrial cameras are primarily used for critical applications such as quality assurance and inspection (defect detection, dimensional measurement), metrology (precision measurement), automated identification (barcode reading, OCR), robotic guidance, security and surveillance in industrial settings, traffic management, and process control in manufacturing. They are crucial for improving efficiency, accuracy, and safety in automated systems.

How is Artificial Intelligence impacting the industrial camera market?

AI is profoundly impacting industrial cameras by enabling advanced capabilities such as intelligent defect detection, predictive maintenance, complex pattern recognition, and autonomous robotic guidance. AI-powered cameras can learn and adapt, performing more sophisticated analytical tasks directly at the edge or through cloud integration, leading to enhanced automation, increased accuracy, reduced false positives, and more intelligent decision-making in industrial processes.

Which industries are the major end-users of industrial cameras?

The major end-user industries for industrial cameras include manufacturing (automotive, electronics and semiconductors, food and beverage, pharmaceutical, metal and machinery), logistics and packaging, defense and aerospace, healthcare, intelligent transportation systems (ITS), and agriculture. These industries leverage vision systems to improve quality, automate processes, and enhance operational efficiency.

What are the key factors driving the growth of the industrial camera market?

The market's growth is primarily driven by the increasing adoption of industrial automation and robotics, the global proliferation of Industry 4.0 and smart factory initiatives, the rising demand for stringent quality control and inspection systems across manufacturing sectors, and continuous technological advancements in machine vision and AI. The expansion of e-commerce and logistics also contributes significantly to this growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted