Fluorite Market

Fluorite Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708156 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

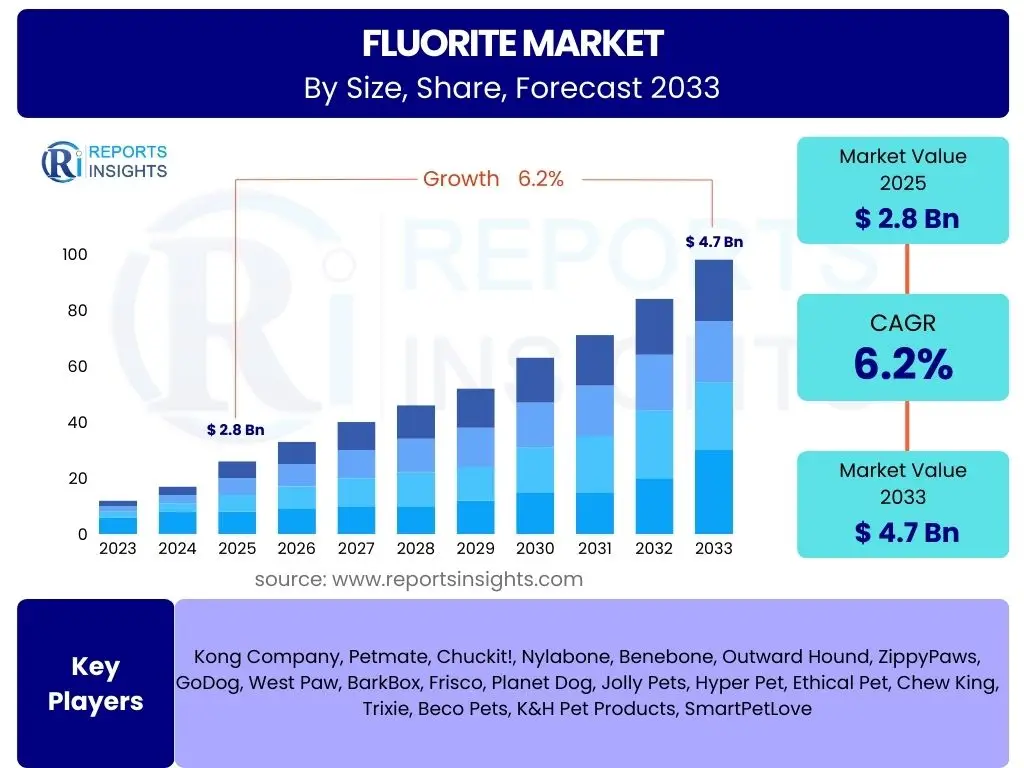

Fluorite Market Size

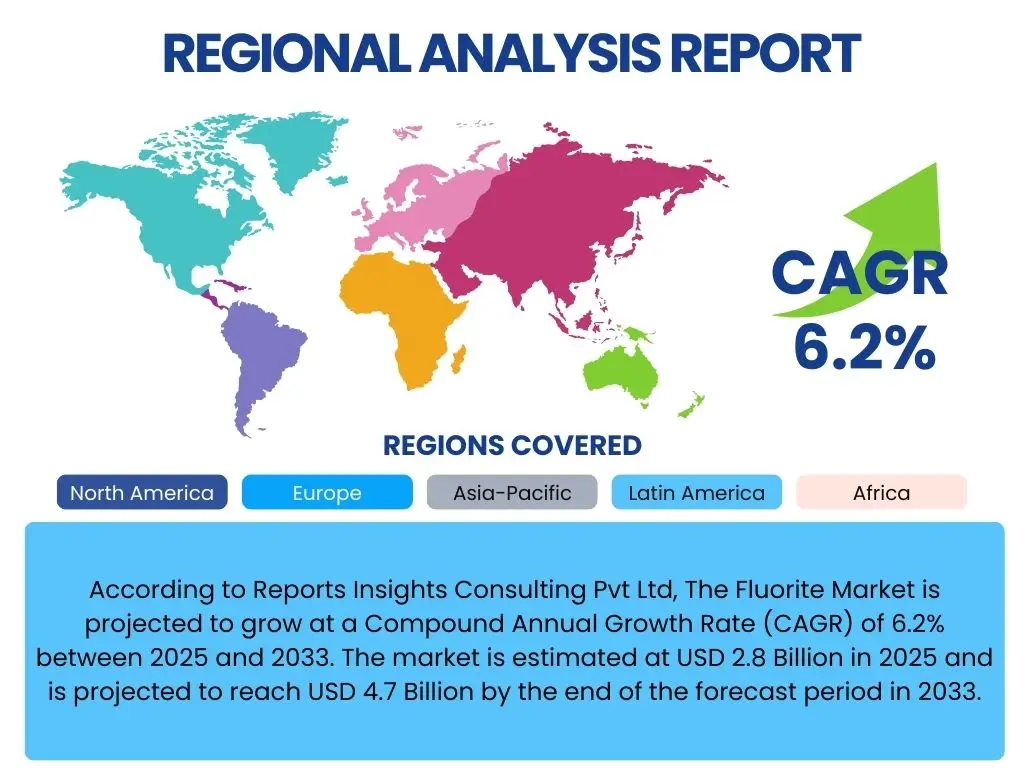

According to Reports Insights Consulting Pvt Ltd, The Fluorite Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033. The market is estimated at USD 2.8 Billion in 2025 and is projected to reach USD 4.7 Billion by the end of the forecast period in 2033.

Key Fluorite Market Trends & Insights

The global fluorite market is currently experiencing dynamic shifts driven by evolving industrial demands and increasing environmental consciousness. Key user inquiries frequently focus on how sustainability initiatives are reshaping mining practices and supply chains, alongside the growing influence of advanced materials research. There is also significant interest in understanding the regional variances in demand and supply, particularly concerning emerging industrial hubs and the impact of geopolitical factors on raw material availability.

Furthermore, the market is characterized by a drive towards higher purity fluorite grades, essential for specialized applications in electronics and advanced chemicals. Technological advancements in beneficiation processes are also gaining traction, aimed at improving extraction efficiency and reducing environmental footprint. These trends collectively underscore a market moving towards greater sophistication and responsible resource management.

- Escalating demand from the electric vehicle (EV) battery sector for lithium hexafluorophosphate production.

- Increased adoption of fluoropolymers in high-performance applications across aerospace, automotive, and medical industries.

- Growing focus on sustainable mining practices and circular economy principles to reduce environmental impact.

- Technological advancements in fluorite beneficiation to produce higher purity acid-grade fluorite.

- Geopolitical shifts impacting global supply chains and encouraging diversification of sourcing strategies.

- Expansion of the semiconductor industry, driving demand for ultra-high purity hydrofluoric acid.

AI Impact Analysis on Fluorite

User queries regarding the impact of Artificial Intelligence on the fluorite market primarily revolve around optimizing operational efficiencies, enhancing safety, and improving resource management throughout the value chain. There is keen interest in how AI can facilitate predictive maintenance in mining operations, refine mineral processing techniques, and contribute to more accurate demand forecasting, especially given the volatile nature of raw material markets. Stakeholders are also exploring AI's potential in discovering new deposits and assessing their economic viability more rapidly.

Beyond mining, AI is anticipated to play a crucial role in the downstream chemical industry, particularly in the synthesis and development of new fluorochemicals and fluoropolymers by accelerating R&D cycles and optimizing manufacturing processes. Concerns often raised include data security, the initial investment required for AI integration, and the need for a skilled workforce to manage these advanced systems. However, the overarching expectation is that AI will drive significant improvements in productivity, cost reduction, and strategic decision-making within the fluorite sector.

- Optimization of mining operations through predictive analytics for equipment maintenance and resource extraction.

- Enhanced efficiency in mineral processing and beneficiation using AI-driven control systems.

- Improved supply chain management and demand forecasting for fluorite and its derivatives.

- Acceleration of R&D in new fluorochemicals and material science through AI-powered simulations.

- Implementation of AI for environmental monitoring and compliance in mining areas, reducing ecological footprint.

- Automation of quality control processes for high-purity fluorite, critical for advanced applications.

Key Takeaways Fluorite Market Size & Forecast

User inquiries into the key takeaways from the fluorite market size and forecast consistently highlight the critical role of industrial expansion and technological innovation in driving growth. A primary insight is the sustained demand across diverse end-use sectors, particularly from the burgeoning electric vehicle and electronics industries, which require high-purity fluorite. The forecast emphasizes a stable upward trajectory, underpinned by increasing global industrialization and the indispensable nature of fluorite in various chemical processes.

Another significant takeaway is the ongoing importance of Asia Pacific as both a major consumer and producer, with emerging economies contributing substantially to market expansion. While supply chain resilience and environmental regulations present ongoing challenges, the market demonstrates adaptability through new extraction technologies and a focus on responsible sourcing. The overall outlook suggests a robust market with continuous innovation shaping its future landscape and emphasizing the value of strategic resource management.

- The fluorite market is poised for steady growth, primarily propelled by the expanding chemical and metallurgical industries.

- Asia Pacific is expected to remain the dominant region, driven by rapid industrialization and manufacturing activities.

- Demand for high-purity fluorite is increasing significantly due to its critical role in advanced technologies like EV batteries and semiconductors.

- Sustainability and environmental compliance are becoming paramount, influencing mining and processing methods.

- Price volatility due to supply-demand imbalances and geopolitical factors remains a key consideration for market participants.

- Investments in new mining projects and beneficiation technologies are crucial to meet future demand and maintain market stability.

Fluorite Market Drivers Analysis

The fluorite market's growth is predominantly fueled by an escalating demand from its diverse end-use industries. The robust expansion of aluminum production, particularly in emerging economies, significantly drives the consumption of metallurgical-grade fluorite. Concurrently, the increasing global production of steel, where fluorite acts as a fluxing agent, maintains a steady demand for the mineral. These traditional industrial applications form the foundational demand base for the market.

Furthermore, the rapid advancements in the chemical industry, particularly in the synthesis of hydrofluoric acid, fluorocarbons, and fluoropolymers, are creating substantial momentum for acid-grade fluorite. The burgeoning electric vehicle (EV) battery sector, requiring lithium hexafluorophosphate derived from fluorite, presents a novel and high-growth application. Similarly, the expanding semiconductor industry's need for ultra-high purity hydrofluoric acid for etching processes further solidifies fluorite's critical importance and acts as a strong driver for market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Aluminum Production | +1.5% | China, India, Middle East | Mid-term (2025-2029) |

| Increasing Demand for Refrigerants and Propellants | +1.0% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Expansion of Semiconductor Industry | +1.2% | South Korea, Taiwan, Japan, USA | Long-term (2025-2033) |

| Burgeoning Electric Vehicle (EV) Battery Market | +1.8% | China, Europe, USA | Long-term (2025-2033) |

| Consistent Demand from Steel Manufacturing | +0.8% | Global, particularly Asia Pacific | Mid-term (2025-2029) |

Fluorite Market Restraints Analysis

Despite robust demand, the fluorite market faces several significant restraints that could impede its growth trajectory. Stringent environmental regulations, particularly concerning mining permits, waste disposal, and emissions from processing plants, impose substantial compliance costs and often lead to operational delays or outright project cancellations. These regulations are particularly impactful in regions with rich deposits but strict environmental policies, limiting supply potential.

Furthermore, the market is susceptible to supply chain disruptions, stemming from geopolitical instability in key producing regions, trade disputes, or natural disasters. Such disruptions can lead to price volatility and uncertainty for end-users, potentially encouraging the search for alternative materials or processes. The high capital expenditure required for developing new fluorite mines and beneficiation facilities, coupled with the long lead times for project approval and construction, also acts as a significant barrier to entry and expansion, limiting the overall market's responsiveness to demand spikes.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations | -1.3% | Europe, North America, China | Long-term (2025-2033) |

| Supply Chain Disruptions and Geopolitical Risks | -1.0% | Global | Mid-term (2025-2029) |

| High Capital Costs for New Mining Projects | -0.7% | Global | Long-term (2025-2033) |

| Potential Substitution by Alternative Materials in Niche Applications | -0.5% | Select Industries, e.g., Steel | Long-term (2025-2033) |

| Price Volatility of Raw Fluorite | -0.8% | Global | Short to Mid-term (2025-2027) |

Fluorite Market Opportunities Analysis

The fluorite market is rich with opportunities stemming from technological advancements and evolving industrial landscapes. A primary opportunity lies in the development of advanced fluoropolymers and specialty fluorochemicals, which are finding new applications in high-tech sectors such as aerospace, medical devices, and renewable energy. These applications often require high-purity fluorite and command premium prices, offering avenues for market expansion and value creation.

Moreover, the increasing global focus on energy efficiency and sustainability presents opportunities for fluorite in the production of next-generation refrigerants with lower global warming potential (GWP) and in various green technologies. The exploration and development of new fluorite deposits, particularly in underexplored regions, could significantly bolster supply security and reduce dependence on a few dominant sources. Furthermore, advancements in recycling technologies for fluorine-containing materials offer a long-term opportunity to create a more circular economy for fluorite, reducing reliance on primary extraction and enhancing resource efficiency.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Fluoropolymers | +1.4% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Increasing Demand for Specialty Fluorochemicals | +1.1% | Global | Mid-term (2025-2029) |

| Exploration of New Fluorite Deposits | +0.9% | Africa, Latin America, Central Asia | Long-term (2028-2033) |

| Advancements in Fluorine Recycling Technologies | +0.7% | Europe, Japan, USA | Long-term (2028-2033) |

| Growing Investment in Green Technologies | +1.0% | Global | Mid-term (2025-2029) |

Fluorite Market Challenges Impact Analysis

The fluorite market faces several inherent challenges that require strategic navigation for sustained growth. One significant challenge is the inherent price volatility of raw fluorite, which is influenced by factors such as global supply-demand imbalances, inventory levels, and speculative trading. This unpredictability complicates long-term planning for both producers and consumers, affecting investment decisions and profitability margins across the value chain.

Another critical challenge is the energy intensity of fluorite processing, particularly for producing higher-grade materials. The high energy consumption contributes significantly to operational costs and environmental footprint, especially with fluctuating energy prices and increasing pressure for decarbonization. Furthermore, the fluorite mining sector often grapples with labor shortages and the need for specialized skills, particularly in remote mining locations. This can impact operational efficiency and drive up labor costs. Public opposition to new mining projects due to environmental concerns or land-use conflicts also poses a substantial challenge, often leading to protracted approval processes and limiting the development of new supply sources.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Price Fluctuations and Market Volatility | -1.1% | Global | Short to Mid-term (2025-2028) |

| Energy Intensity of Processing | -0.9% | Global | Long-term (2025-2033) |

| Labor Shortages and Skilled Workforce Requirements | -0.6% | Major Mining Regions | Mid-term (2025-2029) |

| Public Opposition to New Mining Projects | -0.7% | North America, Europe | Long-term (2028-2033) |

| Management of Mining Waste and Tailings | -0.5% | Global | Mid-term (2025-2029) |

Fluorite Market - Updated Report Scope

This market insights report offers an exhaustive analysis of the global fluorite market, encompassing a detailed examination of market size, growth trends, drivers, restraints, opportunities, and challenges. The scope includes a thorough segmentation analysis by various factors such as type, application, and end-use industry, providing a granular view of market dynamics. Furthermore, a comprehensive regional breakdown is provided, highlighting key geographical markets and their specific contributions to the overall industry landscape, along with a competitive analysis of leading market players.

The report aims to equip stakeholders with actionable intelligence for strategic decision-making, offering future projections and insights into emerging trends that are poised to reshape the industry. It covers historical data to establish a robust baseline, extending into a comprehensive forecast period to project future market performance and identify key areas of growth and potential disruption.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.8 Billion |

| Market Forecast in 2033 | USD 4.7 Billion |

| Growth Rate | 6.2% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Fluorine Corporation, Fluorspar Mining Group, Chemical Solutions Inc., Industrial Minerals Ltd., Mining Innovations Corp., Advanced Fluorine Products, Resource Holdings LLC, Mineral Processing Enterprises, Specialty Chemicals Group, Precision Fluorite Producers, New Century Materials, Green Mineral Resources, Zenith Mining Solutions, Core Chemical Holdings, United Fluorine Systems, Stellar Resources Inc., Apex Mineral Works, Delta Chemical Producers, Horizon Materials Group, Phoenix Fluorite Corp. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The fluorite market is intricately segmented to provide a granular understanding of its diverse applications and demands. This segmentation allows for a detailed analysis of specific market niches, enabling stakeholders to identify key growth areas and tailor strategies effectively. The primary segmentation distinguishes between various grades of fluorite, each catering to different industrial purity requirements and processing methods, which fundamentally dictates its end-use application.

Further breakdowns consider the specific applications where fluorite is utilized, ranging from heavy industries like steel and aluminum production to highly specialized sectors such as electronics and electric vehicle battery manufacturing. Additionally, the market is analyzed based on end-use industries, providing insight into which sectors are driving the most significant demand and where future growth is anticipated. This multi-faceted segmentation ensures a comprehensive view of the fluorite value chain and its contribution across the global industrial landscape.

- By Type: Acid Grade Fluorite, Metallurgical Grade Fluorite, Ceramic Grade Fluorite.

- By Application: Aluminum Production, Steel Manufacturing, Chemical Industry (Hydrofluoric Acid, Fluorocarbons, Fluoropolymers, Other Fluorine Chemicals), Cement Production, Optics, Refrigerants, Electric Vehicle Batteries, Others.

- By End-use Industry: Automotive, Construction, Electronics & Semiconductors, Chemical & Petrochemical, Metallurgy, Aerospace & Defense, Energy, Pharmaceutical, Others.

- By Form: Powder, Lumps.

Regional Highlights

- North America: This region demonstrates stable demand, driven by well-established chemical, automotive, and aerospace industries. Emphasis is placed on specialty fluorochemicals and high-purity applications, with increasing investment in domestic mining and recycling initiatives to enhance supply security and reduce import dependency. The United States and Canada are key markets, focusing on advanced manufacturing and environmental technologies.

- Europe: Characterized by stringent environmental regulations and a strong focus on sustainable practices, Europe is a significant consumer of fluorite for its advanced chemical, automotive, and electronics sectors. There is a growing push for fluorine recycling and the development of eco-friendly fluorochemicals. Germany, France, and the UK are major contributors to regional demand, alongside efforts to diversify sourcing.

- Asia Pacific (APAC): The largest and fastest-growing market for fluorite, APAC's expansion is fueled by rapid industrialization, burgeoning manufacturing capabilities, and significant investments in infrastructure. China and India are major consumers in steel and aluminum production, while South Korea, Taiwan, and Japan lead in semiconductor and EV battery applications. The region is both a primary producer and consumer, influencing global supply-demand dynamics.

- Latin America: Possessing significant fluorite reserves, countries like Mexico and Brazil are key producers. The region's demand is primarily driven by domestic industrial growth, particularly in metallurgy and construction. Exports to North America and Asia Pacific are crucial, with potential for increased investment in mining and processing infrastructure.

- Middle East and Africa (MEA): This region offers considerable potential for fluorite production and consumption. The Middle East's expanding petrochemical and aluminum industries drive demand, while certain African nations hold substantial untapped fluorite deposits. Investment in mining projects and infrastructure development is a key area for future growth and market influence.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Fluorite Market.- Global Fluorine Corporation

- Fluorspar Mining Group

- Chemical Solutions Inc.

- Industrial Minerals Ltd.

- Mining Innovations Corp.

- Advanced Fluorine Products

- Resource Holdings LLC

- Mineral Processing Enterprises

- Specialty Chemicals Group

- Precision Fluorite Producers

- New Century Materials

- Green Mineral Resources

- Zenith Mining Solutions

- Core Chemical Holdings

- United Fluorine Systems

- Stellar Resources Inc.

- Apex Mineral Works

- Delta Chemical Producers

- Horizon Materials Group

- Phoenix Fluorite Corp.

Frequently Asked Questions

What is fluorite and its primary uses?

Fluorite, also known as fluorspar, is a mineral composed of calcium fluoride (CaF2). Its primary uses include being a flux in steelmaking, an opacifier in ceramics, and the essential source for hydrofluoric acid (HF) production. HF is critical for manufacturing fluorocarbons, fluoropolymers, aluminum, and in the electronics industry.

Which industries drive the demand for fluorite?

Key industries driving fluorite demand are the chemical industry (for refrigerants, polymers, and specialty chemicals), steel manufacturing, aluminum production, and more recently, the electric vehicle (EV) battery sector due to its use in lithium hexafluorophosphate production. The semiconductor industry also demands high-purity fluorite derivatives.

What are the main grades of fluorite, and how do they differ?

The main grades are metallurgical grade (metspar, typically 60-85% CaF2) used as a flux in steel and cement; ceramic grade (85-95% CaF2) used in glass and ceramics; and acid grade (acidspar, 97% or more CaF2) which is the highest purity grade and essential for producing hydrofluoric acid and advanced fluorochemicals.

Where are the major fluorite reserves and production centers globally?

Major fluorite reserves are predominantly found in China, Mexico, Mongolia, South Africa, and Russia. China is currently the largest global producer, followed by Mexico, contributing significantly to the world's supply. Other notable producing regions include Europe and parts of Africa.

What are the environmental concerns related to fluorite mining and processing?

Environmental concerns include land disturbance, water pollution from mining activities and tailings ponds, potential release of fluoride into local ecosystems, and energy consumption during beneficiation. Strict regulations are increasingly being implemented to mitigate these impacts, driving efforts towards more sustainable mining and processing methods.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted