Veneer and Plywood Market

Veneer and Plywood Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708112 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Veneer and Plywood Market Size

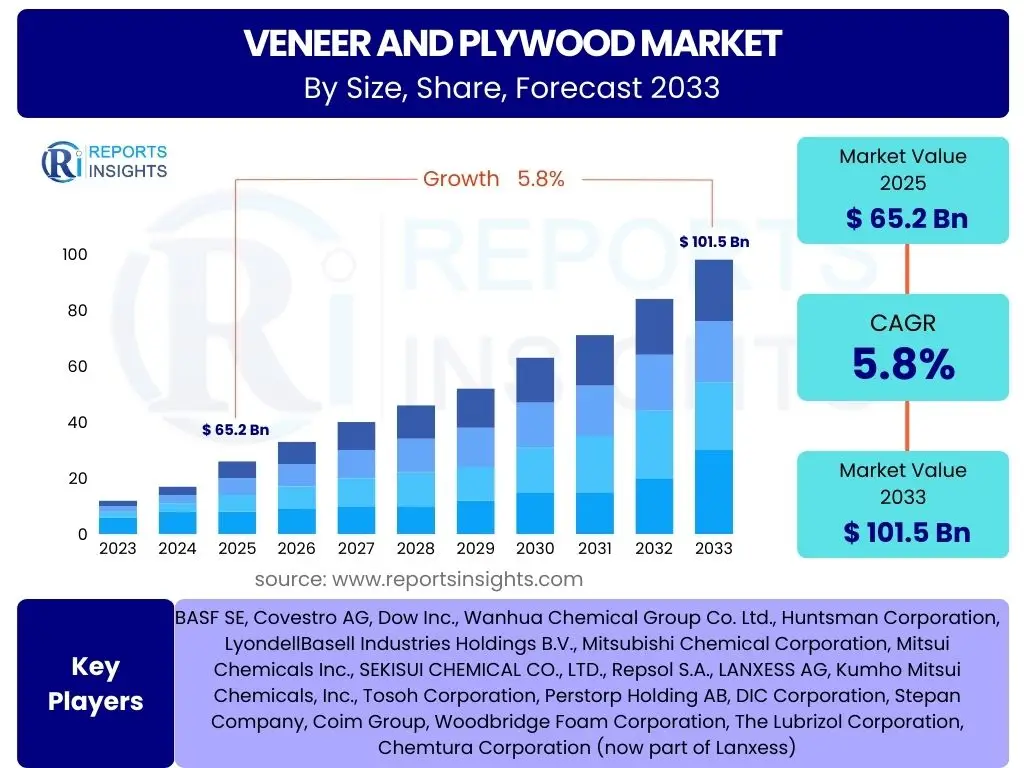

According to Reports Insights Consulting Pvt Ltd, The Veneer and Plywood Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 65.2 Billion in 2025 and is projected to reach USD 101.5 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily fueled by increasing demand from the construction and furniture sectors globally, alongside a growing preference for sustainable and engineered wood products. The market's expansion is further supported by urbanization trends and rising disposable incomes in emerging economies.

The consistent growth forecast reflects the enduring utility and versatility of veneer and plywood in various applications, ranging from structural elements to decorative finishes. While traditional markets in North America and Europe continue to show stable demand, significant acceleration is anticipated in the Asia Pacific region due to rapid infrastructure development and burgeoning residential construction. Innovation in manufacturing processes, including the development of eco-friendly adhesives and fire-retardant panels, is also contributing to market expansion by enhancing product performance and safety.

Key Veneer and Plywood Market Trends & Insights

The Veneer and Plywood market is currently experiencing dynamic shifts driven by evolving consumer preferences, technological advancements, and a heightened focus on environmental sustainability. Users frequently inquire about the integration of sustainable practices, the impact of customization demands, and the adoption of new materials or manufacturing techniques. These inquiries highlight a collective interest in understanding how the industry is adapting to modern challenges and opportunities, particularly in light of global environmental concerns and the pursuit of enhanced product performance and aesthetic appeal.

A significant trend observed is the growing demand for engineered wood products that offer superior strength, stability, and environmental benefits compared to traditional solid wood. This includes products made from sustainably sourced timber and those utilizing low-VOC (Volatile Organic Compound) adhesives, addressing both performance requirements and ecological concerns. The market is also seeing increased application of digital tools in design and production, facilitating greater customization and reducing material waste, thereby meeting specific architectural and design needs more efficiently.

Furthermore, the aesthetic appeal of natural wood grains remains a dominant factor, driving demand for high-quality veneers in interior design and furniture manufacturing. There is a discernible shift towards lightweight and durable plywood solutions for various structural and non-structural applications, including modular construction and vehicle interiors. This emphasis on both functionality and environmental responsibility is reshaping product development and market strategies across the industry.

- Increased adoption of sustainable and eco-friendly wood products, including FSC-certified materials.

- Growing demand for customized veneer and plywood solutions in architectural and interior design.

- Integration of advanced manufacturing technologies for enhanced precision and efficiency.

- Shift towards lightweight, high-strength plywood in construction and transportation sectors.

- Rising popularity of decorative veneers for premium furniture and interior finishes.

- Emphasis on low-VOC adhesives and formaldehyde-free products for improved indoor air quality.

AI Impact Analysis on Veneer and Plywood

User inquiries concerning AI's influence on the Veneer and Plywood industry predominantly center around its potential to revolutionize manufacturing processes, enhance product quality, and optimize supply chain operations. Common questions include how AI can improve material utilization, reduce waste, and provide predictive insights into machinery maintenance. These questions underscore a clear interest in AI's capacity to drive efficiency gains, foster innovation, and address critical industry challenges such as raw material scarcity and fluctuating market demands.

Artificial Intelligence is poised to significantly transform several aspects of the Veneer and Plywood market. In manufacturing, AI-powered computer vision systems are enabling highly accurate quality inspection of veneers and plywood panels, identifying defects such as knots, cracks, or inconsistencies in grain patterns with greater precision and speed than human inspection. This leads to higher product quality, reduced waste, and optimized material usage, directly contributing to cost savings and improved resource management. Furthermore, AI algorithms are being deployed to optimize cutting patterns and veneer peeling processes, maximizing yield from raw logs.

Beyond the factory floor, AI's impact extends to supply chain management and demand forecasting. Predictive analytics, driven by AI, can analyze historical sales data, market trends, and external factors to forecast demand more accurately, allowing manufacturers to optimize inventory levels and production schedules. This reduces lead times, minimizes storage costs, and enhances responsiveness to market fluctuations. Additionally, AI-driven solutions are assisting in predictive maintenance of machinery, reducing downtime and extending equipment lifespan, thereby improving overall operational efficiency and reducing unexpected repair costs.

- Enhanced quality control and defect detection through AI-powered computer vision systems.

- Optimized raw material utilization and cutting patterns to maximize yield.

- Improved production scheduling and operational efficiency through predictive analytics.

- Advanced demand forecasting and supply chain optimization, reducing waste and inventory costs.

- Predictive maintenance for manufacturing machinery, minimizing downtime and extending equipment life.

- Automation of grading and sorting processes for increased speed and consistency.

Key Takeaways Veneer and Plywood Market Size & Forecast

The analysis of user questions regarding the Veneer and Plywood market size and forecast reveals a strong emphasis on understanding the primary growth drivers, the impact of sustainability on market trajectory, and the geographical distribution of market expansion. Users are keen to identify the most significant factors contributing to market growth and how these factors might evolve over the forecast period. There is also considerable interest in discerning the long-term viability and resilience of the industry amidst global economic shifts and changing consumer preferences.

A key takeaway is the robust and sustained growth projected for the Veneer and Plywood market, driven largely by continued expansion in the global construction and furniture manufacturing industries. The market's resilience is underscored by its ability to adapt to evolving environmental regulations and consumer demands for eco-friendly products, which are increasingly becoming a standard rather than a niche requirement. This adaptation includes the development of innovative engineered wood products and the adoption of more sustainable sourcing practices.

Furthermore, the Asia Pacific region is expected to remain the dominant and fastest-growing market, propelled by rapid urbanization, substantial infrastructure investments, and a burgeoning middle class driving demand for residential and commercial construction. While traditional markets in North America and Europe will continue to contribute steadily, the dynamism of emerging economies will largely shape the global market's expansion. The ongoing diversification of applications for veneer and plywood, from interior design to specialized industrial uses, further solidifies its market position and offers diverse avenues for future growth.

- Consistent market growth projected at a CAGR of 5.8%, reaching USD 101.5 Billion by 2033.

- Strong demand from the construction, furniture, and interior design sectors as primary growth catalysts.

- Sustainability and eco-friendly product development are pivotal for future market competitiveness.

- Asia Pacific remains the leading and fastest-growing region due to rapid infrastructure development and urbanization.

- Technological advancements in manufacturing and material science are enhancing product quality and versatility.

- The market is resilient, adapting to global economic shifts and consumer preferences for durable and aesthetically pleasing wood products.

Veneer and Plywood Market Drivers Analysis

The Veneer and Plywood market is significantly propelled by several key drivers that reflect global economic and demographic trends. Foremost among these is the escalating demand from the construction and real estate sectors, particularly in rapidly urbanizing regions. As populations grow and infrastructure develops, the need for residential, commercial, and industrial buildings directly translates into increased consumption of wood-based panels. This driver is further amplified by government investments in public infrastructure projects and a global trend towards aesthetic and durable interior finishes.

Another crucial driver is the burgeoning furniture industry, where veneer and plywood are fundamental components due to their versatility, cost-effectiveness, and aesthetic appeal. The rising disposable incomes globally, coupled with a preference for modern, modular, and customizable furniture, are fueling this demand. Additionally, the growing awareness and preference for sustainable and engineered wood products are acting as a significant catalyst, as these materials offer improved performance characteristics and a reduced environmental footprint compared to traditional solid wood options. These factors collectively contribute to the robust expansion of the market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Construction & Real Estate Sector | +1.5% | Global, particularly APAC (China, India), North America | Long-term (5+ years) |

| Increasing Demand for Furniture & Interior Design | +1.2% | Global, especially Europe, North America, APAC | Medium-term (3-5 years) |

| Rising Preference for Engineered Wood Products | +1.0% | Global, particularly developed economies | Long-term (5+ years) |

| Urbanization & Infrastructure Development | +0.8% | Emerging Economies (APAC, Latin America, MEA) | Long-term (5+ years) |

| Versatility & Cost-Effectiveness over Solid Wood | +0.7% | Global | Ongoing |

Veneer and Plywood Market Restraints Analysis

Despite its growth potential, the Veneer and Plywood market faces several significant restraints that could temper its expansion. One of the primary concerns is the volatility in raw material prices, particularly for timber. Fluctuations in timber supply, often influenced by environmental factors, weather patterns, and logging regulations, can lead to unpredictable production costs and impact profit margins for manufacturers. This unpredictability makes long-term planning and pricing strategies challenging, potentially affecting market stability and investment.

Another key restraint involves increasing environmental regulations and concerns regarding deforestation. Governments globally are implementing stricter policies on logging, forest management, and trade of wood products, aiming to combat illegal logging and promote sustainable forestry. While necessary for ecological balance, these regulations can limit raw material availability, increase compliance costs for manufacturers, and necessitate significant shifts in sourcing strategies. Additionally, the availability and competitive pricing of alternative materials, such as plastics, metals, and composite boards, present a challenge by offering consumers a broader range of choices that may sometimes be more cost-effective or suitable for specific applications.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices (Timber) | -1.0% | Global, especially Southeast Asia, Europe, North America | Short-term to Medium-term (1-5 years) |

| Stringent Environmental Regulations & Deforestation Concerns | -0.8% | Europe, North America, key timber-producing regions | Long-term (5+ years) |

| Availability of Alternative Building Materials | -0.7% | Global | Ongoing |

| Health Concerns Related to VOC Emissions from Adhesives | -0.5% | Developed Economies (Europe, North America) | Medium-term (3-5 years) |

Veneer and Plywood Market Opportunities Analysis

The Veneer and Plywood market presents numerous opportunities for growth and innovation, driven by evolving consumer demands and technological advancements. A significant opportunity lies in the burgeoning demand for engineered wood products (EWPs), which offer superior performance characteristics, sustainability benefits, and design flexibility over traditional wood. These products cater to modern construction practices requiring high strength-to-weight ratios, dimensional stability, and efficient resource utilization, thus expanding the application scope for wood-based panels.

Another promising avenue is the continuous innovation in adhesive technologies and manufacturing processes. The development of formaldehyde-free or low-VOC adhesives addresses growing environmental and health concerns, opening doors to new markets and applications, particularly in residential and interior spaces where air quality is paramount. Furthermore, the expansion into new and specialized applications, such as in the automotive, marine, and aerospace industries, where lightweight and durable materials are highly valued, offers significant market diversification potential. Untapped potential in emerging economies, driven by rapid urbanization and rising disposable incomes, also represents a substantial opportunity for market players seeking geographical expansion and new consumer bases.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Engineered Wood Products | +1.3% | Global, especially North America, Europe, APAC | Long-term (5+ years) |

| Innovation in Adhesive Technologies (Low-VOC, Formaldehyde-Free) | +1.0% | Developed Economies (Europe, North America) | Medium-term (3-5 years) |

| Expansion into New Application Areas (Automotive, Marine) | +0.9% | Global, specialized industries | Long-term (5+ years) |

| Untapped Potential in Emerging Economies | +0.8% | APAC, Latin America, MEA | Long-term (5+ years) |

| Customization and Design Flexibility for Niche Markets | +0.6% | Global | Medium-term (3-5 years) |

Veneer and Plywood Market Challenges Impact Analysis

The Veneer and Plywood market encounters several formidable challenges that require strategic responses from industry players. One significant challenge is the increasing intensity of competition, leading to price sensitivity and pressure on profit margins. The market is fragmented with numerous regional and global players, making differentiation and brand loyalty difficult without significant innovation or cost advantages. This competitive landscape often results in aggressive pricing strategies, particularly in commodity-grade plywood products.

Another critical challenge is maintaining compliance with a growing array of stringent quality and environmental standards. As consumer awareness about product safety and sustainability increases, regulatory bodies in various countries are implementing stricter rules regarding formaldehyde emissions, responsible sourcing, and material composition. Meeting these standards often requires substantial investment in R&D, new manufacturing processes, and certification, adding to operational complexities and costs. Furthermore, supply chain disruptions, stemming from geopolitical events, natural disasters, or global health crises, can severely impact the availability of raw materials and finished products, leading to production delays and increased logistical expenses, thereby posing a constant threat to market stability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Price Sensitivity | -0.9% | Global | Ongoing |

| Adherence to Stringent Quality and Environmental Standards | -0.7% | Developed Economies, Global Trade | Long-term (5+ years) |

| Supply Chain Disruptions (Raw Material & Logistics) | -0.6% | Global | Short-term to Medium-term (1-5 years) |

| Skilled Labor Shortages in Manufacturing | -0.5% | Developed Economies | Medium-term (3-5 years) |

Veneer and Plywood Market - Updated Report Scope

This report provides a comprehensive analysis of the global Veneer and Plywood market, offering in-depth insights into market dynamics, segmentation, regional trends, and competitive landscape. It covers historical performance, current market status, and future projections, aiming to equip stakeholders with critical information for strategic decision-making. The scope encompasses detailed examination of market drivers, restraints, opportunities, and challenges, along with the impact of emerging technologies like AI and the growing importance of sustainability across the industry value chain. The study's robust methodology ensures accurate and actionable market intelligence.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 65.2 Billion |

| Market Forecast in 2033 | USD 101.5 Billion |

| Growth Rate | 5.8% CAGR |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Greenply Industries, Century Plyboards, UPM-Kymmene Oyj, SVEZA, Boise Cascade Company, Weyerhaeuser Company, Georgia-Pacific LLC, Huber Engineered Woods LLC, Louisiana-Pacific Corporation, Roseburg Forest Products, PotlatchDeltic Corporation, Columbia Forest Products, Atlantic Plywood Corporation, Murphy Plywood Company, Garnica Plywood, Arauco, Linyi Guosen Wood Co. Ltd., Samling Global Limited, Rimbunan Hijau Group, Holdings LLC |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global Veneer and Plywood market is comprehensively segmented to provide granular insights into its diverse components and applications. This segmentation is crucial for understanding specific market dynamics, identifying growth opportunities within niche categories, and formulating targeted business strategies. The primary segmentation categories include Type, Product, Application, and End-use, each further broken down into sub-segments reflecting the variety and complexity of the market offerings. This detailed breakdown allows for a precise evaluation of market performance across different product categories and usage scenarios.

The segmentation by Type distinguishes between Plywood and Veneer, which are fundamental product forms with distinct characteristics and applications. Product segmentation elaborates on these, including Softwood Plywood, Hardwood Plywood, Engineered Wood Veneer, Decorative Veneer, and Structural Plywood, reflecting variations in material composition, manufacturing, and intended functionality. Application-based segmentation highlights key usage areas such as Furniture & Cabinetry, Construction, Interior Decoration, Packaging, and specialized sectors like Automotive & Marine, illustrating the broad utility of these materials across industries. Finally, End-use segmentation categorizes demand into Residential, Commercial, and Industrial sectors, offering insights into consumer and business-to-business consumption patterns.

- By Type: Plywood, Veneer

- By Product: Softwood Plywood, Hardwood Plywood, Engineered Wood Veneer, Decorative Veneer, Structural Plywood

- By Application: Furniture & Cabinetry, Construction (Flooring, Wall Paneling, Roofing), Interior Decoration, Packaging, Automotive & Marine, Others (e.g., Musical Instruments, Sports Equipment)

- By End-use: Residential, Commercial, Industrial

Regional Highlights

- Asia Pacific (APAC): Dominates the global market and is projected to exhibit the fastest growth. This is primarily due to rapid urbanization, extensive infrastructure development projects, and a thriving construction sector in countries like China, India, and Southeast Asian nations. Rising disposable incomes also fuel demand for residential and commercial spaces, as well as furniture.

- North America: Represents a mature market characterized by stable demand from the residential construction and renovation sectors. Strong economic growth and consumer spending on home improvements drive consistent market activity, particularly in the United States and Canada.

- Europe: A significant market driven by high aesthetic standards in interior design, robust furniture manufacturing, and stringent environmental regulations promoting sustainable wood products. Countries such as Germany, the UK, and France are key contributors, focusing on innovative and eco-friendly solutions.

- Latin America: Expected to show steady growth, fueled by increasing investment in infrastructure and a growing housing sector in countries like Brazil and Mexico. Economic development and urbanization are key factors influencing market expansion.

- Middle East and Africa (MEA): Emerging as a promising market with significant opportunities, particularly in the GCC countries due to ambitious construction projects, diversification efforts away from oil, and a growing tourism sector. South Africa also contributes to regional demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Veneer and Plywood Market.- Greenply Industries

- Century Plyboards

- UPM-Kymmene Oyj

- SVEZA

- Boise Cascade Company

- Weyerhaeuser Company

- Georgia-Pacific LLC

- Huber Engineered Woods LLC

- Louisiana-Pacific Corporation

- Roseburg Forest Products

- PotlatchDeltic Corporation

- Columbia Forest Products

- Atlantic Plywood Corporation

- Murphy Plywood Company

- Garnica Plywood

- Arauco

- Linyi Guosen Wood Co. Ltd.

- Samling Global Limited

- Rimbunan Hijau Group

- Holdings LLC

Frequently Asked Questions

What is the projected growth rate for the Veneer and Plywood market?

The Veneer and Plywood market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, reaching an estimated value of USD 101.5 Billion by 2033.

What are the primary drivers for the Veneer and Plywood market's growth?

Key drivers include robust demand from the global construction and real estate sectors, the expanding furniture and interior design industries, increasing preference for engineered wood products, and rapid urbanization, especially in emerging economies.

How is sustainability influencing the Veneer and Plywood industry?

Sustainability is a major trend, driving demand for eco-friendly products, sustainably sourced timber (e.g., FSC-certified), and low-VOC/formaldehyde-free adhesives. Manufacturers are increasingly adopting greener practices to meet environmental regulations and consumer preferences.

What role does technology, like AI, play in the Veneer and Plywood market?

AI is transforming the industry through enhanced quality control (computer vision), optimized material utilization, predictive maintenance for machinery, and advanced demand forecasting. These applications improve efficiency, reduce waste, and boost overall productivity.

Which geographical regions are expected to show the most significant growth?

The Asia Pacific (APAC) region is expected to be the dominant and fastest-growing market, driven by rapid urbanization, substantial infrastructure investments, and a burgeoning construction sector in countries such as China and India.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted